Brealey, Myers. Principles of Corporate Finance. 7th edition

Подождите немного. Документ загружается.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

Back Matter Appendix B Answers to

Quizzes

© The McGraw−Hill

Companies, 2003

c. Project interactions may be ignored. Some op-

portunities, such as the closing or sale of a divi-

sion, will not be considered. Strategic invest-

ments may be missed.

d. Creates a bias in favor of quick payback projects

and against long-lived projects that may have

large NPVs.

3. A change in the hurdle rate is offset by more or less

optimistic forecasts by project sponsors. There’s no

way out: the financial manager can’t avoid careful

assessment of cash-flow forecasts.

4. Agency costs: value lost when managers do not act

to maximize value. This includes costs of monitor-

ing and control.

Private benefits: perks or other advantages enjoyed

by managers.

Empire building: investing for size, not NPV.

Free-rider problem: when one shareholder, or group

of shareholders, acts to monitor and control man-

agement, all shareholders benefit.

Entrenching investment: managers choose or design

investment projects which increase the managers’

value to the firm.

Delegated monitoring: monitoring on behalf of

principals. For example, the board of directors

monitors management performance on behalf of

stockholders.

5. Monitoring is costly and encounters diminishing

returns. Also, completely effective monitoring

would require perfect information.

6. (a) Dollar amount; (b) EVA Income earned

(cost of capital investment); (c) They are essen-

tially the same; (d) EVA makes the cost of capital

visible to managers. Compensation based on EVA

encourages them to dispose of unnecessary assets

and to forego investment unless it earns more than

the cost of capital; (e) Yes.

7. Return on investment 1.6/20 .08 or 8%. EVA

1.6 (.115 20) $.7 million. EVA is negative.

8. (a) False: profits may be depressed temporarily, but

in a steady state, writing off R&D can increase the

book rate of return; (b) true—because asset value is

understated, the ratio of income to assets is biased

upward.

9. Cash flow, economic, less, greater.

APPENDIX B Answers to Quizzes 1023

10.

Year 1 Year 2 Year 3

Cash flow 0 78.55 78.55

PV at start of year 100.00 120.00 65.45

PV at end of year 120.00 65.45 0

Change in value during year 20.00 54.55 65.45

Expected economic income 20.00 24.00 13.10

Chapter 13

1. c

2. Weak, semistrong, strong, strong, weak.

3. (a) False; (b) false; (c) true; (d) false; (e) false; (f) true.

4. (a) Decline to $200; (b) less; (c) A slight abnormal

fall (the split is likely to have led investors to expect

an above-average rise in dividends).

5. (a) False; (b) true; (c) false; (d) true; (e) false; (f) true

(a small change in price in the absence of new infor-

mation causes a large increase in demand).

6. .

7. (a) True; (b) false; (c) true; (d) true.

8. Decrease. The stock price already reflects an ex-

pected 25% increase. The 20% increase conveys bad

news relative to expectations.

9. a. An investor should not buy or sell shares based

on apparent trends or cycles in returns.

b. A CFO should not speculate on changes in interest

rates or foreign exchange rates. There is no reason

to think that the CFO has superior information.

6 1.2 1.45 521.05%

c. A financial manager evaluating the creditwor-

thiness of a large customer could check the cus-

tomer’s stock price and the yield on its debt. A

falling stock price or a high yield could indicate

trouble ahead.

d. Don’t assume that accounting choices which in-

crease or decrease earnings will have any effect

on stock price.

e. The company should not seek diversification

just to reduce risk. Investors can diversify on

their own.

f. Stock issues do not depress price if investors be-

lieve the issuer has no private information.

Chapter 14

1. Internally generated cash 77

Financial deficit 23

Net share issues 14

Debt issues 38

2. (a) False; (b) true; (c) true; (d) false.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

Back Matter Appendix B Answers to

Quizzes

© The McGraw−Hill

Companies, 2003

3. (a) ; (b) 78,000 shares;

(c) 2,000 shares are held as Treasury stock; (d) 20,000

shares.

40,000/.50 80,000 shares

7. a. Net proceeds of public issue 10,000,000

150,000 80,000 $9,770,000; net proceeds of

private placement $9,970,000.

b. PV of extra interest on private placement

i.e., extra cost of higher interest on private place-

ment more than outweighs saving in issue costs.

N.b. We ignore taxes.

c. Private placement debt can be custom-tailored

and the terms more easily renegotiated.

8. An underwriter building a book solicits bids from

investors, but the bids are not binding and are used

only as a guide to set the issue price.

9. (a) Number of new shares, 50,000; (b) Amount of

new investment, $500,000; (c) Total value of com-

pany after issue, $4,500,000; (d) Total number of

shares after issue, 150,000; (e) Stock price after issue,

$4,500,000/150,000 $30; (f) The opportunity to

buy one share is worth $20.

Chapter 16

1. (a) A1, B5; A2, B4; A3, B3; A4, B1; A5, B2. (b) March

7 ex-dividend date; (c) (.34 4)/80.20 .017, or

1.7%; (d) (.34 4)/3.20 .43 or 43%; (e) The price

would fall to .

2. (a) .26; (b) .36.

3. (a) False; (b) true.

4. a. False. The dividend depends on past dividends

and current and forecasted earnings.

b. True. This target does reflect growth opportuni-

ties and capital expenditure requirements.

c. False. Dividends are adjusted gradually to a tar-

get. The target is based on current or forecasted

earnings multiplied by the target payout ratio.

d. True. Dividend changes convey information to

investors.

e. False. Dividends are “smoothed.” Managers

rarely increase regular dividends temporarily.

They may pay a special dividend, however.

f. False. Dividends are rarely cut when repur-

chases are being made.

80.20/1.1 $

ˇ 72.91

a

10

t1

.005 10,000,000

1.085

t

$ˇ 328,000,

1024 APPENDIX B Answers to Quizzes

(e) (f)

Common stock $ 45,000 $40,000

Additional paid-in 25,000 10,000

capital

Retained earnings 30,000 30,000

Common equity 100,000 80,000

Treasury stock 5,000 30,000

Net common $ 95,000 $50,000

equity

4. (a) 80 votes; (b) .

5. Similarities with debt: (a) Fixed income; (b) preferred

stockholders have limited voting rights.

Similarities with equity: (a) Dividend is within

discretion of directors; (b) no final repayment date;

(c) dividend is not an allowable deduction from

taxable profits.

6. (a) subordinated; (b) floating rate; (c) convertible;

(d) warrant; (e) common stock; preferred stock.

7. (a) False; (b) true; (c) false.

8. A debt issue sold in international markets.

9. Support of the payment mechanism, facilitating

borrowing and lending, pooling risk.

Chapter 15

1. (a) Further sale of an already publicly traded stock;

(b) U.S. bond issue by foreign corporation; (c) Bond

issue by industrial company; (d) Bond issue by

large industrial company.

2. (a) B; (b) A; (c) D; (d) C.

3. a. Financing of startup companies.

b. First sale of a security to public investors.

c. Trading of a security after it is issued.

d. Description of a security offering filed with

the SEC.

e. Winning bidders for a new issue tend to

overpay.

f. One or a few underwriters buy an entire issue.

4. (a) A large issue; (b) a bond issue; (c) subsequent is-

sue of stock; (d) a small private placement of bonds.

5. (a) False; (b) true; (c) true.

6. (a) 135,000 shares; (b) primary: 500,000 shares; sec-

ondary: 400,000 shares; (c) $25 or 31%, which is

higher than the average underpricing.

10 80 800 votes

Millions

Underwriting cost $ 5.04

Administrative cost .82

Underpricing 22.5

Total $28.36

Note: Calculation ignores cost of shares sold

under greenshoe option.

(d)

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

Back Matter Appendix B Answers to

Quizzes

© The McGraw−Hill

Companies, 2003

5. a. Reinvest in the stock. If

the ex-dividend price is , this

should involve the purchase of 500/147.50, or

about 3.4 shares.

b. Sell shares worth . If the ex-

dividend price is , this should involve

the sale of 3,000/195, or about 15 shares.

6. (a) Raise an additional £2 million by an issue of

shares; (b) Reduce cash by $10 million or issue new

shares for $10 million.

7. a. Company value is unchanged at

. Share price stays at $140.

b. The discount rate r (DIV

1

/P

0

) g (20/140)

.05 .193. The price at which shares are re-

purchased in year 1 is 140 (1 r) 140

1.193 $167. Therefore the firm repurchases

50,000/167 299 shares. Total dividend pay-

ments in year 1 fall to 5,000 10 $50,000,

which is equivalent to 50,000/(5000 299)

$

ˇ 700,000

5,000 140

$ˇ 200 $ˇ 5

1,000 $

ˇ 3 $ˇ 3,000

$

ˇ 150 $ˇ 2.50

1,000 $

ˇ .50 $ˇ 500 $10.64 a share. Similarly, in year 2 the firm re-

purchases 281 shares at $186.52 and the divi-

dend per share increases by 11.7% to $11.88. In

each subsequent year total dividends increase

by 5%, the number of shares declines by 6% and

therefore dividends per share increase by 11.7%.

The constant growth model gives PV share

10.64/(.193 .117) $140.

8. a. $127.25.

b. Nothing; the stock price will stay at $130.

846,154 shares will be repurchased.

c. The with-dividend price stays at $130. Ex-

dividend it drops to $124.50; 883,534 shares will

be issued.

9. Current tax law: (a) shouldn’t care; (b) prefers Lo;

(c) prefers Hi; (d) shouldn’t care; (e) shouldn’t care.

Same rate of tax: An individual now shouldn’t care.

Otherwise preferences do not change.

APPENDIX B Answers to Quizzes 1025

Market Value

Common stock $16,000,000

(8 million shares at $2)

Short-term loans $ 2,000,000

Chapter 17

1. (a) .10P; (b) Buy 10% of B’s debt 10% of B’s eq-

uity; (c) .10(P 100); (d) Borrow an amount equal

to 10% of B’s debt and buy 10% of A’s equity.

2. Note the market value of Copperhead is far in ex-

cess of its book value:

.13 20/60(.13 .08) .147. If stockholders

pass on more of the firm’s risk to debtholders, ex-

pected return on equity will be less than 14.7%.

4. a. (i)

A

.

(ii) ; (iii) .

b. (i) .10.

(ii)

.

(iii) ; (iv) .

c. (i) 50%; (ii) 6.7 (i.e., the P/E ratio falls to offset

the increase in EPS).

r

A

.10r

D

.05

r

E

.15

.10 1.5 .052 1.5 r

E

2

r

A

a

D

D E

r

D

b a

E

D E

r

E

b

A

1.0

D

0

E

2.0

1.0 1.5 02 1.5

E

2

a

D

D E

D

b a

E

D E

E

b

5. a.

Operating income ($) 500 1,000 1,500 2,000

Interest ($) 250 250 250 250

Equity earnings ($) 250 750 1,250 1,750

Earnings per share .33 1.00 1.67 2.33

Return on shares (%) 3.3 10 16.7 23.3

Ms. Kraft owns .625% of the firm, which proposes

to increase common stock to $17 million and cut

short-term debt. Ms. Kraft can offset this by (a) bor-

rowing .00625 1,000,000 $6,250, and (b) buying

that much more Copperhead stock.

3. Expected return on assets is r

A

.08 30/80 .16

50/80 .13. The new return on equity will be r

E

b.

.

E

1.07

.8 1.25 02 1.75

E

2

A

a

D

D E

D

b a

E

D E

E

b

6. a. True, so long as the market value of “old” debt

does not change.

b. False. MM’s Proposition I says only that overall

firm value does not depend on

capital structure.

1V D E2

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

Back Matter Appendix B Answers to

Quizzes

© The McGraw−Hill

Companies, 2003

c. False. Borrowing increases equity risk even if

debt is default-risk-free.

d. False. Limited liability affects the relative values

of debt and equity, not their sum.

e. True. Limited liability protects shareholders if

the firm defaults.

f. True—but the required rate of return on equity

and the firm’s assets are the same only if the firm

holds risk-free assets. In this case , and all

equal the risk-free rate of interest.

g. False. The shareholders could make the same

debt issue on their own account.

h. True. To put it more precisely, it assumes that the

expected rate of return to equity goes up, but

stockholders’ required rate of return goes up pro-

portionately. Therefore, stock price is unchanged.

i. False. The formula

does not require .

j. False. The clientele has to be willing to pay extra

for the debt, which it will not do if plenty of cor-

porate debt issues are already available.

7. See Figure 17.5.

8. (a) ; (b) (unchanged),

; (c) 18.3%.

9. (a) 10%; (b) 13.3%.

10. (a) Not affected; (b) 16 million; (c) $250 million;

(d) ; (e) No one.

11. (a) It rises by $2 per share or $30 million; (b) 5 million;

(c) $250 million (unchanged); (d) (us-

ing market values); (e) Shareholders gain, investors

in old debt lose.

Chapter 18

1. a. PV tax

b. .

c. PV tax .

2. a. PV tax .

b. .

c. New PV tax .

Therefore, company

$151.67

.

3. a. Relative advantage of

b. Relative .advantage .69/1.6921.652 1.54

.69

1121.652

1.06.

debt

1 T

p

11 T

pE

211 T

C

2

value 168 24 7.67

shield

a

5

t1

.401.08 602

11.082

t

$ˇ 7.67

T

C

20 $ˇ 8

shield T

C

D $ˇ 16

shield T

C

D $ˇ 350

a

5

t1

.351.08 10002

11.082

t

$ˇ 111.80PV tax shield

25.93.

shield

T

C

1r

D

D2

1 r

D

.351.08 10002

1.08

130/250 .52

D/V 160/250 .64

D

.3,

E

.9

A

.6r

A

.15, r

E

.175

r

D

a constant

r

E

r

A

1D/E21r

A

r

D

2

r

E

r

A

, r

D

4. a. Direct costs of financial distress are the legal and

administrative costs of bankruptcy. Indirect costs

include possible delays in liquidation (Eastern

Airlines) or poor investment or operating deci-

sions while bankruptcy is being resolved. Also

the threat of bankruptcy can lead to costs.

b. If financial distress increases odds of default, man-

agers’ and shareholders’ incentives change. This

can lead to poor investment or financing decisions.

c. See the answer to 4(b). Examples are the “games”

described in Section 18.3.

5. Not necessarily. Announcement of bankruptcy can

send a message of poor profits and prospects. Part

of the share price drop can be attributed to antici-

pated bankruptcy costs, however.

6. A firm with no taxable income saves no taxes by bor-

rowing and paying interest. The interest payments

would simply add to its tax-loss carry-forwards.

Such a firm would have little tax incentive to borrow.

7. a. Stockholders win. Bond value falls, since the

value of assets securing the bond has fallen.

b. Bondholder wins if we assume the cash is left in-

vested in Treasury bills. The bondholder is sure

to get $26 plus interest. Stock value is zero, be-

cause there is no chance that firm value can rise

above $50.

c. The bondholders lose. The firm adds assets

worth $10 and debt worth $10. This would in-

crease Circular’s debt ratio, leaving the old

bondholders more exposed. The old bondhold-

ers’ loss is the stockholders’ gain.

d. Both bondholders and stockholders win. They

share the (net) increase in firm value. The bond-

holders’ position is not eroded by the issue of a

junior security. (We assume that the preferred

does not lead to still more game playing and that

the new investment does not make the firm’s as-

sets safer or riskier.)

e. Bondholders lose because they are at risk for

longer. Stockholders win.

8. Specialized, intangible assets such as growth op-

portunities are most likely to lose value in financial

distress. Safe, tangible assets with good second-

hand markets are least likely to lose value. Costs of

financial distress are thus likely to be less for, say,

real estate firms or trucking companies than for ad-

vertising firms or high-tech growth companies.

9. More profitable firms have more taxable income to

shield and are less likely to incur the costs of dis-

tress. Therefore the trade-off theory predicts high

(book) debt ratios. In practice the more profitable

companies borrow least.

10. Firms have a pecking order for new financing. In-

ternal finance is preferred, followed by debt and

1026 APPENDIX B Answers to Quizzes

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

Back Matter Appendix B Answers to

Quizzes

© The McGraw−Hill

Companies, 2003

then by external equity. Each firm’s observed debt

ratio reflects its cumulative requirements for exter-

nal finance. The more profitable companies borrow

least because they have sufficient internal finance.

11. When a company issues securities, outside investors

worry that management may have unfavorable in-

formation. If so the securities can be overpriced. This

worry is much less with debt than equity. Debt secu-

rities are safer than equity, and their price is less af-

fected if unfavorable news comes out later.

A company that can borrow (without incur-

ring substantial costs of financial distress) usually

does so. An issue of equity would be read as “bad

news” by investors, and the new stock could be

sold only at a discount to the previous market

price.

12. Financial slack is most valuable to growth compa-

nies with good but uncertain investment opportu-

nities. Slack means that financing can be raised

quickly for positive-NPV investments. But too

much financial slack can tempt mature companies

to overinvest. Increased borrowing can force such

firms to pay out cash to investors.

Chapter 19

1. Market values of debt and equity are D .9 75

$67.5 million and E 42 2.5 $105 million.

D/V .39.

The key assumptions: stable capital structure (D/V

constant); Federated will pay taxes at 35% marginal

rate in all relevant future years; use WACC as dis-

count rate for projects with same risk as average of

firm’s assets.

2. Step 1: .

Step 2: r

D

.086, r

E

.145 (.145 .086)(15/85)

.155.

Step 3: WACC .086(1 .35).15 .155(.85) .14.

3. (a) False; (b) true; (c) true.

4. The method values the equity of a company by dis-

counting cash flows to stockholders at the cost of

equity. See Section 4.5 for more details. The method

assumes that the debt-to-equity ratio will remain

constant.

r .091.392 .181.612 .145

WACC .0911 .352.39 .181.612 .1325, or 13.25%.

5. (a) True; (b) false, if interest tax shields are valued

separately; (c) true; (d) true.

6. Rule 1 assumes that debt supported by a project is

paid off on a fixed schedule regardless of project per-

formance. Rule 2 assumes that debt is rebalanced to

keep the ratio of debt to project value constant.

7. Acceptance of a project triggers financing costs or

benefits. Examples: interest tax shields, issue

costs, subsidized financing tied to the project.

Other side effects are encountered in international

investment.

8. APV base-case NPV PV financing side effects

(a) APV 0 .15(500,000) 75,000; (b) APV 0

175,000 175,000; (c) APV 0 76,000

76,000

9. a. 12%, of course.

b. ,

WACC .075(1 .35)(.30) .139(.70) .112, or 11.2%.

10. PV tax shield (.10/.35)576,000 $164,600; APV

170,000 164,600 $334,600.

11. a. Base-case NPV 1,000 1200/1.20 0.

b. PV tax shield (.35 .1 .3(1000))/1.1 9.55.

APV 0 9.55 $9.55.

12. No. The more debt you use, the higher rate of

return equity investors will require. (Lenders may

demand more also.) Thus there is a hidden cost of

the “cheap” debt: It makes equity more expensive.

13. The after-tax borrowing or lending rate. This as-

sumes that the company can lend or borrow at a

safe after-tax rate.

14. PV 16(1 .35)/(1 .055(1 .35)) $10.04 million.

Chapter 20

1. Call; exercise; put; European; call; assets; bondholders

(lenders); assets; promised payment to bondholders.

2. Figure 20.13a represents a call seller; Figure 20.13b

represents a call buyer.

3. a. The exercise price of the put option (i.e., you’d

sell stock for the exercise price);

b. The value of the stock (i.e., you would throw

away the put and keep the stock).

4. Value of call PV(exercise price) value of put

value of asset (e.g., share).

See table below.

r

E

.12 1.12 .075 2130/702 .139

APPENDIX B Answers to Quizzes 1027

At Maturity: Share Price Exceeds Exercise Price Share Price Below Exercise Price

Action Value Action Value

Call PV(EX) Exercise call Stock price Don’t exercise call Exercise price

Put share Don’t exercise put Stock price Exercise put Exercise price

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

Back Matter Appendix B Answers to

Quizzes

© The McGraw−Hill

Companies, 2003

Relationship holds only for European options with

same exercise price.

5. Buy a call and lend the present value of the exercise

price.

6. a. Keep gold stocks and buy 6-month puts with an

exercise price equal to 83.3% of the current price.

b. Sell gold stocks, invest for 6 months at

6%. The remaining can be used to buy

calls on the gold stocks with the same exercise

price.

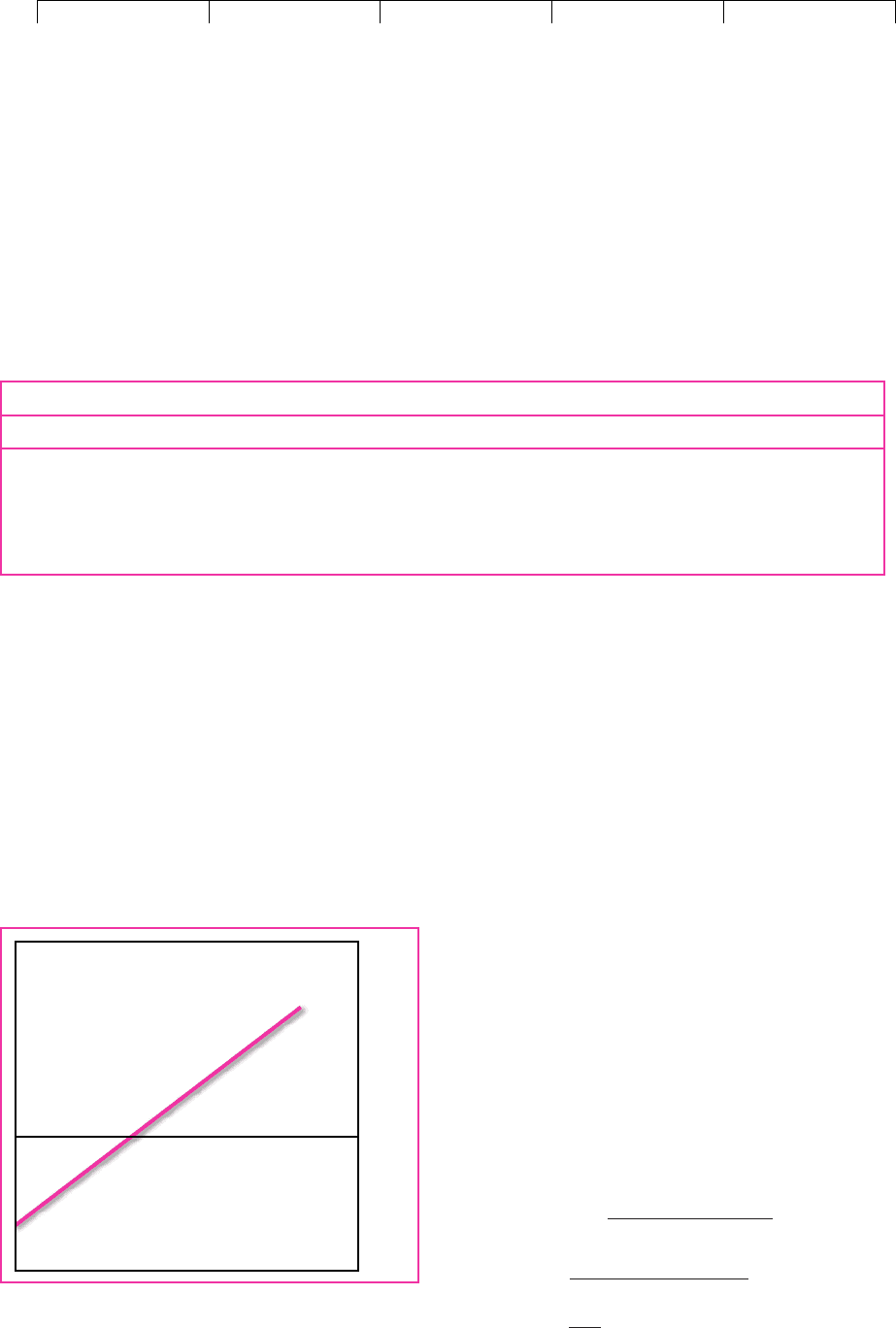

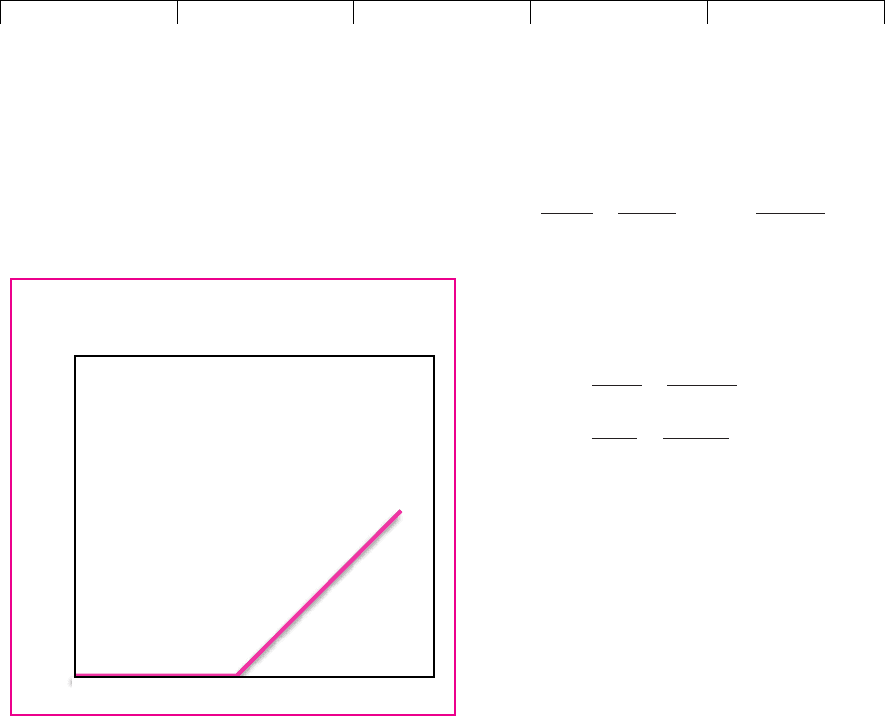

7. (a) See Figure 4; (b) stock price

PV(EX) 100

100/1.1 $9.09.

£115,000

£485,000

1028 APPENDIX B Answers to Quizzes

8.

At Maturity: Asset Value Exceeds Loan Asset Value Below Loan

Action Value Action Value

Call on assets Exercise call Assets Don’t exercise Zero

with exercise amount of loan call

price amount

of loan

Common stock Repay loan Assets Default Zero

amount of loan

9. Stockholders have the option to walk away from

their debts, in which case lender takes over assets.

Default put is important for firms in distress (i.e.,

asset value low relative to amount of loan).

10. The lower bound is the option’s value if it expired

immediately: either zero or the stock price less

the exercise price, whichever is larger. If an

(American) call option’s price were less than the

lower bound, you could exercise immediately

and make a sure profit. The upper bound is the

stock price.

11. Figure 20.13(b) doesn’t show the cost of purchasing

the call. The profit from call purchase would be

negative for all stock prices less than exercise price

plus cost of call. Figure 20.13(a) doesn’t record the

proceeds from selling the call.

12. (a) Zero; (b) Stock price less the present value of the

exercise price.

13. The call price (a) increases; (b) decreases; (c) in-

creases; (d) increases; (e) decreases; (f) decreases.

14. a. All investors, however risk-averse, should

value more highly an option on a volatile stock.

For both Exxon Mobil and AOL the option is

valueless if stock price is below the exercise

price, but the option on AOL has more upside

potential.

b. Other things equal, stockholders lose and

debtholders gain if the company shifts to safer as-

sets. When the assets are risky, the default put is

more valuable. Debtholders bear much of the

losses if asset value declines, but shareholders get

the gains if asset value increases.

Chapter 21

1. a. Using risk-neutral method, (p 20) (1 p)

(16.7) 1, p .48.

.

b.

.

8

14.7

.544

Delta

spread of option prices

spread of stock prices

Value of call

1.48 82 1.52 02

1.01

3.8.

Payoff

Stock

price

100

FIGURE 4

Chapter 20, Quiz question 7.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

Back Matter Appendix B Answers to

Quizzes

© The McGraw−Hill

Companies, 2003

c.

2. The period to expiration is subdivided into an in-

definitely large number of subperiods (and when

there is no incentive to early exercise).

3. (a) No. The maximum delta is 1.0 when the ratio

of stock price to exercise price is very high. (b) No.

(c) Delta increases. (d) Delta increases.

4. Because option risk changes as time passes and the

stock price changes.

APPENDIX B Answers to Quizzes 1029

Current Possible Future

Cash Flow Cash Flows

Buy call 3.8 0 8.0

equals

Buy .544 shares 21.8 18.2 26.2

Borrow 18.0 18.0 18.2 18.2

3.8 0 8.0

d. Possible stock prices with call option prices in

parentheses:

40

(4.0)

33.3 48.0

(0) (8.4)

27.8 40 57.6

(0) (0) (17.6)

Option prices were calculated as follows:

Month 1: (i) ,

(ii) .

Month 0: .

e. .Delta

spread of option prices

spread of stock prices

8.4

14.7

.57

1.48 8.42 1.52 02

1.01

4.0

1.48 17.62 1.52 02

1.01

8.4

1.48 02 1.52 02

1.01

0

5. Using the replicating portfolio method, delta 13.33/(73.33

41.25) .416.

Current Possible Future

Cash Flow Cash Flows

Buy call 6.05 0 13.33

equals

Buy .416 shares 22.86 17.14 30.48

Borrow 16.81 16.81 17.14 17.14

6.05 0 13.33

Using the risk-neutral method, (p 33.3) (1 p)

(25) 2, p .463.

The put price is 9.87.

Value of call

1.463 13.332 1.537 02

1.02

6.05.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

Back Matter Appendix B Answers to

Quizzes

© The McGraw−Hill

Companies, 2003

6. Using the replicating portfolio method, delta

13.75/(68.75 44) .556.

Value of call

1.489 13.752 1.511 02

1.02

6.59.

1030 APPENDIX B Answers to Quizzes

Current Possible Future

Cash Flow Cash Flows

Buy call 6.59 0 13.75

equals

Buy .556 shares 30.56 24.44 38.19

Borrow 23.97 23.97 24.44 24.44

6.59 0 13.75

Using the risk-neutral method, (p 25) (1 p)

(20) 2, p .489.

Lower risk means less upside for the call option.

Thus option value falls.

7. a. .

b.

Delta 100/1200 502 .667

Current Possible Future

Cash Flow Cash Flows

Buy call 36.36 0 100

equals

Buy .667 shares 66.67 33.33 133.33

Borrow 30.30 30.30 33.33 33.33

36.36 0 100

c. .

d.

e. No. The true probability of a price rise is almost

certainly higher than the risk-neutral probabil-

ity, but it does not help to value the option.

8. a. Call value $3.44.

b. Put value call value PV(exercise price)

stock price $1.67.

9. True; as the stock price rises, the risk of the option falls.

10. a. You would exercise early if the stock price was suf-

ficiently low. There may be little opportunity for

further gains in the option value and it would be

better to invest the exercise price to earn interest.

b. Don’t exercise early. The interest savings from

delaying payment of the exercise price is larger

than the dividend foregone.

c. If the stock price and dividend are sufficiently

high, it may pay to exercise early to capture the

dividend.

Chapter 22

1. Expansion option; abandonment option; timing

option (i.e., option to postpone investment); flexi-

Value of call

1.4 1002 1.6 02

1.10

36.36.

1p 1002 11 p21502 10,

p .4

ble production (i.e., option to exchange one asset

for another).

2. a. Increase value (unless the cash flows from the

Mark II needed to be discounted at a higher rate).

b. Increase value.

c. Reduce value.

3. a. Call (i.e., expansion option); (b) option to ex-

change one asset for another; (c) call on oil

price; (d) timing option (Forest has an in-the-

money call); (e) call (option to make subse-

quent investment in China); (f) put (i.e., aban-

donment option); (g) timing option (owner has

an in-the-money call).

4. a. You can’t use any single discount rate for option

payoffs. The risk of an option changes as asset

price changes and time passes.

b. The risky asset may be worth less as a result, but

option owner can capitalize from up moves

while not losing from down moves.

c. Option value depends on value of underlying

asset. DCF is needed to get this value.

5. a. You learn more about land prices and best use of

the land.

b. By developing immediately, you capture rents

immediately.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

Back Matter Appendix B Answers to

Quizzes

© The McGraw−Hill

Companies, 2003

Chapter 23

1. a. (i) 0; (ii) 0; (iii) 0; (iv) $10; (v) $20.

b.

3. a The Norwegian bond has the highest yield (5.6%)

and the Finnish bond has the lowest (4.5%).

b. The Finnish bond has the longest duration (7.9

years) and the Norwegian has the shortest

(7.1 years).

4. a.

b.

c. Less (it is between the 1-year and 2-year spot

rates).

d. Yield to maturity; spot rate.

5. a. Fall (e.g., 1-year 10% bond is worth 110/1.1

100 if r 10% and is worth 110/1.15 95.65 if

r 15%).

b. Less (e.g., see 5(a)).

c. Less (e.g., with r 5%, 1-year 10% bond is worth

110/1.05 104.76).

d. Higher (e.g., if r 10%, 1-year 10% bond is

worth 110/1.1 100, while 1-year 8% bond is

worth 108/1.1 98.18).

e. No, low-coupon bonds have longer durations

(unless there is only one period to maturity) and

are therefore more volatile (e.g., if r falls from 10%

to 5%, the value of a 2-year 10% bond rises from

100 to 109.3 (a rise of 9.3%). The value of a 2-year

5% bond rises from 91.3 to 100 (a rise of 9.5%).

6. a. (100/90.826)

(1/2)

1 .0493, or 4.93%;

(100/73.565)

(1/7)

1 .0448, or 4.48%;

(100/70.201)

(1/8)

1 .0452, or 4.52%;

(100/67.787)

(1/9)

1 .0441, or 4.41%;

(100/29.334)

(1/30)

1 .0417, or 4.17%.

b. Downward.

c. Higher (the yield is a complicated average of the

different spot rates).

d. 73.565/70.201 1 .0479, or 4.79%; 70.201/

67.787 1 .0356, or 3.56%.

7. a. Price today is 108.425; price after 1 year is

106.930.

b. Return (106.930 8)/108.425 1 .06, or 6%.

c. If a bond’s yield to maturity is unchanged, the

return to the bondholder is equal to the yield.

8. a. False. Duration depends on the coupon as well

as the maturity.

b. False. Given the yield to maturity, volatility is

proportional to duration.

c. True. A lower coupon rate means longer dura-

tion and therefore higher volatility.

d. False. A higher interest rate reduces the relative

present value of (distant) principal repayments.

PV

50

1 y

1,050

11 y2

2

PV

50

1 r

1

1,050

11 r

2

2

2

6.9375

1.0402

6.9375

1.0402

2

…

106.9375

1.0402

20

139.57

APPENDIX B Answers to Quizzes 1031

Theoretical value

of warrant

(colored line)

Exercise price ($40) Stock price

c. Buy the warrant and exercise, then sell the stock.

.

2. (a) No; (b) no; (c) ; (d) no, worse

off; (e) zero; (f) more; (g) (i) less, (ii) less, (iii) more,

(iv) more, (v) more; (h) when the dividends on the

stock outweigh the interest on the exercise price;

(i) more.

3. (a) $15,000; (b) $29,000.

4. (a) 1,000/47 21.28; (b) 1,000/50 $20.00; (c) 21.28

41.50 $883.12, or 88.31%; (d) 650/21.28 $30.55;

(e) no (not if the investor is free to convert immedi-

ately); (f) $12.22, i.e., (910 650)/21.28; (g) (47/41.50)

1 .13, or 13%; (h) when the price reaches 102.75%

of par.

5. (a) $7.00; (b) $7.05.

6. (a) False; (b) true; (c) false; (d) false; (e) true; (f) true.

Chapter 24

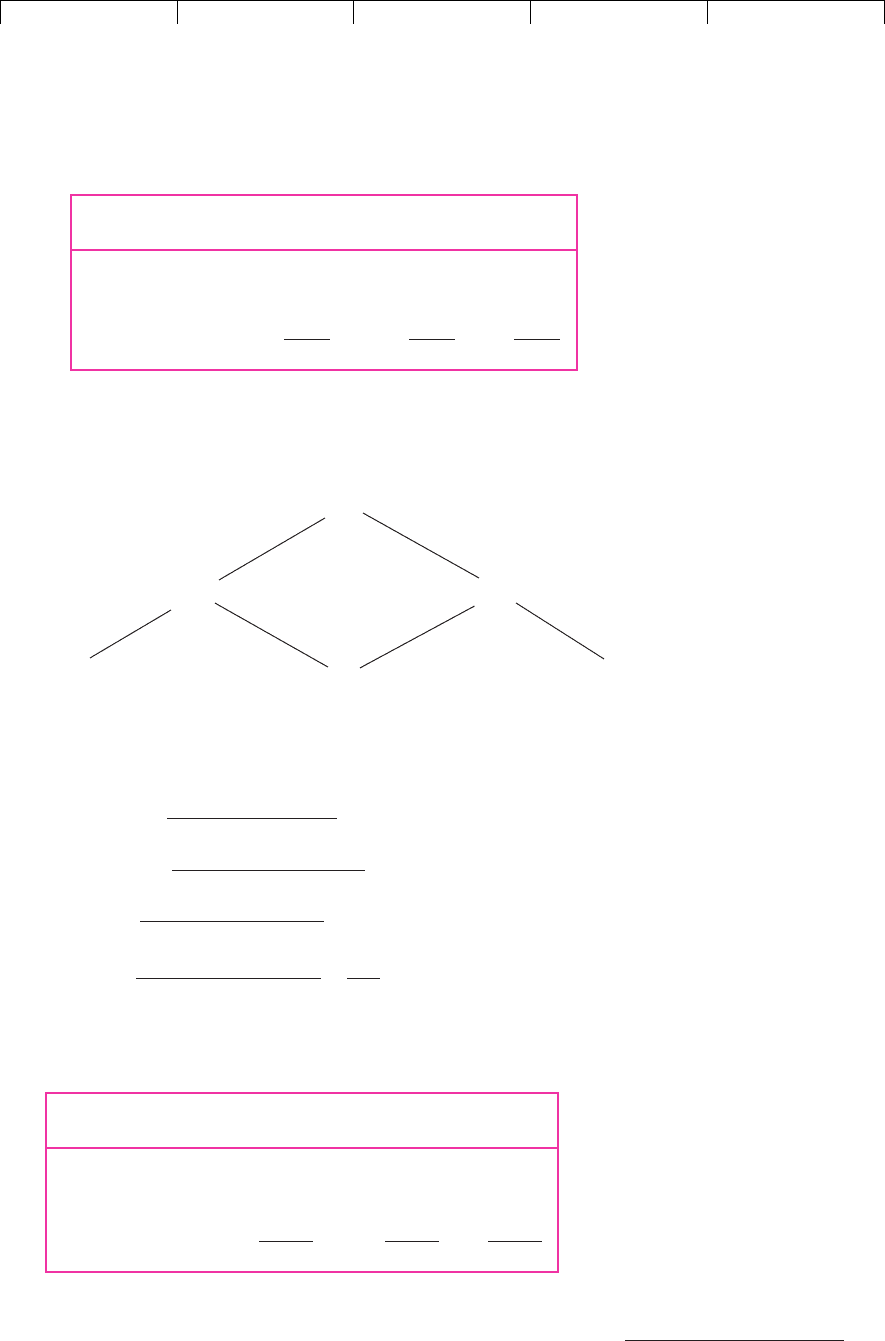

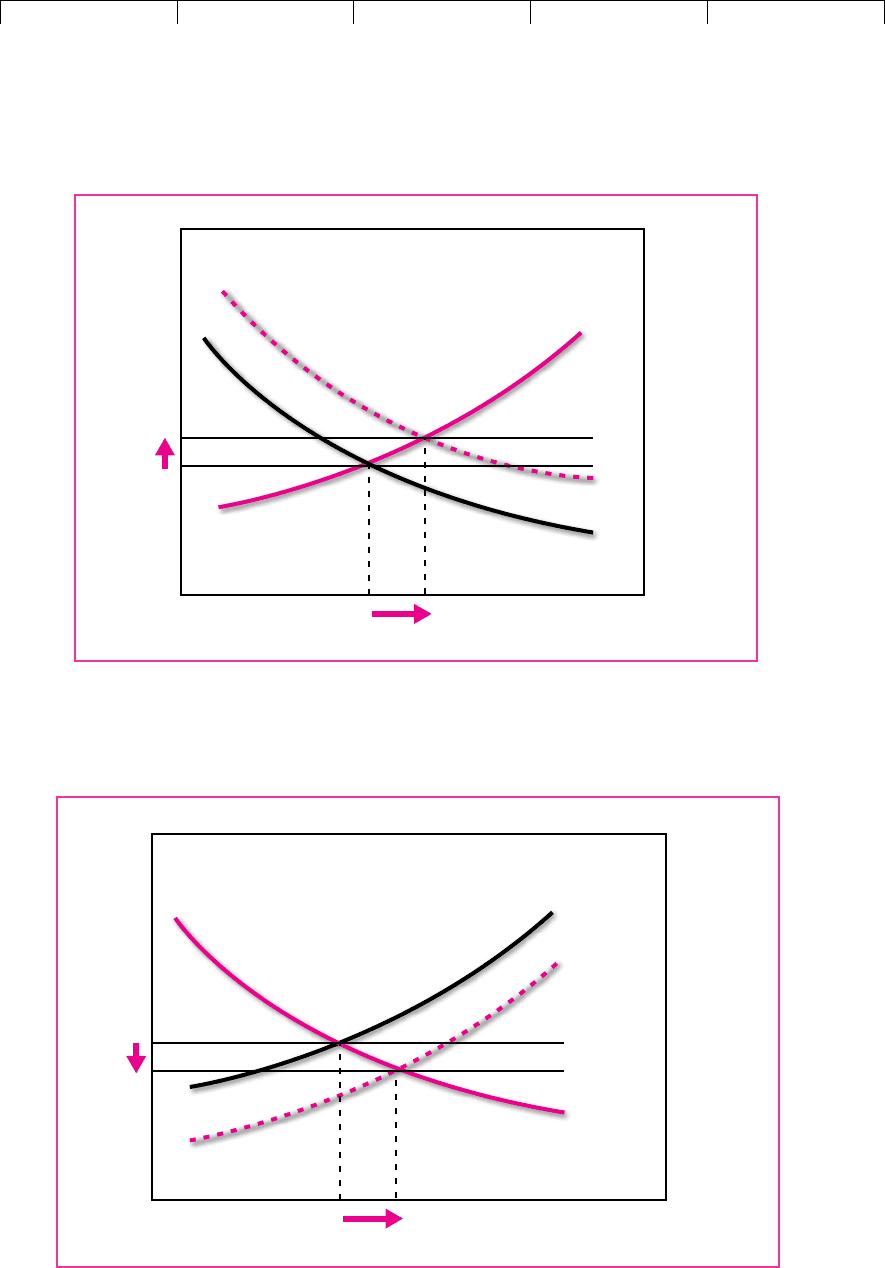

1a.Figure 5 shows that an increase in the demand

for capital increases investment and savings.

The rate of interest also rises.

b. Figure 6 shows that an increase in the supply of

capital also increases investment and savings.

The rate of interest falls.

2. There are 20 coupon payments of 6.9375 plus a

principal payment of 100. With a discount rate of

8.04/2 4.02%, PV is

1/3 70 $

ˇ 23.33

Net gain 5 40 60 $

ˇ 15

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

Back Matter Appendix B Answers to

Quizzes

© The McGraw−Hill

Companies, 2003

1032 APPENDIX B Answers to Quizzes

Investment

by all firms

New level of investment

Percent

New

interest

rate

r

New demand

for capital

Supply

of capital

Old

demand

for capital

FIGURE 5

Chapter 24, Quiz question 1(a).

Investment

by all firms

New level of investment

Percent

New

interest

rate

r

Old supply

of capital

New supply

of capital

Demand

for capital

FIGURE 6

Chapter 24, Quiz question 1(b).