ACCA - P5 Study text - Emile Woolf INT - 2010

Подождите немного. Документ загружается.

Chapter 18: Developments in management accounting and performance management

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 425

the sales volumes that it will be able to achieve for the product over its expected

life.

There may also be estimates of the capital investment required, and any incremental

fixed costs (such as marketing costs or costs of additional salaried staff).

Taking estimates of sales volumes, capital investment requirements and incremental

fixed costs over the life cycle of the product, it should be possible to calculate a

target cost. The target cost for the product is the maximum variable cost for the

product, that will provide at least the minimum required return on investment.

There will be a gap between the cost at which the product can be made now and the

target cost. The aim should be to close the gap, and reduce the cost of making the

product to the target cost level. The most effective way of closing the gap is to re-

design the product, so that it can be produced at less cost.

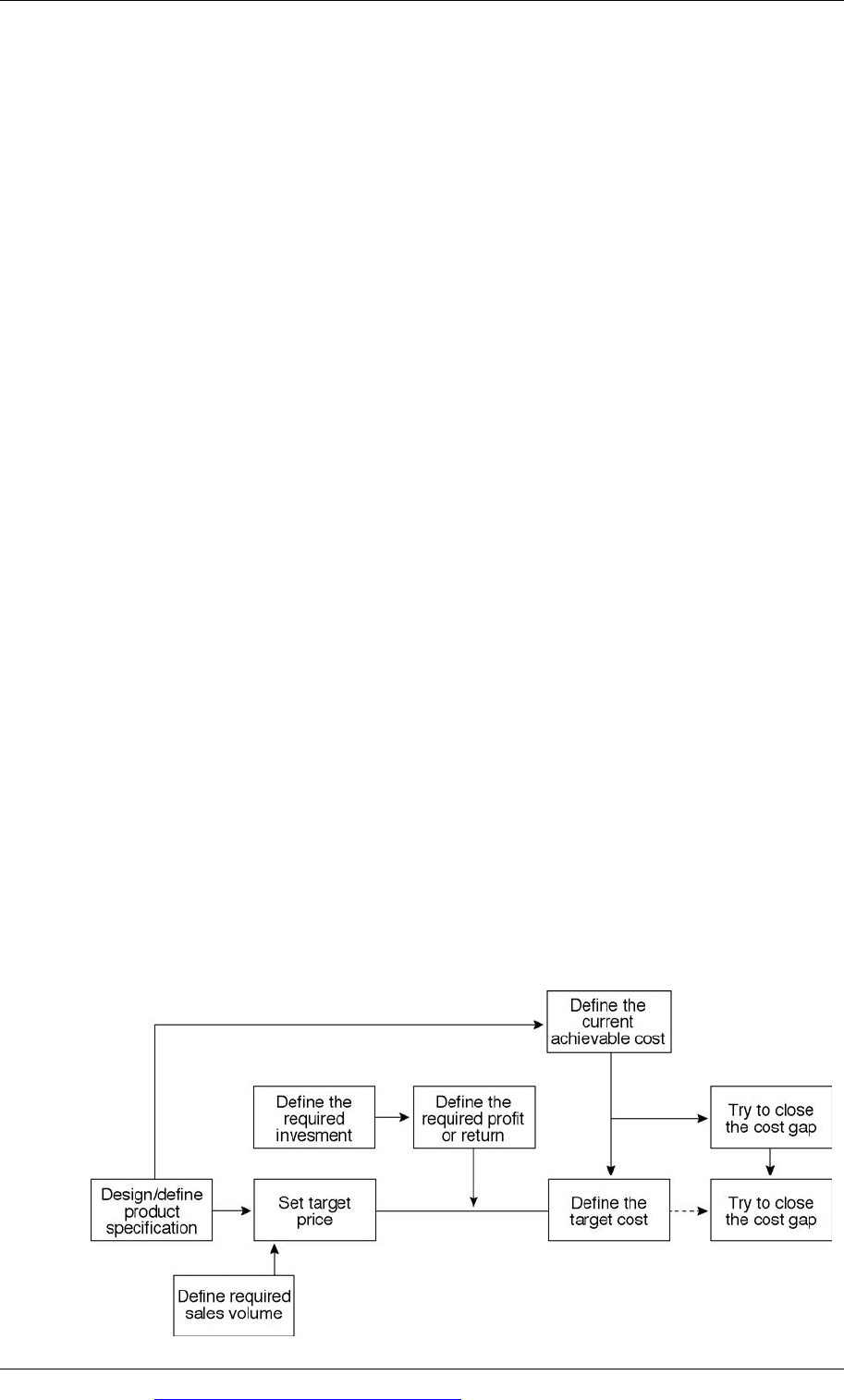

The steps in a target costing exercise are therefore as follows:

Decide the type of product required

Decide what the required sales volume should be (and market share)

Decide what price the product must have in order to achieve the target sales

volume

Estimate the amount of investment required to develop and market the product

Estimate the required profit, measured as a return on the investment (ROI, NPV

or IRR measurements are possible)

Measure the target cost for the product: the target cost per unit of product is

estimated total revenue minus target profit, divided by the expected sales

volume in unit.

The target cost should be compared with the estimated cost of making the product

to the current specification. The current cost of the product is likely to be much

higher than the target cost, and the challenge is therefore to reduce costs from the

current estimated level to the target cost level. Usually, this will require a re-design

of the product, to new (and cheaper) specifications.

The elements in the target costing process are shown in the diagram below.

Target costing

Paper P5: Advanced performance management

426 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Example

A company has designed a new product. It currently estimates that to make the

product, an investment of $1,000,000 in machinery would be required. The residual

value of this investment would be $300,000 at the end of year 4, when the product is

expected to reach the end of its marketable life.

After studying potential demand in the market, the company has set a target selling

price of $20. It has been estimated that at this price, the annual sales volume in units

would be:

Year Sales volume

units

1 20,000

2 30,000

3 40,000

4 10,000

The current estimate of costs is that it would cost $14 to make each unit of the

product, but that there would be no incremental fixed costs. The company has a cost

of capital of 10% for this type of project.

This data can be used to calculate a target cost for the new product, and to identify

the current size of the cost gap.

In the table below, the variable cost per unit of product is shown as V.

Year

Capital cost/

residual value

Revenue

Variable

costs

Discount

factor at

10%

PV of

variable

costs

PV of other

cash flows

$ $ $ $ $

0 (1,000,000)

1.000

(1,000,000)

1 400,000

20,000V

0.909

18,180V 363,600

2 600,000

30,000V

0.826

24,780V 495,600

3 800,000

40,000V

0.751

30,040V 600,800

4 300,000 200,000

10,000V

0.683

6,810V 340,500

79,810V 800,500

In order to make a return of at least 10% on the investment in the project, the

maximum variable cost per unit that can be permitted is $800,500/79,810 = $10.03.

The target cost for the product should therefore be $10.03, say $10 per unit. The

current estimated cost is $14 per unit; therefore the cost gap is $4.

The company needs to identify ways of closing this cost gap.

4.3 Techniques for achieving the target cost

Techniques used by project teams to achieve the target cost include value

engineering (VE) and functional analysis.

Chapter 18: Developments in management accounting and performance management

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 427

Value engineering (VE)

Value engineering is an approach to designing new products in a way that achieves

the target amount of value. The target cost is analysed into:

cost elements for each department (such as direct material costs, direct labour

costs and depreciation costs), and

functional components (for example, in a motor car functional components

include the engine, the transmission system, the braking system, the chassis and

so on).

Value engineering then begins with an investigation into the functions of the

materials and parts purchased, with a view to either reducing costs or improving

the product’s performance and quality. For each material or component, the VE

team might ask questions such as:

What is the function of this material or component?

Is it necessary?

Can it be simplified?

Are all the features of the product or component necessary?

Can a standard part or component be used, instead of the part or component

that is currently in the product specification. Using standard components will

reduce costs, because standard components are purchased in larger quantities at

lower costs.

A VE project makes extensive use of cost tables. These provide a detailed analysis of

the costs of the product, and help the VE project team to identify the major factors

that drive the costs of the product. The team can identify areas of product design

where cost reductions of the required magnitude can be made.

The cost tables can be used to provide information about how the costs of the

product would be affected by:

using different production resources

using different materials, different manufacturing methods

changing the functions of the product, and

changing the product design.

Functional analysis

Functional analysis looks at each function of a product, with the aim of deciding:

whether the functions performed by the product can be modified

whether the product functions can be reduced

whether the product functions can be increased (increasing the functions of a

product may increase the cost of the product, but add to its value to the

customer by even more), or

whether two or more functions can be combined.

Paper P5: Advanced performance management

428 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

To carry out functional analysis, cost tables are needed. These should provide

detailed costs of each product function, so that the implications for cost of altering

the product’s functions can be considered.

4.4 Kaizen costing

For companies that practice TQM and continuous improvement methods, Kaizen

costing takes over where target costing ends.

Target costing is used in the design and development stage for a new product.

Kaizen costing is applied from the time that a product goes into full production

until the end of the product’s life.

Taken together, target costing and Kaizen costing are systems for life cycle costing.

The philosophy of continuous improvement (Kaizen) is based on the view that

markets are highly competitive and industry must try to keep reducing costs in

order to reduce selling prices in order to maintain a competitive advantage. Kaizen

costing is a management accounting system that provides cost information to help

with achieving improvements without loss of product quality or value.

Most of the costs of a product over its entire life cycle are committed during the

design and development stage. This is why target costing is a valuable technique for

the control of costs (without loss of value). However, there is still some scope for

further cost reduction after commercial production and marketing of the product

has begun.

A Kaizen costing system is therefore a costing system that is designed to help a

company to reduce product costs.

A target for cost reductions is set. This target is below the current cost. The cost

reduction must be achieved without any loss of value for the customer. For

example, a target might be set to reduce unit costs of production by 5% within

two years.

Teams are established to identify methods of making improvements.

Kaizen focuses on making small improvements, and it is unlikely that a single

improvement will be sufficient to achieve the target cost reductions. Many

different improvements might be needed, over a period of time.

Actual costs are continually compared with the target costs, and progress

towards achieving the target cost is monitored through regular reporting.

The project teams must continually review production conditions to find ways

of making more improvements and more cost reductions.

Normally, teams are rewarded with bonuses if they achieve their cost reduction

targets.

When one cost reduction target is met, another cost reduction target takes its

place. With Kaizen, the process of seeking improvements never ends.

Chapter 18: Developments in management accounting and performance management

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 429

Techniques for continuous improvement

Teams that are given the responsibility for making improvements might use value

analysis (VA) methods. VA is similar to value engineering, except that VA is

applied to existing products and VE to products during their design and

development stage.

The types of questions that might be asked are as follows:

Can common materials and parts be used? The same part might be used in two

or more parts of the product, or the same part might be used for several different

products that the company manufactures.

How much of the cost consists of purchased materials and components? Can

major suppliers be persuaded to reduce their own costs and prices?

Can improvements be made in logistics (distribution) or packaging?

Can the investment in the product (for example, working capital) be reduced?

Can improvements be made in production systems or maintenance methods?

Can the work be organised in a different way?

A system of value analysis must be supported by a management accounting system

that provides relevant cost data.

Kaizen costing compared with standard costing

It is useful to compare Kaizen costing with traditional standard costing.

With standard costing, expected costs are established based on current

production methods. Variances between actual and standard costs are

calculated, and variance reports focus on significant variations between actual

costs and the current standard. There is no motivation to make improvements

and reduce costs below the existing standard.

With Kaizen costing, actual costs are compared with the target, not an existing

standard. The variance reporting system is used to monitor progress towards the

target cost.

With standard costing, managers are encouraged to prevent adverse variances.

For example, if there is an adverse material price variance, the manager

responsible might decide to buy materials at a lower price from a different

supplier. The result could be a loss of quality, a fall in value and a reduction in

customer satisfaction. With Kaizen costing, reductions in cost must be achieved

without any loss of value.

Target costing and Kaizen costing are examples of management techniques that call

for a different management accounting system. In particular, project teams need

cost tables to assist them with identifying ways in which cost reductions might be

achieved and they need information to monitor progress towards targets.

A 1993 article on Kaizen and Kaizen costing concluded: ‘In the US, changes in the

focus and methods of production need to be accompanied by changes in

management accounting systems. The Japanese have provided guidance on how

management accounting can play a significant role in creating sustainable

competitive advantage for a firm. The more organisations rid themselves of

Paper P5: Advanced performance management

430 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

traditional management accounting practices, the better is the chance that the new

ideas about manufacturing can take over and really show their worth. Old ways of

product costing blunt a firm’s ability to compete effectively and hinder their ability

to focus on world-class performance.’

(‘New product costing, Japanese style’: Margaret Lgagne and Richard Discenza.

CPA Journal May 1993).

Chapter 18: Developments in management accounting and performance management

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 431

Environmental management accounting

The purpose of environmental management accounting

A framework for environmental management accounting

EMA techniques

5 Environmental management accounting

5.1 The purpose of environmental management accounting

For some companies, environmental issues are significant, in terms of both strategy

and cost.

Poor environmental behaviour can result in significant costs or losses, such as

fines for excessive pollution, environmental taxes, loss of land values, the cost of

law suits, and so on.

Environmental behaviour can affect the perception of customers, and their

attitudes to a company and its products. Increasingly, consumers take

environmental factors into consideration when they make their buying

decisions.

Environmental management accounting can be used to provide information to

management to help with the management of environmental issues. Traditional

management accounting techniques:

Under-estimate or even ignore the cost of poor environmental behaviour

over-estimate the costs of improving environmental practices, and

under-estimate the benefits of improving environmental practices.

Environmental management accounting (EMA) provides managers with financial

and non-financial information to support their environmental management

decision-making. EMA complements other ‘conventional’ management accounting

methods, and does not replace them.

The main applications of EMA are for:

estimating annual environmental costs (for example, costs of waste control)

budgeting

product pricing

investment appraisal (for example, estimating clean-up costs at the end of a

project life and assessing the environmental costs of a project)

estimating savings from environmental projects.

Paper P5: Advanced performance management

432 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

5.2 A framework for environmental management accounting

Burritt et al (2001) suggested a framework for EMA based on providing information

to management:

from internal or external sources

as monetary or physical measurements

as historical or forward-looking information

where the focus is short-term or longer-term

that consists of routine reports or ad hoc information.

Four of these elements of EMA are shown in the following table:

Environmental management accounting (EMA)

Monetary EMA Physical EMA

Short-term focus Long-term focus Short-term focus Long-term focus

Historical

orientation

Routine

reporting

Environmental cost

accounting

Analysis of

environmentally-

induced capital

expenditures

Material and

energy flow

accounting

Accounting for

environmental

capital impacts

Ad hoc (one-

off)

information

Historical

assessment of

environmental

decisions

Environmental

life cycle costing,

environmental

target costing

Historical

assessment of

short-term

environmental

impacts, e.g. of a

site or product

Post-investment

assessment of

environmental

impacts of capital

expenditures

Future

orientation

Routine

reporting

Environmental

operational budgets

and capital budgets

(monetary

reporting)

Environmental

long-term

financial

planning

Environmental

long-term physical

planning

Ad hoc (one-

off)

information

Relevant

environmental

costing (e.g. special

orders)

Environmental

life cycle

budgeting and

target costing

Assessment of

environmental

impacts

Physical

environmental

investment

appraisal. Specific

project life cycle

analysis

Chapter 18: Developments in management accounting and performance management

©

EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides

433

Paper P5: Advanced performance management

434 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

5.3 EMA techniques

Environmental management accounting techniques include:

re-defining costs

input-output analysis

environmental activity based accounting

environmental life cycle costing

Re-defining costs

The US Environmental Protection Agency (1998) suggested terminology for

environmental costing that distinguishes between:

conventional costs: these are environmental costs of materials and energy that

have environmental relevance and that can be ‘captured’ in costing systems

potentially hidden costs: these are environmental costs that might get lost within

the general heading of ‘overheads’

contingent costs: these are costs that might be incurred at a future date, such as

clean-up costs

image and relationship costs: these are costs associated with promoting an

environmental image, such as the cost of producing environmental reports.

There are also costs of behaving in an environmentally irresponsible way, such

as the costs of lost sales as a result of causing a major environmental disaster.

In traditional management accounting systems, environmental costs (and benefits)

are often hidden. EMA attempts to identify these costs and bring them to the

attention of management.

Input-output analysis

Input-output analysis is a method of analysing what goes into a process and what

comes out. It is based on the concept that what goes into a process must come out or

be stored. Any difference is residual, which is regarded as waste.

Inputs and outputs are measured initially in physical quantities, including

quantities of energy and water. They are then given a monetary value.

Inputs

100%

Output product 60%

Scrap sold for re-cycling 20%

Disposed of as waste 15%

Unaccounted for 5%

Environmental activity based accounting

Environmental activity based accounting is the application of environmental costs

to activity based accounting. A distinction is made between: