Principles of Finance with Excel (Основы финансов c Excel)

Подождите немного. Документ загружается.

PFE Chapter 19, Capital structure and valuation page 63

12. XYZ Corp. is about to borrow $100,000. The terms of the loan specify an annual

equal repayment of principal in each of the next 8 years. The loan rate is r

D

= 8%, and

XYZ has a corporate tax rate of T

C

= 40%. If the loan interest is an expense for tax

purposes for XYZ, and if there are no other taxes besides corporate taxes, what will be the

increase in XYZ’s market value?

13. Go back to the exercise of buying the turfing machine (Section 20.3). Repeat the

exercise assuming the loan is repaid in 10 equal payments. What is the NPV of the

investment now?

14.

14.a. According to a recent tax reform in Lower Fantasia, the personal tax rate on

all ordinary income except capital gains from stocks was changed from 0% to 25%.

Capital gains will henceforth be taxed at 15%. The Lower Fantasia corporate tax

rate remains unchanged at 40%. Assuming you plan to take a loan, what will be

better – to borrow using your firm or take a personal loan? Show the net advantage

of corporate debt in this case.

14.b. Will your answer to 14.a. change if the corporate tax rate becomes 20%?

15.

15.a. Eddy, from Exercise 5, needs your help again. He didn’t purchase the firm

since the bank didn’t approved him the loan, but now his dad is willing to step in

and help him by loaning him the same amount ($300,000). In addition, after the

PFE Chapter 19, Capital structure and valuation page 64

recent elections he’s now facing a personal tax rate of 40% (equal to the corporate

tax rate) and a 15% tax on equity income. What should he do – finance the

purchase using a firm or take a personal loan? Calculate the total amount received

by the stakeholders (shareholders and debt holders).

15.b. Assuming Eddy purchases the firm next door using his own firm, calculate

the value of the firm, his cost of equity and the WACC (assume his unlevered

discount rate is 12%).

16. Assume that the corporate tax rate is T

C

= 30%, the equity income tax rate is T

E

= 10%.

What is the ordinary income tax rate T

D

for which an investor will be indifferent between

choosing a personal loan or a loan using a firm?

17.

17.a. Repeat exercise 11 (Oxford Corporation) assuming the ordinary income tax

rate is T

D

= 34% and the personal equity tax rate is T

E

= 15%.

17.b. For this case calculate the “net advantage of corporate debt” and calculate the

expression

()

(

)

(

)

()

111

1

DEC

D

TTT

T

T

−−− −

=

−

.

18. You are interested in buying a machine that will produce sales of $50,000 in each of

the next six years. The machine costs $120,000 and has a six year life. It is straight line

depreciated to a zero salvage value. In addition, the machine activity costs $18,000

annually. The discount rate you decided to use for the machine’s FCF is 12%.

PFE Chapter 19, Capital structure and valuation page 65

You are considering taking a 9%, six-year, loan to finance the purchase of the

machine. The loan amount will be $70,000. The loan terms specify annual payments of

interest only in years 1-5 and the repayment of the whole principal in year 6. Assuming

that the corporate tax rate is T

C

= 40%, the personal tax rate (on ordinary income) is T

D

=

22% and the equity tax rate is T

E

= 15%, answer the following:

18.a. What is the machine FCF?

18.b. What is the NPV of the machine if it is financed with equity only?

18.b. Calculate the “net advantage of corporate debt,” T.

18.c. What is the NPV of the machine if it is financed with a mix of equity and

debt?

19.

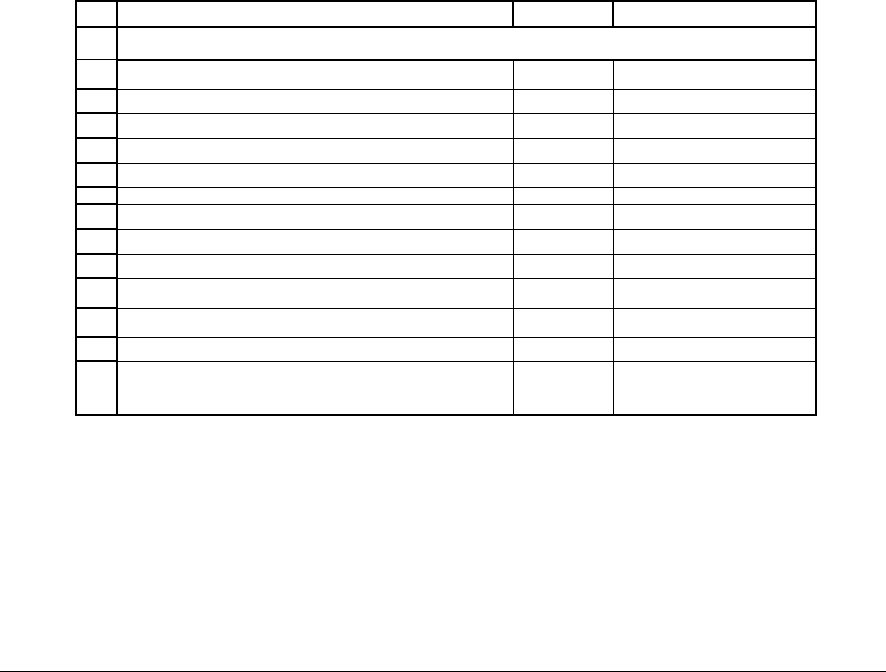

19.a. Fill in the following Excel sheet:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

ABC

Corporate tax rate, T

C

36%

Anticipated equity tax

Tax rate

Dividend yield 2.50% 40%

Capital gains yield 5.00% 10%

Net after-tax yield

??

Before tax yield

??

Personal tax rate on equity income, T

E

??

Personal tax rate on ordinary income, T

D

??

Tax advantage of debt over equity:

(1-T

D

)-(1-T

C

)*(1-T

E

)

??

FILL IN THE TAX EFFECTS

19.b. Show in a graph the change in “net advantage of corporate debt” as a

function of the personal tax rate.

PFE Chapter 21, Capital structure, empirical evidence page 1

CHAPTER 21: THE EVIDENCE ON CAPITAL STRUCTURE

*

this version: February 8, 2004

Chapter contents

Overview..............................................................................................................................2

21.1. Summarizing the theory.............................................................................................5

21.2. How do firms capitalize?...........................................................................................8

21.3. Measuring a firm’s asset

β

Assets

and WACC, an example........................................14

21.4. Repeating the asset

β

calculation for an industry ....................................................21

21.5. Academic evidence..................................................................................................25

Summing up.......................................................................................................................26

*

This is a preliminary draft of a chapter of Principles of Finance with Excel. © 2001 – 2004 Simon Benninga

(benninga@wharton.upenn.edu

).

PFE Chapter 21, Capital structure, empirical evidence page 2

Overview

Chapter 17 discussed the theory of capital structure, which concerns itself with the effects

of financing on the valuation of assets. Capital structure theory asks whether, all other factors

being the same, firms which are more highly leveraged are worth more than firms with less

leverage.

In Chapter 17 we suggested that the importance of capital structure depends on how it

affects the ability of the corporation to extract cash from its operating and its financial activities.

If, by increasing its leverage, a corporation can increase the total amount of cash it pays to its

shareholders and bondholders, then it should do so. If, on the other hand, increasing leverage

does not change the amount of cash paid to shareholders and bondholders, then increased

leverage is not worthwhile.

In Chapter 17 we related the corporate ability to extract cash from a corporation’s

activities to the trade-off between personal and corporate taxation: Corporate borrowing is tax

deductible (since interest is an expense for tax purposes); this tends to favor corporations with

more rather than less debt in their capital structures. On the other hand, a corporation with more

debt in its capital structure channels more of its income to bondholders rather than to

shareholders, and bondholders have a higher tax rate on their interest income than do

shareholders on their equity income.

To see why the Chapter 17 discussion of leverage is important, suppose for a moment

that firms with more debt are worth more than similar but less-levered firms. Then we would

suggest to corporate managers the following steps:

PFE Chapter 21, Capital structure, empirical evidence page 3

• Corporate managers should strive to increase the amount of debt used in financing

corporate activities. If, for example, a firm builds a new plant, then it should try to

borrow the maximal amount it can to build the plant.

• Corporate managers should minimize the amount of cash they have on hand (subject, of

course, to operational and safety considerations). If leverage (that is, paying interest on

debt) adds to value, then holding cash (that is, having an asset which earns interest) is a

detriment to value.

• Corporate managers should increase the corporate dividend payments. By paying out

dividends, managers decrease the amount of cash on hand and thus increase the effective

leverage of the firm.

• For the same reason corporate managers should increase share repurchases, which

decrease the amount of cash on hand and thus increase effective leverage.

The bullets above tell a manager how she should operate if leverage is a positive value

driver. If, on the other hand, leverage is a negative value driver—meaning that more leverage

decreases corporate value—then the manager should take the opposite actions. And if—as we

suggested at the end of Chapter 17—leverage is a neutral value drive because the tax benefits of

corporate leverage are offset by the tax disadvantages of leverage at the personal taxation level,

then none of the above matters.

As you can see, leverage theory can have significant operative implications.

What do we do in this chapter?

Chapter 17 was largely theoretical. In this chapter, on the other hand, we discuss the

market evidence on capital structure. We ask whether we see—in market prices, cost of capital,

PFE Chapter 21, Capital structure, empirical evidence page 4

and market risk measures—evidence for or against the positive effects of more debt on the value

of firms.

In section 21.1 we summarize the results of Chapter 17. The upshot of these results is

that the effects of financing on valuation depend largely on the tax system. Roughly speaking, if

firms, by borrowing, can increase the total cash flow available to shareholders and bondholders,

then the firms should move towards a more leveraged capital structure.

The remaining sections of the chapter ????

Finance concepts discussed

• What are some facts about capital structure (how do firms capitalize?)

• Does capital structure affect the value of the firm?

• Does capital structure affect the cost of capital?

• Are there other important considerations? Bankruptcy costs, control, etc.

• How do you measure the firm’s unlevered cost of capital r

U

?

• How do you compute the WACC for an industry?

Excel functions used

• Average

• Stdev

• Regression (trendline)

PFE Chapter 21, Capital structure, empirical evidence page 5

21.1. Summarizing the theory

The theory of capital structure outlined in the previous chapter says that the effect of

capital structure on the value of the firm is primarily due to tax considerations. Very roughly

speaking, if firms enjoy interest tax deductibility which is unavailable to their shareholders, then

firms should borrow and increase their debt/equity ratios. This theory—the “Modigliani-Miller”

theory (Chapter 17, sections ???-???)—should be contrasted with the “Miller model” (Chapter

17, sections ??? - ???) which postulates that the advantage of corporate debt is to some extent

offset by the tax advantage of equity to investors.

These are complex concepts which we illustrated with two simple examples (Arthur ABC

and Arthur XYX) in the previous chapter. We sum up:

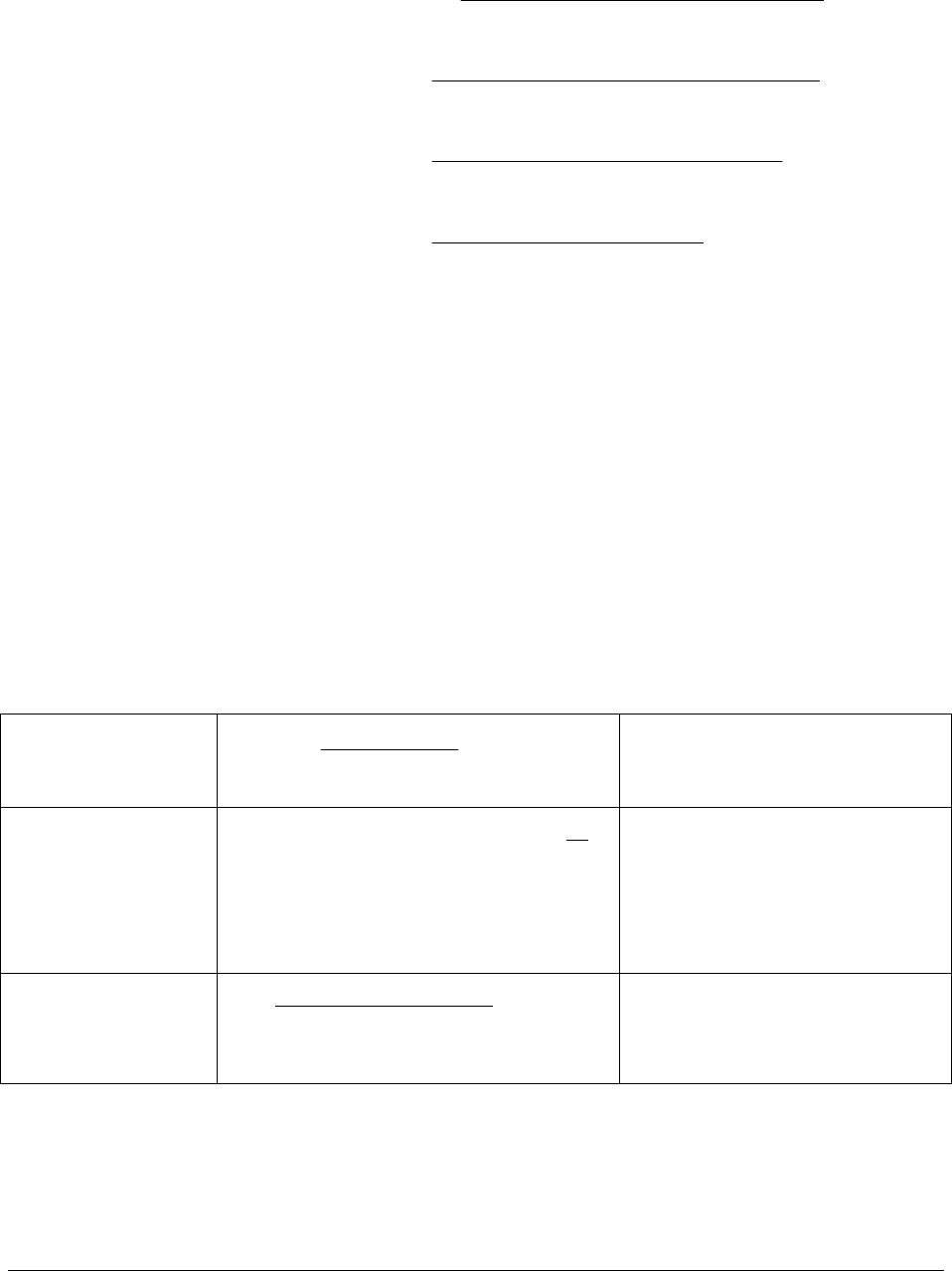

1. Leverage adds value to a firm if the capitalized value of the interest tax shields is positive:

()

()

()()()

()

1

11*1*

,

11

LU

D

EC t

U

t

DD

V V PV Capitalized interest tax shields

T T T Interest

PV FCFs discounted at r

Tr

∞

=

=+

⎡⎤

−−− −

⎣⎦

=+

+−

∑

Here:

()

C

E

D

T the corporate tax rate

T the personaltaxrateonequityincome

T the personaltaxrateonordinaryincome including interest

=

=

=

2. Assuming that a firm is contemplating a permanent change in its capital structure,

PFE Chapter 21, Capital structure, empirical evidence page 6

()

(

)

(

)

(

)

()

()()()

()

()()()

()

()()()

()

1

11*1*

11

11*1**

1

11*1*

*

1

11*1

1

DEC

t

DD

DECD

DD

DEC

D

DEC

D

T T T Interest

PV Capitalized interest tax shields

Tr

TTTrDebt

Tr

TTTDebt

TDebt

T

TTT

where T

T

∞

=

⎡⎤

−−− −

⎣⎦

=

+−

⎡⎤

−−− − ∆

⎣⎦

=

−

⎡⎤

−−− − ∆

⎣⎦

==∆

−

⎡⎤

−−− −

⎣⎦

=

−

∑

3. In the classic Modigliani-Miller theory, which invokes only corporate taxes,

C

TT= , so that

debt always adds to value. In Miller’s more complex model, which takes into account both

personal and corporate taxes, T can be positive, negative, or zero, depending on the sign of

()()()

111

D

ED

TTT−−− −. Miller hypothesized that

(

)

(

)

(

)

1110

DED

TTT

−

−− − =; if this is so,

then there would be no advantage to debt over equity financing.

4. Leverage affects both the weighted average cost of capital (WACC) and the cost of equity r

E

:

Weighted average

cost of capital,

WACC

(

)

*1

*

U

ED T

WACC r

ED

+−

=

+

If debt adds value (i.e., T > 0),

leverage decreases the WACC

Cost of equity of a

levered firm, r

E

() ( )

*1 *1

EU U D C

D

rr r Tr T

E

⎡⎤

=+ −− −

⎣⎦

More debt always makes equity

more risky and increases the

cost of equity r

E

. The amount

by which the equity becomes

more risk depends on the

relative sizes of T and T

C

.

Cost of unlevered

capital, r

U

()

**(1 ) *

*1

DCE

U

rD T rE

r

ED T

−

+

=

+−

Often we estimate a firm’s cost

of equity; this formula lets you

back out the unlevered cost of

capital from r

E

.

5. Contrary to the formula in 2 above, the value of debt interest tax shields is not the only factor

in determining the effect on firm value of a change in debt. Three other prominent factors

PFE Chapter 21, Capital structure, empirical evidence page 7

discussed by academics and practitioners are: bankruptcy costs, the costs of financial control

(change name), and the option effects associated with debt. These costs are difficult to quantify,

but they certainly exist:

5.a. Costs of financial distress (“bankruptcy costs”): Increasing a firm’s leverage also

makes it more likely that a firm will have a greater future probability of getting into

financial trouble. The present value of the costs of getting out of this trouble (they should

be called “costs of financial distress,” but they are usually call termed “bankruptcy

costs”) should be deducted from the benefits of additional leverage.

1

5.b. Costs of financial control. Borrowers will usually lend the firm more money only if

they can exercise more control. Often this control involves debt covenants. These are

restrictions imposed by the lender on the firm. For example, the Giant Industries bond

issue discussed in section 15.4 (page000) has the following covenants:

“The Indentures . . . contain restrictive covenants that, among other things, restrict the ability of

the Company and its subsidiaries to create liens, to incur or guarantee debt, to pay dividends, to

repurchase shares of the Company's common stock, to sell certain assets or subsidiary stock, to

engage in certain mergers, to engage in certain transactions with affiliates or to alter the

Company's current line of business.”

1

Empirical research in finance estimates bankruptcy costs as generally less than 10% of the face

value of debt at the time of bankruptcy. If the Modigliani-Miller full tax shield on debt were to

hold, it is unlikely that bankruptcy costs of this magnitude would retard corporate desires for

more leverage. A recent paper (Timothy Fisher and M. Jocelyn Martel, "On Direct Bankruptcy

Costs and the Firm's Bankruptcy Decision" (January 2001). http://ssrn.com/abstract=256128

)

gives interesting information of the size of bankruptcy and liquidation costs in Canada.