Principles of Finance with Excel (Основы финансов c Excel)

Подождите немного. Документ загружается.

PFE Chapter 20, Capital structure and valuation page 23

Question 4: At what price will Potfooler repurchase its shares?

Answer: By issuing $3 million of debt, Potfooler has raised its total market value by

$1,200,000 (from $10 million to $11.2 million). This increase in value belongs to all the

shareholders. Since there are 100,000 shares outstanding before the share repurchase, this means

that each share’s price increases by

$1,200,000

$12

100,000

= . Thus the answer to this question is that

the share price for repurchase is $112: Of this amount $100 is the share price before the

repurchase, and $12 is the increase in the share price as a result of the debt issue.

Question 5: How many shares will Potfooler repurchase?

Answer: According to the previous question, Potfooler will repurchase its shares at $112

per share. Since the company has issued $3 million in debt to repurchase the shares, this means

that it will repurchase

$3,000,000

26,785.71

$112

=

.

Question 6: What was Potfooler’s cost of equity before the repurchase of shares?

Answer: Potfooler has an annual free cash flow (FCF) of $2,000,000. Thus its unlevered

cost of equity,

()

2,000,000

20%

10,000,000

E

U

FCF

rU

V

== =.

PFE Chapter 20, Capital structure and valuation page 24

Question 7: What is Potfooler’s cost of equity after the repurchase of the shares on

the open market?

Answer: Potfooler issues $3 million in 8% debt in order to repurchase shares. Thus its

annual interest bill is 8%*3,000,000 = $240,000. Since interest is an expense for tax purposes,

the company’s shareholders will have an annual expected cash flow of:

(

)

()

,1

2,000,000 1 40% *240,000

1,856,000

C

Annual equity cash flow after debt issuance FCF T *interest=−−

=−−

=

The value of the equity after the share repurchase is $8,200,000, so that the cost of equity of the

levered company is

()

1,856,000

22.63%

8,200,000

E

rL==.

Question 8: What is Potfooler’s weighted average cost of capital (WACC) before the

repurchase of the shares?

Answer: Recall the definition of the WACC:

()

**1*

EDC

ED

WACC r r T

ED ED

=+−

++

.

The answer to question 8 is easy: Since Potfooler, before the share repurchase, has only equity,

its WACC =

r

U

= 20%.

Question 9: What is Potfooler’s weighted average cost of capital (WACC) after the

repurchase of the shares?

Answer:

PFE Chapter 20, Capital structure and valuation page 25

() ()

()

**1*

8,200,000 3,000,000

22.63%* 8%* 1 40% 17.86%

8,200,000 3,000,000 8,200,000 3,000,000

EDC

ED

WACC r L r T

ED ED

=+−

++

=+−=

++

Question 10: Why is

()

EU

rL r> ?

Answer: Before Potfooler issued its bonds, the only risk borne by shareholders was the

business risk inherent in the company’s free cash flow. After the company issues its bonds,

shareholders have to bear two kinds of risk: business risk

and financial risk. Thus r

E

(L)

represents a discount rate for cash flows which are riskier than the discount rate for the FCFs,

r

U

.

Since riskier cash flows have higher discount rates, it follows that

(

)

EU

rL r>

.

Question 11: Why does the market value of Potfooler increase after the issuance of

the debt and repurchase of the equity?

Answer: By issuing the debt, the shareholders of Potfooler get an additional annual cash

flow—the tax shield on the debt interest. This tax shield is riskless, and its value is:

()

1

*

1

***

*

C

t

t

D

CCD

C

DD

T Interest payment

Present value interest tax shield

r

T Interest payment T r D

TD

rr

∞

=

=

+

===

∑

The present value of the tax shield accounts for the increase in Potfooler’s market value:

N

N

Potfooler's value The PV of

b

efore the debt additional

issuance interest tax

shields

LU C

VV TD

↑↑

=+.

PFE Chapter 20, Capital structure and valuation page 26

Question 12: Why does the WACC decrease after the repurchase?

Answer: After the company issues its debt, it gains an additional cash flow (the tax shield

on the interest). This cash flow is riskless. Thus the

average risk of the company’s total cash

flows—its FCF plus the interest tax shield—decreases. Since the WACC represents the average

riskiness of the company, it decreases.

20.5. Potfooler exam question, second part

Having answered the long exam question of the previous section, students at Eastern

Lower Fantasia State University were asked to put the calculations for questions 1-9 into an

Excel spreadsheet. Here’s the answer:

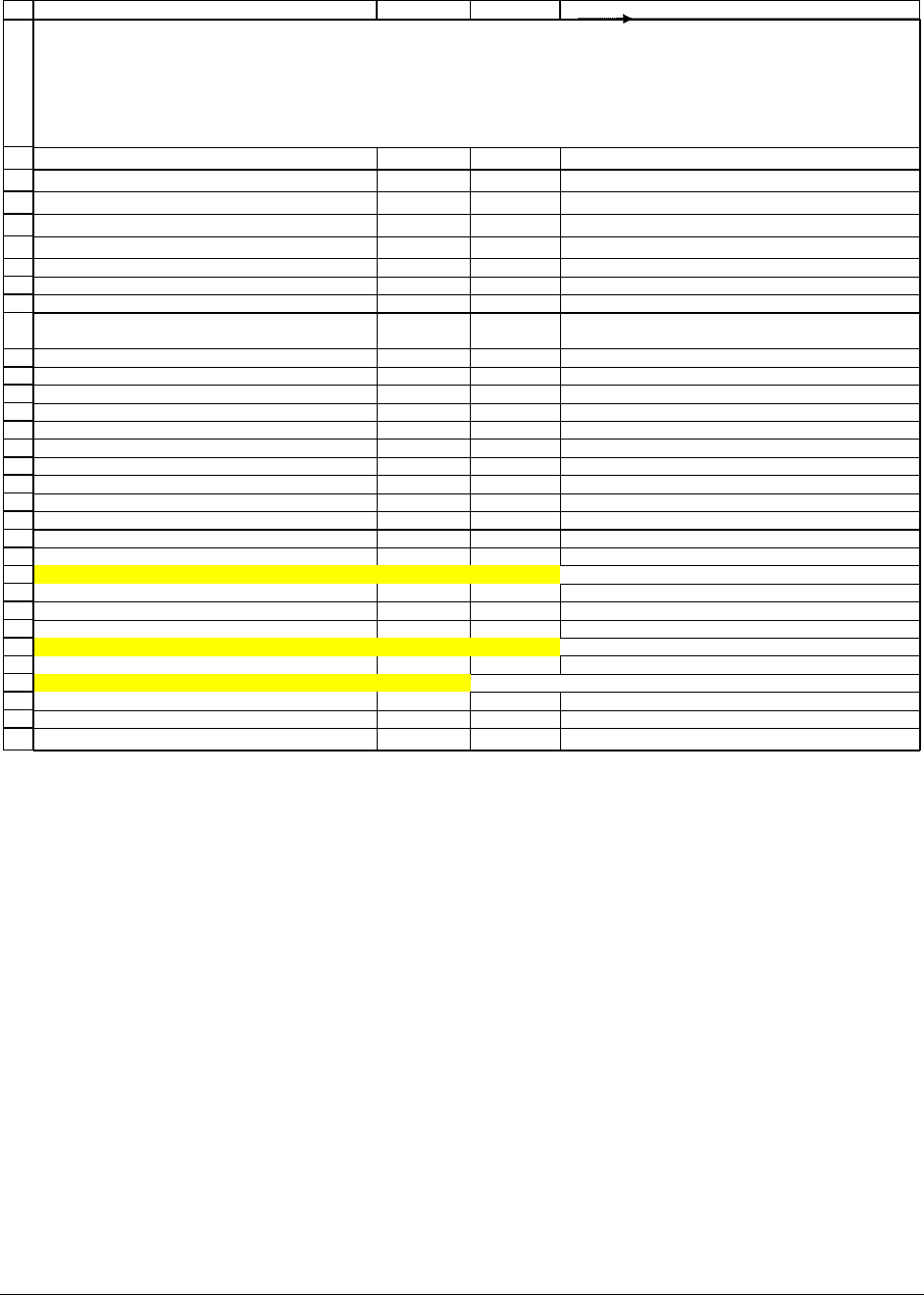

PFE Chapter 20, Capital structure and valuation page 27

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

ABC

Unlevered company

Annual free cash flow (FCF)

$2,000,000

Number of shares 100,000

Price per share $100

Total equity value $10,000,000 <-- =B5*B4

Question 1: V

U

, unlevered value of Potfooler

$10,000,000 <-- =B6

Levered compan

y

Debt issued $3,000,000

Interest rate on debt 8%

T

C

, Lower Fantasia corporate tax rate

40%

Question 2: V

L

, levered value of Potfooler, V

L

= V

U

+ T

C

*D

$11,200,000 <-- =B8+B13*B11

Question 3: Equity value after share repurchase, E = V

L

- D

$8,200,000

Incremental firm value from exchanging

equity by debt = V

L

- V

U

= T

C

*D

$1,200,000 <-- =B13*B11

Incremental firm value on a per-share basis $12 <-- =B16/B4

Question 4: New share value, after repurchase $112 <-- =B5+B17

Question 5: Number of shares repurchased =

[debt used for repurchase]/[new share value]

26,785.71 <-- =B11/B18

Number of shares remaining afte

r

repurchase = original number of shares

minus number of shares repurchased

73,214.29 <-- =B4-B20

Check:

Market value of remaining shares =

number of remaining shares * new share value

$8,200,000 <-- =B21*B18

Question 6: Potfooler's cost of equity when unlevered,

r

U

=FCF/V

U

20.00%

Annual interest costs, before taxes $240,000 <-- =B11*B12

Annual equity cash flow, after interest = FCF - (1-TC)*interest $1,856,000 <-- =B3-(1-B13)*B26

Question 7: Potfooler's cost of equity when levered,

r

E

(L)=[FCF-(1-T

C

)*interest]/[value of equity, E]

22.63% <-- =B27/B22

Question 8: Potfooler's WACC before the debt issuance = r

U

20.00%

Question 9: Potfooler's WACC after the debt issuance

= r

E

(L)*E/(E+D)+r

D

*(1-T

C

)*D/(E+D)

Percentage of equity in Potfooler = E/(E+D) 73.21% <-- =B22/B14

Percentage of debt in Potfooler = D/(E+D) 26.79% <-- =B11/B14

WACC = r

E

(L)*E/(E+D)+r

D

*(1-T

C

)*D/(E+D)

17.86% <-- =B28*B33+B12*(1-B13)*B34

POTFOOLER--DEBT ISSUED TO REPURCHASE SHARES

This spreadsheet enables us to do some interesting analysis:

What happens if the corporate tax rate T

C

= 0%?

When T

C

= 0, leverage doesn’t change the value of the firm. If you put T

C

= 0% into cell

B13 of the previous spreadsheet, you’ll get a demonstration of this. The spreadsheet is given

below, and the analysis follows after the spreadsheet:

PFE Chapter 20, Capital structure and valuation page 28

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

ABC

Unlevered company

Annual free cash flow (FCF)

$2,000,000

Number of shares 100,000

Price per share $100

Total equity value $10,000,000 <-- =B5*B4

Question 1: V

U

, unlevered value of Potfooler

$10,000,000 <-- =B6

Levered compan

y

Debt issued $3,000,000

Interest rate on debt 8%

T

C

, Lower Fantasia corporate tax rate

0%

Question 2: V

L

, levered value of Potfooler, V

L

= V

U

+ T

C

*D

$10,000,000 <-- =B8+B13*B11

Question 3: Equity value after share repurchase, E = V

L

- D

$7,000,000

Incremental firm value from exchanging

equity by debt = V

L

- V

U

= T

C

*D

$0 <-- =B13*B11

Incremental firm value on a per-share basis $0 <-- =B16/B4

Question 4: New share value, after repurchase $100 <-- =B5+B17

Question 5: Number of shares repurchased =

[debt used for repurchase]/[new share value]

30,000.00 <-- =B11/B18

Number of shares remaining afte

r

repurchase = original number of shares

minus number of shares repurchased

70,000.00 <-- =B4-B20

Check:

Market value of remaining shares =

number of remaining shares * new share value

$7,000,000 <-- =B21*B18

Question 6: Potfooler's cost of equity when unlevered,

r

U

=FCF/V

U

20.00%

Annual interest costs, before taxes $240,000 <-- =B11*B12

Annual equity cash flow, after interest = FCF - (1-TC)*interest $1,760,000 <-- =B3-(1-B13)*B26

Question 7: Potfooler's cost of equity when levered,

r

E

(L)=[FCF-(1-T

C

)*interest]/[value of equity, E]

25.14% <-- =B27/B22

Question 8: Potfooler's WACC before the debt issuance = r

U

20.00%

Question 9: Potfooler's WACC after the debt issuance

= r

E

(L)*E/(E+D)+r

D

*(1-T

C

)*D/(E+D)

Percentage of equity in Potfooler = E/(E+D) 70.00% <-- =B22/B14

Percentage of debt in Potfooler = D/(E+D) 30.00% <-- =B11/B14

WACC = r

E

(L)*E/(E+D)+r

D

*(1-T

C

)*D/(E+D)

20.00% <-- =B28*B33+B12*(1-B13)*B34

POTFOOLER--DEBT ISSUED TO REPURCHASE SHARES, corporate tax rate = 0%

• The total value of the company doesn’t change (cell B14) when the amount debt (cell

B11) changes. In a formula:

N

C

When T 0%,

this term is zero

LU C U

VV TD V

↑

=

=+ =

• The company’s equity becomes more risky. That is:

(

)

EU

rL r> . You can see this in cell

B28:

r

E

(L) = 25.14% after the debt is issued as opposed to r

U

= 20%.

PFE Chapter 20, Capital structure and valuation page 29

• The company’s share price doesn’t change. After the issuance of the debt and the

repurchase of the equity, the share price is still $100 (cell B18).

• The company’s WACC doesn’t change. The average riskiness of the company’s cash

flows remains the same:

() ()

()

C

Remember that

in this version of the

question T 0%

**1*

7,000,000 3,000,000

25.14%* 8%* 1 0%

7,000,000 3,000,000 7,000,000 3,000,000

20%

EDC

U

ED

WACC r L r T

ED ED

r

↑

=

=+−

++

=+−

++

==

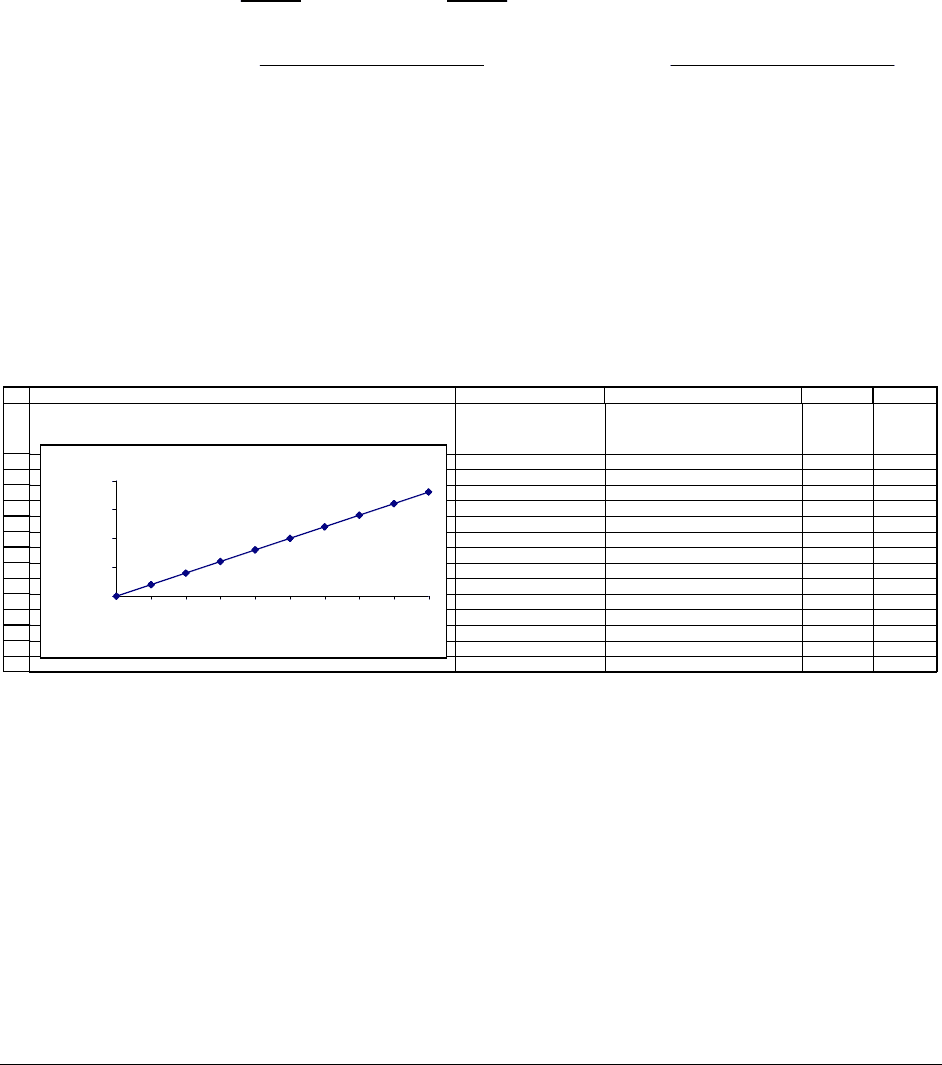

Relate the company’s value to different levels of debt

By making a Data Table (see Chapter ???), we can make the following table and graph:

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

ABCDE

Debt issued

Value of levered firm,

V

L

= V

U

+ T

C

*D

Cost of

equity

r

E

(L)

WACC

0 10,000,000 20.00% 20.00%

1,000,000 10,400,000 20.77% 19.23%

2,000,000 10,800,000 21.64% 18.52%

3,000,000 11,200,000 22.63% 17.86%

4,000,000 11,600,000 23.79% 17.24%

5,000,000 12,000,000 25.14% 16.67%

6,000,000 12,400,000 26.75% 16.13%

7,000,000 12,800,000 28.69% 15.63%

8,000,000 13,200,000 31.08% 15.15%

9,000,000 13,600,000 34.09% 14.71%

Levered value V

L

as a function of firm debt

10,000,000

11,000,000

12,000,000

13,000,000

14,000,000

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

Debt

20.6. Considering personal as well as corporate taxes—the case of XYZ Corp.

In our story about ABC Corp (Arthur and Mom), the capital structure decision mattered

because Lower Fantasia taxes corporations but not individuals. The result is that shareholders

(like Arthur) benefit from having companies borrow instead of doing the borrowing themselves.

PFE Chapter 20, Capital structure and valuation page 30

In this section we tell the story of Upper Fantasia, a country very much like Lower Fantasia, but

with a somewhat different tax system. Upper Fantasia has 3 kinds of taxes:

•

Corporations are subject to a 40% corporate tax rate. We denote this tax rate by T

C

.

•

Individual income derived from shares (this refers to dividends and capital gains on

shares—in the jargon of the Upper Fantasia tax code, this is called “equity income”) is

subject to a 10% tax rate. The equity tax rate is denoted by T

E

.

•

All ordinary income (this term includes individual income derived from bonds; however

it does not include equity income) is subject to a 30% tax rate. We denote this tax rate by

T

D

. When individuals pay interest, they get to deduct the interest payments from their

ordinary income.

As before, our mythical entrepreneur, Arthur XYZ, is trying to figure out how to finance

his purchase of XYZ Corp. His Mom (bless her!) is always available to lend him money. The

questions about the debt are the same as before:

•

Should the purchase of the company be financed with debt?

•

If so, who should borrow—the company or Arthur?

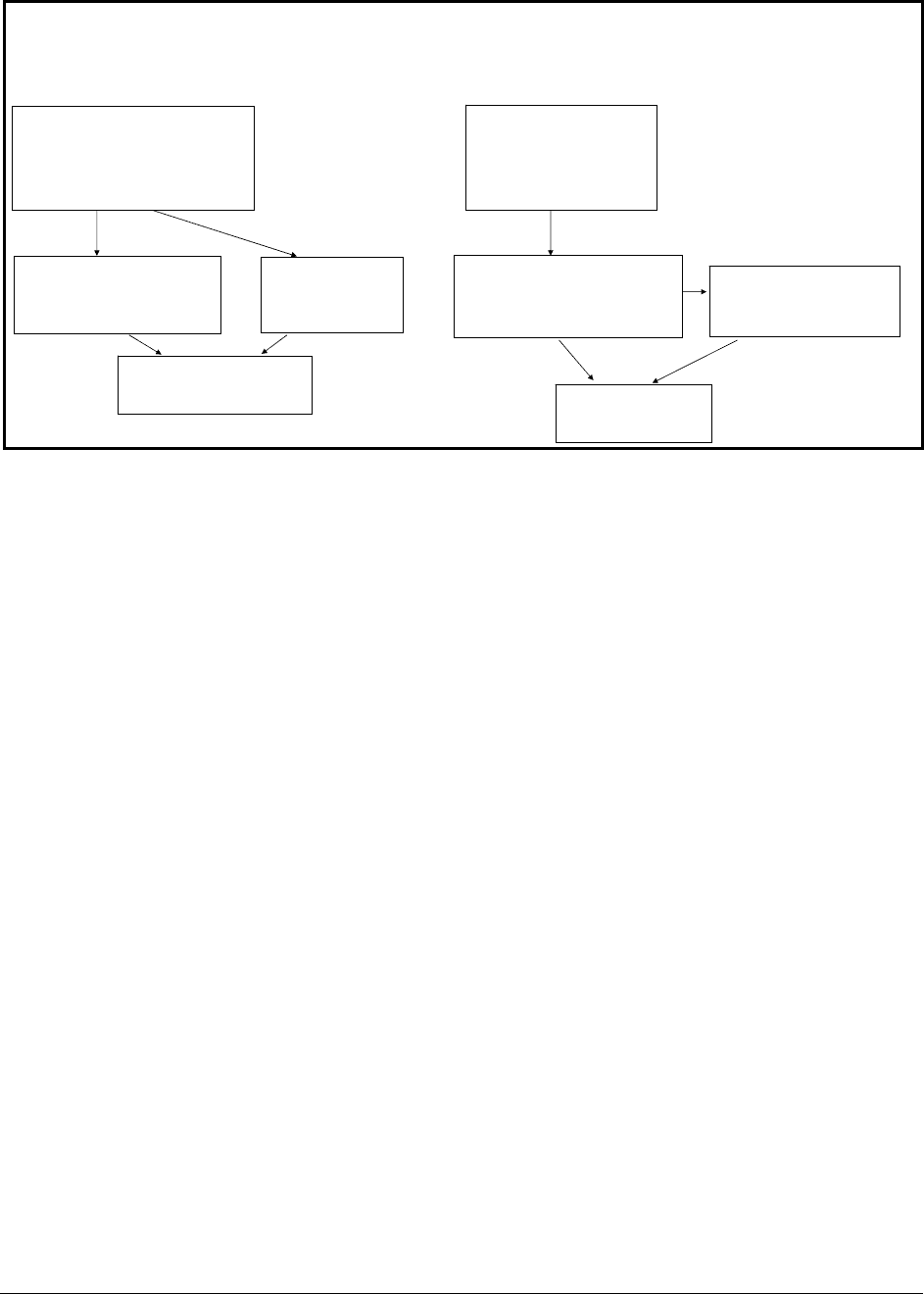

The diagram below explains the cash flows:

PFE Chapter 20, Capital structure and valuation page 31

Alternative A: Company borrows from Arthur's Mom Alternative B: Arthur borrows from Mom

FINANCING ARTHUR'S PURCHASE OF XYZ

Upper Fantasia tax code: Corporate income tax, T

C

= 40%,

Personal taxes: Tax on equity income, T

E

= 10%, Tax on all other income, T

D

= 30%

XYZ Corp. -- Levered

Company has $3,000 of 8% perpetual debt from Arthur's

mother. Corporate income tax, T

C

= 40%.

FCF = $1000 [This is after corporate taxes]

Equity income after interest payment =

$1000 - 8%*3,000*(1-40%) = $856

Paid to Arthur XYZ, sole owner

Arthur XYZ-- sole owner of XYZ's equity.

XYZ pays Arthur $856. Personal tax on equity

income, T

E

= 10% . Arthur pays his mother $240 in

interest. Interest is an ordinary-income expense;

tax rate on ordinary income, T

D

= 30%.

After-tax income = $856*(1-10%) = $770.40

Arthur's mother. Gets $300

interest from Arthur. Personal tax

on interest income, T

D

= 30%.

Annual after-tax income:

8%*$3000*(1-30%) = $168

Family income: Arthur + Mom

Arthur: $ 770.40

Mom: $ 168.00

Total: $ 938.40

XYZ Corp. -- no debt

FCF = $1000 [After corporate taxes.]

Equity income = $1000

Paid to Arthur XYZ, sole owner

Arthur XYZ -- sole owner of XYZ's equity. Borrowed

$3000 of perpetual debt from Mom at 8%. Interest

payments create 30% tax shield.

Personal tax on equity income, T

E

= 10%.

= 30%. Interest is an ordinary-income expense; tax rate

on ordinary income, T

D

= 30%.

Annual income

$

1000

*(

1

10

%)

8

%*

3000

*(

1

30

%)

732

Family income: Arthur + Mom

Arthur: $ 732.00

Mom: $ 168.00

Total: $ 900.00

Arthur's mother. Gets interest from Arthur.

Personal tax on interest income, T

D

= 30%.

Annual income =

8%*$3000*(1-30%) = $168

When the company borrows the money, the total family income is $938.40. This

compares to the total income of $900 when Arthur borrows the money from Mom. So it’s better

in this case for the company to borrow the money.

In order to understand what’s happening, we create a spreadsheet. We’ll have more to

say about this spreadsheet (and the economics underlying it) below, but in the meantime, we

stress its final conclusion

•

Since the total family income (the combined income of Arthur XYZ and his Mom) is

larger when the company borrows than when Arthur borrows (cell B27 versus cell C27),

the company should lever itself, and not Arthur.

•

The advantages of corporate borrowing are considerably less in this case than in the

previous case of ABC Corp. In the previous case corporate leverage of $3,000 added $96

to the family cash flows each year; in the current case it adds only $38.40. The

difference is, of course, the fact that we now have taxes on personal income, which were

absent in the ABC Corp. example.

PFE Chapter 20, Capital structure and valuation page 32

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

ABC D

Computing the family income

T

C

, corporate tax rate

40%

T

E

, personal equity tax rate

10%

T

D

, personal debt tax rate on ordinary income

30%

r

D

, interest rate

8%

D, Debt 3,000

FCF, free cash flow (already after corporate taxes) 1,000

Company

borrows

A

rthur

borrows

FCF, after personal tax 1,000.00 1,000.00

Corporate debt 3,000.00 0.00

Corporate pre-tax interest payment 240.00 0.00

Corporate after-tax interest payment 144.00 0.00 <-- =C13*(1-$B$3)

Payout to equity owners 856.00 1,000.00 <-- =C11-C14

Arthur's income

Pre-tax equity income from XYZ 856.00 1,000.00 <-- =C15

Post-tax equity income from XYZ 770.40 900.00 <-- =C18*(1-$B$4)

Arthur's debt 0.00 3,000.00

Arthur's pre-tax interest payment 0.00 240.00 <-- =$B$6*C20

Arthur's after-tax interest payment 0.00 168.00

Arthur's post-tax income 770.40 732.00 <-- =C19-C22

Mom's pre-tax income 240.00 240.00 <-- =C20*B6

Mom's post-tax income 168.00 168.00 <-- =C25*(1-$B$5)

Total family income 938.40 900.00 <-- =C23+C26

Who should borrow--Arthur or company? Company <-- =IF(B27>C27,"Company",IF(B27<C27,"Arthur","Indifferent"))

Net advantage of corporate debt

(1-T

D

)-(1-T

E

)*(1-T

C

)

0.16

FINANCING ARTHUR'S PURCHASE OF XYZ

Upper Fantasia tax code: Corporate income tax, T

C

= 40%,

Personal taxes: Tax on equity income, T

E

= 10%, Tax on all other income, T

D

=

30%

In order to understand this better, we need some equations:

(

)

(

)

(

)

()()()

Dividend to Arthur Income from

debt to Mom

Arthur's after-tax dividend

Net t

**1*1 **1

**1 1*1

DCEDD

DDEC

Total cash produced by firm FCF r Debt T T r Debt T

FCF r Debt T T T

↑↑

↑

↑

=− − −+ −

⎡⎤

=+ −−− −

⎣⎦

()()()( )( )( )

ax corporate tax-advantage of debt

1 1 * 1 1 30% 1 10% * 1 40% 16%

DCE

In thiscase T T T=− −− − =− −− − =

The term which makes all the difference is