Principles of Finance with Excel (Основы финансов c Excel)

Подождите немного. Документ загружается.

PFE Chapter 12, Appendix: The efficient frontier with more than two assets Page 48

Exercises for Appendix 2

All 3 problems relate to the following statistics for stocks ABC, QPD, and XYZ:

1

2

3

4

5

6

7

8

9

10

ABCD

ABC QPD

X

YZ

Average return 22.00% 17.50% 30.00%

Variance 0.20.050.17

Standard deviation 44.72% 22.36% 41.23%

Correlations

Corr(ABC,QPD) 0.05

Corr(ABC,XYZ) -0.1

Corr(QPD,XYZ) 0.5

RETURN STATISTICS FOR 3 STOCKS

A1. Find the average return and standard deviation of a portfolio composed of 50% of stock

ABC, 20% of stock QPD and 30% of stock XYZ.

A.2. Find the minimum variance portfolio and its statistics.

A.3. Find the portfolio having maximum return given that the portfolio standard deviation is

30%.

PFE, Chapter 13: The CAPM and SML page 1

CHAPTER 13: THE CAPITAL ASSET

PRICING MODEL (CAPM)

*

this version: December 2002

Chapter contents

Overview......................................................................................................................................... 2

13.1. Risky portfolios and the riskless asset ..................................................................................3

13.2. Three points on the capital market line (CML)—exploring optimal investment

combinations ................................................................................................................................. 13

13.3. Computing the market portfolio M: the Sharpe ratio......................................................... 17

13.4. The security market line (SML): A remarkable fact.......................................................... 21

Summing up.................................................................................................................................. 26

EXERCISES ................................................................................................................................. 28

Appendix: The CAPM with 3 or more assets .............................................................................. 31

*

Notice: This is a preliminary draft of a chapter of Principles of Finance with Excel by Simon Benninga

(benninga@wharton.upenn.edu

). Check with the author before distributing this draft (though you will probably get

permission). Make sure the material is updated before distributing it. All the material is copyright and the rights

belong to the author.

PFE, Chapter 13: The CAPM and SML page 2

Overview

In this chapter we add a risk-free asset to the portfolio problem discussed in Chapter 12.

Adding this asset gives the investor new possibilities: She can invest either in stocks, or in the

risk-free asset, or in some combination of the two. These new investment possibilities allow the

investor to achieve superior returns. The addition of a risk-free asset to the portfolio of risk

assets leads to four new concepts:

• The capital market line (CML) is the set of all optimal investment portfolios for an

investor. A portfolio on the CML is a combination of the risk-free asset and the risky

assets.

• The market portfolio (denoted by the letter M) is the best portfolio of risky assets

available to the investor.

• The security market line (SML) describes the relation between the expected returns of

any asset and the asset’s risk.

• Beta (denoted by the Greek letter

β

) is a measure of the asset’s risk used in the SML.

Finance concepts used

• Portfolios, risk-free asset

• Capital market line (CML)

• Beta, security market line (SML)

• Sharpe ratio

Excel functions used

• VarP, StdevP, Sqrt

PFE, Chapter 13: The CAPM and SML page 3

• Sophisticated graphing

• Solver

13.1. Risky portfolios and the riskless asset

We start by considering a portfolio problem of the kind dealt with in Chapter 12. There

are two risky assets, Stock A and Stock B. Now suppose there exists a risk-free asset—an asset

which gives an annual interest payment with certainty. You can think of this asset as being a

savings account in a bank or a government bond. In the examples of this section, we’ll suppose

that the risk-free asset gives a 2% annual return. we’ll denote the return on the risk-free asset by

r

f

. The first few lines of the following spreadsheet gives you all the details:

PFE, Chapter 13: The CAPM and SML page 4

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

ABC DE

Stock A Stock B

Average return 7.00% 15.00%

Variance 0.0064 0.0196

Sigma 8.00% 14.00%

Covariance of returns 0.00

Correlation 0.10

Risk-free rate, r

f

2%

Round dot portfolio

•

A 0.9

B 0.1

Mean 7.80% <-- =B29*$B$3+(1-B29)*$C$3

Sigma 7.47%

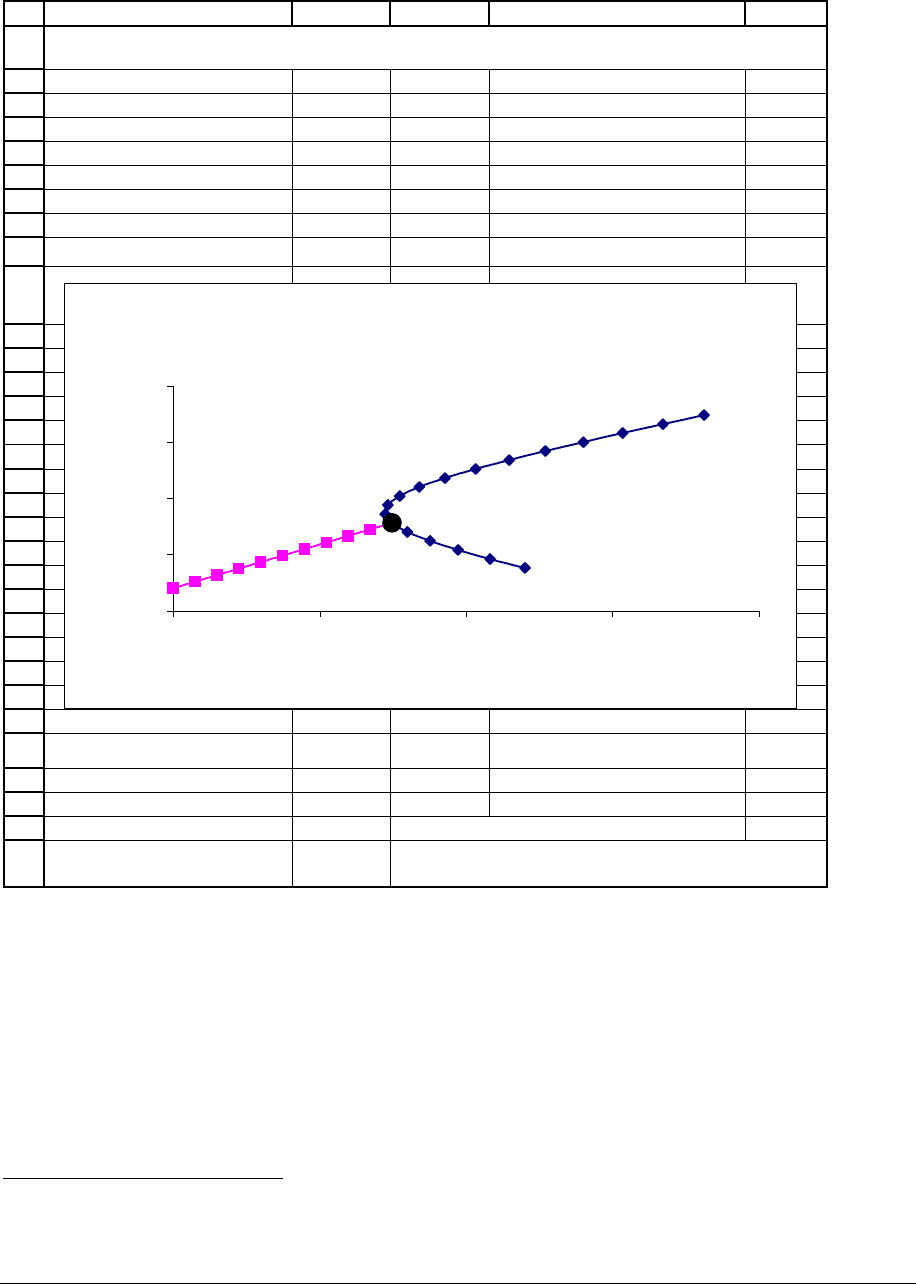

TWO STOCKS AND A RISK-FREE ASSET

<-- =SQRT(B29^2*$B$4+(1-B29)^2*$C$4

+2*B29*(1-B29)*$B$6)

Expected Return and Standard Deviation of Portfolio

Return

0%

5%

10%

15%

20%

0% 5% 10% 15% 20%

Standard deviation of portfolio return,

σ

p

Expected portfolio return, E(r

p

)

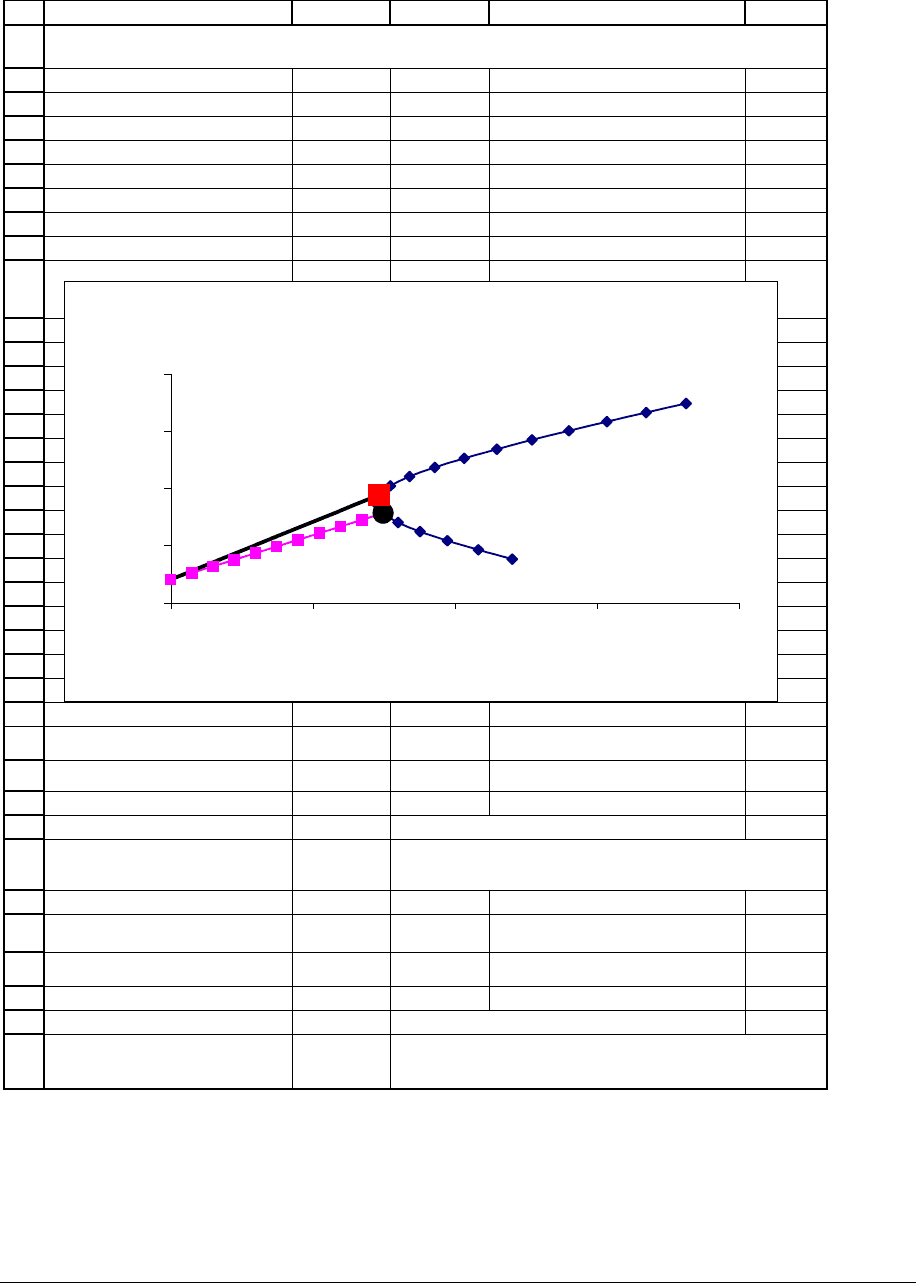

The curved line gives the portfolio mean and standard deviation of combinations of Stock

A and Stock B.

1

The straight line shows the mean and standard deviation of portfolio

combinations of the risk-free asset (which returns r

f

= 2%) and a specific portfolio of risky

assets, denoted by round dot

•).

1

This was illustrated in Chapters 11 and 12.

PFE, Chapter 13: The CAPM and SML page 5

Notice that rows 29-32 give you information about the round dot portfolio •: It is

composed of 90% stock A and 10% stock B, and it has expected return 7.8% and standard

deviation of return 7.47%.

Computing a point on the straight line

In the spreadsheet below we indicate two points on the straight line which connects the

risk-free rate r

f

and the round dot portfolio

•

. Each point represents a portfolio which is partly

invested in the risk free asset and partly in the portfolio

•

. Take a look, and then after the

spreadsheet we’ll show you how to calculate the mean and standard deviation of the points on

the line.

PFE, Chapter 13: The CAPM and SML page 6

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

ABC DE

Stock A Stock B

Average return 7.00% 15.00%

Variance 0.0064 0.0196

Sigma 8.00% 14.00%

Covariance of returns 0.00

Correlation 0.10

Risk-free rate 2%

TWO STOCKS AND A RISK-FREE ASSET

Expected Return and Standard Deviation of Portfolio

Return

0%

2%

4%

6%

8%

10%

12%

14%

16%

0% 5% 10% 15% 20%

Standard deviation of portfolio return,

σ

p

Expected portfolio return, E(r

p

)

p

q

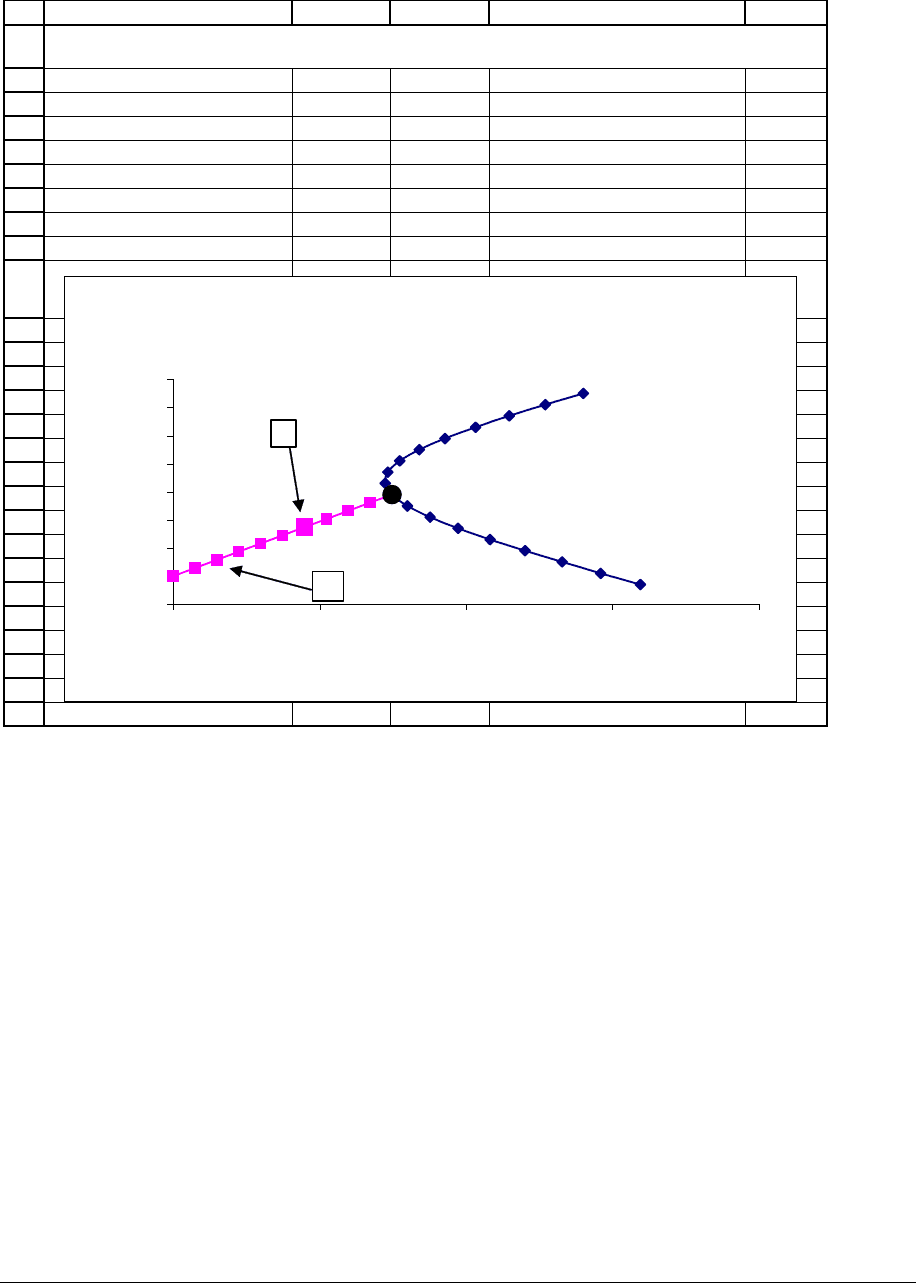

The “round-dot portfolio”

• is composed of an investment 90% in A and 10% in B.

What about portfolio p? p is a portfolio invested 60% in the “round-dot portfolio” and 40% in

the risk-free asset. To compute the returns of this portfolio, we use the following equations:

()

N

()()

N

Percent in

Percent in

"round-dot"

risk-free asset

portfolio

Percent in

"round-dot"

portfolio

1 * 60%*7.8% 40%* 2% 5.48%

60%* 7.47% 5.48%

p round dot f

p round dot

Er x Er x r

x

σσ

−

↑

↑

−

↑

=+−=+=

===

In a similar fashion portfolio q—invested 20% in the “round-dot” portfolio and 80% in

the risk-free asset—has statistics:

PFE, Chapter 13: The CAPM and SML page 7

()

N

()()

N

Percent in

Percent in

"round-dot"

risk-free asset

portfolio

Percent in

"round-dot"

portfolio

1 * 20% *7.8% 80%*2% 3.16%

20%*7.47% 1.49%

q round dot f

q round dot

Er x Er x r

x

σσ

−

↑

↑

−

↑

=+−=+=

===

A statistical note

The equations used in the last calculation follow from our lessons in portfolio statistics in

Chapter 11. Suppose the investor invests a percentage of her wealth x in a portfolio A of risky

assets which has expected return E(r

A

) and standard deviation of return

σ

A

. Suppose she invests

the rest of her wealth 1-x in a risk-free asset which has expected return r

f

and standard deviation

of return 0. By the formula given in Chapter 12, the portfolio’s expected return is its weighted-

average return:

()

()( )

1

pA f

E

rxEr xr=+−

.

The portfolio’s return variance is

()

()( )

()

()

(

)

()

2

2

= 0, since = 0, since

the risk-free the risk-free

asset is risk-free asset is

(duh!) risk-free

(duh!)

222

12**1*,

pA f f

AA

Varr xVarr x Varr x x CovAr

xVar r x

σ

↑↑

=+− +−

==

.

This means that the standard deviation of the portfolio’s return is

p

A

x

σ

σ

=

.

PFE, Chapter 13: The CAPM and SML page 8

Improving on round dot portfolio

•

We can do better than line connecting r

f

and the round dot portfolio • by choosing

another portfolio on the efficient frontier. The line connecting the risk-free asset and the “red-

square” portfolio below is an improvement on the line of the previous section:

PFE, Chapter 13: The CAPM and SML page 9

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

ABC DE

Stock A Stock B

Average return 7.00% 15.00%

Variance 0.0064 0.0196

Sigma 8.00% 14.00%

Covariance of returns 0.00

Correlation 0.10

Risk-free rate 2%

Round dot portfolio

•

A 0.9

B 0.1

Mean 7.80% <-- =B29*$B$3+(1-B29)*$C$3

Sigma 7.47%

Red square portfolio

Ç

A 0.7

B 0.3

Mean 9.40% <-- =B35*$B$3+(1-B35)*$C$3

Sigma 7.33%

TWO STOCKS AND A RISK-FREE ASSET

<-- =SQRT(B29^2*$B$4+(1-B29)^2*$C$4

+2*B29*(1-B29)*$B$6)

<-- =SQRT(B35^2*$B$4+(1-B35)^2*$C$4

+2*B35*(1-B35)*$B$6)

Expected Return and Standard Deviation of

Portfolio Return

0%

5%

10%

15%

20%

0% 5% 10% 15% 20%

Standard deviation of portfolio return,

σ

p

Expected portfolio return, E(r

p

)

Since the new line is higher than the old line, all the points on the line to the red square

■

are better than the points on the line to the black circle

• . For any point on the round dot line