Principles of Finance with Excel (Основы финансов c Excel)

Подождите немного. Документ загружается.

PFE Chapter 19, Capital structure and valuation page 43

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

ABC DEF

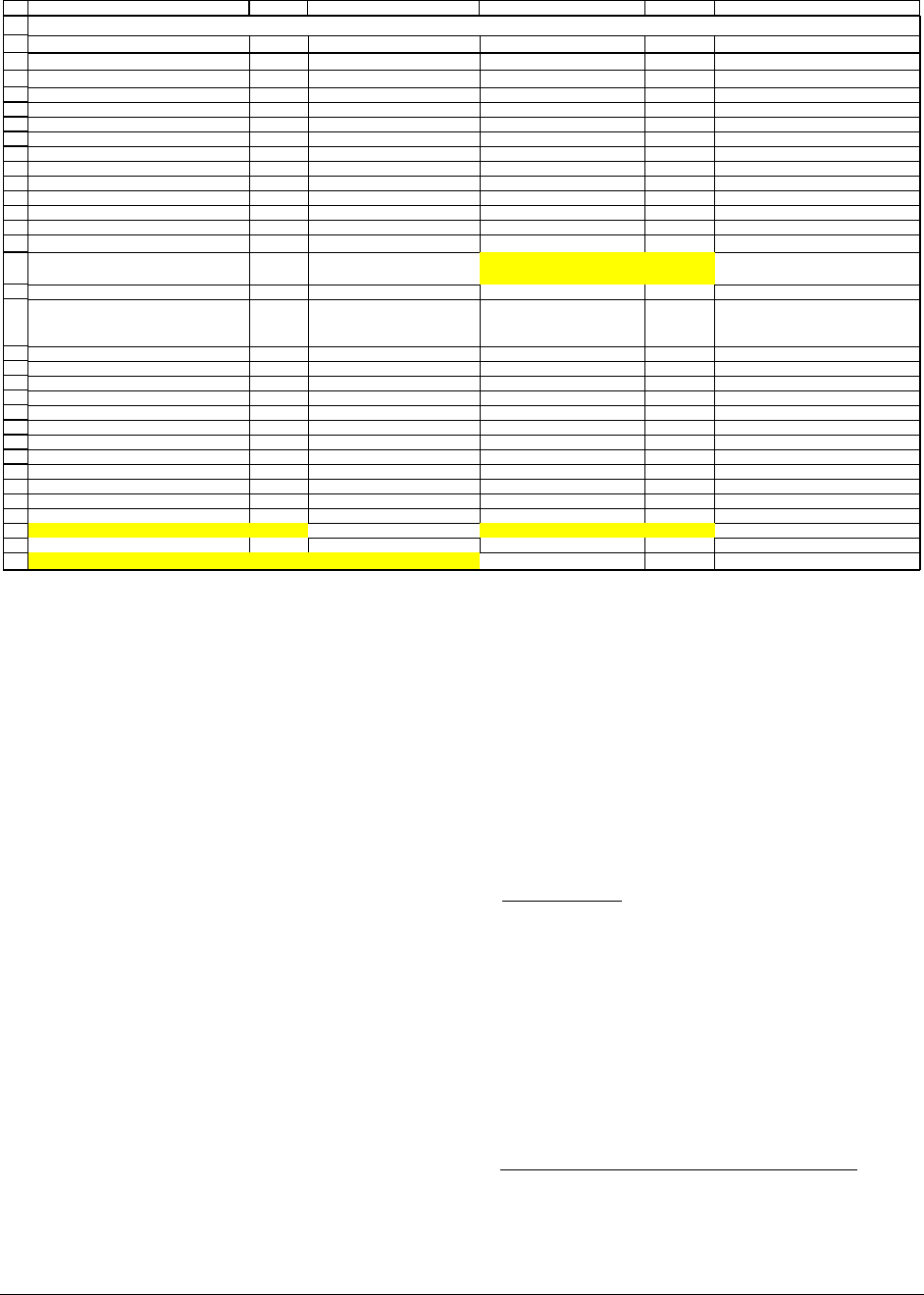

T

C

, corporate tax rate

40%

T

E

, personal tax rate on equity

10%

T

D

, personal tax rate on debt

30%

Machine cost, year 0 100,000

Free cash flow (FCF) calculation

Additional sales, annually 40,000

Additional annual cost of sales 15,000

Annual depreciation 10,000 <-- =B6/10

Annual FCF, years 1-10 19,000 <-- =(1-B2)*(B9-B10-B11)+B11

Discount rate for machine FCFs 15% Loan to buy machine 50,000

r

D

, loan interest rate

8%

Net annual advantage of debt

financing, (1-T

D

)-(1-T

E

)*(1-T

C

)

16% <-- =(1-B4)-(1-B3)*(1-B2)

Year

Machine

FCF

Tax

advantage

of interest

0 -100,000 <-- =-B6

1 19,000 <-- =$B$12 640 <-- =$E$16*$E$15*$E$14

2 19,000 640 <-- =$E$16*$E$15*$E$14

3 19,000 640

4 19,000 640

5 19,000 640

6 19,000 640

7 19,000 640

8 19,000 640

9 19,000 640

10 19,000 640

Machine NPV -4,643 <-- =B19+NPV(B14,B20:B29) Loan NPV 4,801 <-- =E19+NPV(E15*(1-B4),E20:E29)

NPV: Machine + Loan 158 <-- =B31+E31

THE SONDERTURF STURFING MACHINE

In Upper Fantasia debt is not always valuable!

The Lower Fantasia tax system—which has only a corporate tax T

C

but no other taxes on

personal income—always makes it more valuable to finance with debt. You can see this from

the following formula drawn from Figure 20.2, which holds in Lower Fantasia:

()

()

1

*

1

Lower Fantasia

Ct

L

UUU

t

t

D

T Interest

V V PV interest taxshields V V

r

∞

=

=+ =+ >

+

∑

.

The same formula in Upper Fantasia—with its more complicated (but more realistic) tax system

which combines a corporate income tax T

C

with a personal tax on equity income T

E

and a

personal tax on ordinary income T

D

—is given by:

()

(

)

(

)

(

)

()

()

1

11*1*

11

N

D

EC t

Upper Fantasia

LU U

t

t

DD

T T T Interest

V V PV interest taxshields V

Tr

=

⎡⎤

−−− −

⎣⎦

=+ =+

+−

∑

The last expression need not always be positive. For example:

PFE Chapter 19, Capital structure and valuation page 44

(

)

(

)

(

)

()

()

()()()

()()()

()

()

()()()

()()()

()

()

()()()

1

1

1

11*1*

01 1*1 0

11

11*1*

01 1*1 0

11

11*1*

01 1*10

11

N

DEC t

DEC

t

t

DD

N

DEC t

DEC

t

t

DD

N

DEC t

DEC

t

t

DD

TTTInterest

if T T T

Tr

TTTInterest

if T T T

Tr

T T T Interest

if T T T

Tr

=

=

=

⎡⎤

−−− −

⎣⎦

>−−−−>

+−

⎡⎤

−−− −

⎣⎦

=

−−− −=

+−

⎡⎤

−−− −

⎣⎦

<

−−− −<

+−

∑

∑

∑

The conclusion is that in Upper Fantasia, financing with debt need not make a project

more valuable. Suppose, for example, that T

C

= 40%, T

E

= 3%, and T

D

= 50%. Then the

spreadsheet below shows that financing the sturfing machine with debt decreases the NPV:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

ABC DEF

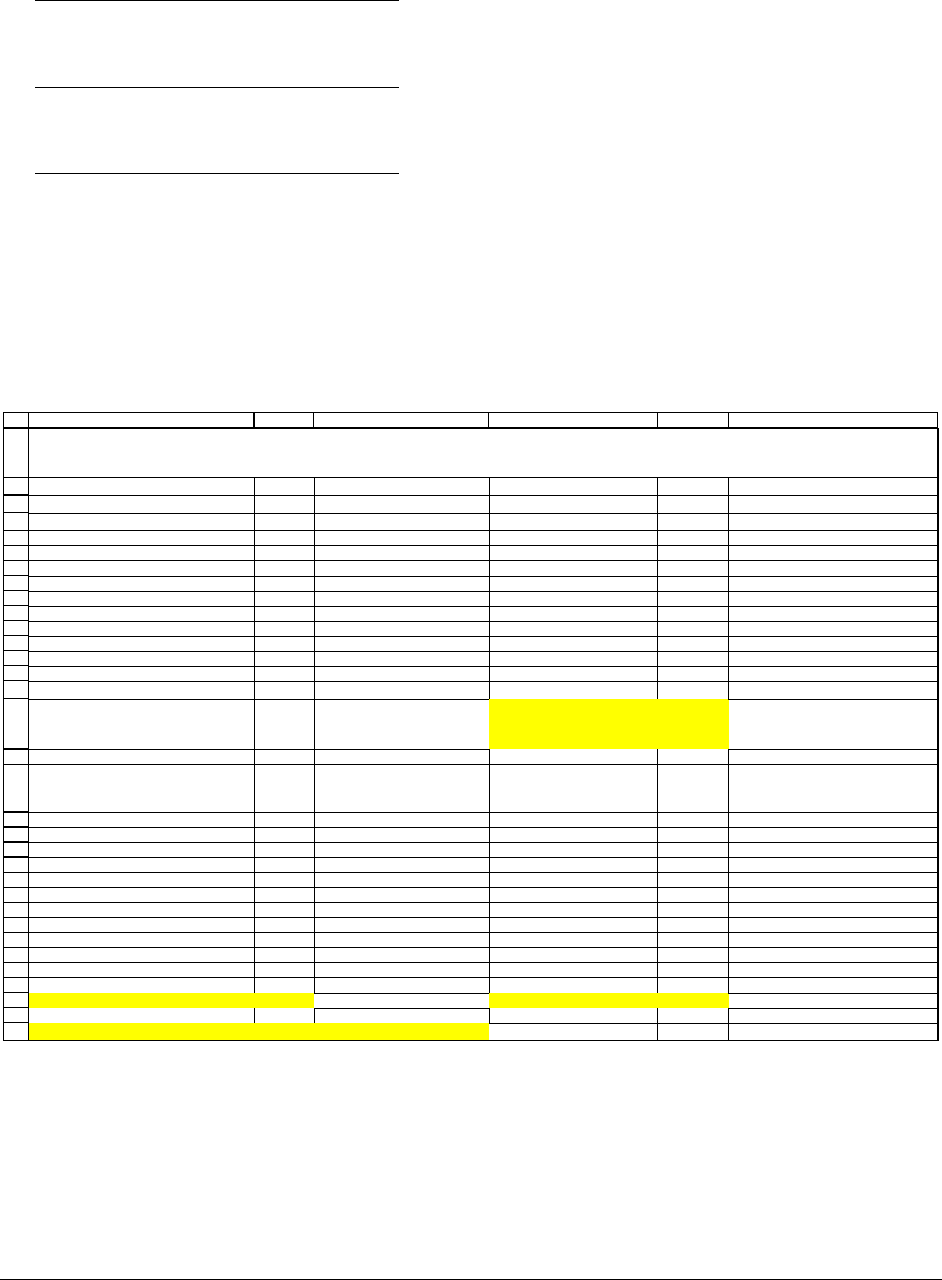

T

C

, corporate tax rate

40%

T

E

, personal tax rate on equity

3%

T

D

, personal tax rate on debt

50%

Machine cost, year 0 100,000

Free cash flow (FCF) calculation

Additional sales, annually 40,000

Additional annual cost of sales 15,000

Annual depreciation 10,000 <-- =B6/10

Annual FCF, years 1-10 19,000 <-- =(1-B2)*(B9-B10-B11)+B11

Discount rate for machine FCFs 15% Loan to buy machine 50,000

r

D

, loan interest rate

8%

Net annual advantage of debt

financing, (1-T

D

)-(1-T

E

)*(1-T

C

)

-8% <-- =(1-B4)-(1-B3)*(1-B2)

Year

Machine

FCF

Tax

advantage

of interest

0 -100,000 <-- =-B6

1 19,000 <-- =$B$12 -328 <-- =$E$16*$E$15*$E$14

2 19,000 -328 <-- =$E$16*$E$15*$E$14

3 19,000 -328

4 19,000 -328

5 19,000 -328

6 19,000 -328

7 19,000 -328

8 19,000 -328

9 19,000 -328

10 19,000 -328

Machine NPV -4,643 <-- =B19+NPV(B14,B20:B29) Loan NPV -2,660 <-- =E19+NPV(E15*(1-B4),E20:E29)

NPV: Machine + Loan -7,304 <-- =B31+E31

THE SONDERTURF STURFING MACHINE

different taxes make debt disadvantageous!

PFE Chapter 19, Capital structure and valuation page 45

20.9. Relevering Smotfooler Inc., an Upper Fantasia company

In Section 20.4 we offered a question from a Finance 101 exam at Eastern Lower

Fantasia State University. This section offers a similar question from an exam at Upper Fantasia

University (their football team is called the Ufus).

Here’s the question: Smotfooler, Inc. is a well-known Upper Fantasia company. Here

are some facts about the company:

• Smotfooler expects to have an annual free cash flow of $2 million at the end of years 1, 2,

3, … forever. Recall that the free cash flow is the after-tax amount of cash that the

company generates from its business activities.

• Smotfooler currently has 100,000 shares outstanding on the Upper Fantasia stock

exchange. The Smotfooler share price is $100 per share.

• Smotfooler currently has no debt. However, a financial analyst has suggested that the

company issue $3,000,000 of perpetual debt and use the proceeds to repurchase shares.

The current interest rate on debt in Upper Fantasia is 8%, and the interest payments on

the debt will be made annually.

• Tax rates in Upper Fantasia are: T

C

= 40%, T

D

= 30%, T

E

= 10%.

Students on the finance exam were asked to answer the following questions:

Question 1: What is the current market value of Smotfooler?

Answer: Smotfooler currently has 100,000 shares outstanding, each of which is worth

$100. Thus the company’s equity value is currently $10,000,000 = $100*100,000. Since the

company has no debt, this is also its market value. In short: $10,000,000

U

V

=

.

PFE Chapter 19, Capital structure and valuation page 46

Question 2: After Smotfooler issues $3,000,000 of debt, what will be its market

value?

Answer: Since Upper Fantasia has only a corporate income tax, the relation

LU

VVTD=+ holds, where:

()()

(

)

()

()

(

)

(

)

()

1 1 * 1 1 30% 1 40% 1 10%

22.86%

1 1 30%

DCE

D

TTT

T

T

−−− − − −− −

== =

−−

.

(See also cell B7 on the spreadsheet below).

This means that after the company issues its debt, its market value will be

10,000,000 22.86%*3,000,000 10,685,714

LU

VVTD=+ = + = .

Question 3: After Smotfooler issues debt of $3,000,000 and uses the proceeds to

repurchase shares, what will be the company’s total equity value, E?

Answer: After Potfooler issues the debt and repurchases the shares, the total value of its

equity, E, plus the total value of its debt, D, have to sum to the company’s total market value V

L

.

In short:

10,685,714

But $3,000,000, and therefore:

L

VED

D

E =10,685,714-3,000,000=7,685,714

==+

=

Question 4: At what price will Smotfooler repurchase its shares?

Answer: By issuing $3 million of debt, Smotfooler has raised its total market value by

$685,714 (from $10 million to $10,685,714). This increase in value belongs to all the

shareholders. Since there are 100,000 shares outstanding before the share repurchase, this means

PFE Chapter 19, Capital structure and valuation page 47

that each share’s price increases by

$685,714

$6.86

100,000

= . Thus the answer to this question is that

the share price for repurchase is $106.86. Of this amount $100 is the share price before the

repurchase, and $6.86 is the increase in the share price as a result of the debt issue.

Question 5: How many shares will Smotfooler repurchase?

Answer: According to the previous question, Smotfooler will repurchase its shares at

$106.86 per share. Since the company has issued $3 million in debt to repurchase the shares, this

means that it will repurchase

$3,000,000

28,074.87

$106.86

=

.

Question 6: What was Smotfooler’s cost of equity before the repurchase of shares?

Answer: Smotfooler has an annual free cash flow (FCF) of $2,000,000. Thus its

unlevered cost of equity,

()

2,000,000

20%

10,000,000

EU

U

FCF

rU r

V

== = = .

Question 7: What is Smotfooler’s cost of equity after the repurchase of the shares

on the open market?

Answer: Smotfooler issues $3 million in 8% debt in order to repurchase shares. Thus its

annual interest bill is 8%*8,000,000 = $240,000. Since interest is an expense for tax purposes,

the company’s shareholders will have an annual expected cash flow of:

(

)

()

,1

2,000,000 1 40% *240,000

1,856,000

C

Annual equity cash flow after debt issuance FCF T *interest=−−

=−−

=

PFE Chapter 19, Capital structure and valuation page 48

The value of the equity after the share repurchase is $7,685,714, so that the cost of equity of the

levered company is

()

1,856,000

24.15%

7,685,714

E

rL==.

Note from Figure 20.4. that there’s another way to do this calculation:

() ( ) ( )

()()

11

3,000,000

20% 20% 1 22.86% 8% 1 40% 24.15%

7,685,714

EUU DC

D

rL r r T r T

E

=+ −− − =⎡⎤

⎣⎦

=+ − − − =

⎡⎤

⎣⎦

Question 8: What is Smotfooler’s weighted average cost of capital (WACC) before

the repurchase of the shares?

Answer: Recall the definition of the WACC:

() ()

**1*

EDC

ED

WACC r L r T

ED ED

=+−

++

.

The answer to question 8 is easy: Since Smotfooler, before the share repurchase, has only

equity, its WACC = r

U

= 20%.

Question 9: What is Smotfooler’s weighted average cost of capital (WACC) after

the repurchase of the shares?

Answer:

() ()

()

**1*

7,685,714 3,000,000

24.15%* 8%* 1 40% 18.72%

7,685,714 3,000,000 7,685,714 3,000,000

EDC

ED

WACC r L r T

ED ED

=+−

++

=+−=

++

PFE Chapter 19, Capital structure and valuation page 49

Question 10: Why is

()

EU

rL r> ?

Answer: Before Smotfooler issued its bonds, the only risk borne by shareholders was the

business risk inherent in the company’s free cash flow. After the company issues its bonds,

shareholders have to bear two kinds of risk: business risk and financial risk. Thus r

E

(L)

represents a discount rate for cash flows which are riskier than the discount rate for the FCFs, r

U

.

Since riskier cash flows have higher discount rates, it follows that

(

)

EU

rL r>

.

Question 11: Why does the market value of Smotfooler increase after the issuance

of the debt and repurchase of the equity?

Answer: By issuing the debt, Smotfooler increases the amount of cash it produces by

()()()

11*1*

DCE

T T T Interest payment−−− −⎡⎤

⎣⎦

for every year which it has debt. This additional

cash flow is riskless. Since the holders of riskless cash flows in Upper Fantasia use a discount

rate of

()

1*

D

D

Tr−

to value the cash flows, it follows that:

(

)

(

)

(

)

()

()

()()()

()

()()()

()

()

()

()

()

N

1

11*1

1

11*1*

-

11

11*1

1

11*1

**

1

DCE

D

DCE

t

t

DD

DCE

DD

DCE

D

DD

T

TTT

T

T T T Interest payment

Value of additional debt related cash flows

Tr

TTT

Interest payment

Tr

TTT

rD T D

Tr

∞

=

↑

=

−−− −

−

−−− −⎡⎤

⎣⎦

=

+−

−−− −

=

−

−−− −

==

−

∑

The present value of the tax shield accounts for the increase in Smotfooler’s market value:

N

N

The PV of

Smotfooler's value

additional

before the debt

debt-related

issuance

cash flows

LU

VV TD

↑

↑

=+.

PFE Chapter 19, Capital structure and valuation page 50

Question 12: Does debt always increase corporate value in Upper Fantasia?

Answer: No. It depends on the sizes of the three tax rates T

C

, T

D

, and T

E

. In the example

below, there is a net tax disadvantage to debt—by issuing debt, Smotfooler lowers its market

value and raises its WACC:

1

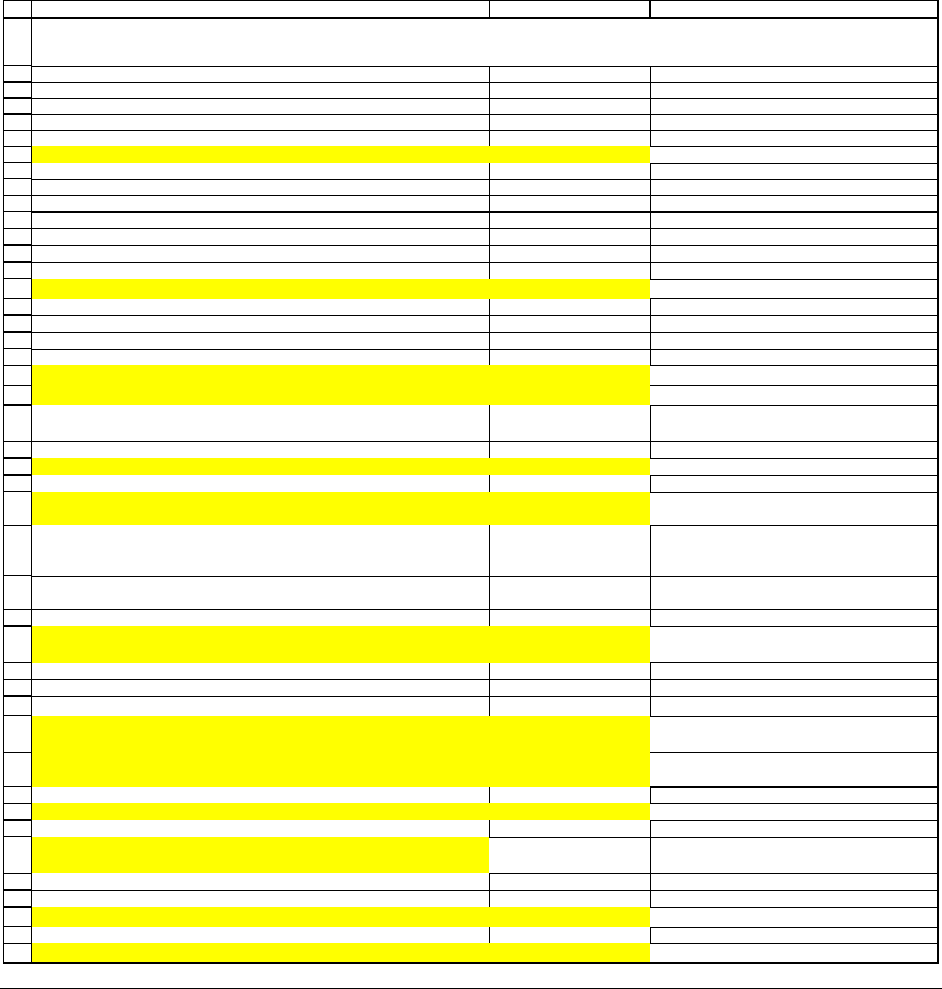

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

ABC

Upper Fantasia tax system

T

C

,

U

pper

F

an

t

as

i

a corpora

t

e

t

ax ra

t

e

40

%

T

E

,

U

pper

F

an

t

as

i

a persona

l

t

ax ra

t

e on equ

it

y

i

ncome

10

%

T

D

,

U

pper

F

an

t

as

i

a persona

l

t

ax ra

t

e on or

di

nary

i

ncome

30

%

A

nnua

l

d

e

bt

a

d

van

t

age:

(

1

-

T

D

)

-

(

1

-

T

E

)*(

1

-

T

C

)

16

%

<-- =

(

1-B5

)

-

(

1-B4

)*(

1-B3

)

PV

o

f

d

e

bt

a

d

van

t

age:

T

=

[(

1

-

T

D

)

-

(

1

-

T

E

)*(

1

-

T

C

)]/(

1

-

T

D

)

22.86

%

<-- =B6

/(

1-B5

)

Unlevered company

Annual free cash flow (FCF)

$2,000,000

Number of shares 100,000

Price per share $100

Total equity value $10,000,000 <-- =B12*B11

Question 1: V

U

, unlevered value of Smotfooler

$10,000,000 <-- =B13

Levered company

Debt issued $3,000,000

Interest rate on debt 8%

Question 2: V

L

, levered value of Smotfooler, V

L

= V

U

+ T*D

$10,685,714 <-- =B15+B7*B18

Question 3: Equity value after share repurchase, E = V

L

- D

$7,685,714

Incremental firm value from exchanging

equity by debt = V

L

- V

U

= T*D

$685,714 <-- =B20-B15

Incremental firm value on a per-share basis $7 <-- =B22/B11

Question 4: New share value, after repurchase $106.86 <-- =B12+B23

Question 5: Number of shares repurchased =

[debt used for repurchase]/[new share value]

28,074.87 <-- =B18/B24

Number of shares remaining after

repurchase = original number of shares

minus number of shares repurchased

71,925.13 <-- =B11-B26

Check: Market value of remaining shares =

number of remaining shares * new share value

$7,685,714 <-- =B27*B24

Question 6: Smotfooler's cost of equity when unlevered,

r

U

=FCF/V

U

20.00%

Annual interest costs, before taxes $240,000 <-- =B18*B19

Annual equity cash flow, after interest = FCF - (1-T

C

)*interest

$1,856,000 <-- =B10-(1-B3)*B32

Question 7: Smotfooler's cost of equity when levered,

r

E

(L)=[FCF-(1-T

C

)*interest]/[value of equity, E]

24.15% <-- =B33/B28

Note: See formula in row 44 below for another

way to compute the levered cost of equity

Question 8: Smotfooler's WACC before the debt issuance = rU 20.00%

Question 9: Smotfooler's WACC after the debt issuance

= r

E

(L)*E/(E+D)+r

D

*(1-TC)*D/(E+D)

Percentage of equity in Smotfooler = E/(E+D) 71.93% <-- =B28/B20

Percentage of debt in Smotfooler = D/(E+D) 28.07% <-- =B18/B20

WACC = r

E

(L)*E/(E+D)+r

D

*(1-T

C

)*D/(E+D)

18.72% <-- =B34*B40+B19*(1-B3)*B41

Additional formula: r

E

(L)=r

U

+[r

U

*(1-T)-r

D

*(1-T

C

))*D/E

24.15% <-- =B30+(B30*(1-B7)-B19*(1-B3))*B18/B21

SMOTFOOLER--DEBT ISSUED TO REPURCHASE SHARES

Smotfooler is located in Upper Fantasia

PFE Chapter 19, Capital structure and valuation page 51

20.10. Is there really an advantage to debt?

In this chapter we’ve laid out the theory of capital structure. We can answer the question

of the importance of capital structure in several ways:

Method 1: What are the relevant tax rates T

C

, T

D

, T

E

?

As you can see, the value of XYZ Corp. is critically dependent on 2 factors:

•

r

U

, the risk-adjusted rate of return for the free cash flows. This rate is unaffected by the

capital structure, since the free cash flows are operating cash flows and do not depend on

the financing of the firm.

•

()()()

111

D

CE

TTT−−− −--the relative after-tax costs of debt versus equity income.

Looking at this second parameter, we examine several cases. In the case below, the anticipated

dividend yield of 2% is taxed at 40% while the anticipated capital gains yield of 6% is taxed at

10%. The equity tax rate is 17.5%, and the net tax advantage of debt over equity is 8.02%:

1

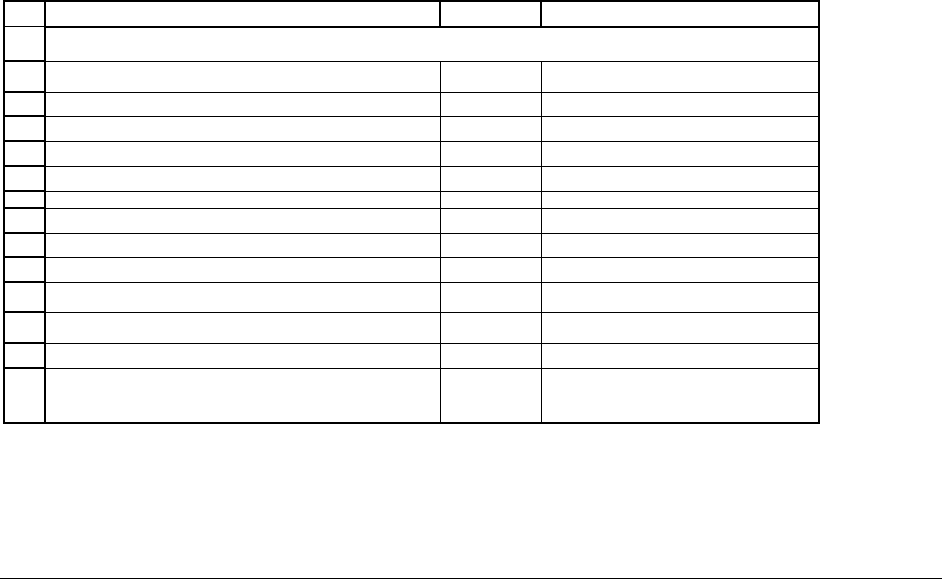

2

3

4

5

6

7

8

9

10

11

12

13

14

ABC

Corporate tax rate, T

C

37%

Anticipated equity tax

Tax rate

Dividend yield 2.00% 40%

Capital gains yield 6.00% 10%

Net after-tax yield 6.60% <-- =B5*(1-C5)+B6*(1-C6)

Before tax yield 8.00% <-- =B5+B6

Personal tax rate on equity income, T

E

17.50% <-- =1-B8/B9

Personal tax rate on ordinary income, T

D

40.00%

Tax advantage of debt

over equity: (1-T

D

)-(1-T

C

)*(1-T

E

)

8.02% <-- =(1-B12)-(1-B2)*(1-B11)

WHAT ARE THE RELATIVE TAX EFFECTS

With a somewhat different yield and tax configuration there is actually a net tax

disadvantage to debt:

PFE Chapter 19, Capital structure and valuation page 52

1

2

3

4

5

6

7

8

9

10

11

12

13

14

ABC

Corporate tax rate, T

C

37%

Anticipated equity tax

Tax rate

Dividend yield 0.00% 40%

Capital gains yield 6.00% 0%

Net after-tax yield 6.00% <-- =B5*(1-C5)+B6*(1-C6)

Before tax yield 6.00% <-- =B5+B6

Personal tax rate on equity income, T

E

0.00% <-- =1-B8/B9

Personal tax rate on ordinary income, T

D

40.00%

Tax advantage of debt

over equity: (1-T

D

)-(1-T

C

)*(1-T

E

)

-3.00% <-- =(1-B12)-(1-B2)*(1-B11)

WHAT ARE THE RELATIVE TAX EFFECTS

Below you will see a third case in which only corporate income is taxed. In this case

there is an overwhelming advantage to debt financing:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

ABC

Corporate tax rate, T

C

37%

Anticipated equity tax

Tax rate

Dividend yield 5.00% 0%

Capital gains yield 0.00% 0%

Net after-tax yield 5.00% <-- =B5*(1-C5)+B6*(1-C6)

Before tax yield 5.00% <-- =B5+B6

Personal tax rate on equity income, T

E

0.00% <-- =1-B8/B9

Personal tax rate on ordinary income, T

D

0.00%

Tax advantage of debt

over equity: (1-T

D

)-(1-T

C

)*(1-T

E

)

37.00% <-- =(1-B12)-(1-B2)*(1-B11)

WHAT ARE THE RELATIVE TAX EFFECTS

Method 2: What’s the evidence in firm behavior?

Instead of asking whether tax rates support a net tax advantage, we can also look at

different firms. We can ask whether in a particular industry there is a consistent behavior

towards debt. The answer is no, as you will see in Chapter 20. As you will see in Chapter 20,