Brealey, Myers. Principles of Corporate Finance. 7th edition

Подождите немного. Документ загружается.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

III. Practical Problems in

Capital Budgeting

12.Making Sure Managers

Maximize NPV

© The McGraw−Hill

Companies, 2003

pressure for immediate book profits, the more the regional manager is tempted to

forgo good investments or to favor quick-payback projects over longer-lived proj-

ects, even if the latter have higher NPVs.

Would EVA solve this problem? No, EVA would be negative in the first two

years of the Nodhead store. In year 2, for example,

This calculation risks reinforcing the regional manager’s qualms about the new

Nodhead store.

Again, the fault here is not in the principle of EVA but in the measurement of in-

come. If the project performs as projected in Table 12.7, the negative EVA in year 2

is really an investment.

EVA ⫽ 33 ⫺ 1.10 ⫻ 8332⫽⫺50, or ⫺$50,000

CHAPTER 12

Making Sure Managers Maximize NPV 329

Year

123456

Cash flow 100 200 250 298 298 298

Book value at

start of year,

straight-line

depreciation 1,000 833 667 500 333 167

Book value at

end of year,

straight-line

depreciation 833 667 500 333 167 0

Change in book

value during year ⫺167 ⫺167 ⫺167 ⫺167 ⫺167 ⫺167

Book income ⫺67 ⫹33 ⫹83 ⫹131 ⫹131 ⫹131

Book ROI ⫺.067 ⫹.04 ⫹.124 ⫹.262 ⫹.393 ⫹.784

Book depreciation 167 167 167 167 167 167

TABLE 12.7

Forecasted book

income and ROI for

the proposed

Nodhead store. Book

ROI is lower than the

true rate of return

for the first two

years and higher

thereafter.

12.6 MEASURING ECONOMIC PROFITABILITY

Let us think for a moment about how profitability should be measured in princi-

ple. It is easy enough to compute the true, or economic, rate of return for a com-

mon stock that is continuously traded. We just record cash receipts (dividends) for

the year, add the change in price over the year, and divide by the beginning price:

The numerator of the expression for rate of return (cash flow plus change in

value) is called economic income:

Economic income ⫽ cash flow ⫹ change in present value

⫽

C

1

⫹ 1P

1

⫺ P

0

2

P

0

Rate of return ⫽

cash receipts ⫹ change in price

beginning price

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

III. Practical Problems in

Capital Budgeting

12.Making Sure Managers

Maximize NPV

© The McGraw−Hill

Companies, 2003

Any reduction in present value represents economic depreciation; any increase in

present value represents negative economic depreciation. Therefore

and

The concept works for any asset. Rate of return equals cash flow plus change in

value divided by starting value:

where PV

0

and PV

1

indicate the present values of the business at the ends of years

0 and 1.

The only hard part in measuring economic income and return is calculating

present value. You can observe market value if shares in the asset are actively

traded, but few plants, divisions, or capital projects have shares traded in the stock

market. You can observe the present market value of all the firm’s assets but not of

any one of them taken separately.

Accountants rarely even attempt to measure present value. Instead they give us

net book value (BV), which is original cost less depreciation computed according

to some arbitrary schedule. Companies use the book value to calculate the book re-

turn on investment:

Therefore

If book depreciation and economic depreciation are different (they are rarely the

same), then the book profitability measures will be wrong; that is, they will not

measure true profitability. (In fact, it is not clear that accountants should even try

to measure true profitability. They could not do so without heavy reliance on sub-

jective estimates of value. Perhaps they should stick to supplying objective infor-

mation and leave the estimation of value to managers and investors.)

It is not hard to forecast economic income and rate of return. Table 12.8 shows

the calculations. From the cash-flow forecasts we can forecast present value at the

start of periods 1 to 6. Cash flow plus change in present value equals economic in-

come. Rate of return equals economic income divided by start-of-period value.

Of course, these are forecasts. Actual future cash flows and values will be higher

or lower. Table 12.8 shows that investors expect to earn 10 percent in each year of

the store’s six-year life. In other words, investors expect to earn the opportunity

cost of capital each year from holding this asset.

24

Notice that EVA calculated using present value and economic income is zero in

each year of the Nodhead project’s life. For year 2, for example,

EVA ⫽ 100 ⫺ 1.10 ⫻ 1002⫽ 0

Book ROI ⫽

C

1

⫹ 1BV

1

⫺ BV

0

2

BV

0

⫽ C

1

⫹ 1BV

1

⫺ BV

0

2

Book income ⫽ cash flow ⫺ book depreciation

Rate of return ⫽

C

1

⫹ 1PV

1

⫺ PV

0

2

PV

0

Economic income ⫽ cash flow ⫺ economic depreciation

Economic depreciation ⫽ reduction in present value

330 PART III Practical Problems in Capital Budgeting

24

This is a general result. Forecasted profitability always equals the discount rate used to calculate the

estimated future present values.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

III. Practical Problems in

Capital Budgeting

12.Making Sure Managers

Maximize NPV

© The McGraw−Hill

Companies, 2003

EVA should be zero, because the project’s true rate of return is only equal to the cost

of capital. EVA will always give the right signal if income equals economic income

and asset values are measured accurately.

Do the Biases Wash Out in the Long Run?

Some people downplay the problem we have just described. Is a temporary dip in

book profits a major problem? Don’t the errors wash out in the long run, when the

region settles down to a steady state with an even mix of old and new stores?

It turns out that the errors diminish but do not exactly offset. The simplest

steady-state condition occurs when the firm does not grow, but reinvests just

enough each year to maintain earnings and asset values. Table 12.9 shows steady-

state book ROIs for a regional division which opens one store a year. For simplic-

ity we assume that the division starts from scratch and that each store’s cash flows

are carbon copies of the Nodhead store. The true rate of return on each store is,

therefore, 10 percent. But as Table 12.9 demonstrates, steady-state book ROI, at 12.6

percent, overstates the true rate of return. Therefore, you cannot assume that the

errors in book ROI will wash out in the long run.

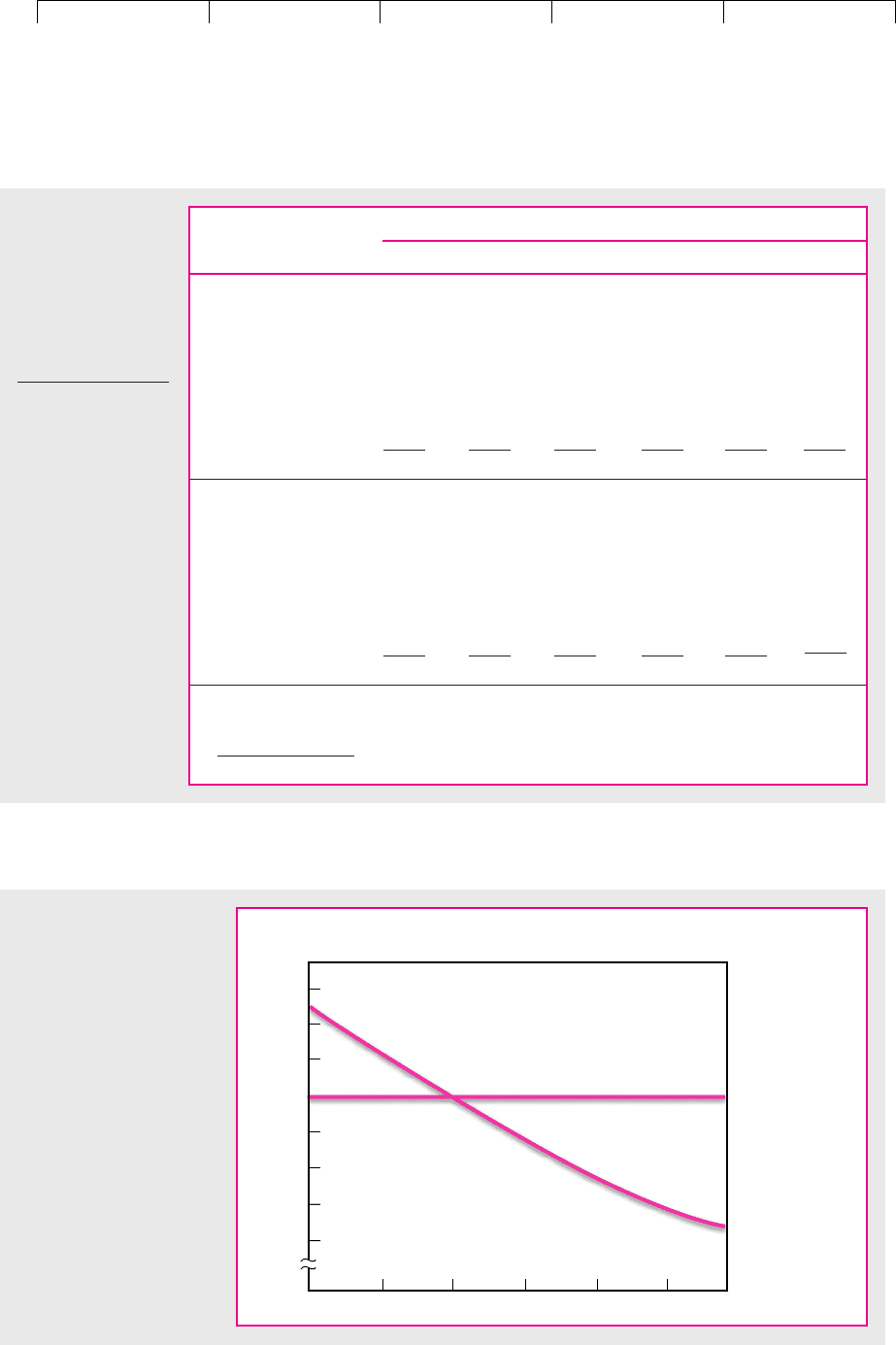

Thus we still have a problem even in the long run. The extent of the error de-

pends on how fast the business grows. We have just considered one steady state

with a zero growth rate. Think of another firm with a 5 percent steady-state growth

rate. Such a firm would invest $1,000 the first year, $1,050 the second, $1,102.50 the

third, and so on. Clearly the faster growth means more new projects relative to old

ones. The greater weight given to young projects, which have low book ROIs, the

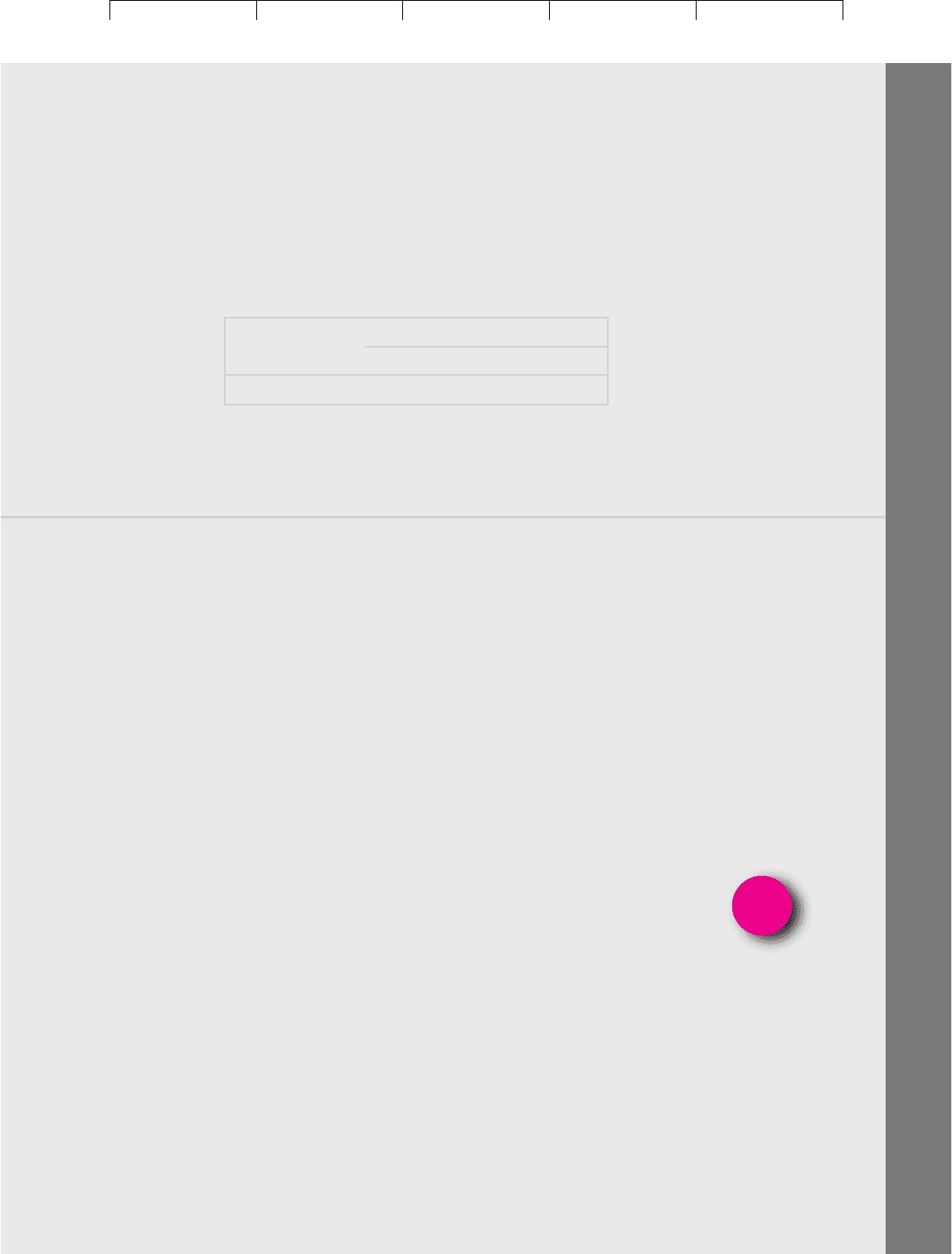

lower the business’ apparent profitability. Figure 12.1 shows how this works out

for a business composed of projects like the Nodhead store. Book ROI will either

overestimate or underestimate the true rate of return unless the amount that the

firm invests each year grows at the same rate as the true rate of return.

25

CHAPTER 12 Making Sure Managers Maximize NPV 331

Year

123456

Cash flow 100 200 250 298 298 298

PV, at start

of year,

10 percent

discount rate 1,000 1,000 901 741 517 271

PV at end

of year,

10 percent

discount rate 1,000 900 741 517 271 0

Change in value

during year 0 ⫺100 ⫺160 ⫺224 ⫺246 ⫺271

Economic income 100 100 90 74 52 27

Rate of return .10 .10 .10 .10 .10 .10

Economic depreciation 0 100 160 224 246 271

TABLE 12.8

Forecasted economic

income and rate of

return for the

proposed Nodhead

store. Economic

income equals cash

flow plus change in

present value. Rate

of return equals

economic income

divided by value at

start of year.

Note: There are minor

rounding errors in some

annual figures.

25

This also is a general result. Biases in steady-state book ROIs disappear when the growth rate equals

the true rate of return. This was discovered by E. Solomon and J. Laya, “Measurement of Company Prof-

itability: Some Systematic Errors in Accounting Rate of Return,” in A. A. Robichek (ed.), Financial Re-

search and Management Decisions, John Wiley & Sons, Inc., New York, 1967, pp. 152–183.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

III. Practical Problems in

Capital Budgeting

12.Making Sure Managers

Maximize NPV

© The McGraw−Hill

Companies, 2003

332 PART III Practical Problems in Capital Budgeting

Year

123456

Book income

for store*

1 ⫺67 ⫹33 ⫹83 ⫹131 ⫹131 ⫹131

2 ⫺67 ⫹33 ⫹83 ⫹131 ⫹131

3 ⫺67 ⫹33 ⫹83 ⫹131

4 ⫺67 ⫹33 ⫹83

5 ⫺67 ⫹33

6 ⫺67

Total book income ⫺67 ⫺34 ⫹49 ⫹180 ⫹311 ⫹442

Book value

for store

1 1,000 833 667 500 333 167

2 1,000 833 667 500 333

3 1,000 833 667 500

4 1,000 833 667

5 1,000 833

6 1,000

Total book value 1,000 1,833 2,500 3,000 3,333 3,500

Book ROI for

all stores ⫽

total book income

total book value

⫺.067 ⫺.019 ⫹.02 ⫹.06 ⫹.093 ⫹.126

†

TABLE 12.9

Book ROI for a group

of stores like the

Nodhead store. The

steady-state book

ROI overstates the

10 percent economic

rate of return.

*Book income ⫽ cash

flow ⫹ change in book

value during year.

†

Steady-state book ROI.

Rate of growth,

percent

Economic rate of return

Book rate of return

Rate of return,

percent

25

2015105

12

11

10

9

8

7

FIGURE 12.1

The faster a firm grows, the

lower its book rate of return

is, providing true prof-

itability is constant and cash

flows are constant or

increasing over project life.

This graph is drawn for a

firm composed of identical

projects, all like the

Nodhead store (Table 12.7),

but growing at a constant

compound rate.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

III. Practical Problems in

Capital Budgeting

12.Making Sure Managers

Maximize NPV

© The McGraw−Hill

Companies, 2003

What Can We Do about Biases in Accounting Profitability Measures?

The dangers in judging profitability by accounting measures are clear from this

chapter’s discussion and examples. To be forewarned is to be forearmed. But we

can say something beyond just “be careful.”

It is natural for firms to set a standard of profitability for plants or divisions. Ide-

ally that standard should be the opportunity cost of capital for investment in the

plant or division. That’s the whole point of EVA: to compare actual profits with the

cost of capital. But if performance is measured by return on investment or EVA,

then these measures need to recognize accounting biases. Ideally, the financial

manager should identify and eliminate accounting biases before judging or re-

warding performance.

This is easier said than done. Accounting biases are notoriously hard to get rid

of. Thus, many firms end up asking not “Did the widget division earn more than

its cost of capital last year?” but “Was the widget division’s book ROI typical of a

successful firm in the widget industry?” The underlying assumptions are that

(1) similar accounting procedures are used by other widget manufacturers and

(2) successful widget companies earn their cost of capital.

There are some simple accounting changes that could reduce biases in perfor-

mance measures. Remember that the biases all stem from not using economic de-

preciation. Therefore why not switch to economic depreciation? The main reason

is that each asset’s present value would have to be reestimated every year. Imag-

ine the confusion if this were attempted. You can understand why accountants set

up a depreciation schedule when an investment is made and then stick to it apart

from exceptional circumstances. But why restrict the choice of depreciation sched-

ules to the old standbys, such as straight-line? Why not specify a depreciation pat-

tern that at least matches expected economic depreciation? For example, the Nod-

head store could be depreciated according to the expected economic depreciation

schedule shown in Table 12.8. This would avoid any systematic biases.

26

It would

break no law or accounting standard. This step seems so simple and effective that

we are at a loss to explain why firms have not adopted it.

27

One final comment: Suppose that you do conclude that a project has earned less

than its cost of capital. This indicates that you made a mistake in taking on the proj-

ect and, if you could have your time over again, you would not accept it. But does

that mean you should bail out now? Not necessarily. That depends on how much

the assets would be worth if you sold them or put them to an alternative use. A

plant that produces low profits may still be worth operating if it has few alterna-

tive uses. Conversely, on some occasions it may pay to sell or redeploy a highly

profitable plant.

Do Managers Worry Too Much about Book Profitability?

Book measures of profitability can be wrong or misleading because

1. Errors occur at different stages of project life. When true depreciation is

decelerated, book measures are likely to understate true profitability for

new projects and overstate it for old ones.

CHAPTER 12

Making Sure Managers Maximize NPV 333

26

Using expected economic depreciation will not generate book ROIs that are exactly right unless real-

ized cash flows exactly match forecasted flows. But we expect forecasts to be right, on average.

27

This procedure has been suggested by several authors, for example by Zvi Bodie in “Compound In-

terest Depreciation in Capital Investment,” Harvard Business Review 60 (May–June 1982), pp. 58–60.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

III. Practical Problems in

Capital Budgeting

12.Making Sure Managers

Maximize NPV

© The McGraw−Hill

Companies, 2003

334 PART III Practical Problems in Capital Budgeting

2. Errors also occur when firms or divisions have a balanced mix of old and

new projects. Our steady-state analysis of Nodhead shows this.

3. Errors occur because of inflation, basically because inflation shows up in

revenue faster than it shows up in costs. For example, a firm owning a plant

built in 1980 will, under standard accounting procedures, calculate

depreciation in terms of the plant’s original cost in 1980 dollars. The plant’s

output is sold for current dollars. This is why the U.S. National Income and

Product Accounts report corporate profits calculated under replacement cost

accounting. This procedure bases depreciation not on the original cost of

firms’ assets, but on what it would cost to replace the assets at current prices.

4. Book measures are often confused by creative accounting. Some firms pick

and choose among available accounting procedures, or even invent new

ones, in order to make their income statements and balance sheets look

good. This was done with particular imagination in the “go-go years” of the

mid-1960s and the late 1990s.

Investors and financial managers have learned not to take accounting prof-

itability at face value. Yet many people do not realize the depth of the problem.

They think that if firms eschewed creative accounting, everything would be all

right except perhaps for temporary problems with very old or very young projects.

In other words, they worry about reason 4, and a little about reasons 1 and 3, but

not at all about 2. We think reason 2 deserves more attention.

SUMMARY

Visit us at www.mhhe.com/bm7e

We began this chapter by describing how capital budgeting is organized and

ended by exposing serious biases in accounting measures of financial perfor-

mance. Inevitably such discussions stress the mechanics of organization, control,

accounting, and performance measurement. It is harder to talk about the informal

procedures that reinforce the formal ones. But remember that it takes informal

communication and personal initiative to make capital budgeting work. Also, the

accounting biases are partly or wholly alleviated because managers and stock-

holders are smart enough to look behind book earnings.

Formal capital budgeting systems usually have four stages:

1. A capital budget for the firm is prepared. This is a plan for capital expenditure by

plant, division, or other business unit.

2. Project authorizations are approved to give authority to go ahead with specific

projects.

3. Procedures for control of projects under construction are established to warn if proj-

ects are behind schedule or are costing more than planned.

4. Postaudits are conducted to check on the progress of recent investments.

Capital budgeting is not entirely a bottom-up process. Strategic planners prac-

tice capital budgeting on a grand scale by attempting to identify those businesses

in which the firm has a special advantage. Project proposals that support the firm’s

accepted overall strategy are much more likely to have clear sailing as they come

up through the organization.

But don’t assume that all important capital outlays appear as projects in the cap-

ital budgeting process. Many important investment decisions may never receive

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

III. Practical Problems in

Capital Budgeting

12.Making Sure Managers

Maximize NPV

© The McGraw−Hill

Companies, 2003

CHAPTER 12 Making Sure Managers Maximize NPV 335

formal financial analysis. First, plant or division managers decide which projects

to propose. Top management and financial staff may never see the alternatives.

Second, investments in intangible assets, for example, marketing and R&D out-

lays, may bypass the capital budget. Third, there are countless routine investment

decisions that must be made by middle management. These outlays are small if

looked at one by one, but they add up.

Capital investment decisions must be decentralized to a large extent. Conse-

quently agency problems are inevitable. Managers are tempted to slack off, to

avoid risk, and to propose empire-building or entrenching investments. Empire

building is a particular threat when plant and divisional managers’ bonuses de-

pend just on earnings or on growth in earnings.

Top management mitigates these agency problems by a combination of moni-

toring and incentives. Many large companies have implemented sophisticated in-

centive schemes based on residual income or economic value added (EVA). In

these schemes, managers’ bonuses depend on earnings minus a charge for capital

employed. There is a strong incentive to dispose of unneeded assets and to acquire

new ones only if additional earnings exceed the cost of capital. Of course EVA de-

pends on accurate measures of earnings and capital employed.

Top management also create agency costs (e.g., empire building). In this case

they are the agents and shareholders are the principals. Shareholders’ interests are

represented by the board of directors and are also protected by delegated monitors

(e.g., the accountants who audit the company’s books).

In most public corporations, top management’s compensation is tied to the per-

formance of the company’s stock. This aligns their interests with shareholders’. But

compensation tied to stock returns is not a complete solution. Stock returns re-

spond to events outside management’s control, and today’s stock prices already re-

flect investors’ expectations of managers’ future performance.

Thus most firms also measure performance by accounting or book profitability.

Unfortunately book income and return on investment (ROI) are often seriously bi-

ased measures of true profitability. For example, book ROIs are generally too low

for new assets and too high for old ones. Businesses with important intangible as-

sets generally have upward-biased ROIs because the intangibles don’t appear on

the balance sheet.

In principle, true or economic income is easy to calculate: You just subtract eco-

nomic depreciation from the asset’s cash flow. Economic depreciation is simply the

decrease in the asset’s present value during the period.

Unfortunately we can’t ask accountants to recalculate each asset’s present

value every time income is calculated. But it does seem fair to ask why they don’t

try at least to match book depreciation schedules to typical patterns of economic

depreciation.

FURTHER

READING

The most extensive study of the capital budgeting process is:

J. L. Bower: Managing the Resource Allocation Process, Division of Research, Graduate School

of Business Administration, Harvard University, Boston, 1970.

The article by Pohlman, Santiago, and Markel is a more up-to-date survey of current practice:

R. A. Pohlman, E. S. Santiago, and F. L. Markel: “Cash Flow Estimation Practices of Large

Firms,” Financial Management, 17:71–79 (Summer 1988).

Visit us at www.mhhe.com/bm7e

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

III. Practical Problems in

Capital Budgeting

12.Making Sure Managers

Maximize NPV

© The McGraw−Hill

Companies, 2003

336 PART III Practical Problems in Capital Budgeting

For an easy-to-read description of EVA, with lots of success stories, see

A. Ehrbar: EVA: The Real Key to Creating Wealth, John Wiley & Sons, Inc., New York, 1998.

Biases in book ROI and procedures for reducing the biases are discussed by:

E. Solomon and J. Laya: “Measurement of Company Profitability: Some Systematic Errors

in the Accounting Rate of Return,” in A. A. Robichek (ed.), Financial Research and Manage-

ment Decisions, John Wiley & Sons, Inc., New York, 1967, pp. 152–183.

F. M. Fisher and J. I. McGowan: “On the Misuse of Accounting Rates of Return to Infer Mo-

nopoly Profits,” American Economic Review, 73:82–97 (March 1983).

J. A. Kay: “Accountants, Too, Could Be Happy in a Golden Age: The Accountant’s Rate of

Profit and the Internal Rate of Return,” Oxford Economic Papers, 28:447–460 (1976).

Z. Bodie: “Compound Interest Depreciation in Capital Investment,” Harvard Business Re-

view, 60:58–60 (May–June 1982).

QUIZ

1. True or false?

a. The approval of a capital budget allows managers to go ahead with any project

included in the budget.

b. Capital budgets and project authorizations are mostly developed “bottom up.”

Strategic planning is a “top-down” process.

c. Project sponsors are likely to be overoptimistic.

d. Investments in marketing (for new products) and R&D are not capital outlays.

e. Many capital investments are not included in the company’s capital budget. (If

true, give some examples.)

f. Postaudits are typically undertaken about five years after project completion.

2. Explain how each of the following actions or problems can distort or disrupt the capi-

tal budgeting process.

a. Overoptimism by project sponsors.

b. Inconsistent forecasts of industry and macroeconomic variables.

c. Capital budgeting organized solely as a bottom-up process.

d. A demand for quick results from operating managers, e.g., requiring new capital

expenditures to meet a payback constraint.

3. What is the practical implication of Brealey and Myers’s Second Law? The law reads,

“The proportion of proposed projects having a positive NPV at the corporate hurdle

rate is independent of the hurdle rate.”

4. Define the following: (a) Agency costs in capital investment, (b) private benefits, (c) em-

pire building, (d) free-rider problem, (e) entrenching investment, (f) delegated monitoring.

5. Monitoring alone can never completely eliminate agency costs in capital investment.

Briefly explain why.

6. Here are several questions about economic value added or EVA.

a. Is EVA expressed as a percentage or a dollar amount?

b. Write down the formula for calculating EVA.

c. What is the difference, if any, between EVA and residual income?

d. What is the point of EVA? Why do firms use it?

e. Does the effectiveness of EVA depend on accurate measures of accounting income

and assets?

7. The Modern Language Division earned $1.6 million on net assets of $20 million. The cost

of capital is 11.5 percent. Calculate the net percentage return on investment and EVA.

8. True or false? Briefly explain your answers.

a. Accountants require companies to write off outlays for R&D as current expenses.

This makes R&D-intensive companies look less profitable than they really are.

Visit us at www.mhhe.com/bm7e

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

III. Practical Problems in

Capital Budgeting

12.Making Sure Managers

Maximize NPV

© The McGraw−Hill

Companies, 2003

CHAPTER 12 Making Sure Managers Maximize NPV 337

b. Companies with valuable intangible assets will show upward-biased accounting

rates of return.

9. Fill in the blanks:

“A project’s economic income for a given year equals the project’s __________ less its

__________ depreciation. Book income is typically __________ than economic income

early in the project’s life and __________ than economic income later in its life.”

10. Consider the following project:

Period

012 3

Net cash flow ⫺100 0 78.55 78.55

The internal rate of return is 20 percent. The NPV, assuming a 20 percent opportunity

cost of capital, is exactly zero. Calculate the expected economic income and economic de-

preciation in each year.

PRACTICE

QUESTIONS

1. Discuss the value of postaudits. Who should conduct them? When? Should they con-

sider solely financial performance? Should they be confined to the larger projects?

2. Draw up an outline or flowchart tracing the capital budgeting process from the initial

idea for a new investment project to the completion of the project and the start of oper-

ations. Assume the idea for a new obfuscator machine comes from a plant manager in

the Deconstruction Division of the Modern Language Corporation.

Here are some questions your outline or flowchart should consider: Who will pre-

pare the original proposal? What information will the proposal contain? Who will eval-

uate it? What approvals will be needed, and who will give them? What happens if the

machine costs 40 percent more to purchase and install than originally forecasted? What

will happen when the machine is finally up and running?

3. Compare typical compensation and incentive arrangements for (a) top management,

for example, the CEO or CFO, and (b) plant or division managers. What are the chief

differences? Can you explain them?

4. Suppose all plant and division managers were paid only a fixed salary—no other in-

centives or bonuses.

a. Describe the agency problems that would appear in capital investment decisions.

b. How would tying the managers’ compensation to EVA alleviate these problems?

5. Table 12.10 shows a condensed income statement and balance sheet for Androscoggin

Copper’s Rumford smelting plant.

a. Calculate the plant’s EVA. Assume the cost of capital is 9 percent.

b. As Table 12.10 shows, the plant is carried on Androscoggin’s books at $48.32

million. However, it is a modern design, and could be sold to another copper

company for $95 million. How should this fact change your calculation of EVA?

6. Here are a few questions about compensation schemes that tie top management’s com-

pensation to the rate of return earned on the company’s common stock.

a. Today’s stock price depends on investors’ expectations of future performance.

What problems does this create?

b. Stock returns depend on factors outside the managers’ control, for example,

changes in interest rates or prices of raw materials. Could this be a serious

problem? If so, can you suggest a partial solution?

c. Compensation schemes that depend on stock returns do not depend on accounting

income or ROI. Is that an advantage? Why or why not?

Visit us at www.mhhe.com/bm7e

EXCEL

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

III. Practical Problems in

Capital Budgeting

12.Making Sure Managers

Maximize NPV

© The McGraw−Hill

Companies, 2003

338 PART III Practical Problems in Capital Budgeting

7. Herbal Resources is a small but profitable producer of dietary supplements for pets.

This is not a high-tech business, but Herbal’s earnings have averaged around $1.2 mil-

lion after tax, largely on the strength of its patented enzyme for making cats nonaller-

genic. The patent has eight years to run, and Herbal has been offered $4 million for the

patent rights.

Herbal’s assets include $2 million of working capital and $8 million of property,

plant, and equipment. The patent is not shown on Herbal’s books. Suppose Herbal’s

cost of capital is 15 percent. What is its EVA?

8. List and define the agency problems likely to be encountered in a firm’s capital invest-

ment decisions.

9. Large brokerage and investment companies, such as Merrill Lynch and Morgan Stan-

ley Dean Witter, employ squadrons of security analysts. Each analyst devotes full time

to an industry—aerospace, for example, or insurance—and issues reports and buy,

hold, or sell recommendations for companies in the industry. How do security analysts

help overcome free-rider problems in monitoring management? How do they help

avoid agency problems in capital investment?

10. What is meant by delegated monitoring? Who are these monitors and what roles do

they play?

11. True or false? Explain briefly.

a. Book profitability measures are biased measures of true profitability for individual

assets. However, these biases “wash out” when firms hold a balanced mix of old

and new assets.

b. Systematic biases in book profitability would be avoided if companies used

depreciation schedules that matched expected economic depreciation. However,

few, if any, firms have done this.

12. Calculate the year-by-year book and economic profitability for investment in polyzone

production, as described in Chapter 11. Use the cash flows and competitive spreads

shown in Table 11.2.

What is the steady-state book rate of return (ROI) for a mature company produc-

ing polyzone? Assume no growth and competitive spreads.

13. Suppose that the cash flows from Nodhead’s new supermarket are as follows:

Income Statement for 2001 Assets, December 31, 2001

Revenue $56.66 Net working capital $7.08

Raw materials cost 18.72

Operating cost 21.09 Investment in plant and equipment 69.33

Depreciation 4.50 Less accumulated depreciation 21.01

Pretax income 12.35 Net plant and equipment 48.32

Tax at 35% 4.32

Net income $8.03 Total assets $55.40

TABLE 12.10

Condensed financial

statements for the Rumford

smelting plant. See practice

question 5 (figures in $

millions).

Visit us at www.mhhe.com/bm7e

Year

0123456

Cash flows ($ thousands) ⫺1,000 ⫹298 ⫹298 ⫹298 ⫹138 ⫹138 ⫹138

a. Recalculate economic depreciation. Is it accelerated or decelerated?

b. Rework Tables 12.7 and 12.8 to show the relationship between the “true” rate of

return and book ROI in each year of the project’s life.

EXCEL