Menke W. Geophysical Data Analysis: Discrete Inverse Theory

Подождите немного. Документ загружается.

138

8

Non -Gaussian Distributions

8.4

Solving

L,

Norm

Problems

We shall show that this problem can be transformed into a “linear

programming” problem, a type that has been studied intensively and

for which means of solution are known (e.g., the so-called Simplex

algorithm; see Section

12.7).

The linear programming problem can be

stated as follows:

Find the

x

that maximizes

z

=

cTx

subject to the constraints

This problem was first studied by economists and business operations

analysts. For example,

z

might represent the profit realized

by

a factory

producing a product line, where the number

of

each product is given

by

x

and the profit on each item given by

c.

The problem is to

maximize the total profit

z

=

cTx

without violating the constraint that

one can produce only a positive amount of each product, or any other

linear inequality constraints that might represent labor laws, union

regulations, physical limitation of machines, etc. Computer programs

that can solve the linear programming problem are readily available.

First, we shall consider the completely underdetermined linear

problem with a priori model parameters, mean

(m),

and variance

a;.

The problem is to minimize the weighted length

L

=

c

[mi

-

(m,)la,f

subject to the constraint

Gm

=

d.

We first introduce 5Mnew variables

m:,

m”,,

a,,

x,,

and

x:,

where

i

=

1,

. . .

,

M.

The linear program-

ming problem may be stated as follows [Ref.

61:

Minimize

C

a,a;f

subject to the constraints

G[m’

-

m”]

=

d

[mi

-

my]

+

xi

-

ai

=

(mi)

[mi

-

my]

-

x;

+

ai

=

(mi)

mi20

my20

ai

2

0

XI

2

0

xi20

(8.10)

This linear programming problem has

5M

unknowns and

8.4

Solving

L,

Norm

Problems

139

N

+

2M constraints.

If

one makes the identification

m

=

m'

-

m",

signs of the elements of

m

are not constrained even though those of

m'

and

m"

are. Note that the remaining constraints can be rewritten as

a;

-

x;

=

[m;

-

(mi)]

a.

I1

-

x!

=

-

[m;

-

(mi)]

(8.11)

where the

a,,

x,,

and

xi

are nonnegative. Now

if

[m,

-

(m,)]

is posi-

tive, the first equation requires

a,

2

[m,

-

(m,)]

since

x,

cannot be

negative. The second constraint can always be satisfied by choosing

some appropriate

xi.

On the other hand, if

[m,

-

(m,)]

is negative,

then the first constraint can always be satisfied by choosing some

appropriate

x,

but the second constraint requires that

a,

2

-

[m,

-

(m,)].

Taken together, these two constraints imply that

a,

2

[[m,

-

(m,)]l.

Minimizing

X

a,a;f

is therefore equivalent to minimiz-

ing the weighted solution length

L.

The

L,

minimization problem has

been converted to a linear programming problem.

The completely overdetermined problem can be converted into a

linear programming problem in a similar manner. We introduce

2M+ 3Nnew variables, mi, mi',

i

=

1,

Mand

a,,

x,,

xi,

i

=

1,

Nand

2N constraints. The equivalent linear programming problem

is

[Ref.

61:

Minimize

z

aia;,'

subject to the constraints

z

Gij[m(

-

my]

+

xi

-

=

d,

(8.12)

The mixed-determined problem can be solved by any of several

methods. By analogy to the

L,

methods described in Chapters 3 and

7,

we could either pick some a priori model parameters and minimize

E

+

L,

or try to separate the overdetermined model parameters from

the underdetermined ones and apply a priori information to the

underdetermined ones only. The first method leads to a linear pro-

gramming problem similar to the two cases stated above but with even

140

8

Non -Gaussian Distributions

more variables

(5M

+

3N)

and constraints

(2M

+

2N):

Minimize

C

a,a&f

+

C

a:ozl

subject to the constraints

(8.13)

The second method is more interesting. We can use the singular-

value decomposition to identify the null space of

G.

The solution then

has the form

P

M

1-

I

I-pi

1

mest

=

c.

u,vp,

+

C

b,v,,

=

Vpa

+

Vob

(8.14)

where the

v’s

are the model eigenvectors from the singular-value

decomposition and

a

and

b

are vectors with unknown coefficients.

Only the vector

a

can affect the prediction error,

so

one uses the

overdetermined algorithm to determine it:

find

aest

that minimizes

E

=

Ild

-

Gmll,

=

Id,

-

[UpApal,la;,l

1

(8.15)

Next, one uses the underdetermined algorithm to determine

b:

find

best

that minimizes

M

L

=

Ilm

-

(m)II

=

a;tI[V,b],

-

(mi

-

[Vpaest],)l

(8.16)

I==

1

It is possible to implement the basic underdetermined and overdeter-

mined

L,

algorithms in such a manner that the many extra variables

are never explicitly calculated [Ref.

61.

This procedure vastly decreases

the storage and computation time required, making these algorithms

practical for solving moderately large

(M

=

100)

inverse problems.

8.5

TheL,Norm

141

8.5

The

L,

Norm

While the

L,

norm weights “bad” data less than the

L2

norm, the

L,

norm weights it more:

The prediction error and solution length are weighted by the reciprocal

of their a priori standard deviations. Normally one does not want to

emphasize outliers,

so

the

L,

form is useful mainly in that it can

provide a “worst-case” estimate of the model parameters for compari-

son with estimates derived on the basis of other norms. If the estimates

are in fact close to one another, one can be confident that the data are

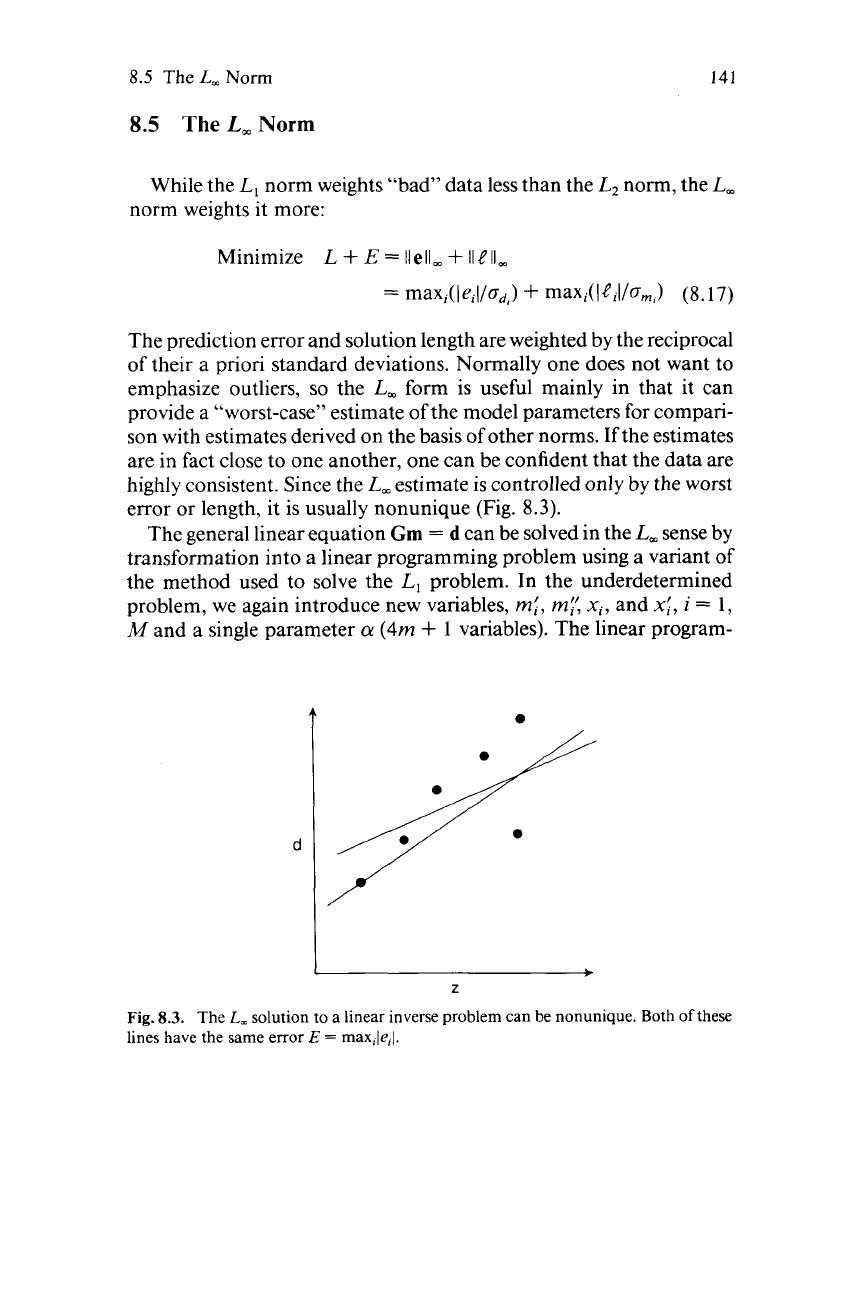

highly consistent. Since the

L,

estimate is controlled only by the worst

error or length, it is usually nonunique (Fig.

8.3).

The general linear equation

Gm

=

d

can be solved in the

L,

sense by

transformation into a linear programming problem using a variant of

the method used to solve the

L,

problem. In the underdetermined

problem, we again introduce new variables,

rn:,

rnl:

xi,

and

x:,

i

=

1,

M

and a single parameter

a

(4m

+

1

variables). The linear program-

Z

Fig.

8.3.

The

L,

solution to a linear inverse problem can be nonunique. Both

of

these

lines have the same error

E

=

max,le,l.

142

8

Non -Gaussian Distributions

ming problem is

Minimize

a

subject to the constraints

G[m’

-

m”]

=

d

[mi

-

m:’]

+

x,

-

aam,

=

(m,)

(8.18)

[mi

-

my3

-

x:

+

aam,

=

(m,)

m:ro

m:’20

a20

x,rO

xi20

where m

=

m’

-

m”.

We note that the new constraints can be written

as

(8.19)

where

a,

x,

,

and

xi

are nonnegative. Using the same argument as was

applied in the

L,

case, we conclude that these constraints require that

a

2

[[m,

-

(m,)]/o,,l

for all

i.

Since this problem has but a single

parameter

a,

it must therefore satisfy

a

2

max,(l[m,

-

(mi>l/am,l>

(8.20)

Minimizing

CII

yields the

L,

solution. The linear programming prob-

lem for the overdetermined case

is

Minimize

a

subject to the constraints

(8.21)

mi”

0

my20

a20

xi20

x;ro

The mixed-determined problem can be solved by applying these

algorithms and either of the two methods described for the

L,

problem.

NONLINEAR INVERSE

PROBLEMS

9.1

Parameterizations

In setting up any inverse problem, it is necessary to choose variables

to represent data and model parameters (to select a parameterization).

In many instances this selection is rather ad hoc; there might be no

strong reasons for selecting one parameterization over another. This

can become a substantial problem, however, since the answer obtained

by solving an inverse problem is dependent on the parameterization.

In other words, the solution is not invariant under transformations of

the variables. The exception is the linear inverse problem with Gaus-

sian statistics, in which solutions are invariant for any linear repa-

rameterization of the data and model parameters.

As

an illustration of this difficulty, consider the problem of fitting a

straight line to the data pairs

(1,

I),

(2,2),

(3,3),

(4,5).

Suppose that we

regard these data as

(z,

d)

pairs where

z

is an auxiliary variable. The

least squares

fit

is

d

=

-0.500

+

1.3002.

On

the other hand, we might

regard them as

(d’,

z’)

pairs where

z’

is the auxiliary variable. Least

143

144

9

Nonlinear Inverse

Problems

squares then gives

d’

=

0.309

+

0.743z’, which can be rearranged as

z’

=

-0.416

+

1.345d’. These two straight lines have slopes and

intercepts that differ by about

20%.

This discrepancy arises from two sources. The first is an inconsistent

application of probability theory. In the example above we alternately

assumed that

z

was exactly known and

d

followed Gaussian statistics

and that

z

=

d’

followed Gaussian statistics and

d

=

z’

was exactly

known. These are two radically different assumptions about the distri-

bution of errors,

so

it

is

no wonder that the solutions are different.

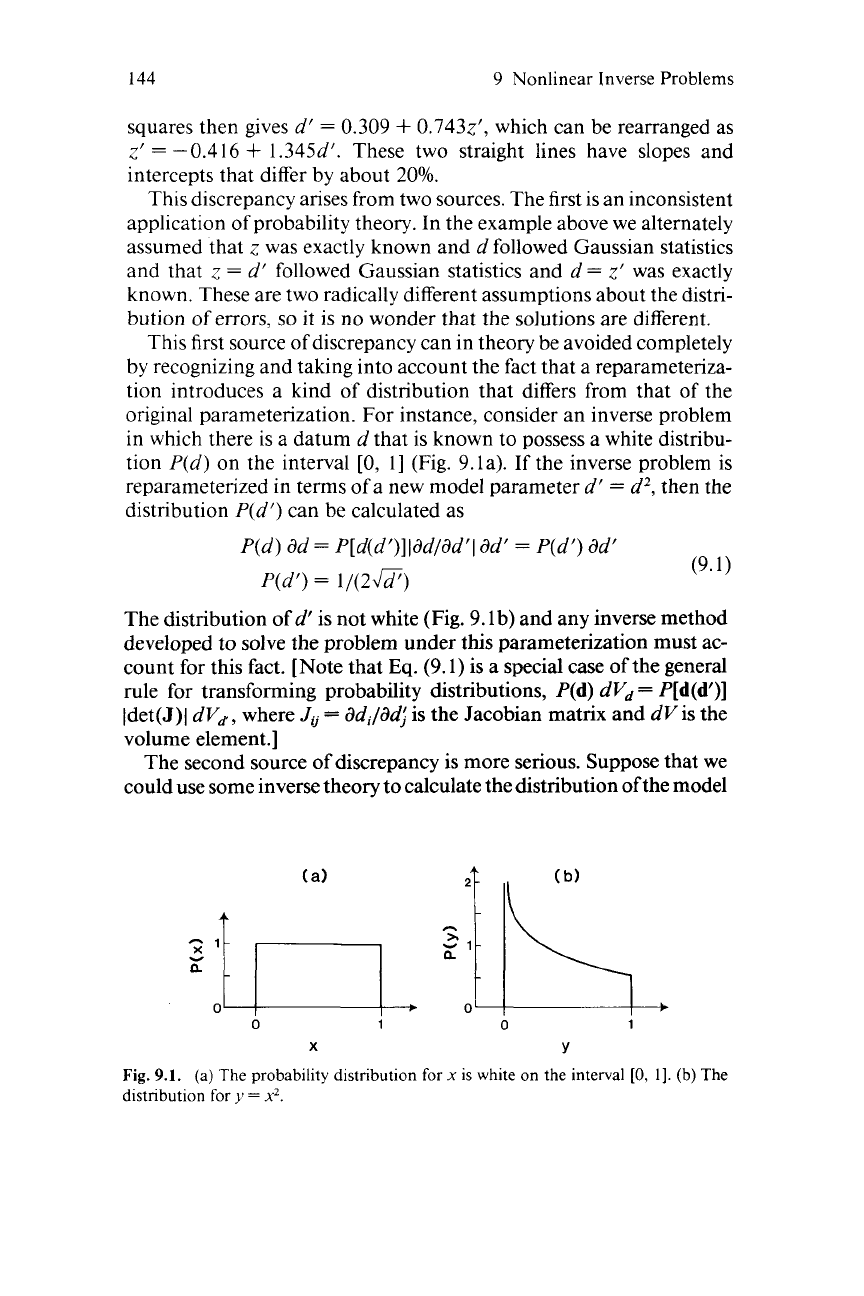

This first source of discrepancy can in theory be avoided completely

by recognizing and taking into account the fact that a reparameteriza-

tion introduces a kind of distribution that differs from that of the

original parameterization. For instance, consider an inverse problem

in which there is a datum

d

that is known to possess a white distribu-

tion

P(d)

on the interval

[0,

I] (Fig. 9.1a).

If

the inverse problem is

reparameterized in terms

of

a new model parameter

d’

=

d2,

then the

distribution

P(d’)

can be calculated as

P(d)

dd

=

P[d(d’)]ldd/dd’I

ad‘

=

P(d’)

dd‘

(9.1)

P(d’)

=

1/(2G)

The distribution of

d’

is not white (Fig. 9. lb) and any inverse method

developed to solve the problem under this parameterization must ac-

count for this fact. [Note that

Eq.

(9.1) is a special case of the general

rule for transforming probability distributions, P(d)

dVd

=

P[d(d’)]

Idet(J)I

dVd,

where

JU

=

dd,/dd,l

is the Jacobian matrix and

dVis

the

volume element.]

The second source of discrepancy is more serious. Suppose that we

could use some inverse theory to calculate the distribution ofthe model

21

1

I

(a)

I

,

?)

i\

).

Y

n

0

0

1

0

1

X

Y

Fig.

9.1.

(a)

The

probability distribution

for

x

is white

on

the interval

[0,

11.

(b) The

distribution

for

y

=

x2.

9.1

Parameterizations

145

parameters under a particular parameterization. We could then use

Eq.

(9.1)

to find

theirdistributionunderanyarbitraryparameterization.

Insofar as the distribution of the model parameters

is

the answer to the

inverse problem, we would have the correct answer in the new parame-

terization. Probability distributions are invariant under changes of

parameterization. However, a distribution is not always the answer for

which we are looking. More typically, we need an estimate (a single

number) based on a probability distribution (for instance, its maxi-

mum likelihood point or mean value).

Estimates are not invariant under changes in the parameterization.

For example, suppose

P(m)

has a white distribution as above. Then

if

m’

=

m2,

P(m’)

=

1/(2&2).

The distribution in

m

has no maximum

likelihood point, whereas the distribution in

m’

has one at

m’

=

m

=

0.

The distributions also have different means (expectations)

E:

E[~I

=

m~(m)

am

=

m

am

=

4

E[m‘]

=

m’P(m’)

am’

=

I

+&2

amf

=

4

Even though

m’

equals the square of the model parameter

m,

the

expectation of

m’

is not equal to the square of the expectation of

m:

There is some advantage, therefore, in working explicitly with

probability distributions as long as possible, forming estimates only at

the last step.

If

m

and

m’

are two different parameterizations of model

parameters, we want to avoid as much as possible sequences like

distribution for

m

-

estimate of

m

-

estimate of

m’

I

(9.2)

I’ I’

I

4

+

(:I2.

in favor of sequences like

distribution for

m

-

distribution for

m’

__*

estimate of

rn’

Note, however, that the mathematics for this second sequence

is

typically much more difficult than that for the first.

There are objective criteria for the “goodness” of a particular esti-

mate of a model parameter. Suppose that we are interested in the value

of a model parameter

m.

Suppose further that this parameter either

is

deterministic with a true value or (if it is a random variable) has a

well-defined distribution from which the true expectation could be

calculated if the distribution were known. Of course, we cannot know

the true value; we can only perform experiments and then apply

146

9

Nonlinear Inverse Problems

inverse theory to derive an estimate of the model parameter. Since any

one experiment contains noise, the estimate we derive will not coin-

cide with the true value

of

the model parameter. But we can at least

expect that if we perform the experiment enough times, the estimated

values will scatter about the true value. If they do, then the method of

estimating is said to be

unbiased.

Estimating model parameters by

taking nonlinear combinations of estimates of other model parameters

almost always leads to bias.

d

0.001

I

I I

0

5

10

15 20

L

log

d

-

L

Fig.

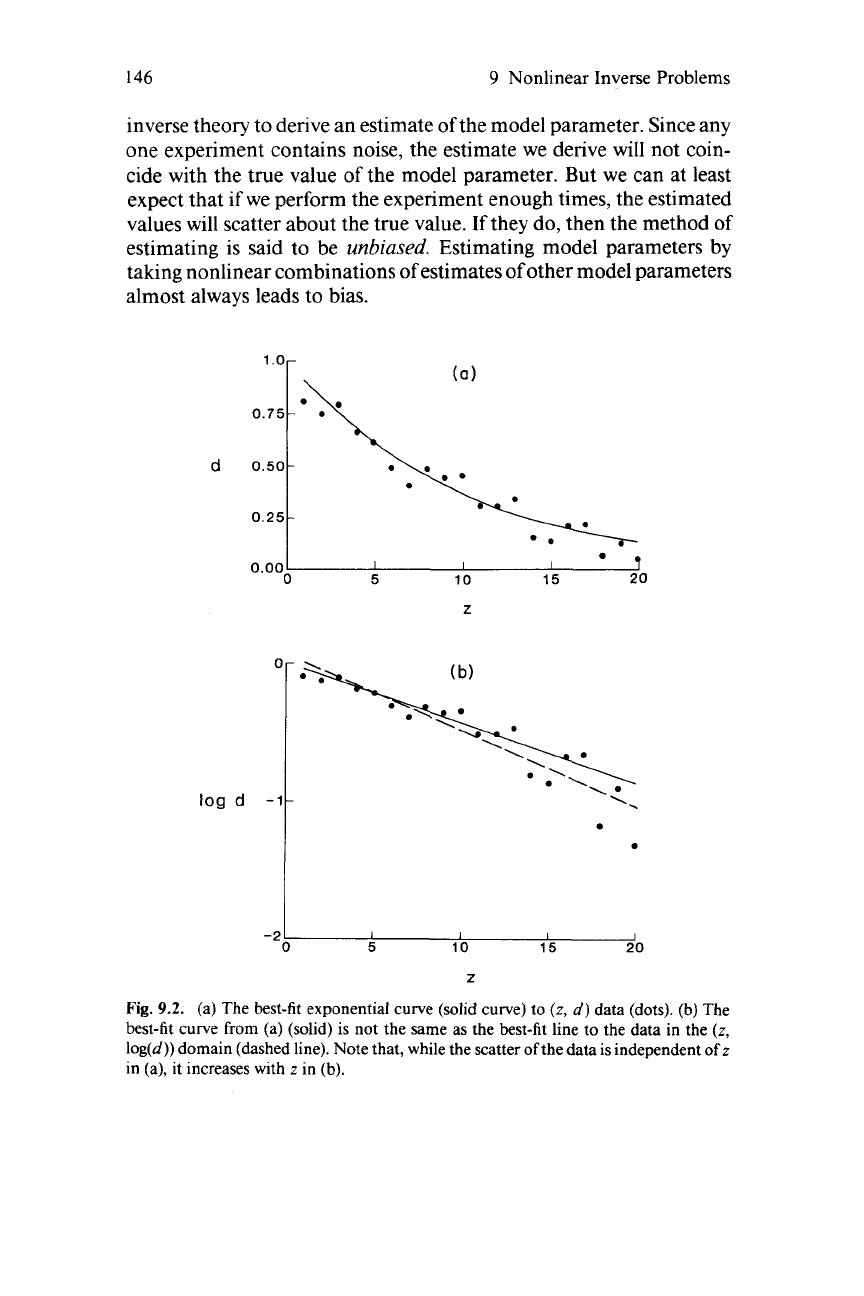

9.2.

(a) The best-fit exponential curve (solid curve) to

(z,

d)

data (dots).

(b)

The

best-fit curve from (a) (solid) is not the same as the best-fit line to the data in the

(z,

log(d)) domain (dashed line). Note that, while the scatter of the data is independent of z

in (a), it increases with

z

in

(b).

9.3

The Nonlinear Inverse Problem with Gaussian Data

147

9.2

Linearizing Parameterizations

One of the reasons for changing parameterizations is that it is

sometimes possible to transform an inverse problem into a form that

can be solved by a known method. The problems that most commonly

benefit from such transformations involve fitting exponential and

power functions to data. Consider a set of

(z,

d)

data pairs that are

thought to obey the model

di

=

m,

exp(m2zi). By making the transfor-

mation

m;

=

log(m,),

m;

=

m2,

and

dj=

log(di), we can write the

model as the linear equation

di

=

m{

+

m;z2,

which can be solved by

simple least squares techniques. To justify rigorously the application

of least squares techniques to this problem, we must assume that the

dj

are independent random variables with a Gaussian distribution of

uniform variance. The distribution of the data in their original pa-

rameterization must therefore be non-Gaussian.

For example,

if

the exponential decays with increasing

z

for all

m2

<

0,

then the process of taking a logarithm amplifies the scattering

of the near-zero points that occurs at large

z.

The assumption that the

dj

have uniform variance, therefore, implies that the data

d

were

measured with an accuracy that increases with

z

(Fig.

9.2).

This

assumption may well be inconsistent with the facts of the experiment.

Linearizing transformations must be used with some caution.

9.3

The Nonlinear Inverse Problem with

Gaussian Data

Linearizing transformations cannot be found for most inverse prob-

lems. We must consider other methods for directly solving the nonlin-

ear problem. We shall begin by considering the very general implicit

equation

f(d, m)

=

0

(where

f

is of length

p

5

M

+

N).

We simplify by

assuming that the data

d

and a priori model parameters

(m)

have

Gaussian distributions with covariance [cov

d]

and [cov

m],

respec-

tively. If we let

x

=

[d, mIT,

we can think of the a priori distribution of

the data and model as a cloud in the space

S(x)

centered about the

observed data and mean a priori model parameters, with a shape

determined by the covariance matrix [cov

x]

(Fig.

9.3).

This matrix

[cov

x]

contains [cov

d]

and [cov

m]

on diagonal blocks. In principle

the off-diagonal blocks could be made nonzero, indicating some cor-