Principles of Finance with Excel (Основы финансов c Excel)

Подождите немного. Документ загружается.

PFE Chapter 20, Capital structure and valuation page 33

()

(

)

(

)

After-tax After-tax After-tax

ordinary income equity income corporate income

(including interest)

Net after-tax personal

income from pre-tax corporate

cash flows

111

DEC

TTT

↑↑↑

↑

−−− −

If this term is positive, as in the previous example (see cell B32), then XYZ corporation should

borrow; if it’s negative—as in the next example (in which the corporate tax rate is T

C

= 20%),

then Arthur should borrow and not the firm:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

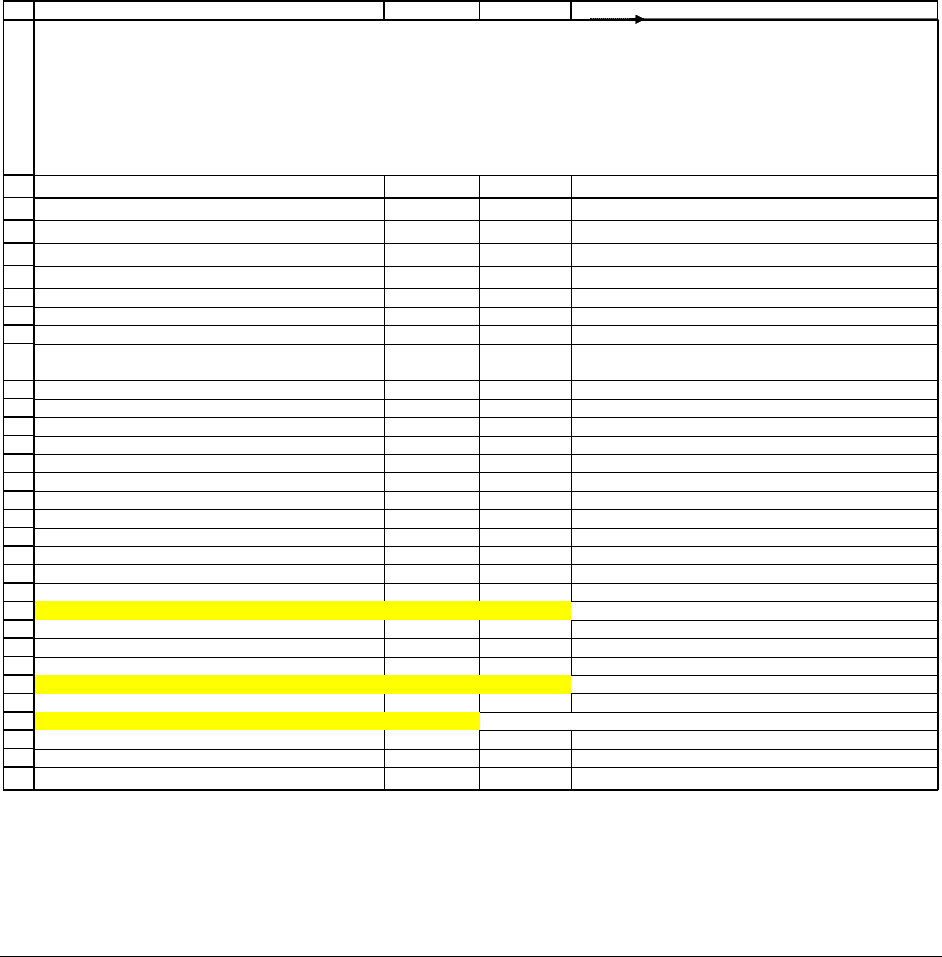

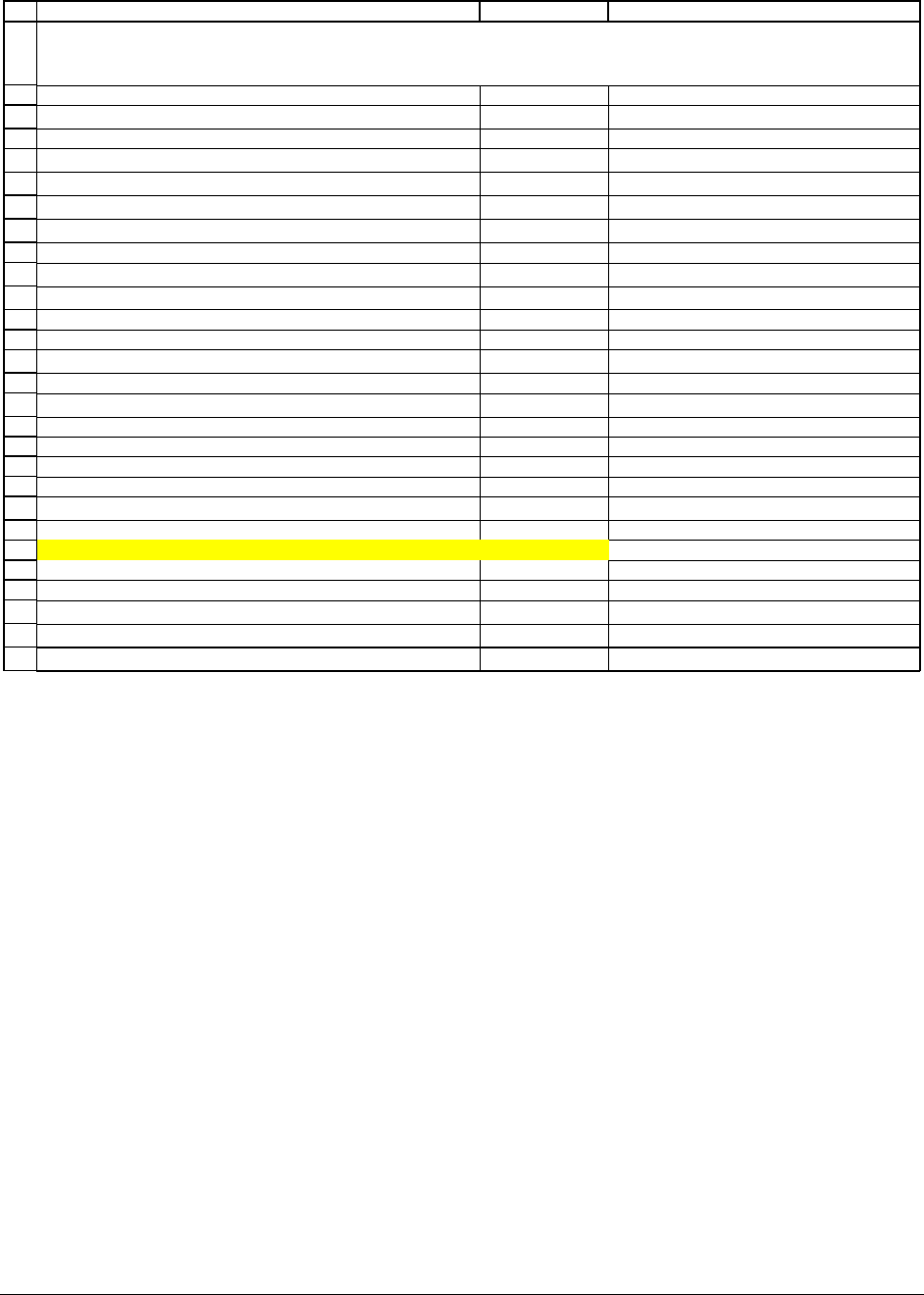

ABC D

Computing the family income

T

C

, corporate tax rate

20%

T

E

, personal equity tax rate

10%

T

D

, personal debt tax rate on ordinary income

30%

r

D

, interest rate

8%

D, Debt 3,000

FCF, free cash flow (already after corporate taxes) 1,000

Company

borrows

A

rthur

borrows

FCF, after personal tax 1,000.00 1,000.00

Corporate debt 3,000.00 0.00

Corporate pre-tax interest payment 240.00 0.00

Corporate after-tax interest payment 192.00 0.00 <-- =C13*(1-$B$3)

Payout to equity owners 808.00 1,000.00 <-- =C11-C14

Arthur's income

Pre-tax equity income from XYZ 808.00 1,000.00 <-- =C15

Post-tax equity income from XYZ 727.20 900.00 <-- =C18*(1-$B$4)

Arthur's debt 0.00 3,000.00

Arthur's pre-tax interest payment 0.00 240.00 <-- =$B$6*C20

Arthur's after-tax interest payment 0.00 168.00

Arthur's post-tax income 727.20 732.00 <-- =C19-C22

Mom's pre-tax income 240.00 240.00 <-- =C20*B6

Mom's post-tax income 168.00 168.00 <-- =C25*(1-$B$5)

Total family income 895.20 900.00 <-- =C23+C26

Who should borrow--Arthur or company? Arthur <-- =IF(B27>C27,"Company",IF(B27<C27,"Arthur","Indifferent"))

Net advantage of corporate debt

(1-T

D

)-(1-T

E

)*(1-T

C

)

-0.02

FINANCING ARTHUR'S PURCHASE OF XYZ

Upper Fantasia tax code: Corporate income tax, T

C

= 20%

(instead of 40% in previous example)

Personal taxes: Tax on equity income, T

E

= 10%,

Tax on all other income, T

D

= 30%

PFE Chapter 20, Capital structure and valuation page 34

Some Finance History (2)

The Modigliani-Miller model dates from two articles published in 1958 and 1963. In

1977 Merton Miller (half of the MM team), reconsidered the problem of capital structure. He

still focused on taxation, but this time considered the case where both corporate and personal

income was taxed.

Miller’s reasoning, incorporated in our example of XYZ Corp, was that the corporate tax

rate T

C

gives an advantage to corporations wishing to finance with debt. On the other hand, for

individuals equity income is generally taxed at a lower rate T

E

than the tax rate T

D

on debt

income. The primary reason for this is that the major part of income from equity is received by

shareholders as capital gains; these are not only taxed at a lower tax rate, but the taxes on capital

gains are also postponable (as a shareholder, you can decide when to sell your shares and realize

your capital gains). This postponability lowers the T

E

below the statutory rate (see some

discussion in Chapter 21). Thus, Miller reasoned, there is a tradeoff:

•

On the corporate level, the deductibility of interest means that corporations produce

higher before-personal-tax payouts to stakeholders (bondholders and shareholders) when

they have more debt financing.

•

On the personal level, giving stakeholders (bond and shareholders) more interest income

instead of equity income means taxing them at higher personal rates.

This tradeoff is summarized in the expression

(

)

(

)

(

)

111

D

CE

TTT−−− −:

()

(

)

(

)

Payments to debtholders are Equity income is taxed twice:

only taxed at the personal tax of once at the firm

the debtholder, since the firm makes these

payments out of pre-tax income

11*1

DCE

TTT

↑↑

−−−−

level (since

payments to shareholders are paid

out of after-tax earnings), and then again at the

personal level

On the other hand, , so that there is a tradeoff ...

ED

TT

↑

<

PFE Chapter 20, Capital structure and valuation page 35

XYZ CORP--ARTHUR AND MOM'S INCOME

XYZ Corp

A

fte

r

-tax cost of debt: (1-T

C

)r

D

Each $ of before tax interest paid:

1) Decreases shareholder income by (1-T

C

)

2) Increases Arthur's Mom's interest payments by $1.

Shareholder Arthur

Equity income taxed at T

E

Each $ of before tax interest paid by XYZ

decreases Arthur's income from the

company by (1-T

C

)*(1-T

E

)

Bondholder Mom

Interest income taxed at T

D

Each $ of interest paid by the company

increases Mom's income by (1-T

D

)

Family income: Arthur + Mom

Each $ of before-tax interest paid by XYZ increases Mom's

income by (1-T

D

) and decreases Arthur's by (1-T

C

)*(1-T

E

).

Net effect: (1-T

D

) - (1-T

E

)*(1-T

C

).

If this is positive, it's good for the family and the firm should

increase its borrowing; if its negative, it's bad for the family and

the firm should decrease its borrowing.

Miller suggested that

in equilibrium

(1-T

D

) - (1-T

E

)*(1-T

C

) = 0

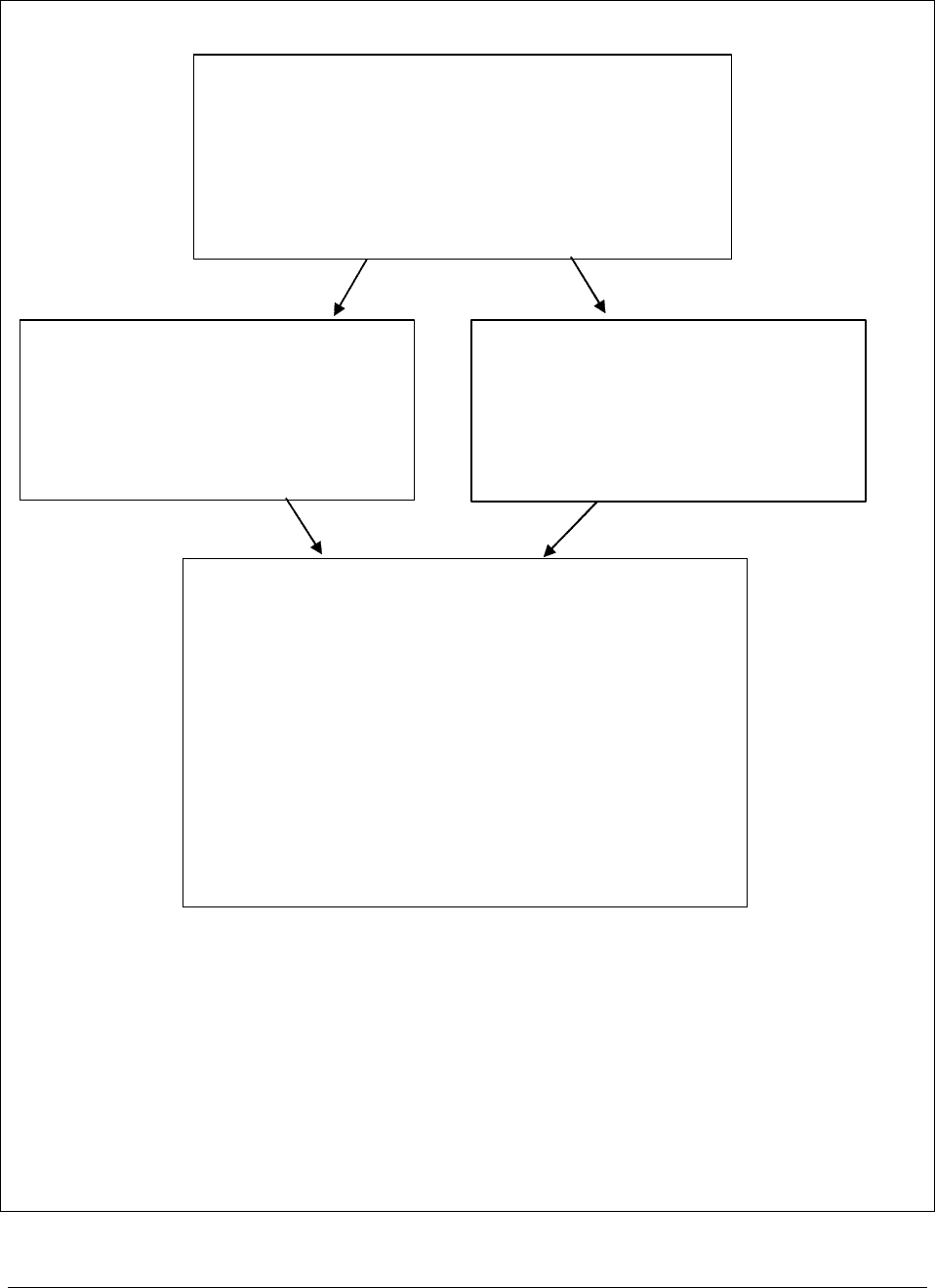

Figure 20.3. Cash flows of Arthur + Mom’s family income. In this flow diagram, Arthur is the

shareholder of XYZ Corp., and Mom is the bondholder of XYZ (meaning: she lends the

company money). Each $1 of interest income paid to Mom by XYZ Corp. changes the family

income by

()()()

11*1

D

EC

TTT−−− −. If this term is positive, then XYZ Corp.’s borrowing from

Mom adds to the family income; if it is negative, then XYZ Corp.’s borrowing detracts from the

family income.

PFE Chapter 20, Capital structure and valuation page 36

20.7. Valuing XYZ Corp.—taking account of leverage and taxes

We redo the calculations in section 20.2, but this time use all the taxes—the corporate tax

rate T

C

, the personal tax rate on equity income T

E

, and the personal tax rate on ordinary income

(including interest) T

D

. Without leverage XYZ Corp’s FCFs are worth $5,000:

()

()

1

,@

1,000 1,000

5,000

20%

1.20

U

t

t

U

V Unlevered value of XYZ

PV future FCFs discounted unlevered discount rate

Annual FCF

r

∞

=

=

=

== ==

∑

We use the additivity principle to value the levered version of XYZ Corp:

(

)

() ()

11

-

1,000 1,000

5,000

20%

11.20

The unlevered value of the firm is

the present value of its free cash flows

discounted an an appropriate (unlevered)

cost

LU

t

U

tt

tt

U

V V PV additional debt related CFs

FCF

V

r

∞∞

==

=+

====

+

=

∑∑

()()()

()

()

()

()

1

1

of capital

11*1*

11

8%*3,000*16% 38.4

685.71

5.6%

1 8%* 1 30%

The tax shields created

by the debt are discounted at the

con

U

DCE t

t

t

DD

t

t

r

T T T Interest

Interest tax

PV

shields

Tr

∞

=

∞

=

⎧

⎪

⎪

⎪

⎪

⎨

⎪

⎪

⎪

⎪

⎩

⎡− − − − ⎤

⎛⎞

⎣⎦

=

⎜⎟

⎝⎠

+−

===

+

+−

∑

∑

sumer's after-tax interest rate.

5,685.71

⎧

⎪

⎪

⎪

⎪

⎪

⎨

⎪

⎪

⎪

⎪

⎪

⎩

=

XYZ Corp is worth more as a levered firm than as an unlevered firm because it produces

more cash for its owners when it is levered. The additional cash produced—generated by the

PFE Chapter 20, Capital structure and valuation page 37

fact that the company has a cheaper cost of debt than Arthur—is worth $685.71, which is the

present value of the future tax shields on the interest:

(

)

(

)

(

)

()

()

()()()

()

()()()

()

()()()

()

1

11*1*

11

11*1

*

1

11*1

*

1

11*1

*

1

DCE

t

t

DD

DCE

DD

DCE

DD

DCE

D

T T T Interest

Interest tax

PV

shields

Tr

TTT

I

nterest

Tr

TTT

I

nterest

Tr

TTT

D

T

∞

=

⎡⎤

−−− −

⎛⎞

⎣⎦

=

⎜⎟

⎝⎠ +−

⎡⎤

−−− −

⎣⎦

=

−

⎡⎤

−−− −

⎣⎦

=

−

⎡⎤

−−− −

⎣⎦

=

−

∑

We use the letter T to denote the debt-valuation factor:

(

)

(

)( )

()

11*1

1

DCE

D

TTT

T

T

⎡

⎤

−−− −

⎣

⎦

=

−

. T is

the capitalized advantage of debt.

9

What about the cost of capital—r

E

and WACC with leverage?

The levered version of XYZ Corp. is worth $5,685.71, of which $3,000 is debt.

Subtracting the value of the debt from the total worth of the company, we see that the equity of

the company is worth $2,685.71. In order to calculate the firm’s cost of equity r

E

, we first

compute the after-tax cash flows accruing to the equity owners:

[

]

()

--

1,000 8%*3,000* 1 40% 856.00

annual after corporate tax equity cash flow FCF after -tax interest paid by XYZ=−

⎡⎤

=− −=

⎣⎦

The discounted value of this annual equity cash flow of $856.00 is the value of the equity; this

defines the cost of equity r

E

:

9

To relate this to the previous case with only corporate taxes, note that when T

E

= T

D

= 0, T = T

C

.

PFE Chapter 20, Capital structure and valuation page 38

()

()

1

1

1

856.00 856.00

2,685.71

1

856.00

31.87%

2685.71

t

t

t

E

t

t

E

E

E

equity cash flow

Equity value

r

r

r

r

∞

=

∞

=

=

+

==

+

⇒= =

∑

∑

With a little mathematical flimflammery, we can show that:

() ( )

N

()()

U

r is the discount

rate for the FCFs,

When XYZ borrows, it's shareholders

which represents

bear an additional

the firm's business

risk

*1 *1

3,000

20% 20% 1 22.86% 8% 1 40%

2,685.71

EU U D C

fi

D

rr r Tr T

E

↑

↑

⎡⎤

=+ −− −

⎣⎦

⎡⎤

=+−−−

⎣⎦

. The

term above represents the financial risk

premium for the equity holders

31.87%

nancialrisk

=

We can now compute the WACC:

()

()

1

2,685.71 3,000

31.87% 8% 1 40%

2,685.71 3,000 2,685.71 3,000

17.59%

EDC

ED

WACC r r T

ED ED

=+−

++

=+−

++

=

With a little more “flimflammery” we can show that discounting the FCFs at the WACC

gives the total value of the firm:

()()

11

1,000 1,000

5,685.71

17.59%

1 1 17.59%

t

tt

tt

FCF

WACC

∞∞

==

===

++

∑∑

Here’s all of this summarized in a spreadsheet:

PFE Chapter 20, Capital structure and valuation page 39

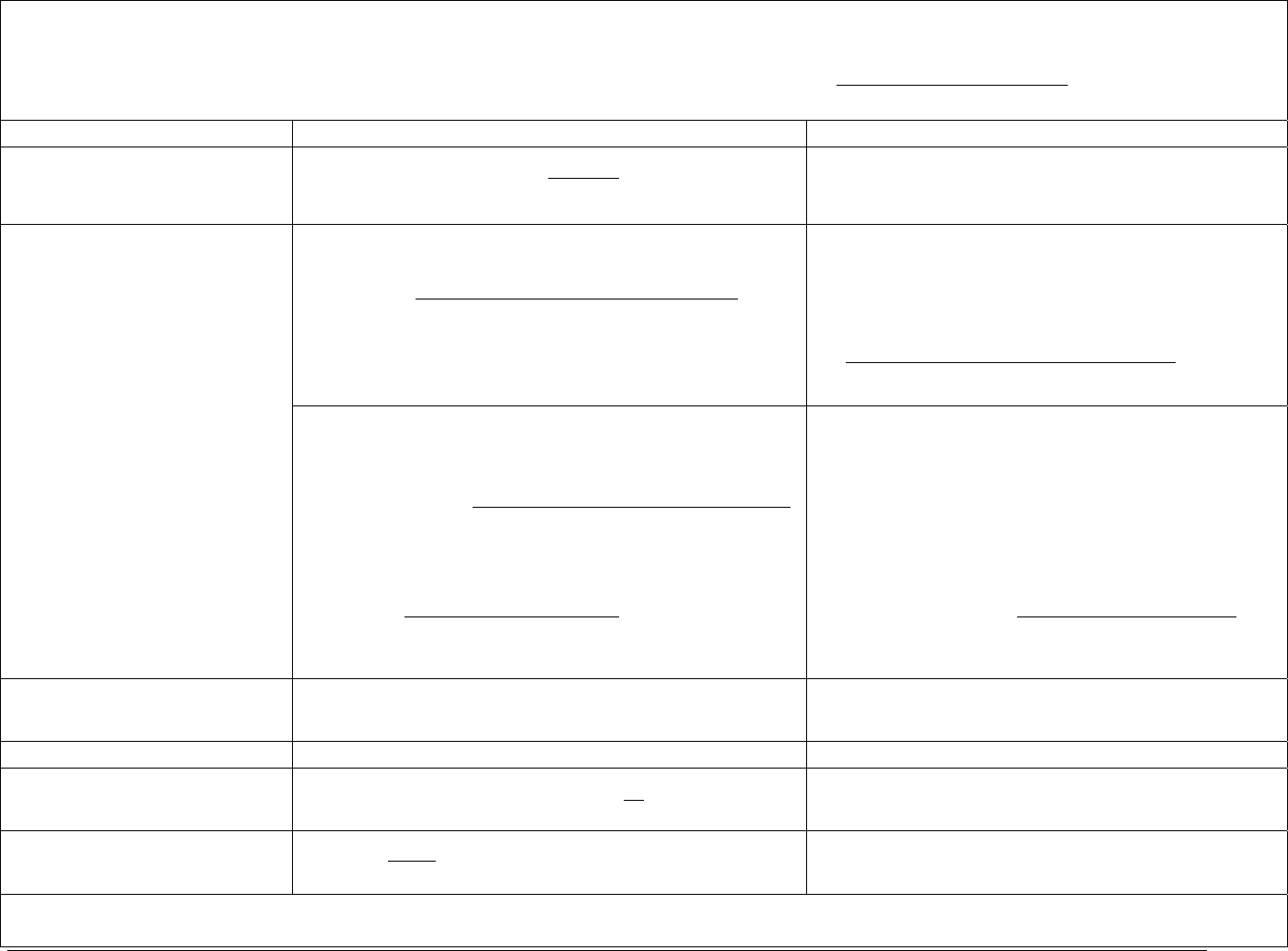

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

ABC

FCF, annual free cash flow (already after corporate taxes) 1,000

r

U

, unlevered cost of capital

20%

D, Debt 3,000

r

D

, interest rate

8%

T

C

, corporate tax rate

40%

T

E

, personal equity tax rate

10%

T

D

, personal debt tax rate on ordinary income

30%

Tax advantage of debt, (1-T

D

)-(1-T

C

)*(1-T

E

)

16.00% <-- =(1-B8)-(1-B6)*(1-B7)

T= [(1-T

D

)-(1-T

C

)*(1-T

E

)]/(1-T

D

) , tax factor

22.86% <-- =B10/(1-B8)

V

alue of firm

V

U

, unlevered value

5,000.00 <-- =B2/B3

Value of tax shield on interest 685.71 <-- =B10*B5*B4/((1-B8)*B5)

V

L

, levered value of firm

5,685.71 <-- =B15+B14

E, value of equity 2,685.71 <-- =B16-B4

Cash flow to equity 856.00 <-- =B2-(1-B6)*B5*B4

Return on equity, r

E

(L)

31.87% <-- =B20/B18

WACC 17.59% <-- =B21*B18/B16+(1-B6)*B5*B4/B16

Three checks

Return on equity, r

E

(L) = r

U

+ [r

U

*(1-T) - r

D

*(1-T

C

)]*D/E

31.87% <-- =B3+(B3*(1-B11)-B5*(1-B6))*B4/B18

Value of firm, V

L

= FCF/WACC

5,685.71 <-- =B2/B23

Value of firm, V

L

= V

U

+ T*D

5,685.71 <-- =B14+B11*B4

COMPUTING THE WACC IN THE MILLER MODEL

with corporate and personal taxes

Summarizing this section

We complete this section by restating its major conclusions. If corporate income is taxed,

and if the tax system differentiates between income derived from equity and ordinary income,

then leverage (borrowing) may increase or decrease the value of the firm, depending on the sign

of the tax factor

()()()

11*1

D

EC

TTT−−− −.

A summary table is given below:

PFE Chapter 20, Capital structure and valuation page 40

SUMMARY TABLE—CHANGING LEVERAGE WHEN CORPORATE AND PERSONAL INCOME ARE TAXED

Symbols: Corporate tax rate: T

C

, personal tax rate on equity income T

E

, personal tax rate on ordinary income T

D

Tax advantage of debt =

(

)

(

)

(

)

11*1

D

CE

TTT−−− −, Tax factor:

(

)

(

)

(

)

()

11*1

1

D

CE

D

TTT

T

T

−−− −

=

−

Item Formula Why

V

U

= Value of unlevered firm

()

1

1

t

U

t

t

U

FCF

V

r

∞

=

=

+

∑

The value of the unlevered firm is the PV of future

FCFs discounted at r

U

, the unlevered cost of

capital

(

)

()()()

()

()

1

111*

11

LU

N

D

EC t

U

t

t

DD

V V PV net interest taxshields

TTTInterest

V

rT

=

=+

⎡⎤

−−− −

⎣⎦

=+

+−

∑

Another way to write this is *

LU

VVTD

=

+ , where

The value of the levered firm is V

U

plus the present

value of future interest tax shields. When there are

both corporate and personal taxes, the PV of the tax

shields is given by:

(

)

(

)

(

)

()

()

1

111*

11

N

D

EC t

t

t

DD

TTTInterest

rT

=

⎡⎤

−−− −

⎣⎦

+−

∑

V

L

= Value of the levered firm

(

)

()()()

()

()

()()()

()

1

111*

11

*,

111

1

LU

DEC

U

t

t

DD

U

DEC

D

V V PV net interest taxshields

T T T Interest

V

rT

VTD

TTT

where T

T

∞

=

=+

⎡⎤

−−− −

⎣⎦

=+

+−

=+

−−− −

=

−

∑

The cell to the left contains the formula for the

value of the levered firm when the firm issues

perpetual debt. This formula is the same as the

parallel formula in Figure 20.2 for the case where

T

E

=T

D

=0.

In the general case where personal taxes are

perhaps not zero,

(

)

(

)

(

)

()

111

1

D

EC

D

TTT

T

T

−−− −

=

−

can

be positive, negative, or zero.

E = Value of equity

(

)

1

U

E

VTD=−−

The equity value of the levered firm =

(

)

1

LU

E

VDV TD=−=−−

D=Value of Debt D

()

E

rL

= Cost of equity of the

levered firm

() ( ) ( )

11

EUU DC

D

rL r r T r T

E

⎡

⎤

=+ −− −

⎣

⎦

WACC = weighted average

cost of capital

WACC=

L

FCF

V

Figure 20.4 . Corporate value and cost of capital when corporate income is taxed at rate T

C

, personal ordinary income is taxed at rate T

D

, and

personal equity income is taxed at rate T

E

.

PFE Chapter 19, Capital structure and valuation page 41

20.8. Buying a sturfing machine in Upper Fantasia

In this section and the next we return to the examples of sections 20.3 and 20.4. This

time we do these examples for a company in Upper Fantasia, where, as you will recall there are

three tax rates:

• In Upper Fantasia corporate income is taxed at the rate T

C

= 40%

• Personal income from equity (meaning: dividends and capital gains) is taxed at rate T

E

=

10%

• Personal income from all other sources is taxed at rate T

D

= 30%

Sonderturf considers buying a sturfing machine

Sonderturf Corp., a company is Upper Fantasia, is considering purchasing a new sturfing

machine. The sturfing machine costs $100,000; it has a ten-year life, during which it is straight-

line depreciated to zero salvage value. In each of the ten years of the machine’s life, it will

produce sales of $40,000. These sales will cost $15,000 to produce. The result is that the

machine has an annual free cash flow of $19,000 per year.

The Sonderturf financial wizards have determined that an appropriate risk-adjusted

discount rate for the sturfing machine’s free cash flows is r

U

= 15%. Discounting the machine’s

FCFs at this rate shows that it has a negative NPV of -$4,643. Thus the conclusion is that

Sonderturf should not acquire the sturfing machine. (For details of these calculations, refer to

section 20.3, page000.)

PFE Chapter 19, Capital structure and valuation page 42

Sonderturf gets a loan to buy the machine

Having heard the bad news from Sonderturf, the sturfing machine’s manufacturer offers

the company a loan of $50,000. The loan’s conditions are exactly the same as those of the loan

in section 20.??? which was offered to Sonderturf in Lower Fantasia: In years 1-9, Sonderturf

will pay only interest ($4,000), and in year 10 it will pay interest of $4,000 as well as repay the

loan principal.

It follows from Figure 20.4 that the value of the loan is

()

()()()

()

()

()()()

10

1

,

,,

111*

11

1 30% 1 10% 1 40%

CE

D

DEC t

t

t

DD

loan in Upper Fantasia where there are corporate income

PV taxes T taxes on equity income T

and taxes on ordinaryincome T

T T T Interest

PV net interest tax shields

rT

=

⎛⎞

⎜⎟

=

⎜⎟

⎜⎟

⎝⎠

−−− −

⎡⎤

⎣⎦

=

+−

−−− −

=

∑

()

()

10

1

*$4,000

$4,801

1 1 30%

t

t

D

r

=

⎡⎤

⎣⎦

=

+−

∑

The Sonderturf financial wizards conclude that the company should now purchase the

machine, taking the loan to finance part of the purchase. They calculate that:

()()

(

)

()( )

()()()

()

()

In Upper Fantasia the tax shield

takes account of corporate as well as

personal taxes:

10

DEC t

t

t=1

DD

1-T - 1-T 1-T *Interest

1+ 1-T * r

NPV machine loan NPV machine NPV loan

NPV machine PV loan interest tax shields

↑

⎡⎤

⎣⎦

+= +

=+

∑

$4,643 $4,801

$158

=− +

=

The calculations are shown in the following Excel spreadsheet: