Gasch R., Twele J. (Eds.) Wind Power Plants: Fundamentals, Design, Construction and Operation

Подождите немного. Документ загружается.

502 15.2 Erection and operation of wind turbines

appears to an onlooker to have been finally erected. However, several days of

work will have to be spent for completing the internal installations and the con-

nections before initial operation.

Fig. 15-13 Hoisting the Rotor by means of main mobile crane and assisting mobile crane [9]

According to the German Renewable Energy Sources Act, the feed-in tariff valid

for the individual wind turbine is determined by the date of the first electricity

feed into the grid. Since the feed-in tariffs are usually reduced from year to year, it

may be essential to set the wind turbine at least shortly into operation already in

the end of December to get the higher tariff. This explains, among others, why the

number of installed wind turbines is usually higher in the second half of the year

than in the first half of the year despite the more unfavourable weather conditions

for installation.

15 Planning, operation and economics of wind farm projects 503

Commissioning and take-over

Several weeks of testing usually pass between the production of the first kilowatt-

hour of electricity and the handing over of the wind turbine to the operator. The

future operator/operational manager of the wind turbine checks himself or

arranges for an inspection to take place in order to see whether the wind turbine

was delivered and erected as agreed by contract and to ensure it proper and fault-

less functioning.

The common procedure is:

- Test operation, surveyed by the manufacturer and adjustment of parame-

ters to the site-specific conditions

- Inspection and elimination of deficiencies by the manufacturer

- Acceptance inspection and handing-over to the operator or operational

manager which defines the begin of the defect liability period

After the elimination of “childhood diseases“ (e.g. rotor unbalance) and the final

adaption of control parameters to the site conditions, the wind turbine is officially

commissioned and handed over tot the operator. An independent expert usually in-

spects the wind turbine for the operator to check and clarify whether the specifica-

tions of the contract have been all fulfilled. This inspection involves checking the

technical condition of the wind turbine itself, as well as its auxiliary installations

such as aviation safety markings or lights, a possibly modified power curve for the

reduction of noise emission and so on. The requirements of the building permit are

of prime importance in this context.

Wind turbine operation

Operation and inspection

The wind turbine shall now operate for a minimum of 20 years with the highest

possible availability. The technical operator surveys all technical aspects of the

wind farm project. After expiration of the defect liability period, any risks arising

from the operation have to be borne by the operator, as well the costs for mainte-

nance and repair if there is no full-service contract.

The safe operation of technical systems as a wind turbine has to be verified

through periodical inspections of all mechanical and electrical components and

testing their proper functioning. Moreover, the safety equipment for climbing the

tower (ladder, lift, harness, rescue devices, etc.) is checked and all other aspects

that are related to potential risks, such as fire hazard, environmentally hazardous

materials, machine damage, etc.

504 15.2 Erection and operation of wind turbines

In Germany, it is required that wind turbines are checked every two to four years

by an independent expert. The interval depends on the wind turbine size and

whether a service contract exists for the wind turbine. The aim is to minimise dan-

ger to the environment, humans and the machine itself, or to reduce these risks to

an accountable degree at least.

High availability and high yield are irrelevant in the context of safety; however,

these two issues are of upmost importance for the operator Hence, a “condition-

oriented inspection” of the wind turbine should be carried out. All components are

inspected to see whether faults, malfunction defects or damages announce or have

already occurred. The focus is primarily on bearings and gearbox. Based on the

recommendations of the inspection report, the operator decides whether mainte-

nance, repair or even component exchange is necessary, e.g. of a bearing of the

generator.

Full-service contracts offered by wind turbine manufacturer with the manufac-

turer continuing to be responsible for maintenance and repair of the wind turbine

also provide an alternative. However, in this case as well, it is still the duty of the

technical operator to care about a reliable operation with high availabilities and

maximised energy yield. The following has to be surveyed by the technical

operator:

- Operation during the defect liability period,

- Handing-over at the end of the defect liability period according to the

purchase contract (usually 2 to 3 years),

- Operation after the expiration of the defect liability period,

- Maintenance and repair and

- Inspection and control of the operation.

Maintenance and repair

The necessary service works and intervals are documented in the technical specifi-

cations of the wind turbine. All bearings have to be lubricated periodically. All

mechanical components, electrical devices and control components have to be

maintained. Small repairs are carried out without delay. The technical operator

will then be given a service protocol.

The operator is responsible for successful operation of the wind farm, but there

is often a separate technical wind farm manager caring for technical tasks of

O&M. Apart from a very good technical knowledge of wind turbines this person

needs to be able to communicate in a clear and effective manner with the (more

economically oriented) wind farm management team and all the other external

partners concerned: wind turbine manufacturer, service companies, grid operator,

inspectors and other experts, authorities, and so on. The duties are:

15 Planning, operation and economics of wind farm projects 505

- Collection and management of all technical information (e.g. contracts,

manuals, circuit diagrams, etc.),

- Remote monitoring of the wind turbine operation (e.g. energy production

measured at the electricity meter, status messages and permanently

recorded operating data),

- Regular visits to the wind turbines and wind farms for visual inspections

- Organisation and survey of service and repair works,

- Generation of periodical reports on successful operation (energy yield

and availability) and technical condition (malfunction and repair) and

- Improvement and optimisation of wind turbine operation for increased

availability and energy yield

Acquisition of operating data and condition monitoring

Wind turbines run usually in an automatic operation mode and are controlled by

the internal supervisory and control computer. Typically, communication with the

control room of the wind turbine manufacturer or the technical wind farm manager

will be initiated only in the event of malfunction. Then, the wind turbine sends an

email, fax or sms, and the service team has to take action.

Furthermore, the wind turbine stores its operating data, which includes current

wind speed, wind direction, rotational speed, electrical power, several tempera-

tures and further operational parameters. These can be read out with the System

Control And Data Acquisition Software (SCADA) and are the data on which the

technical wind farm manager bases his assessment of the wind turbine condition

and any measures that may need to be carried out.

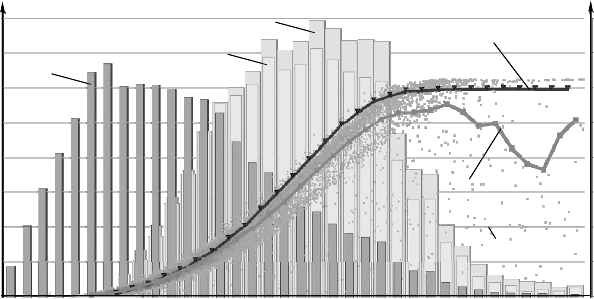

Fig. 15-14 shows the yield data versus the wind speed measured with the nacelle

anemometer for a six-month period of operation. The 10-minute averages of the

electrical power are sorted into wind speed class bins, forming the real energy his-

togram which shows the energy yield per wind class (cf. section 4.3). For com-

parison, the theoretical energy histogram is also displayed. This is calculated from

the measured wind speeds (i.e. the measured wind histogram) and the power curve

of the wind turbine manufacturer. The differences are clearly visible, not only be-

tween the histograms but also between the theoretical and real power curve which

provides valuable information on site quality and wind turbine operation.

506 15.2 Erection and operation of wind turbines

0

500

1000

1500

2000

Electrical power in kW

0

Frequency in %

2

4

6

8

024 6 810121416

Theoretical energy histogram

Real energy histogram

Power curve of contract

Wind

histogram

Power curve from

operation data

Operating

points

Wind speed in m/s

0

500

1000

1500

2000

Electrical power in kW

0

Frequency in %

2

4

6

8

024 6 810121416

Theoretical energy histogram

Real energy histogram

Power curve of contract

Wind

histogram

Power curve from

operation data

Operating

points

Wind speed in m/s

Fig. 15-14 Operating data of a wind turbine [11]

The analysis of the operating data reveals the efficiency of operation. Malfunction

statistics and trend analysis provide information on problems arising with certain

components. The prevention of damages can be improved by installing a condition

monitoring system (CMS). By vibration measurements, the condition of the main

drive train components bearings and gear box is permanently monitored and

assessed in order to prevent a machine breakdown with possible consequential

damages. Moreover, scheduling repair or replacement of the affected component

is facilitated, i.e. deciding whether an immediate component replacement is neces-

sary or whether there is enough useful life remaining for waiting with the works

until the end of the windy season). The CMS offers the better alternative to periodical

short-time measurement and assessment by an expert but it requires some invest-

ment costs.

Insurances for wind turbines

The types of risks and who is to bear them are the most important questions for in-

surance companies. The manufacturer alone bears all risks before installation or

handing-over of the wind turbine to the operator. In all phases of the wind farm

project – from production and transport to the years-lasting operation – there is the

risk that proper operation may be disturbed or interrupted by unexpected events.

The wind turbines have to be insured against machine breaking and external dan-

gers (fire, lightning, etc.).

Additionally, it is advisable be insured against operation interruption to compen-

sate for yield loss during downtimes. In some cases, the financing bank stipulates

such an insurance in order to make sure that the loan can be repaid. Practical

experience from wind turbine operation has revealed that prolonged downtimes

15 Planning, operation and economics of wind farm projects 507

following an insured event of damage (e.g. lightning strike or generator damage)

can result in significantly increased insurance costs. If the cause of a minor dam-

age (e.g. a hot running bearing) was not detected a more serious consequential

damage may result, e.g. a fire in the nacelle.

The third kind of required insurance is liability insurance. This covers events

where somebody or something is damaged by the wind turbine which may even

incluce damage due to a falling machine component or a piece of ice – or even fire

in the field below the wind turbine caused by a fire in the nacelle.

At any rate, risks which cannot be insured include the following: wear due to

operation, third party damages to the wind turbine, negligence by installation of

already defective components as well as the effects of war and accidents in

nuclear power plants.

Decommissioning and repowering of wind turbines

At the end of the operating period the wind turbine has to be decommissioned, cf.

Fig. 15-1. Another economic alternative is so-called repowering which is the re-

placement of many small wind turbines by a few bigger ones. The local options

for this should be checked carefully already in the wind farm planning because

decommissioning or repowering should be considered in the contracts.

New wind turbines are not only bigger than smaller ones. Typically, they are

more quiet and more efficient, showing higher availability and energy yield at the

same site and as well as reduced service costs. Therefore, repowering brings tech-

nical progress and economic benefits. Moreover, a few big wind turbines have a

reduced the visual impact on the landscape compared to the case of many small

wind turbines. First and foremost, repowering is a decision based on economic

considerations. Mostly, it is only economically viable after 20 years of operation.

However, several successful repowering projects in Germany have already proven

the increased economic benefit as well as the reduced visual impact.

15.2.2 Legal aspects

In order to implement the wind farm project and operate the wind turbines, it is

necessary to establish a company, cf. Fig. 15-1, since operating wind turbines im-

plies a commercial venture.

For a small wind farm with only a few participators a partnership under the

German Civil code such as a BGB company is suitable. The formation of a BGB

company does not require much effort as no formalities are involved except for

registration with the tax office. There is no need for the minimum capital or the

registration in the commercial register. However, the partners concerned are

commercially liable, meaning that they together with their entire personal assets

508 15.2 Erection and operation of wind turbines

are liable for the company. The proceeds and losses are offset against other in-

come in the income tax return.

In Germany, investment in wind farm projects has been primarily carried out

by private individuals. Therefore, the legal form of a limited liability company

should not be chosen for the operating company but rather a limited partnership

with a limited liability company as a general partner. The limited liability com-

pany is responsible for the business and technical management. Private investors

acquire the shares as limited partners in the limited partnership thus providing the

required equity. This combines the advantages of both legal company forms. Lim-

ited partners get their share of proceeds and losses in the course of a separate de-

termination of the annual accounts, declare them and are liable for the capital they

have contributed.

If the wind farm project is started as a local or regional initiative, it is often

quite easy to find investors without having to conduct a major marketing cam-

paign. A nationwide search for investors would be appropriate if investment

amounted to several hundred million Euros. A closed-end investment company is

then launched and announced in a fonds prospectus. In this case the legal frame-

work of the liability in respect of information contained in fonds prospectus has to

be observed. The given information should follow the common standards (e.g.

IDW 4, quality standard of the German Association of Certified Public Account-

ants) and have the attestation of a certified accountant.

All further legal implications (rights and duties of the limited partner, their right to

say in a matter, etc.) have to be regulated in the company contracts of the operat-

ing company.

15.2.3 Economic efficiency of operation

If the financing has been secured and the wind farm project implemented, the

revenue from the electricity sold are offset against the operation costs (cf. section

15.1.3). The legal framework of the German Renewable Energy Sources Act

(German: EEG) stipulates the feed-in tariffs per kWh which form the basis of the

20-years feed-in contract [12]. In absence of such a set regulation regarding the

feed-in tariffs, it would be difficult to finance a wind farm project as it incurs rela-

tively high investment costs. The framework of the German Electricity Feed-in

Act (German: Stromeinspeisegesetz, StrEG, 1991 to 2000) and the successor

scheme of the EEG which followed in April 2000 is internationally regarded as a

good example of a legal framework which helps to turn a wind farm project, for

favourable site conditions, into a safe and profitable capital investment. The EEG

differentiates according to site quality in order not to privilege coastal sites vis-à-

vis inland sites which have disadvantageous wind conditions through lower mean

wind speeds. Further details regarding the legal framework can be found in the

references, e.g. [8, 12].

15 Planning, operation and economics of wind farm projects 509

The usual company accounts with the balance sheet and the profit and loss state-

ment are required for every year of operation. Apart from the economic develop-

ment of the wind farm project, the development of liquidity (cash) plays a decisive

role as risk of insolvency lurks in the worst-case scenario. Illiquidity would mean

that the project has failed economically. Besides operating costs (see section

15.1.3 and Figures 15-16), the debt service (interest and repayment/amortisation)

for the external financing (approx. 75%) results in large cash flows during the fi-

nancing period, usually the first ten years. In the first years, the dept service may

reach up to 2/3 of the proceeds.

0

100.000

200.000

300.000

400.000

500.000

600.000

700.000

1 2 3 4 5 6 7 8 9 1011121314151617181920

Betriebsjahr

k€

Rated power of WEC: 600 kW

Annual mean wind speed: v = 6,25 m/s

(at hub height)

Total investment: 723 000 €

Equity: 25%

Year of operation

-20.000

-10.000

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

90.000

1 2 3 4 5 6 7 8 9 1011121314151617181920

Betriebsjahr

k€

Feed-in tariff

reduction

two years

without repayment

Year of operation

k€

k€

0

LiquidityProceeds

0

100.000

200.000

300.000

400.000

500.000

600.000

700.000

1 2 3 4 5 6 7 8 9 1011121314151617181920

Betriebsjahr

k€

Rated power of WEC: 600 kW

Annual mean wind speed: v = 6,25 m/s

(at hub height)

Total investment: 723 000 €

Equity: 25%

Year of operation

-20.000

-10.000

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

90.000

1 2 3 4 5 6 7 8 9 1011121314151617181920

Betriebsjahr

k€

Feed-in tariff

reduction

two years

without repayment

Year of operation

k€

k€

0

LiquidityProceeds

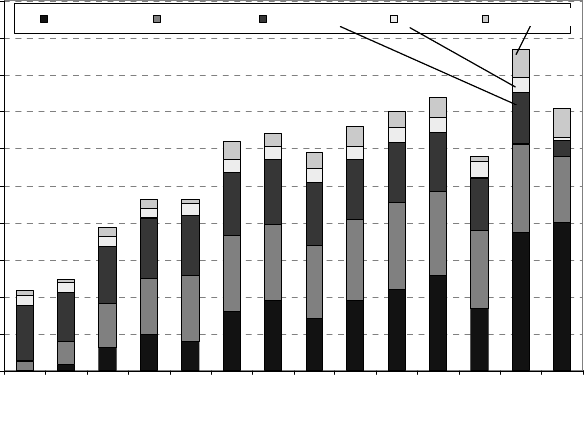

Fig. 15-15 Development of the liquidity and proceeds of a wind farm project with a 600 kW

wind turbine

510 15.2 Erection and operation of wind turbines

Fig. 15-15, top, shows the development of the liquidity (available cash) of a sound

wind farm project. In order to build up a cash reserve it is quite useful to have two

years without repayment at the start of operation period. This is provided by the

special financing programmes of KfW Bankengruppe for renewable energy pro-

jects. This can help to bridge years which may have a negative balance due to re-

duced energy yield in bad wind years. One should avoid promptly distributing

company profits to investors so as to build up reserves for possible repairs and for

the decommissioning at the end of the project. Nevertheless, a cumulative distri-

bution of 200% to 300% at the end of the 20 years of operation is common for a

sound wind farm project.

The profit and loss statement is decisive when evaluating the annual result. Here,

in contrast to the considerations on liquidity described above, only the interest of

the debt service is considered, the repayment is not relevant, but the annual amor-

tisation is. This may lead to a loss in the first years of operation, Fig. 15-15,

below, which is then credited against the investor’s tax burden. Given the fixed

period of 16 years for amortisation (German law, 2005) the effect is quite small.

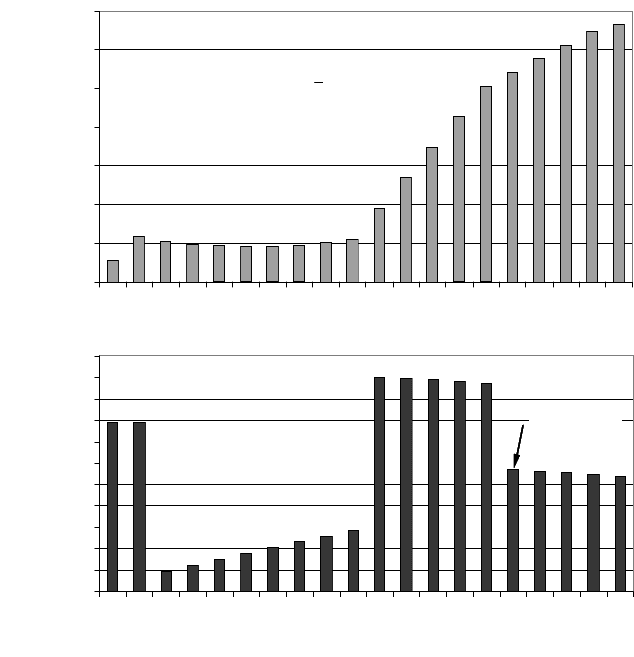

The proportion of the annual operating costs primarilys come from service, main-

tenance, repair and insurance, as discussed already in section 15.1.3. These costs

vary with the years, as shown in Fig. 15-16, and are significantly depend on the

wind turbine size.

0

5

10

15

20

25

30

35

40

45

50

1234567891011121314

Betriebsalter [Jahre]

€/kW a

Reparatur Wartung Versicherung Pacht Sonstiges

Repair Maintenance Insurance Land lease Misc.

Years of operation

0

5

10

15

20

25

30

35

40

45

50

1234567891011121314

Betriebsalter [Jahre]

€/kW a

Reparatur Wartung Versicherung Pacht Sonstiges

0

5

10

15

20

25

30

35

40

45

50

1234567891011121314

Betriebsalter [Jahre]

€/kW a

Reparatur Wartung Versicherung Pacht Sonstiges

Repair Maintenance Insurance Land lease Misc.

Years of operation

Fig. 15-16 Development of the operating costs for wind turbines with a rated power of less than

500 kW [7]

15 Planning, operation and economics of wind farm projects 511

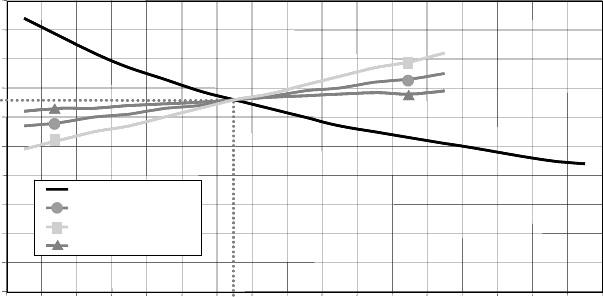

0.000

0.010

0.020

0.030

0.040

0.050

0.060

0.070

0.080

0.090

0.100

-30-25-20-15-10-5 0 5 101520253035404550

Annual production

Interest rate

Investment costs

Operating costs

€/ kWh

Variation from base value in %

0.000

0.010

0.020

0.030

0.040

0.050

0.060

0.070

0.080

0.090

0.100

-30-25-20-15-10-5 0 5 101520253035404550

Annual production

Interest rate

Investment costs

Operating costs

€/ kWh

Variation from base value in %

Fig. 15-17 Specific electricity generation costs, sensitivity to changes of the most important

parameters [13]

Little experience has been gathered for the second decade of operation to date,

hence a conservative estimate is useful [2]. A moderate increase in operating costs

is expected due to inflation.

Fig. 15-17 summarizes the impact of the most important parameters on elec-

tricity generation costs. The effect of the operating costs is relatively low. Due to

the high share of external financing (approx. 75%) the interest level and the level

of the total investment costs are important factors. Nevertheless, there is no doubt

that the wind itself is the biggest influencing factor. Annual production depends

on the cube of the wind speed, as a result of which a 10% higher wind speed may

increase annual production by up to 30%. With respect to the example shown in

Fig. 15-17 this would result in a significant reduction in the specific electricity

generation costs from 0.065 €/kWh to 0.050 €/kWh.

15.2.4 Influence of the hub height and wind turbine concept on

the yield

The suitable wind turbine should be chosen according to the local wind conditions

so as to achieve the highest possible annual yield. First and foremost, the eco-

nomically suitable hub height has to be chosen according to the local wind profile

(increase of the wind speed with the height above ground depending on the rough-

ness length z

0

). For some wind turbines with a rated power between 1.5 and 2.5

MW, Fig. 15-18 shows the significant influence of the hub height on the area-