ACCA Paper P2 (INT) Corporate Reporting Pocket notes - Kaplan 2010

Подождите немного. Документ загружается.

Financial instruments Chapter 12

kaplanpublishing 123

Impairment of financial assets

• Ateachreportingdate,an

assessment should be made as to

whether there has been any impairment

of financial assets.

• Notethatforassetsheldatfairvalue,

this will have been dealt with on the

re-measurement to fair value.

• Impairmentlossesarerecognisedinthe

income statement.

Derivatives

A derivative is a financial instrument with all

three of the following characteristics:

1 its value changes in response to the

change in a specified interest rate,

security price, commodity price, foreign

exchange rate or similar variable

2 it requires little or no initial investment

3 it is settled at a future date.

Derivatives include:

• options

• forwardcontracts

• futures

• swaps.

As seen previously, derivatives are measured

at fair value with changes recognised in the

income statement. However, if a derivative is

used as a hedge, then changes in value are

recognised in equity.

Hedge accounting

Hedge accounting is the accounting

treatment where the gains or losses on the

hedging instruments are recognised in

the same performance statement and in the

Definition

Definition

Financial instruments

124 kaplanpublishing

Chapter 12Financial instruments

same period as the offsetting gains or losses

on the hedged items.

A hedging relationship exists when a

company can define three elements.

1 A hedged item – the asset/liability

or transaction on which risks need to be

reduced;

2 A hedging instrument – the instrument

(usually a derivative) used to offset the

risks on the hedged item; and

3 The hedged risks – the specific risk

(currency, interest rate etc) that is being

hedged.

In order to follow the hedge accounting rules

in IAS 39, the following criteria need to be

met.

1 The hedge must be documented at

inception and the elements of the

hedging relationship defined (hedged

item and instrument).

2 The hedge is expected to be highly

effective.

3 The effectiveness of the hedge can be

measured reliably.

4 Forecast transactions must be highly

probable in order to be hedged’.

5 The effectiveness of the hedge must be

able to be assessed and measured on

an on-going basis.

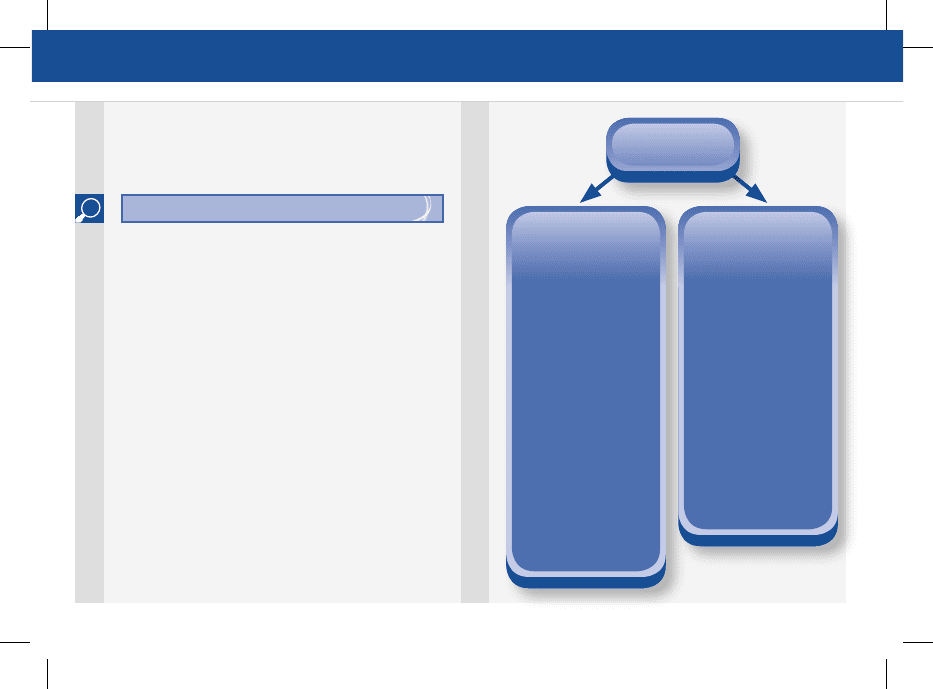

Types of hedge

Therearethreetypesofhedge.Onlytwoare

examinable.

• Fair value hedge

• Cash flow hedge

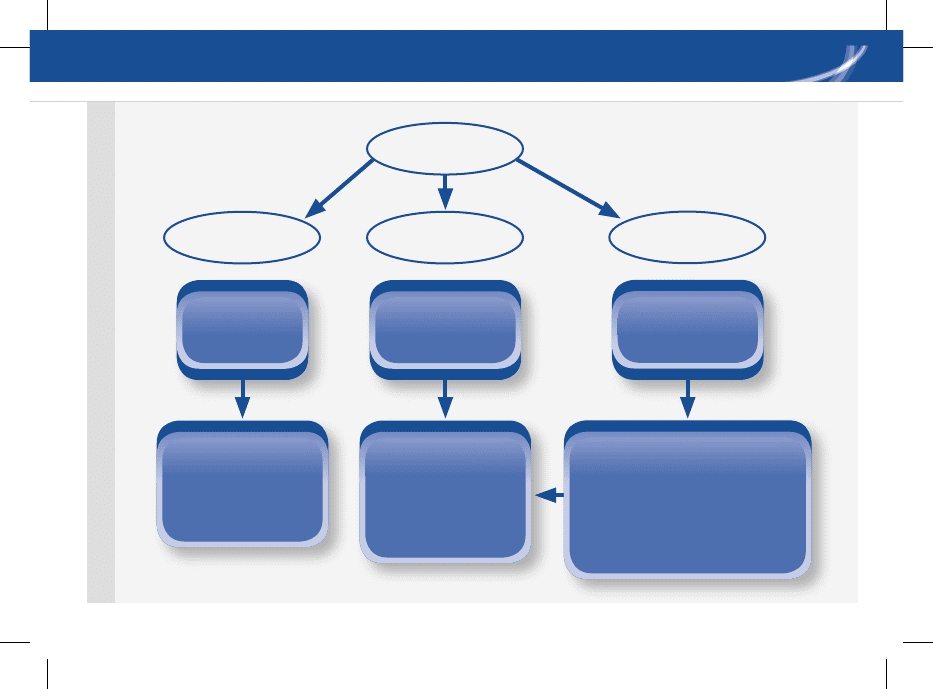

Financial instruments Chapter 12

kaplanpublishing 125

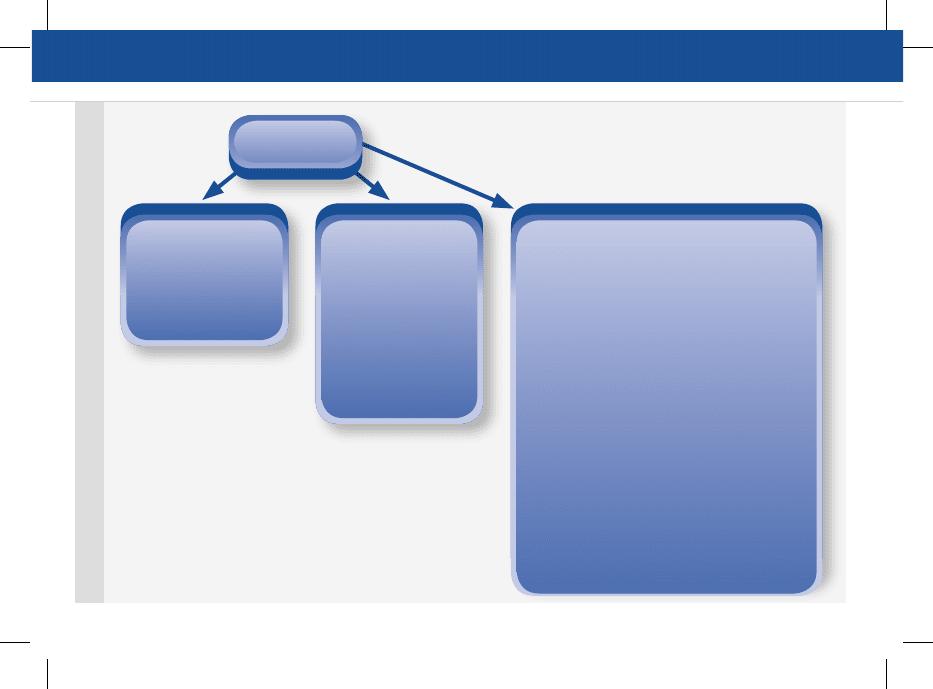

Financial instruments

Hedge of a

recognised asset

or liability

Recognise the hedging

instrument and hedged

item at fair value with

gains and losses to

income statement.

Fair value

Hedge of a net

investment in a

foreign operation

Parent invests in foreign subsidiary-

hedges by taking out a foreign

currency loan to hedge against

changes in value of the investment

due to change in FX rates.

Treat the same way as a

cash flow hedge

Net investment

Hedge against

changes in an

expected cash flow

Remeasure hedging

instrument at fair value

with gain to equity

on effective portion,

ineffective portion to

income statement.

Hedges

Cash flow

Financial instruments

126 kaplanpublishing

Financial instruments Chapter 12

Current Issues

There is an on-going response to the

impact of the global financial crisis. Key

developments include:

Amendments to IFRS 7

This is part of the response by financial

reporting regulators to the global financial

crisis. In March 2009, amendments to IFRS

7 introduced enhanced disclosures regarding

fair value measurement and liquidity risk

arising from financial instruments.

IFRS 9 Financial instruments

This was issued in November 2009 and is

effective from 1 January 2013. Initially, it

deals only with financial assets, although it

will be amended to include financial labilities,

derecognition of financial instruments,

impairment and hedge accounting. As IFRS

9 is updated, the relevant provisions of

existing standards will be withdrawn.

The new standard places increased

emphasis upon fair value measurement and

abolished the available-for-sale category of

financial asset. These factors may result in

increased volatility of reported earnings.

Derecognition

The objective of this ED is to simplify and

standardise derecognition requirements.

There is equivalent work being undertaken

by US FASB to drive towards convergence

on this issue.

Financial instruments

Financial instruments Chapter 12

kaplanpublishing 127

Exam focus

Financial instruments can appear in both

sections A and B of the examination. You

should understand the definitions of each

class of financial asset and liability, together

with their accounting treatment.

Within EN-gage Complete Text Chapter 16,

attempt TYU 4 Bell.

Within EN-gage Complete Text Chapter 16,

attempt TYU 7 Hoggard.

Recent exam questions in this area include:

December 2005 – Ambush•

June 2008 - Sirus•

June 2009 - Aron.•

Financial instruments

128 kaplanpublishing

129

Provisions and events after

the reporting period

In this chapter

IAS 37 Provisions, contingent liabilities and •

contingent assets.

IAS 10 Events after the reporting period.•

chapter

13

Provisions and events after the reporting period

130 kaplanpublishing

Provisions and events after the reporting period Chapter 13

IAS 37 provisions, contingent

liabilities and contingent

assets

• Aprovision is a liability of uncertain

timing or amount.

• Acontingent liability is a possible

obligation arising from past events

whose existence will only be confirmed

on the occurrence of uncertain future

events outside of the entity’s control.

• Acontingent asset is a possible asset

that arises from past events and whose

existence will only be confirmed on the

occurrence of uncertain future events

outside of the entity’s control.

Definition

Recognition

Recognisewhen:

• anentityhasa

presentobligation

(legalor

constructive)asa

resultofapast

event,

• itisprobable

thatanoutflowof

resources

embodying

economicbenefits

willberequiredto

settlethe

obligation,and

• areliable estimate

canbemadeof

theamountofthe

obligation.

Measurement

• Theamount

recognisedasa

provisionshould

bethebest

estimateofthe

expenditure

requiredtosettle

thepresent

obligationatthe

reportingdate.

• Wherethetime

valueofmoneyis

material,the

provisionshould

bediscountedto

presentvalue.

Provisions

Provisions and events after the reporting period

Provisions and events after the reporting period Chapter 13

kaplanpublishing 131

• Inanexamquestionscenario,ask

yourself if the expenditure can be

avoided.

• Ifitcan,thereisnoobligationandthe

provision should not be recognised.

Capitalised provisions – where there is a

future obligation, for example to dismantle an

installation or restore land and buildings back

to their original condition, the present value

of the obligation is capitalised as part of the

cost of the asset as follows:

Dr Non-current assets•

Cr Provisions•

The amount capitalised is depreciated over

the expected useful life of the asset. There

is also an annual finance cost associated

with unwinding the present value of the

future obligation.

Exam focus

Contingent liabilities should not be

recognised. They should be disclosed unless

the possibility of a transfer of economic

benefits is remote.

Contingent assets should not be

recognised. If the possibility of an inflow of

economic benefits is probable they should be

disclosed.

Provisions and events after the reporting period

132 kaplanpublishing

Chapter 13Provisions and events after the reporting period

Future operating losses

• provisionsshould

notberecognised

forfuture

operatinglosses.

Onerous contracts

• provisionsshould

berecognisedfor

thepresent

obligationunder

thecontract.

• E.g.non-cancellable

lease,providefor

theunavoidable

leasepayments.

Restructuring

• provisionscanonlyberecognisedwhere

anentityhasaconstructiveobligationto

carryouttherestructuring.

• aconstructiveobligationarises:

whenthereisadetailedformalplan,

identifyingatleast:

– thebusinessconcerned,

– theprincipallocationsaffected,

– thelocation,function,and

approximatenumberofemployees

beingmaderedundant,

– theexpendituresthatwillbeincurred,

– whentheplanwillbeimplemented;

and

thereisavalidexpectationthattheplan

willbecarriedoutbyeitherimplementing

theplanorannouncingittothoseaffected.

Specific guidance