ACCA P2 (INT) Corporate Reporting - Study text - 2010 (Emile Woolf)

Подождите немного. Документ загружается.

Chapter 4: Group financial statements

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 123

In the statement of financial position, the investment in the associate is as follows:

$

Investmentatcost

147,000

Investor’sshareofpost‐acquisitionprofitsofA 75,000

Minus:Accumulatedimpairmentintheinvestment

(18,000)

–––––––––––––––––––

Investmentintheassociate

204,000

–––––––––––––––––––

Alternatively this can be calculated as:

$

Investor’sshareofnetassetsatendofreportingperiod:

(600,000×30%) 180,000

Goodwill(147,000–(350,000×30%))

42,000

Lessimpairment

(18,000)

–––––––––––––––––––

Investmentintheassociate

204,000

–––––––––––––––––––

The accumulated profits will include:

$

Investor’sshareofpost‐acquisitionprofitsofA

75,000

Minus:Accumulatedimpairmentintheinvestment (18,000)

–––––––––––––––––––

57,000

–––––––––––––––––––

In the statement of comprehensive income, the share of the associate’s after-tax

profit for the year is shown on a separate line in the profit or loss section of the

statement:

Share of profits of associate (30% × $80,000): $24,000.

Trading with an associate: unrealised profit in closing inventory

When the investor entity (or a subsidiary) trades with an associate:

the investor entity might owe money to the associate at the end of the reporting

period, or be owed money by the associate

closing inventory might be held by the investor entity or by the associate that

includes some unrealised profit on sales between the investor entity and the

associate (in the same way that there might be unrealised profit in inventory

sold between a parent and a subsidiary).

The accounting rules for dealing with these items for associates are different from

the rules for subsidiaries.

Paper P2: Corporate Reporting (International)

124 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Inter-entity balances. Any amount owed by the investor entity to the associate or

owed by the associate to the investor entity should be included in the current

liabilities or current assets in the statement of financial position of the investor entity

(and in its consolidated statement of financial position, if it prepares consolidated

accounts). In other words, inter-entity balances are not self-cancelling.

Unrealised inter-group profit. However, any unrealised profit in closing inventory

must be removed.

If the unrealised profit is held in inventory of the investor/reporting entity, the

inventory should be reduced in value by the amount of the unrealised profit

If the unrealised profit is held in inventory of the associate, the investment in the

associate should be reduced by the investor’s share (reporting entity’s share) of

the unrealised profit.

In both cases, there should also be a reduction in the post-acquisition profits of the

associate, and the investor entity’s share of those profits (as reported in profit or

loss). This will reduce the accumulated profits in the statement of financial position.

Example

Entity P acquired 40% of the equity shares of Entity A several years ago. The cost of

the investment was $205,000. There has been no impairment in the investment.

Entity P’s share of the post-acquisition retained profits of Entity A was $90,000 as at

31 December Year 5. In the year to 31 December Year 6, the reported profits after tax

of Entity A were $50,000.

In the year to 31 December Year 6, Entity P sold $200,000 of goods to Entity A, and

the mark-up was 100% on cost. Of these goods, $30,000 were still held as inventory

by Entity A at the year-end.

The unrealised profit on this inventory is $30,000 × (100/200) = $15,000. Entity P’s

share of this unrealised profit is (40%) $6,000.

The unrealised profits are in inventory held by the associate; therefore the

investment in the associate is reduced by the investor company’s share of the

unrealised profit. The investment in the associate at 31 December Year 6 is as

follows:

$

Costoftheinvestment

205,000

EntityP’sshareofpost‐acquisitionprofitsofEntityA

[$90,000+(40%×$50,000)]

110,000

Minus:EntityP’sshareofunrealisedprofitininventory

(6,000)

Minus:Accumulatedimpairmentintheinvestment

(0)

–––––––––––––––––––

309,000

–––––––––––––––––––

Chapter 4: Group financial statements

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 125

The share of the profits of Entity A reported in the profit or loss of Entity P for the

year to 31 December Year 6 is after deducting its share of the unrealised profit:

= (40% × $50,000) – $6,000 = $14,000.

This will also be included within the accumulated profits in the statement of

financial position of Entity P as at 31 December Year 6.

The reasons for the use of the equity method

The equity method is used to represent the nature of the relationship between an

investor and an associate.

The equity method reflects the investor’s significant influence. This is less than

control, but more than just the right to receive dividends that a simple investment

would give.

Consolidated financial statements include 100% of a subsidiary’s assets and

liabilities, because these are controlled by the parent, even if the parent owns less

than 100% of the equity shares. Consolidation would not be an appropriate way of

accounting for an associate.

Under the equity method:

the investor’s share of the associate’s assets, liabilities, profits and losses is

included in the investor’s financial statements; this represents significant

influence

the investor’s share of the associate is shown on one line in profit or loss, one

line in other comprehensive income and one line in the statement of financial

position, making it clear that the associate is separate from the main group (a

single economic entity).

Disadvantages of the equity method

The equity method has some important disadvantages for users of the financial

statements.

Because only the investor’s share of the net assets is shown, information about

individual assets and liabilities can be hidden. For example, if an associate has

significant borrowings or other liabilities, this is not obvious to a user of the

investor’s financial statements.

In the same way, the equity method does not provide any information about the

components that make up an associate’s profit for the period.

5.4 Accounting for interests in joint ventures

The method of accounting for an interest in a joint venture depends on what type of

joint venture it is.

Paper P2: Corporate Reporting (International)

126 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Accounting for a jointly-controlled operation

When an entity has an interest in a jointly-controlled operation, it should recognise

the following in its financial statements:

the assets that it controls and the liabilities that it incurs

the expenses that it incurs, and

its share of the income that it earns from sales by the joint venture.

Example

Entity X and Entity Y undertake a joint venture. Each entity undertakes to bear its

own expenses, but to share revenues from sales by the joint venture 50:50.

During the first year of the operation, Entity X made sales of $420,000 and Entity Y

made sales of $370,000. Costs incurred by Entity X were $280,000 and by Entity Y

were $290,000.

To finance the operation, Entity X took out a bank loan of $40,000.

Profit or loss of Entity X

Since each joint venturer bears all its own expenses, the profit or loss of Entity X will

include:

$

Shareofsales:$(420,000+370,000)×50%

395,000

Owncosts 280,000

Profit

115,000

The sales reported by each joint venturer are 50% of the total sales of the joint

venture, in accordance with the joint venture agreement. The reported sales are not

the sales actually made by the entity: for example the reported sales of Entity X are

not $420,000.

Since Entity X made more sales than Entity Y, the joint venture agreement will

provide for a payment by Entity X to Entity Y, to equalise their actual revenues.

Extracts from statement of financial position, Entity X

The statement of financial position of Entity X will include:

$

Liabilities

Bankloan 40,000

PayabletoEntityY(seebelow)

25,000

Chapter 4: Group financial statements

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 127

Workings

JointventurewithY:currentaccount

$

$

Sales(50%share) 395,000

Cash(ownsales) 420,000

Balance(payabletoY) 25,000

420,000

420,000

Balance(payabletoY)

Accounting for jointly-controlled assets

When an entity has an interest in jointly-controlled assets, it should recognise the

following in its financial statements:

Its share of the jointly-controlled assets, classified according to the nature of the

assets. For example, a joint share of an oil pipeline would be included in

property, plant and equipment in the statement of financial position

Any liabilities that it has incurred

Its share of any liabilities incurred jointly with the other joint venturers

Its income from the sale (or use of) its share of the output of the joint venture,

together with its share of any expenses incurred by the joint venture

Any expenses that it has incurred in respect of its interest in the joint venture.

These assets, liabilities, income and expenses are recognised in the financial

statements of the venturer. This means that no adjustments are needed on

consolidation for these items, when the venturer prepares consolidated financial

statements.

Example

On 1 January 20X7, Entity B and Entity C entered into a joint venture to purchase

and operate an oil pipeline. Both entities would contribute equally to the purchase

cost of $20 million. Entity C was responsible for carrying out all maintenance work

on the pipeline, but maintenance expenses were to be shared between B and C in the

ratio 40%: 60%.

In order to pay for the pipeline, the joint venturers obtained a joint loan of

$20,000,000 from a bank. Interest of $1,500,000 was paid for the year on 31 December

by Entity B.

Both entities would use the pipeline for their own operations, but any income from

third parties would be shared 50%: 50%.

The pipeline has an estimated useful life of 20 years and no residual value. Both

entities apply this depreciation policy to the asset. A full year’s depreciation will be

charged in 20X7.

During the year to 31 December 20X7, maintenance and running expenses were

$1,200,000 and income from third parties was $900,000. All this income was paid to

Entity C by the third parties.

Paper P2: Corporate Reporting (International)

128 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Required

Show the relevant figures that would be recognised in the financial statements of

Entity B and Entity C for the year to 31 December 20X7.

Answer

Total

amount

InEntityB

financial

statements

InEntityC

financial

statements

$ $ $

Jointly‐controlledassets

Property,plantandequipment

Cost 20,000,000 10,000,000 10,000,000

Accumulateddepreciation

1,000,000 500,000 500,000

–

––––––––––––––––––––––

–

–

––––––––––––––––––––––

–

–––––––––––––––––––––––

–

19,000,000 9,500,000 9,500,000

–

––––––––––––––––––––––

–

–

––––––––––––––––––––––

–

–––––––––––––––––––––––

–

Shareofliabilitiesincurred

Bankloan 20,000,000 10,000,000 10,000,000

Current:accountwithB(owedtoB)–seeworkings 720,000

Current:accountwithC(owedbyC)–seeworkings

720,000

Shareofexpenses

Depreciation(50:50) 1,000,000 500,000 500,000

Maintenancecosts(40:60)

1,200,000 480,000 720,000

Interestonloan(50:50)

1,500,000 750,000 750,000

Workings

IntheaccountsofB

JointventurewithC:currentaccount

$

$

Revenuereceivablefrom

C

450,000

Maintenancecosts

(payabletoC) 480,000

InterestpayablebyC 750,000

Balance(payablebyC) 720,000

1,200,000

1,200,000

Balanceb/d 720,000

Chapter 4: Group financial statements

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 129

IntheaccountsofC

JointventurewithB:currentaccount

$

$

Maintenancecosts 480,000

InterestpayabletoB 750,000

(payablebyB)

RevenuepayabletoB 450,000

Balance(payabletoB) 720,000

1,200,000

1,200,000

Balanceb/d 720,000

5.5 Accounting for jointly-controlled entities

IAS 31 requires that an entity should disclose its interest in a jointly-controlled

entity using either:

the proportionate consolidation method, or

the equity method of accounting. This is exactly the same as accounting for

investments in associates.

Proportionate consolidation is described below.

Proportionate consolidation

Proportionate consolidation is a method of accounting in which the financial

statements of a joint venturer recognise:

in its statement of financial position (or consolidated statement of financial

position)

— its proportionate share of the assets it controls jointly, and

— its proportionate share of the liabilities for which it is jointly responsible

in its statement of comprehensive income (or consolidated statement of

comprehensive income), its proportionate share of the income and expenses of

the jointly-controlled entity

Two methods of presentation

Proportionate consolidation can be presented in either of two ways. Both ways are

permitted by IAS 31.

Method 1

A joint venturer may combine its share of the assets, liabilities, income and expenses

of the jointly-controlled entity with similar items, line by line, in its financial

statements.

For example, in its statement of financial position it may combine its share of the

joint venture’s inventory with its own inventory, and combine its share of the

property, plant and equipment of the joint venture with its own property, plant and

equipment.

Paper P2: Corporate Reporting (International)

130 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Method 2

Alternatively, a joint venturer may include separate line items for its share of the

assets, liabilities, income and expenses of the jointly-controlled entity.

For example, in its statement of financial position it may show its share of a current

asset of the jointly-controlled asset on a separate line as part of current assets.

Similarly it may show its share of the property, plant and equipment of the joint

venture in a separate line as part of property, plant and equipment.

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 131

Paper P2 (INT)

Corporate Reporting

CHAPTER

5

Group financial statements:

complex groups

Contents

1 The nature of complex groups

2 Calculating parent entity holdings and non-

controlling interests

3 Identifying the date of acquisition

4 Calculating the non-controlling interest and

goodwill: indirect holdings

Paper P2: Corporate Reporting (International)

132 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The nature of complex groups

Complex group structures

Checking the status of investments

Consolidation in practice and consolidation in the examination

Problem areas with complex groups

1 The nature of complex groups

1.1 Complex group structures

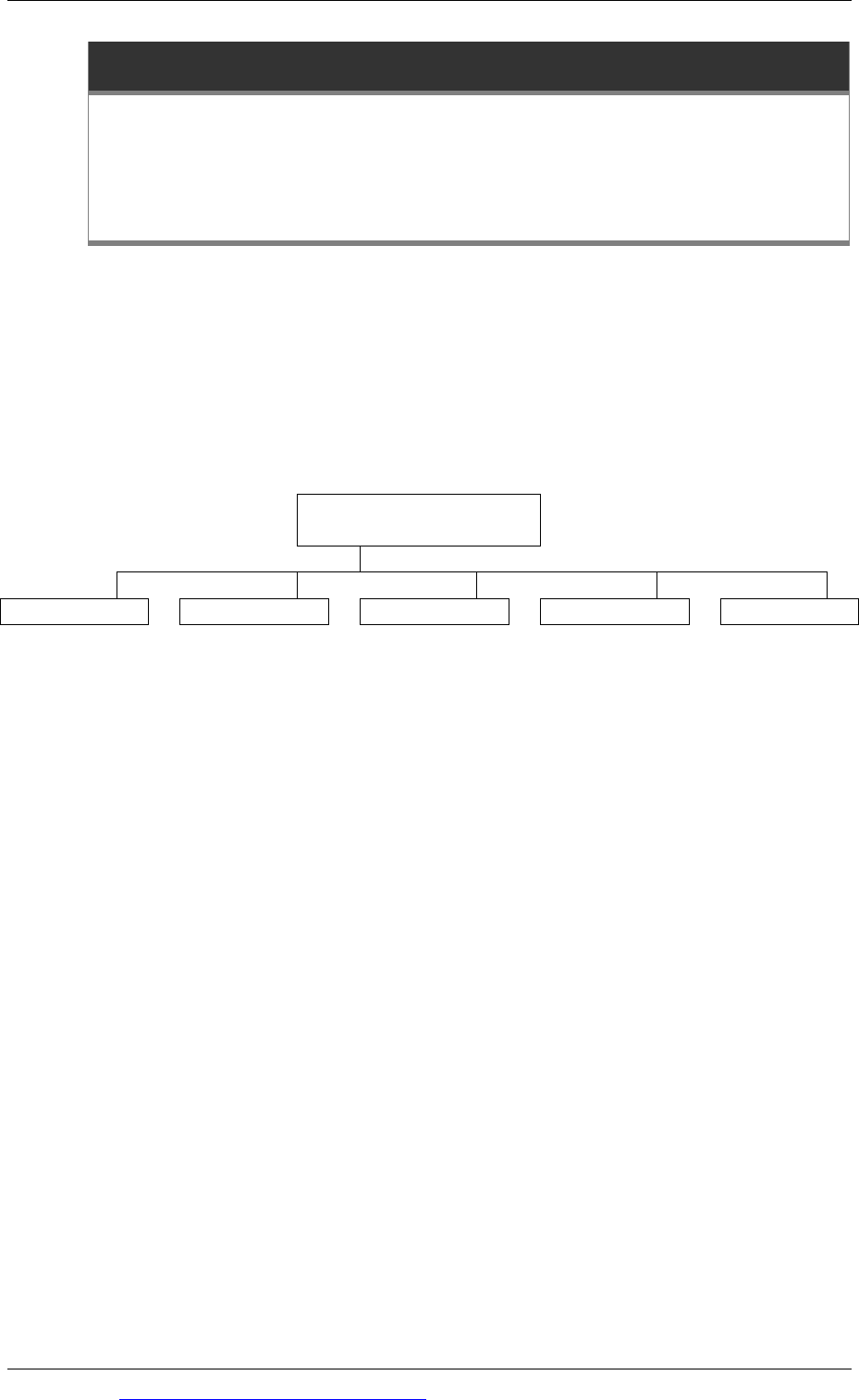

In a simple group, a parent owns one or more subsidiaries and possibly also has an

associate or joint venture.

Parent/holding

company

Subsidiary 1 Subsidiary 2 Subsidiary 3 Subsidiary 4 Associate

A more complex group may be one of the following two types:

A ‘vertical group’ in which the parent company or holding company (H) owns a

subsidiary (S) and the subsidiary owns its own subsidiary (T)

A ‘mixed group’, in which the parent company (H) owns shares in two companies.

It owns more than 50% in one of these companies (S), but less than 50% in the other

company (T). However, company S also owns shares in T, and the combined

shareholding of H and S in company T, taken together, exceeds 50%. (Note that

mixed groups are sometimes called D-shaped groups due to the shape of the group

structure.)

These two types of group are illustrated in the diagrams below. The percentage

shareholdings are included for illustrative purposes, but these percentages will be

used in the examples and explanations that follow.