Principles of Finance with Excel (Основы финансов c Excel)

Подождите немного. Документ загружается.

PFE Chapter 20, Capital structure and valuation page 13

Here’s all of this summarized in a spreadsheet. Note from the title of the spreadsheet that

we’ve given this model a name; we’ve called it the “Modigliani-Miller model with only

corporate tax.” To see why the name, refer to the box “Some history of finance (1)” on page000.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

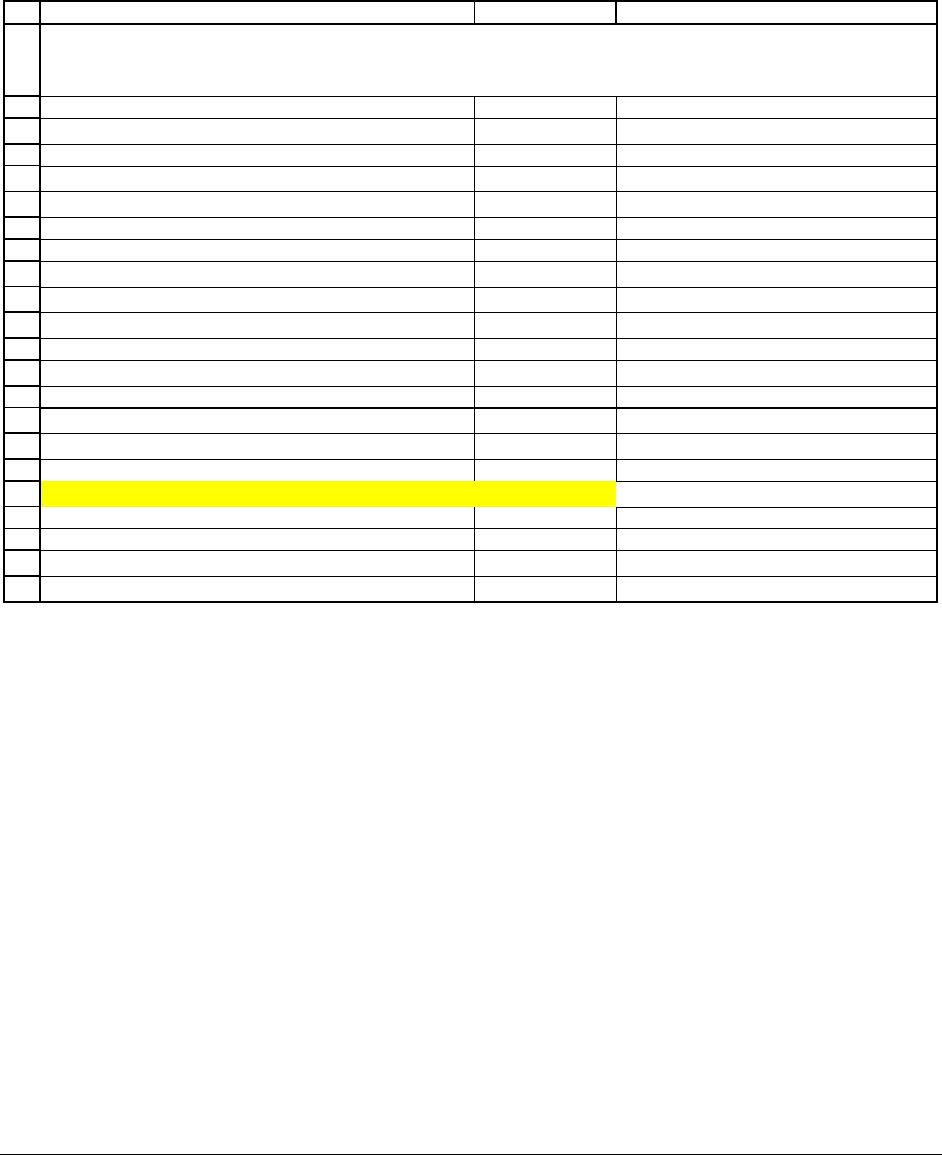

ABC

Annual FCF 1,000

r

U

, unlevered cost of capital

20%

D, debt (perpetual) 3,000

r

D

, the cost of debt (interest rate)

8%

T

C

, corporate tax rate

40%

V

alue of firm

V

U

, unlevered value = FCF/r

U

5,000.00 <-- =B2/B3

Value of tax shield on interest = T

C

*r

D

*D/r

D

= T

C

*D

1,200.00 <-- =B6*B4

V

L

, levered value of firm = V

U

+ T

C

*D

6,200.00 <-- =B10+B9

E, value of equity = V

L

- D

3,200.00 <-- =B11-B4

Cash flow to equity = FCF - (1-T

C

)*interest

856.00 <-- =B2-(1-B6)*B5*B4

Return on equity, r

E

(L)= [FCF - (1-T

C

)*interest]/E

26.75% <-- =B15/B13

WACC = r

E

(L)*E/(E+D) + r

D

*(1-T

C

)*D/(E+D)

16.13% <-- =B16*B13/B11+(1-B6)*B5*B4/B11

Two checks

Return on equity, r

E

(L)= r

U

+ (r

U

- r

D

)*[D/E]*(1-T

C

)

26.75% <-- =B3+(B3-B5)*B4/B13*(1-B6)

Value of firm, V

L

= FCF/WACC

6,200.00 <-- =B2/B18

COMPUTING THE WACC IN MODIGLIANI-MILLER MODEL WITH ONLY

CORPORATE TAXES

We complete this section by restating its major conclusions. If only corporate income is

taxed, leverage (borrowing) increases the value of the firm. This increase in value, represented

by the present value of the tax shields on the debt, increases the value of the firm’s equity,

increases the cost of equity r

E

, and decreases the WACC.

A summary table is given below:

PFE Chapter 20, Capital structure and valuation page 14

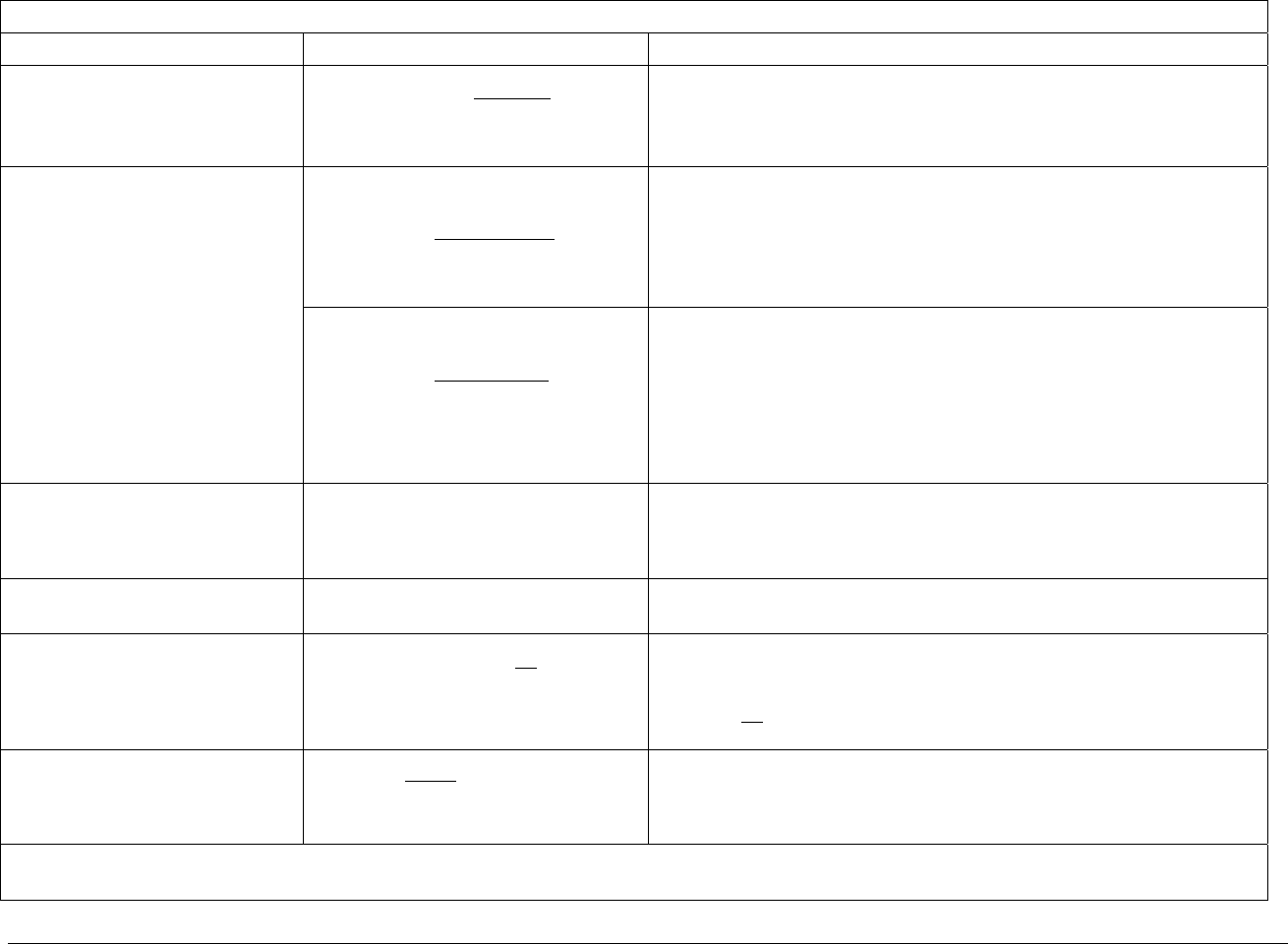

SUMMARY TABLE—CORPORATE VALUATION WHEN ONLY CORPORATE INCOME IS TAXED

Item Formula Why

V

U

= Value of unlevered firm

()

1

1

t

U

t

t

U

FCF

V

r

∞

=

=

+

∑

The value of the unlevered firm is the PV of future FCFs

discounted at r

U

, the unlevered cost of capital

(

)

()

1

*

1

LU

N

Ct

U

t

t

D

V V PV interest taxshields

T Interest

V

r

=

=+

=+

+

∑

The value of the levered firm is V

U

plus the present value of

future interest tax shields. The cell to the left contains the

formula for the value of the levered firm when there are N

interest payments on the debt.

V

L

= Value of the levered

firm

(

)

()

1

*

1

*

LU

C

U

t

t

D

UC

V V PV interest taxshields

T Interest

V

r

VTD

∞

=

=+

=+

+

=+

∑

The cell to the left contains the formula for the levered firm

when the firm issues perpetual debt.

E = Value of equity

(1 ) *

UC

VTD−−

The equity value of the levered firm is the value of the levered

firm minus the value of the firm’s debt:

(

)

*1

LUCUC

EV DV DT DV TD=−=+ −=−−

D=Value of Debt D The value of the debt is the value of the debt. (OK, this ain’t

so original!)

()

E

rL= Cost of equity of the

levered firm

()

[]

()

1

EUUD C

D

rL r r r T

E

=+ − −

The cost of equity r

E

is the discount rate for equity cash flows.

In a levered firm it includes a financial risk premium:

[]

()

1

UD C

D

rr T

E

−−

WACC = weighted average

cost of capital

WACC=

L

FCF

V

You can correctly value the whole firm by discounting its

FCFs at the WACC. This is the valuation principle we’ve

employed in Chapters 6, 9, and 19.

Figure 20.2: Corporate value and cost of capital corporate income is taxed at rate T

C

and when there are no personal taxes.

PFE Chapter 20, Capital structure and valuation page 15

Some History of Finance (1)

The valuation model summarized in the table above is often called the Modigliani-Miller

model, after Professors Franco Modigliani and Merton Miller, both winners of the Nobel Prize in

Economics. In two path-breaking articles published in 1958 and 1963, Modigliani and Miller

showed that the value of the firm would not be affected by the method in which the firm was

financed, except where the tax code explicitly favors one form of financing. In the example of

ABC Corp. in section 20.2, the tax code gives corporations a tax break on debt financing,

whereas individuals (who are untaxed) get no such break; it is therefore optimal for the firm to

finance with more debt and less equity.

Students of finance know this result as the “MM model.” It has been widely studied and

even more widely misunderstood.

In section ??? we consider a variation of the MM model which takes account not only of

corporate taxes but also personal taxes. While the logic is the same, the conclusions are very

different. This model—less widely studied and even more misunderstood—is known as the

Miller model, after Merton Miller, who expounded it in a famous academic article which

appeared in the Journal of Finance in 1977. (See the box “Some History of Finance (2)” on

page000.

20.3. Why debt is valuable in Lower Fantasia—buying a turfing machine

It’s easier to understand the theory of the previous section by looking at some numerical

examples. In this and the following two sections we discuss several such examples. Each of

PFE Chapter 20, Capital structure and valuation page 16

these examples makes the point that under the Lower Fantasia tax regime—in which corporate

income is taxed at a rate T

C

, but in which there are no taxes on personal income—companies

which finance with debt can increase their market value.

The tax regime in Lower Fantasia is characterized by a tax on corporate income but no

other taxes. In the previous section we showed that this tax regime means that the value of

companies in Lower Fantasia is increased when they lever themselves.

We start with an example that shows the effect of financing on a capital budgeting

decision.

Buying a machine

Wonderturf Corp., a company in Lower Fantasia, is considering purchasing a new turfing

machine. The turfing machine costs $100,000; it has a ten-year life, during which it is straight-

line depreciated to zero salvage value. In each of the ten years of the machine’s life, it will

produce sales of $40,000. These sales will cost $15,000 to produce. The result is that the

machine has an annual free cash flow of $19,000 per year (see cell B10 below):

()

(

)

()( )

1* -

1 40% * 40,000 15,000 10,000 10,000

$19,000

C

Annual Wonderturf FCF T Sales Expenses Depreciation Depreciation=− − +

=− − − +

=

PFE Chapter 20, Capital structure and valuation page 17

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

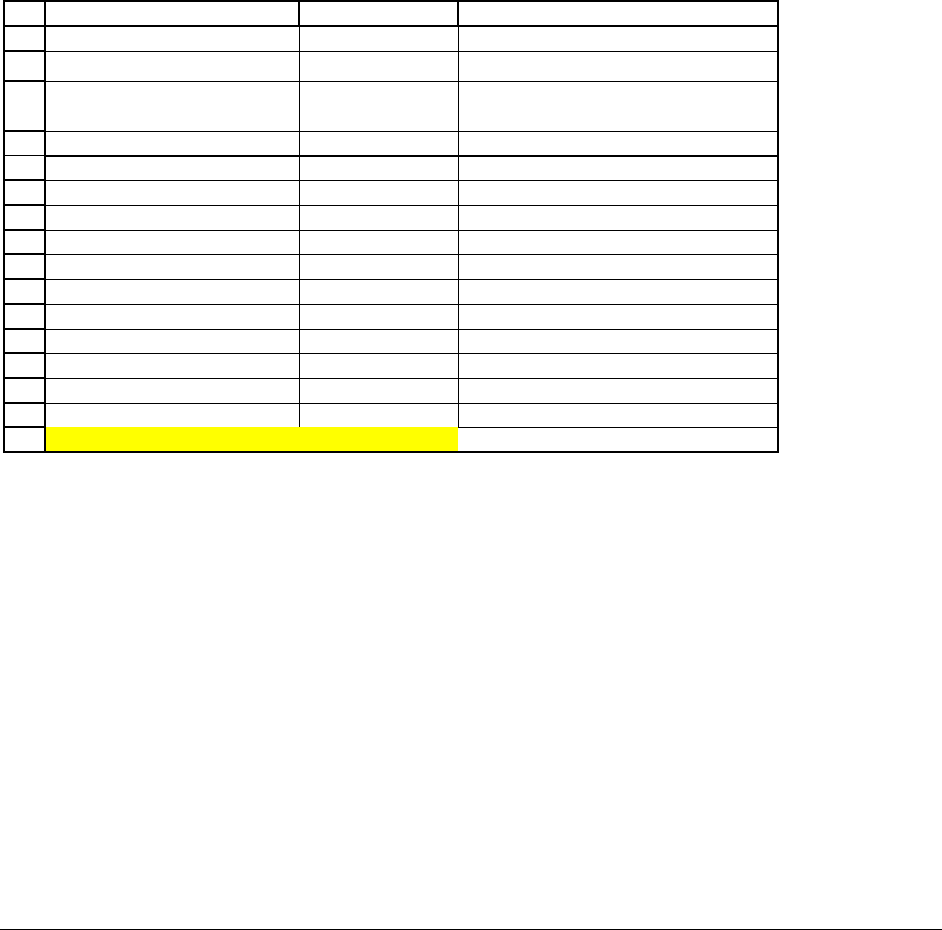

ABC

T

C

, corporate tax rate

40%

Machine cost, year 0 100,000

Free cash flow (FCF) calculation

Additional sales, annually 40,000

Additional annual cost of sales 15,000

Annual depreciation 10,000 <-- =B4/10

Annual FCF, years 1-10 19,000 <-- =(1-B2)*(B7-B8-B9)+B9

r

U

, discount rate for machine FCFs

15%

Year

Machine

FCF

0 -100,000 <-- =-B4

1 19,000 <-- =$B$10

2 19,000

3 19,000

4 19,000

5 19,000

6 19,000

7 19,000

8 19,000

9 19,000

10 19,000

Machine NPV -4,643 <-- =B15+NPV(B12,B16:B25)

THE WONDERTURF TURFING MACHINE

The Wonderturf financial wizards have determined that an appropriate risk-adjusted

discount rate for the turfing machine’s free cash flows is r

U

= 15%. Discounting the machine’s

FCFs at this rate shows that it has a negative NPV of -$4,643 (cell B27). Thus the conclusion is

that Wonderturf should not acquire the turfing machine.

However, there’s more to this story—read on!

Wonderturf gets a loan to buy the machine

Having from Wonderturf that they don’t intend to buy the machine, the turfing machine’s

manufacturer offers the company a loan of $50,000. The loan’s conditions are:

• Interest on the loan is r

D

= 8%. This is also the market interest rate.

PFE Chapter 20, Capital structure and valuation page 18

• The loan’s payments in years 1-9 consist of interest only: 8%*50,000 = 4,000. This

interest is an expense for tax purposes for Wonderturf, so that the after-tax cost of the

interest to the company is (1-40%)*4,000 = $2,400.

• At the end of year 10, Wonderturf must repay the loan principal. In this year, the after-

tax cost of the loan to the company is therefore $52,400 (the loan principal plus the after-

tax interest).

The Excel table below shows that the loan to Wonderturf has a positive NPV of $10,736.

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

DE F

Loan to buy machine 50,000

r

D

, loan interest rate

8%

Loan CFs

50,000 <-- =E12

-2,400 <-- =-(1-$B$2)*$E$13*$E$12

-2,400

-2,400

-2,400

-2,400

-2,400

-2,400

-2,400

-2,400

-52,400 <-- =-(1-$B$2)*$E$13*$E$12-E12

Loan NPV 10,736 <-- =E15+NPV(E13,E16:E25)

The Wonderturf financial wizards now conclude that it is worthwhile buying the turfing

machine if Wonderturf takes the loan. Their logic is:

()

(

)()

$4,643 $10,736

$6,093

Value Wonderturf machine financing Value Wonderturf machine Value financing

+= +

=− +

=

Here’s a spreadsheet which shows their calculations:

PFE Chapter 20, Capital structure and valuation page 19

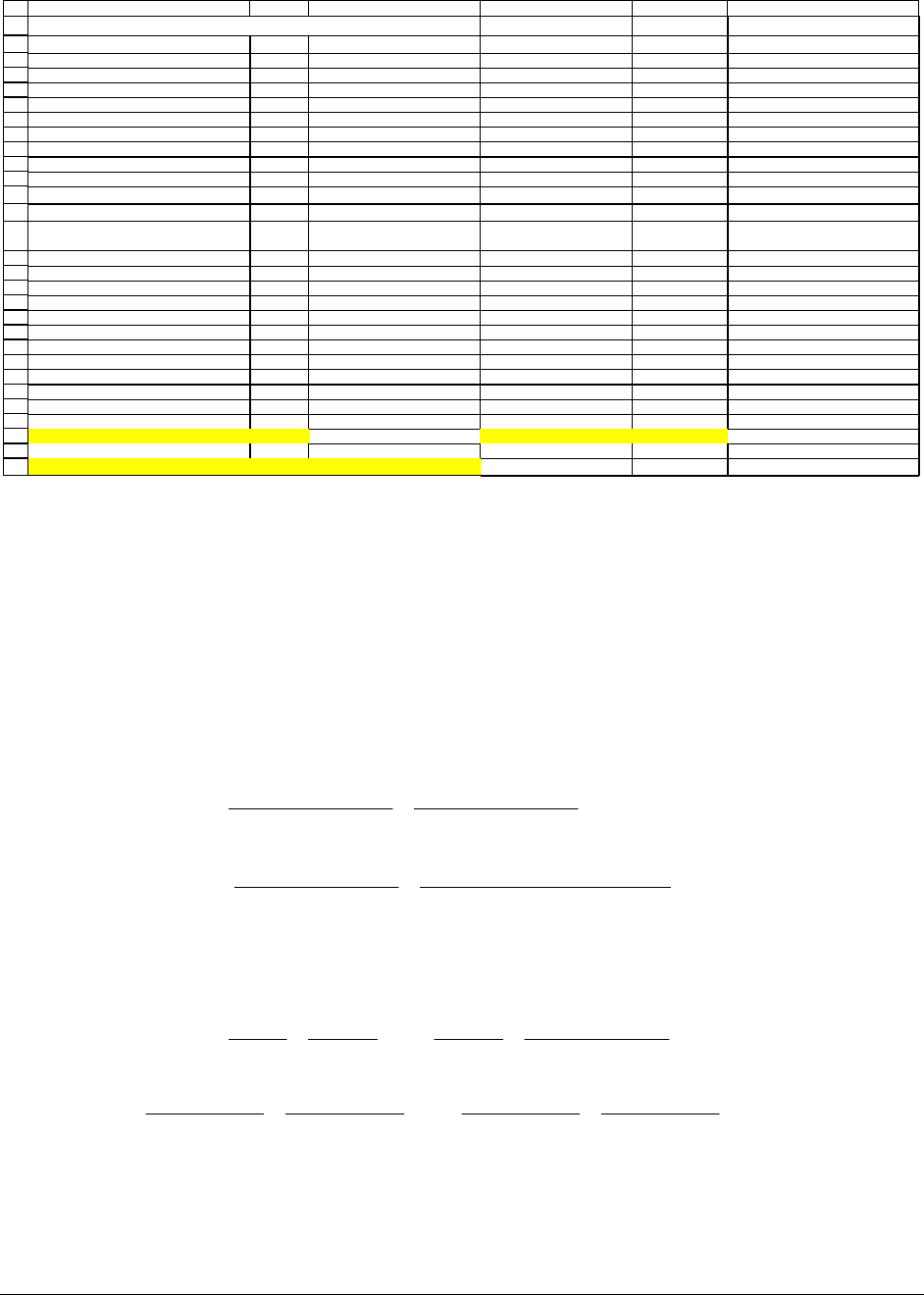

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

ABC DE F

T

C

, corporate tax rate

40%

Machine cost, year 0 100,000

Free cash flow (FCF) calculation

Additional sales, annually 40,000

Additional annual cost of sales 15,000

Annual depreciation 10,000 <-- =B4/10

Annual FCF, years 1-10 19,000 <-- =(1-B2)*(B7-B8-B9)+B9

r

U

, discount rate for machine FCFs

15% Loan to buy machine 50,000

r

D

, loan interest rate

8%

Year

Machine

FCF

Loan CFs

0 -100,000 <-- =-B4 50,000 <-- =E12

1 19,000 <-- =$B$10 -2,400 <-- =-(1-$B$2)*$E$13*$E$12

2 19,000 -2,400

3 19,000 -2,400

4 19,000 -2,400

5 19,000 -2,400

6 19,000 -2,400

7 19,000 -2,400

8 19,000 -2,400

9 19,000 -2,400

10 19,000 -52,400 <-- =-(1-$B$2)*$E$13*$E$12-E12

Machine NPV -4,643 <-- =B15+NPV(B12,B16:B25) Loan NPV 10,736 <-- =E15+NPV(E13,E16:E25)

NPV: Machine + Loan 6,093 <-- =B27+E27

THE WONDERTURF TURFING MACHINE

As you can see in cell B29, the total value of the machine + loan combination is $6,093.

Where does the positive loan NPV come from?

The above analysis shows that the loan to Wonderturf has an NPV of $10,736. If we

analyze this number, we will see that this is exactly the PV of the tax-shields on the loan interest:

()

()

(

)

()

()

()

()

()

2

910

1 40% *4,000 1 40% *4,000

50,000 ...

1.08

1.08

1 40% *4,000 1 40% *4,000 50,000

1.08 1.08

NPV loan

−−

=−−−

−−−

−−

We now split this expression into two parts:

()

() () ()

() () ()

2910

2910

4,000 4,000 4,000 4,000 50,000

50,000 ...

1.08

1.08 1.08 1.08

40%*4,000 40%*4,000 40%*4,000 40%*4,000

...

1.08

1.08 1.08 1.08

NPV loan

−

=−−−−−

+++++

PFE Chapter 20, Capital structure and valuation page 20

The first line above has value 0 (recall from Chapter 5 that a loan and all its repayments

have zero NPV when the discount rate is the loan borrowing rate). The second line above is the

PV of the tax shields on the loan interest. Their value is $10,736:

()

() () ()

2910

40%*4,000 40%*4,000 40%*4,000 40%*4,000

10,736 ...

1.08

1.08 1.08 1.08

NPV loan == + ++ +

Thus the NPV of the loan is the present value of the tax shields on the loan interest

payments.

The Wonderturf result is not surprising!

The second line of Table 20.2 states that the value of a levered company is the sum of the

value of the unlevered company plus the value of the debt tax shields:

(

)

()

1

*

1

LU

Ct

U

t

t

D

V V PV interest taxshields

T Interest

V

r

∞

=

=+

=+

+

∑

This is precisely what we’ve done with our analysis of the Wonderturf turfing machine.

For this machine:

N

()

1

The value of

the machine's

The value of the

cash flows

tax shields from the

loan interest

*

1

4,643 10,736 6,093

L

Ct

U

t

t

D

Vthevalueo

f

the machine when purchased with a loan

TInterest

V

r

∞

=

↑

↑

=

=+

+

=− + =

∑

PFE Chapter 20, Capital structure and valuation page 21

20.4. Why debt is valuable in Lower Fantasia—relevering Potfooler Inc.

For our second example of the effect of financing on firm value, we use a question from a

Finance 101 final exam at Eastern Lower Fantasia State University. As you’ll see it’s a fairly

long question, with many inter-related parts.

6

Here’s the question: Potfooler, Inc. is a well-known Lower Fantasia company. Here are

some facts about the company:

•

Potfooler expects to have an annual free cash flow of $2 million at the end of years 1, 2,

3, … forever. Recall that the free cash flow is the after-tax amount of cash that the

company generates from its business activities.

•

Potfooler currently has 100,000 shares outstanding on the Lower Fantasia stock

exchange. The Potfooler share price is $100 per share.

•

Potfooler currently has no debt. However, a financial analyst has suggested that the

company issue $3,000,000 of perpetual debt and use the proceeds to repurchase shares.

The analyst explains that perpetual debt is debt which has only an annual interest

payment and which has no return of principal.

7

He suggests that this would be

worthwhile for the company, because of the relation

LUC

VVTD

=

+ . The current interest

rate on debt in Lower Fantasia is 8%, and the interest payments on the debt will be made

annually.

Students on the finance exam were asked to answer the following questions:

6

The author’s colleagues at Eastern Lower Fantasia State University love this question because it’s easy to grade. If

a student makes a mistake on any part of the question, then the answers on all subsequent parts of the question will

also be wrong.

7

We discussed this concept in Chapter ???. Such debt is sometimes called a consol.

PFE Chapter 20, Capital structure and valuation page 22

Question 1: What is the current market value of Potfooler?

Answer: Potfooler currently has 100,000 shares outstanding, each of which is worth

$100. Thus the company’s equity value is currently $10,000,000 = $100*100,000. Since the

company has no debt, this is also its market value. In short: $10,000,000

U

V

=

.

Question 2: After Potfooler issues $3,000,000 of debt, what will be its market value?

Answer: Since Lower Fantasia has only a corporate income tax, the relation

LUC

VVTD=+ holds. This means that after the company issues its debt, its market value will be

10,000,000 40%*3,000,000 11,200,000

LUC

VVTD=+ = + = .

Question 3: After Potfooler issues debt of $3,000,000 and uses the proceeds to

repurchase shares, what will be the company’s total equity value, E?

8

Answer: After Potfooler issues the debt and repurchases the shares, the total value of its

equity, E, plus the total value of its debt, D, have to sum to the company’s total market value V

L

.

In short:

11,200,000

But $3,000,000, and therefore:

=11,200,000-3,000,000=8,200,000

L

L

VED

D

E=V -D

=+=

=

8

Notice that up to this point in the exam, we haven’t stated the price at which Potfooler repurchases the shares. This

comes later.