ACCA P2 (INT) Corporate Reporting - Study text - 2010 (Emile Woolf)

Подождите немного. Документ загружается.

Chapter 5: Group financial statements: complex groups

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 133

Examples

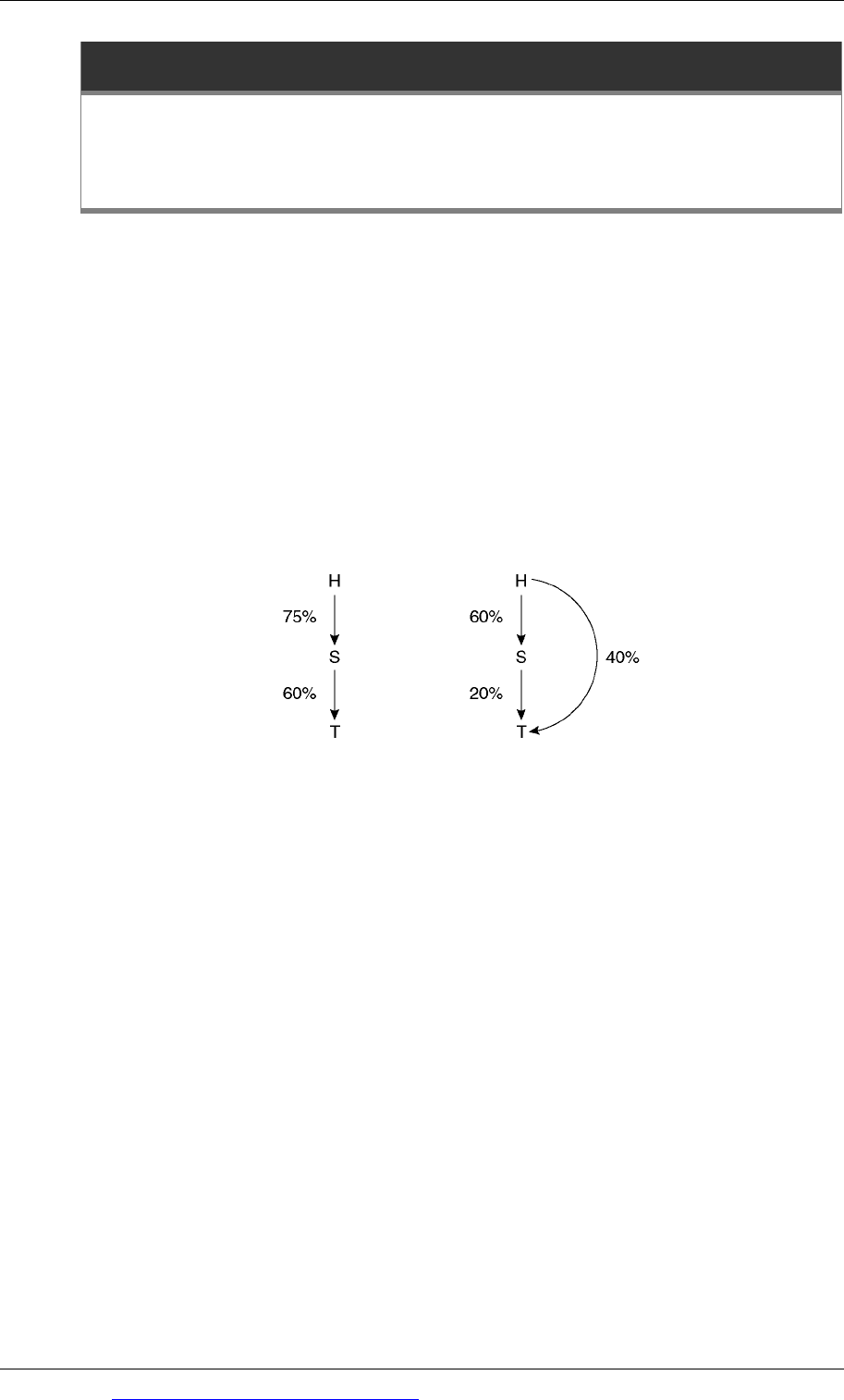

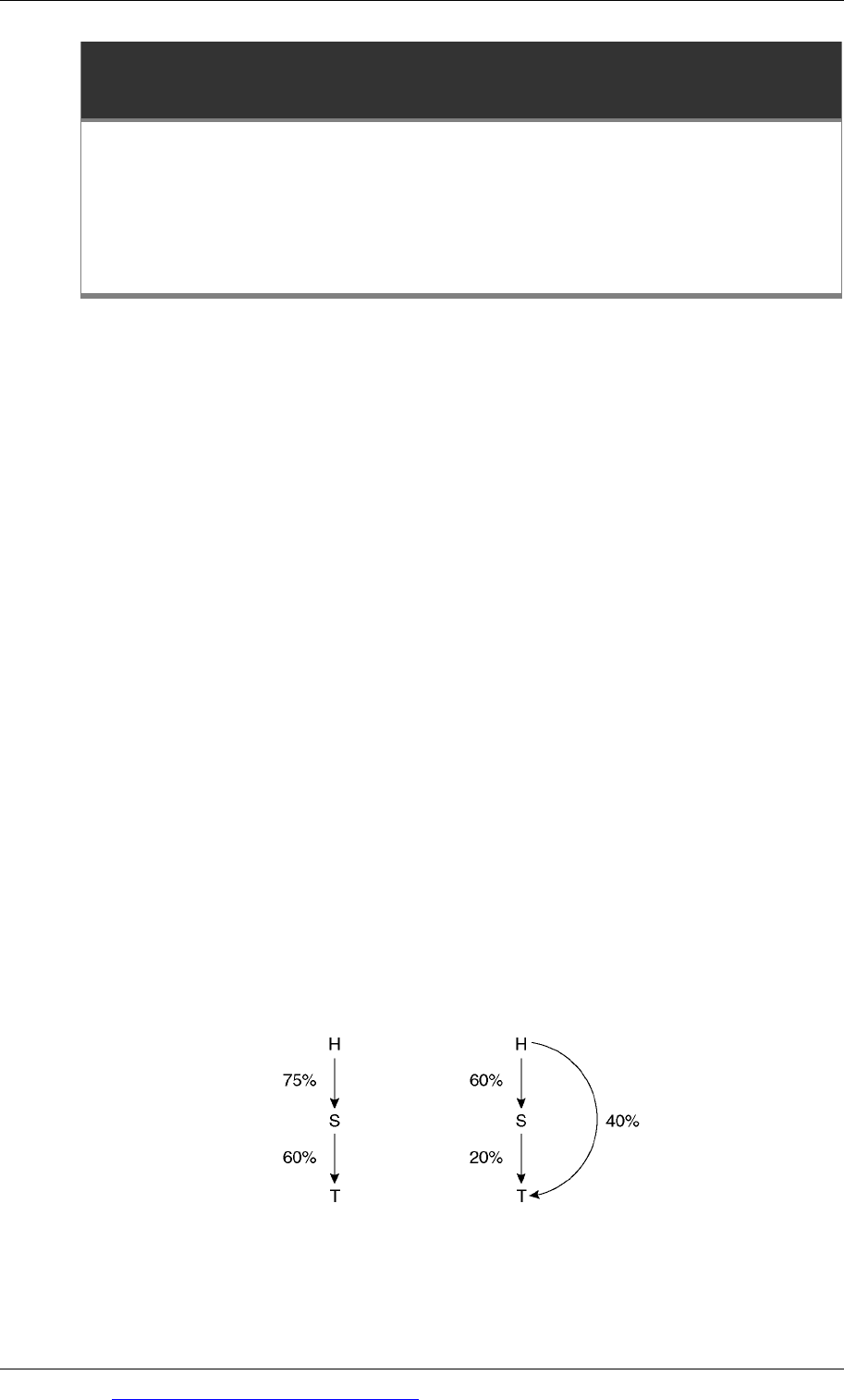

Vertical structure Mixed structure

H

75%

60%

S

T

60%

H

40%

S

20%

In an examination question, there may be more subsidiaries than are shown here.

There may also be associates or joint ventures. However, all the key consolidation

rules can be learned and applied using the structures shown above with just three

companies, H, S and T.

1.2 Checking the status of investments

To deal with complex groups, it is important always to check the status of the

investments and to decide whether an investment is a subsidiary, an associate or a

simple investment. With complex groups, the key test is usually to decide whether

an investment is:

a subsidiary, or

an associate.

The key test of owning a subsidiary in IAS 27 is based on the concept of control.

One important test of control is ownership of more than 50% of the equity share

capital of an entity.

Vertical group example

In the example above of a vertical group above:

H controls S because it owns more than 50% of the shares of S, and

S controls T, because S owns more than 50% of the shares of T.

H therefore controls T through its control of S. T is described as a sub-subsidiary

of H. (A sub-subsidiary is a subsidiary of a subsidiary.)

H is said to have:

a direct interest in S, and

an indirect interest in T.

Paper P2: Corporate Reporting (International)

134 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

H is therefore a holding company with two subsidiaries, S and T. Both S and T will

be included (consolidated) into the group accounts of the H Group.

(Note: You might think that T should not be a subsidiary of H because the effective

interest of H in T is only 75% × 60% = 45%, which is less than 50%. However, this is

an incorrect view. H controls S and S controls T; therefore H controls T through its

control of S.)

Mixed group example

In the example of the mixed group shown above:

H controls S because it owns more than 50% of the shares of S, and

H controls T through its direct ownership of 40% of T and the 20% holding in T

by its subsidiary S. H and S between them own 60% of T, which is sufficient for

control.

Because of this control, T is a subsidiary in the H Group, and both S and T are

subsidiaries of H. Both S and T must therefore be consolidated in the accounts of the

H Group.

1.3 Consolidation in practice and consolidation in the examination

The way in which you should prepare consolidated accounts for a complex group in

the examination should be different from the way that it is done in practice. The

reason for this is to save time in the examination. You should use a short-cut

method that is fully acceptable for examination purposes.

The short-cut method is to prepare the consolidated accounts in a single stage, using

a one-stage method of consolidation. In practice, consolidated accounts for

complex groups are prepared in two (or more) stages.

Consider the example of the vertical group example above, where H owns 75% of S

and S owns 60% of T.

There are two separate groups here:

− T is a subsidiary of S. In practice, this means that S must prepare consolidated

financial statements for the Group S (which consists of S and T). The

consolidated accounts of S should be presented to all the shareholders of S,

including the shareholders other than H.

− T and S are both subsidiaries of H. H is therefore required to prepare

consolidated financial statements for the H Group, including both S and T.

In practice, two sets of consolidated financial statements must therefore be

prepared, one by S for the S Group and one by H for the H Group.

For complex groups, an exam question would require you to prepare consolidated

financial statements for the H group (H, S and T). It would be acceptable to prepare

these financial statements in two stages, first by preparing consolidated accounts for

S and then preparing consolidated accounts for H. However this would take a long

time.

Chapter 5: Group financial statements: complex groups

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 135

It is more efficient and time-saving to prepare the consolidated financial statements

for the total H group in one stage. This one-stage approach method of consolidation

(also called the ‘direct method’) is described below. We strongly recommend that

you should use it in the examination, should you be required to prepare financial

statements for a complex group.

1.4 Problem areas with complex groups

Several aspects of consolidation with complex groups need careful attention. These

are:

calculating the percentage group holdings and the non-controlling interests in

the subsidiaries

deciding the date of acquisition for sub-subsidiaries in vertical groups and

subsidiaries in mixed groups

calculating the amount in the consolidated statement of financial position for the

non-controlling interests, and

calculating the purchased goodwill.

Paper P2: Corporate Reporting (International)

136 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Calculating parent entity holdings and non-controlling interests

The problem

The rules for vertical groups

The rules for mixed groups

2 Calculating parent entity holdings and non-

controlling interests

2.1 The problem

In complex groups, care must be taken when calculating the interest of the parent

entity and the non-controlling interests in the subsidiaries. The same group

structures that were used as examples before will be used again here.

Vertical group Mixed group

Careful attention must be given in these group structures to calculating the parent

entity interest and the non-controlling interest in the ‘bottom’ company in the

group, which in this example is T.

To prepare the consolidated financial statements of H, we need to know the

percentage interest held by:

H in S and

H in T.

The percentage ownership of H in S is straightforward. The problem is to decide the

percentage ownership of H in T.

2.2 The rules for vertical groups

In a vertical group structure, the holding company H is said to have an ‘indirect’

interest in the sub-subsidiary T. H does not own any shares in T, but it has an

indirect interest in T through its control of subsidiary S, which in turn controls T.

When the one-stage method of consolidation is used, the indirect interest of the

holding company in a sub-subsidiary is calculated, as a percentage, as follows:

Chapter 5: Group financial statements: complex groups

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 137

Indirect holding of H in T (%) =

[% direct holding by H in S] × [% direct holding by S in T]

This indirect holding may be less than 50%.

The non-controlling interest in T, as a percentage =

100% minus Indirect holding of H in T (%)

Example

In the above example of a vertical group, the direct and indirect interests of H in its

subsidiaries are calculated as follows:

OwnershipofS

DirectholdingofHinS 75%

Non‐controllinginterestinS(thebalance)

25%

100%

OwnershipofT

DirectholdingofH 0%

IndirectholdingofH(75%×60%)

45%

45%

Non‐controllinginterestinT(thebalance) 55%

100%

Note that the non-controlling interest in the sub-subsidiary T is more than 50% in

this example. This is not unusual in complex groups when the one-stage method of

consolidation is applied.

The ownership percentages calculated in this way are used in the consolidation

process for the vertical group. H has a 75% share of S and a 45% share of T. The non-

controlling interest is 25% in S and 55% in T.

2.3 The rules for mixed groups

In our example of a mixed group, H has two interests in T:

It has a direct interest in T, with the shares that it owns in T.

It also has an indirect interest in T, through its control of S, which also owns

shares in T.

The group interest in the sub-subsidiary T is the sum of the direct interest and the

indirect interest in T.

Paper P2: Corporate Reporting (International)

138 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

%

Direct holding by H in T A

Indirect holding in T [% direct holding by H in S] × [% direct holding by

S in T]

B

A + B

Non-controlling interest % = 100% – (A + B)%

Example

Using the example of the mixed group above and applying the one-stage method of

consolidation, the percentage interest of the holding company in S and T, and the

percentage non-controlling interest in S and T, are calculated as follows:

OwnershipofS

DirectholdingofH 60%

Non‐controllinginterestinS(thebalance)

40%

100%

OwnershipofT

DirectholdingofH 40%

IndirectholdingofH(60%×20%)

12%

52%

Non‐controllinginterestinT(thebalance) 48%

100%

H has a 60% interest in S and a 52% interest in T. The non-controlling interest is 40%

in S and 48% in T. These percentages should be used in the consolidation process.

Chapter 5: Group financial statements: complex groups

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 139

Identifying the date of acquisition

The problem

The rules for vertical groups

The rules for mixed groups

3 Identifying the date of acquisition

3.1 The problem

It is important to establish the date on which a subsidiary is acquired by the group,

for the purpose of consolidation. The date of acquisition is needed to calculate the

pre-acquisition profits, the goodwill and the group’s share of post-acquisition

profits.

Under the ‘one-stage approach’, the consolidated financial statements are prepared

for the ‘top company’ H, which is the holding company for the entire group. Pre-

acquisition profits must be calculated for each subsidiary as at the date that the

subsidiary became a member of the H group.

The problem is that it is not ‘obvious’ what this date should be, in the case of sub-

subsidiaries.

3.2 The rules for vertical groups

The acquisition date for a sub-subsidiary in a vertical group depends on whether:

the holding company H acquired its shares in subsidiary S before S acquired its

shares in the sub-subsidiary T, or

the holding company H acquired its shares in subsidiary S after S acquired its

shares in the sub-subsidiary T.

The rules are as follows:

If the holding company H acquired its shares in subsidiary S before S acquired

its shares in the sub-subsidiary T, the date that T becomes a member of the H

Group is the date that S acquired the shares in T.

If the holding company H acquired its shares in subsidiary S after S acquired its

shares in the sub-subsidiary T, the date that T becomes a member of the H

Group is the date that H acquired its shares in S.

Pre-acquisition reserves and post-acquisition reserves are calculated for each

subsidiary and sub-subsidiary from its date of acquisition.

Paper P2: Corporate Reporting (International)

140 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

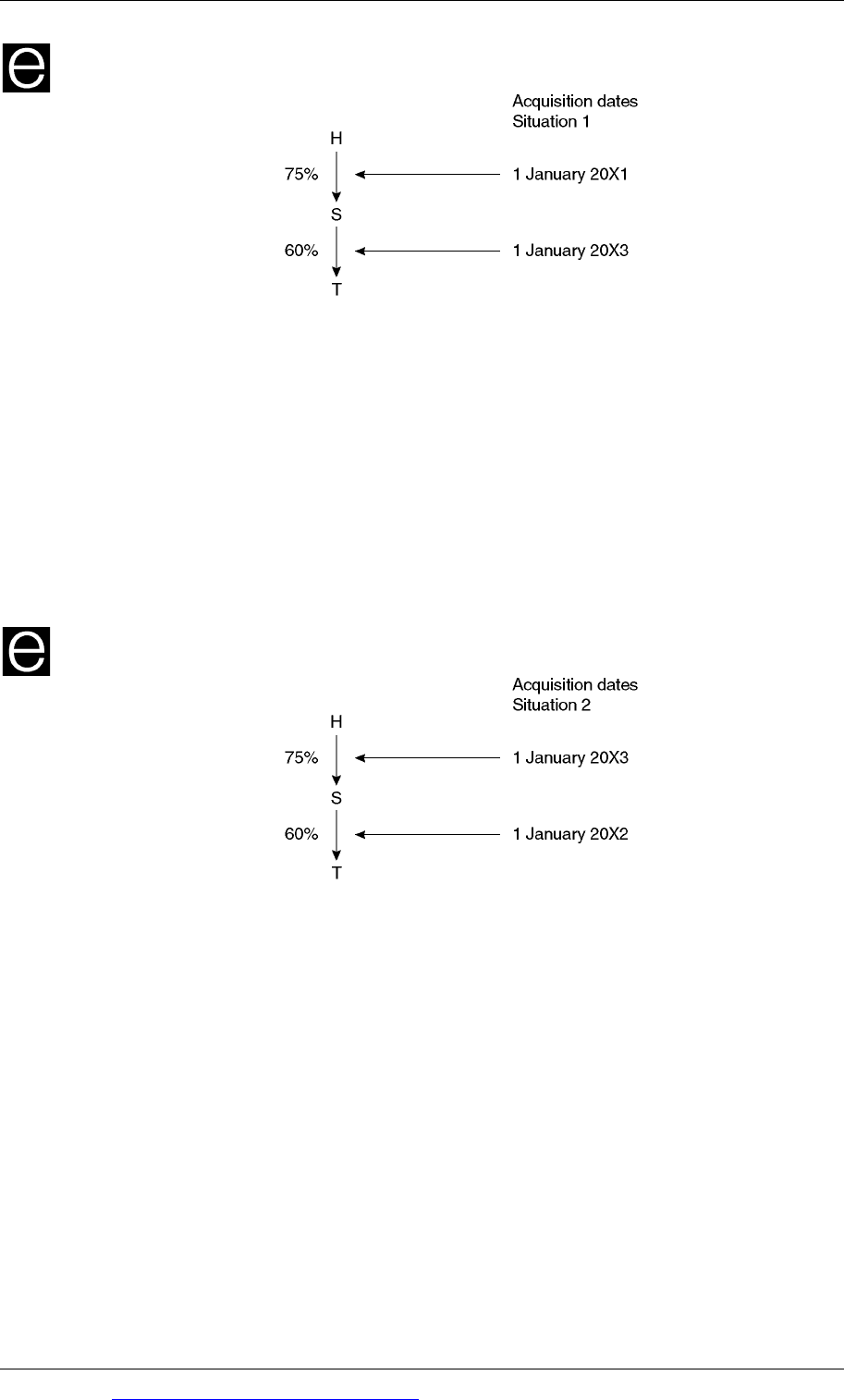

Example: H acquires control of S before S acquires control of T

In this example, H acquired its 75% interest in S on 1 January 20X1 and S acquired

its interest in T on 1 January 20X3, two years later. H acquired control of S before S

acquired control of T.

S joined the H group on 1 January 20X1, and the pre-acquisition profits of S, for

the purpose of the consolidated accounts of the H Group, are the profits existing

at 1 January 20X1.

T joined the H Group on 1 January 20X3, and the pre-acquisition profits of T, for

the purpose of the consolidated accounts of the H Group, are those existing at 1

January 20X3.

Example: H acquires control of S after S acquires control of T

In this example, H acquired its 75% interest in S on 1 January 20X3 and S acquired

its interest in T on 1 January 20X2, one year earlier. H therefore acquired control of S

after S acquires control of T.

S joins the H group on 1 January 20X3, and the pre-acquisition profits of S for the

purpose of the consolidated accounts of the H Group are those existing at 1

January 20X3.

The date that H acquires control of T is the same date that it acquires control of

S. Therefore, T also joins the H Group on 1 January 20X3, and the pre-acquisition

profits of T for the purpose of the consolidated accounts of the H Group are

those existing at 1 January 20X3.

Chapter 5: Group financial statements: complex groups

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 141

3.3 The rules for mixed groups

The same rules apply to mixed groups as they do to vertical groups.

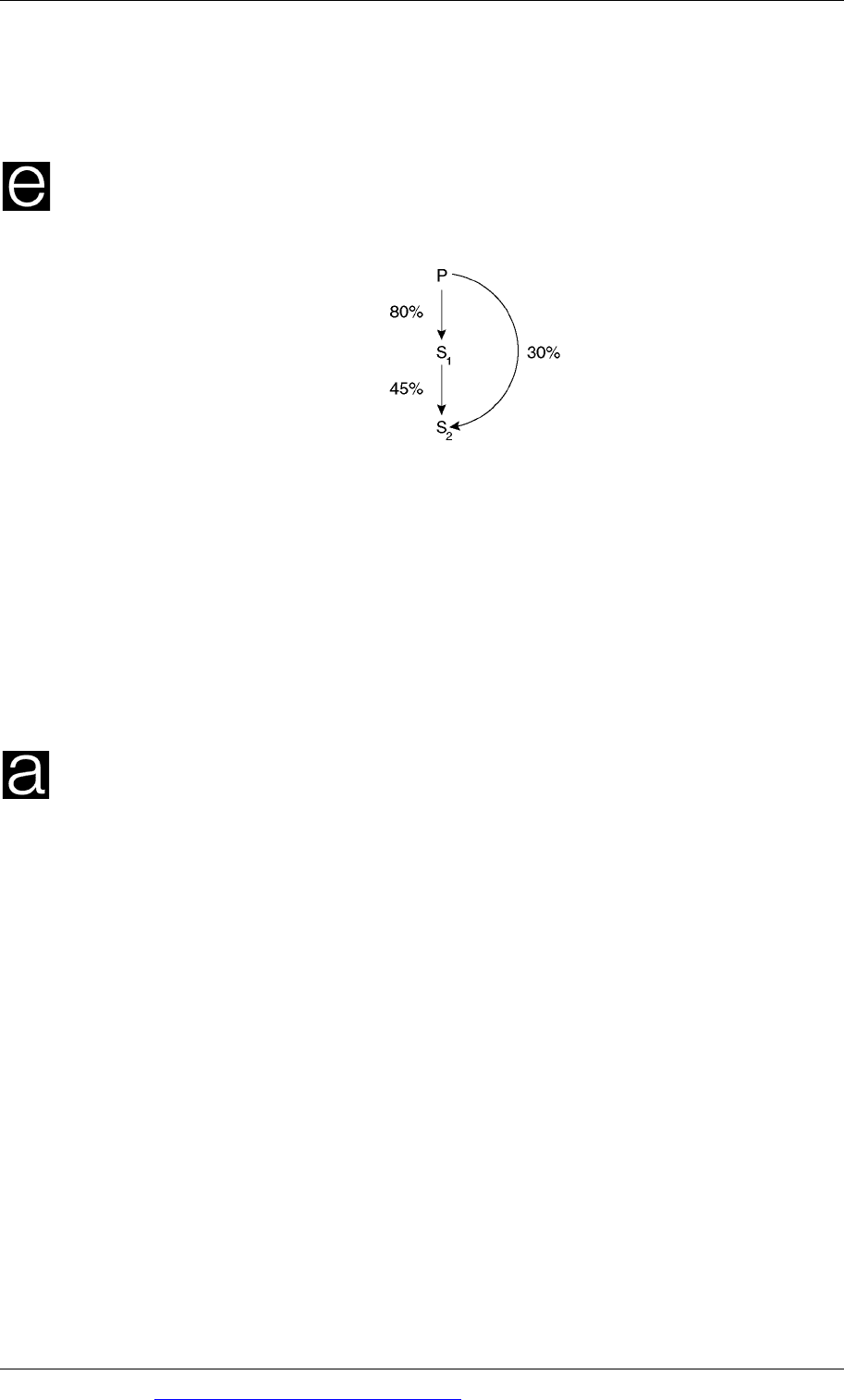

Example

The group structure of the P Group is as follows:

Required

Calculate when S

1

and S

2

became subsidiaries in the P Group in each of the

following situations:

(a) Situation 1: P acquired its shares in S

1

on 1 May 20X1, and its shares in S

2

on 1

May 20X2, and S

1

acquired its shares in S

2

on 1 May 20X3.

(b) Situation 2: P acquired its shares in S

1

on 1 May 20X4, and its shares in S

2

on 1

May 20X2, and S

1

acquired its shares in S

2

on 1 May 20X1.

Answer

The interest of P in S

2

is 30% + (80% × 45%) = 66%.

Situation 1

P obtains control of S

1

on 1 May 20X1 and the pre-acquisition profits of S

1

at that

date are used for consolidation purposes.

The date that P acquires control of S

2

is the date that S

1

acquires its stake in S

2

, which

is 1 May 20X3. The pre-acquisition profits of S

2

, when consolidating the 66%

effective interest of P, are the accumulated profits as at 1 May 20X3.

From 1 May 20X2 to 1 May 20X3, S

2

is an associate of P.

Situation 2

P obtains control of S

1

on 1 May 20X4 and the pre-acquisition profits of S

1

at that

date are used for consolidation purposes.

The date that P obtains control of S

2

is 1 May 20X4, which is the date that he

acquires his stake in S

1

and hence gains indirect control over S

1

’s holding in S

2

.

From 1 May 20X2 to 1 May 20X4, S

2

is an associate of P.

Paper P2: Corporate Reporting (International)

142 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Calculating the non-controlling interest and goodwill: indirect

holdings

The problem: indirect non-controlling interest

Calculating the non-controlling interest for the consolidated statement of

financial position

Cost of the parent entity’s investment in T

Calculating the purchased goodwill

4 Calculating the non-controlling interest and goodwill:

indirect holdings

In this section, it is assumed initially that the partial goodwill method of accounting

for non-controlling interests and goodwill is used. No goodwill in subsidiaries is

therefore attributed to the non-controlling interests.

Applying the full goodwill method to complex groups will be explained later.

4.1 The problem: indirect non-controlling interest

When the one-stage method is used to calculate the percentage share of the

ownership of subsidiaries and the percentage share owned by the non-controlling

interests, these percentages have to be converted into a money value for the purpose

of preparing consolidated accounts.

A problem arises whenever the holding company of the group has an indirect

holding in the shares of a sub-subsidiary (or a subsidiary in a mixed group) through

shares held by a subsidiary. When there is an indirect holding by the parent

company through ownership of shares in a subsidiary, there is also an indirect non-

controlling interest. This is because the non-controlling interests in the subsidiary S

have an interest in the shares of T through their ownership of the shares in S.

The same group structures that we have used before will be used again as

illustration.

Vertical group Mixed group

Vertical group: indirect non-controlling interest

It has already been shown that using the one-stage method, the percentage

ownership of T in the vertical group is as follows: