ACCA P2 (INT) Corporate Reporting - Study text - 2010 (Emile Woolf)

Подождите немного. Документ загружается.

Chapter 5: Group financial statements: complex groups

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 143

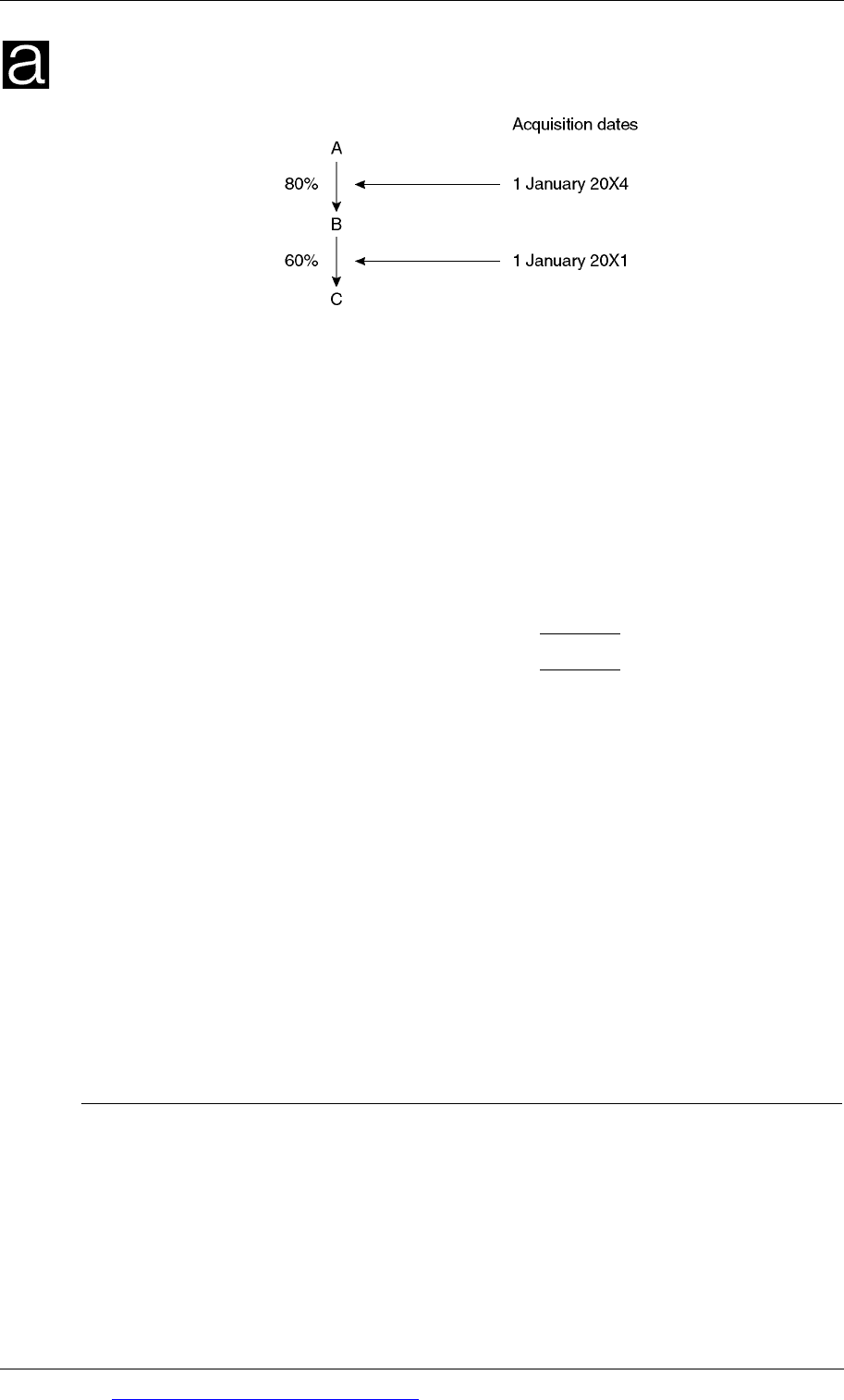

Vertical group

Ownership of T

Direct holding of H 0%

Indirect holding of H (75% × 60%) 45%

H share of ownership of T 45%

Non-controlling interest in T (the balance) 55%

100%

In our vertical group, H has two subsidiaries S and T. This consists of a direct

interest of 75% in the shares of S and an indirect interest of 45% in the shares of T,

through its ownership of S. This gives a non-controlling interest of 25% in S and 55%

in T.

The non-controlling interest in T consists of two elements:

40% of the shares of T are held by shareholders other than S

The 25% non-controlling interest in S owns a share of the 60% of T that is owned

by S. This is an indirect non-controlling interest in T – the part of T that is owned

by the non-controlling interest in S.

Vertical group

Non-controlling interest in T

Direct non-controlling interest in T 40%

Indirect non-controlling interest in T (25% × 60%) 15%

Total non-controlling interest, one-stage method 55%

Mixed group: indirect non-controlling interest

A similar analysis can be applied to a mixed group. It has already been shown that

using the one-stage method, the percentage ownership of T in the mixed group is as

follows:

Mixed group

Ownership of T

Direct holding of H 40%

Indirect holding of H (60% × 20%) 12%

H share of ownership of T 52%

Non-controlling interest in T (the balance) 48%

100%

In our mixed group, H has two subsidiaries, S and T.

It has a 60% interest in S

It has a 52% interest in T. This comprises a direct interest of 40% plus an indirect

interest through S of 12% (60% × 20%).

As already seen, this gives non-controlling interests of 40% in S and 48% in T. The

non-controlling interest in T consists of two elements:

40% of the shares of T are held by shareholders other than S

Paper P2: Corporate Reporting (International)

144 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The 40% non-controlling interest in S owns a share of the 20% of T that is owned

by S. This is an indirect non-controlling interest in T – the part of T that is owned

by the non-controlling interest in S.

Mixed group

Non-controlling interest in T

Direct non-controlling interest in T 40%

Indirect non-controlling interest in T (40% × 20%) 8%

Total non-controlling interest, one-stage method 48%

4.2 Calculating the non-controlling interest for the consolidated statement

of financial position

We need to establish a value for non-controlling interest in the consolidated

statement of financial position.

For a direct subsidiary S, this is not a problem. The non-controlling interest in S

is the percentage of shares held directly by the non-controlling interest in S,

multiplied by the net assets of S.

For a sub-subsidiary, or any other subsidiary with an indirect non-controlling

interest (T), there is a problem. We can calculate a non-controlling interest in T as

the percentage non-controlling interest multiplied by the net assets of T.

However, this would involve some double-counting, of the non-controlling

interest in S and the indirect non-controlling interest in T

(This double-counting problem arises only with the one-stage method of

consolidation.)

To calculate the total non-controlling interest in the group, we have to remove the

double counting. The following approach is recommended:

Non-controlling interest in the H group

Non-controlling interest (NCI) in S (% NCI in S) × (Net assets of S) X

Non-controlling interest (NCI) in T (% NCI in T) × (Net assets of T) Y

Direct and indirect non-controlling interest in S and T (X + Y)

Subtract double counting:

Cost of indirect non-controlling interest

in T

(% NCI in S) × (Cost of

investment by S in T)

(Z)

Non-controlling interest in H Group (X + Y - Z)

4.3 Cost of the parent entity’s investment in T

Having calculated the non-controlling interest in T, we can calculate the parent’s

share of the cost of the investment in T.

The cost of the indirect non-controlling interest in T must be subtracted from the

total cost of the investment by S in T, to obtain the cost of the group’s investment in

T.

Chapter 5: Group financial statements: complex groups

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 145

Cost of investment of S in T A

Cost of indirect non-controlling interest in T B = (X + Y – Z) above

Cost of parent’s investment in T A – B

The cost of the parent’s investment in T is then used to calculate the purchased

goodwill on the acquisition of T.

Example

On 1 June 20X5, H acquired 75% of the shares of S at a cost of $180,000. On the same

date, S acquired 60% of the share capital of T at a cost of $88,000.

Immediately after the acquisition, the statements of financial position of the three

companies were as follows:

H

S

T

$

$

$

InvestmentinSatcost 180,000

‐

‐

InvestmentinTatcost

‐

88,000

‐

Othernetassetsatfairvalue

420,000

112,000

100,000

600,000

200,000

100,000

Sharecapitalandreserves 600,000

200,000

100,000

Required

(a) Calculate the non-controlling interests in the H Group immediately after the

share acquisitions.

(b) Calculate the cost to H of the investment in T.

The H Group uses the partial goodwill method of consolidation.

Answer

The parent entity’s interest in T is 45% (75% × 60%). The non-controlling interest in

T is 55% (100% – 45%).

The non-controlling interest in the H group

$

Non‐controllinginterestinnetassetsofS

25%×$200,000 50,000

Non‐controllinginterestinnetassetsofT 55%×$100,000 55,000

––––––––––––––––––––

105,000

Subtract

Costofindirectnon‐controllinginterestinT

25%×$88,000 (22,000)

––––––––––––––––––––

Non‐controllinginterestinHGroup

83,000

––––––––––––––––––––

Paper P2: Corporate Reporting (International)

146 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

An alternative way of calculating the non-controlling interest would be as follows:

$

NetassetsofS,excludinginvestmentinT(200,000–88,000)

112,000

$

NCIshareoftheseassetsinS:25%×$112,000

28,000

NCIshareofnetassetsofT:55%×$100,000

55,000

Non‐controllinginterestinHGroup

83,000

Cost of parent’s investment in T

$

CostofinvestmentofSinT

88,000

Costofindirectnon‐controllinginterestinT(seeabove) (22,000)

–––––––––––––––––––

Costofparent’sinvestmentinT

66,000

–––––––––––––––––––

4.4 Calculating the purchased goodwill

When the cost of the parent’s investment in the sub-subsidiary has been calculated,

the purchased goodwill on acquisition can be calculated in the normal way, using

the partial goodwill method. It is the difference between the parent’s cost of the

investment and the parent’s share of the net assets acquired, at fair value.

Example

Continuing the previous example of the H Group, and using the partial goodwill

method of consolidation, the goodwill on acquisition is calculated separately for S

and for T, as follows:

S

T

$

$

Costofinvestment

180,000

(seeabove) 66,000

Shareofnetassetsacquired (75%×$200,000) 150,000

(45%×$100,000) 45,000

Goodwill

30,000

21,000

The total purchased goodwill for the H Group at acquisition is therefore $30,000 +

$21,000 = $51,000.

The consolidated statement of financial position of the H Group at the date of the

acquisition of S by H and of T by S can now be constructed as follows.

$

Purchasedgoodwill

51,000

OthernetassetsofHgroupatacquisition(420+112+100) 632,000

683,000

Chapter 5: Group financial statements: complex groups

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 147

SharesandreservesofH 600,000

Post‐acquisitionprofitsofsubsidiaries

0

600,000

Non‐controllinginterests(seeabove) 83,000

683,000

The following example illustrates how a consolidated statement of financial position

should be prepared for a complex group. The steps to take on consolidation are

those described in the previous chapter on consolidated accounts (for the partial

goodwill method), except that calculating the non-controlling interest (which was

Step 4) must now come before calculating the purchased goodwill (which was Step

3).

Example

The summary statements of financial position as at 31 December 20X7 are as

follows:

EntityA

EntityB EntityC

$000

$000

$000

InvestmentinBatcost:2,400shares 5,000

InvestmentinCatcost:180shares

750

Sundrynetassets 9,900

5,000

1,000

14,900

5,750

1,000

Sharecapital:ordinarysharesof$1each 10,000

3,000

300

Accumulatedprofits 4,900

2,750

700

14,900

5,750

1,000

Entity A acquired its investment in Entity B on 1 January 20X7. Entity B acquired its

investment in Entity C on 1 January 20X4. At the dates of the share purchases, the

following information is available:

Date

Accumulatedprofits,

EntityB

Accumulatedprofits,

EntityC

$000 $000

EntityB 1January20X4 2,000 500

EntityB

1January20X7 2,300 650

Required

Prepare the consolidated statement of financial position for the A Group as at 31

December 20X7, using the partial goodwill method of consolidation.

Paper P2: Corporate Reporting (International)

148 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Answer

Group structure

Entity B acquired its interest in Entity C before A purchased its interest in B;

therefore the date of entry into the A Group is the same for both Entity B and Entity

C. This is 1 January 20X7.

Step 1

Calculate the percentage ownership of the subsidiaries held by A and the

percentage ownership of the non-controlling interests.

OwnershipofB

DirectholdingofA 80%

Non‐controllinginterestinB(balancingfigure)

20%

100%

OwnershipofC

DirectholdingofA 0%

IndirectholdingofB(80%×60%)

48%

48%

Non‐controllinginterestinT(balancingfigure)

52%

100%

Step 2

Calculate the net assets of Entity B and Entity C at (1) the end of the current

reporting period and (2) the date of acquisition by the group.

EntityB EntityC

At31

December

20X7

At

acquisition

date

At31

December

20X7

At

acquisition

date

$000

$000

$000 $000

Sharecapital 3,000

3,000

300 300

Accumulatedprofits 2,750

2,300

700 650

–

––––––

–

––––

–

––

–

–

–––––––––––

–

––

–

–––––––––––––––– ––––––––––––

–

––

–

Netassets

(sharecapitalplusreserves)

5,750

––––––––––––––––

5,300

––––––––––––––––

1,000

––––––––––––––––

950

––––––––––––––––

Post‐acquisitionaccumulatedprofits

450=(5,750–5,300) 50=(1,000–950)

Chapter 5: Group financial statements: complex groups

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 149

Step 3

Calculate the non-controlling interest

Use the method described earlier in this chapter.

$

Non‐controllinginterestinnetassetsofB

20%×5,750 1,150

Non‐controllinginterestinnetassetsofC 52%×1,000 520

––––––––––––––––

1,670

Subtract

Costofindirectnon‐controllinginterestinC

20%×750 (150)

(=20%×CostofinvestmentbyBinC)

––––––––––––––––

Non‐controllinginterestinAGroup

1,520

––––––––––––––––

Step 4

Calculate the purchased goodwill

To do this, we must first calculate the cost of the parent company’s investment in

Entity C.

$000

CostofinvestmentofBinC

750

Costofindirectnon‐controllinginterestinC(seeabove) (150)

–––––––––––––

Costofparent’sinvestmentinC

600

–––––––––––––

InvestmentinB

InvestmentinC

$000

$000

Costofinvestment 5,000 (seeabove) 600

Minusshareofnetassetsacquired:

80%×5,300(seeSteps1and2)

(4,240)

48%×950(seeSteps1and2)

(456)

–––––––––––––––

–––––––––––––––

Purchasedgoodwill

760

144

–––––––––––––––

–––––––––––––––

Total purchased goodwill for the group (in $000) = 760 + 144 = 904. (There has been

no impairment of goodwill.)

Step 5

Calculate the post-acquisition accumulated profits of the parent company

Paper P2: Corporate Reporting (International)

150 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

$000

EntityAaccumulatedprofits(parentcompany)

4,900

Parent’sshareof:

EntityBaccumulatedprofits(80%×450)–seeStep2 360

EntityCaccumulatedprofits(48%×50)–seeStep2

24

5,284

We can now prepare the consolidated statement of financial position as at 31

December 20X7.

Consolidatedstatementoffinancialpositionat31December20X7

$000

Goodwill(Step4)

904

Sundrynetassets(9,900+5,000+1,000) 15,900

16,804

Sharecapital 10,000

Reserves(Step5)

5,284

Parentcompany’sshareinequityofthegroup

15,284

Non‐controllinginterest(Step3) 1,520

16,804

4.4 Complex groups: the full goodwill method

The full goodwill method differs from the partial goodwill method in the following

ways:

the calculation of the goodwill at acquisition

the valuation of non-controlling interests, and

the accounting treatment of subsequent impairments in goodwill.

An example will be used to demonstrate the accounting method required, and how

it differs from the partial goodwill method.

Example

The summary statements of financial position as at 31 December Year 8 are as

follows:

EntityA

EntityB EntityC

$000

$000

$000

InvestmentinBatcost:(80%holding) 3,300

InvestmentinCatcost:(60%holding)

2,200

Sundrynetassets 2,700

1,400

3,000

6,000

3,600

3,000

Chapter 5: Group financial statements: complex groups

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 151

Sharecapital:ordinarysharesof$1each 4,000

2,500

2,000

Accumulatedprofits 2,000

1,100

1,000

6,000

3,600

3,000

Entity A acquired its investment in Entity B on 1 January Year 7. Entity B acquired

its investment in Entity C on 31DecemberYear7

The following information is relevant:

Date

Retainedearnings

EntityB

Retainedearnings,

EntityC

$000 $000

1JanuaryYear7 400 200

31DecemberYear7

700 320

Date

FairvalueofNCI,

EntityB

FairvalueofNCI,

EntityC

$000 $000

1JanuaryYear7 800 1,600

31DecemberYear7

960 2,000

The goodwill of Entity B is impaired as at 31 December Year 7 by $500,000.

Required

Prepare the consolidated statement of financial position of the Entity A Group as at

31 December Year 8, using:

(a) the full goodwill method

(b) the partial goodwill method.

Answer

The acquisition of Entity B by Entity A occurred before the acquisition of Entity C

by Entity B. The effective share of the A Group in Entity C is 80% × 60% = 48%.

The relevant retained earnings for the purpose of goodwill calculation are:

Entity B: at 1 January Year 7, $400,000

Entity C: at 31 December Year 7, $320,000.

Full goodwill method

(a) Calculation of goodwill

The fair value of the consideration held in Entity C represents the 60%

shareholding in entity C purchased by Entity B. The 20% shareholding held by

the NCI in Entity B should be deducted in the calculation, as shown below.

Paper P2: Corporate Reporting (International)

152 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The purchased goodwill relating to Entity B and Entity C are calculated as

follows.

Entity B Entity C

$000 $000

Fair value of consideration 3,300 2,200

Indirect holding of C belonging to NCI of B

(20% × 2,200)

(440)

Fair value of NCI at acquisition 800 2,000

4,100 3,760

Fair value of identifiable net assets at acquisition

(Entity B: 2,500 + 400) (Entity C: 2,000 + 320) 2,900 2,320

Purchased goodwill 1,200 1,440

Allowing for the impairment of goodwill in Entity B, the total goodwill at 31

December Year 8 (in $000) = $1,200,000 + $1,440,000 – $500,000 = $2,140,000.

(b) Calculation of NCI

Again, an adjustment is required to the NCI in Entity C to allow for the 20%

share held by the NCI of B in the investment in C.

Entity B Entity C

$000 $000

Fair value of NCI at acquisition 800 2,000

Indirect holding of C belonging to NCI of B

(20% × 2,200)

(440)

Post-acquisition profit attributable to NCI :

Entity B : 20% × (1,000 – 400)

140

Entity C : 52% × (1,000 – 320)

354

Impairment of goodwill: attributable to NCI in B

(20% × 500)

(100)

840 1,914

The total NCI at 31 December Year 8 is (in $000) $2,754.

(c) Calculation of consolidated retained earnings attributable to equity holders

of A

Attributable to parent: $000

Retained earnings of Entity A 2,000

Post-acquisition profit of B: 80% × (1,100 – 400)

560

Post-acquisition profit of C: 48% × (1,000 – 320)

326

Impairment of goodwill attributable to parent: 80% × 500

(400)

Consolidated retained earnings at 31 December Year 8 2,486