ACCA P2 (INT) Corporate Reporting - Study text - 2010 (Emile Woolf)

Подождите немного. Документ загружается.

Chapter 7: Group reorganisations and restructuring

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 173

To create the new holding company, the former shareholders of Company X may

exchange their shares in Company X for shares in the new holding company H.

They become the owners of H, and H is the 100% owner of Company X.

In these arrangements, there is usually just a share-for-share exchange, with shares

in X exchanged for shares in H, and no cash transactions are involved.

Occasionally, however, there may be some cash transactions involved.

The shareholders in Company X may be required to subscribe some extra cash as

well as exchange their shares in Company X in order to acquire their new shares

in H.

The new holding company H may acquire cash from an external source (for

example, by borrowing) and use this cash to buy back and cancel some of the

shares in Company X. In this situation, some shareholders in Company X will

sell their shares and no longer be shareholders in the group; the other

shareholders will exchange their shares for the new shares in H.

Accounting for a new holding company

When a new holding company is created, it has to prepare consolidated financial

statements for the group. At one time when a new holding company was created by

a share exchange, with no cash transactions involved, the restructuring could be

accounted for using the ‘pooling of interests’ method of accounting.

This is illustrated below.

Example

A group consists of a parent company A and a 100%-owned subsidiary B. Entity A

has owned its shares in Entity B since B was incorporated. Their statements of

financial position are shown below.

EntityA

EntityB

$000

$000

Tangiblenon‐currentassets 500

250

InvestmentinB

100

‐

Netcurrentassets

200

150

800

400

Sharecapital 200

100

Reserves

600

300

800

400

A new holding company, H, is created. H acquires all the shares in Entity A in by

issuing and exchanging 400,000 $1 shares of its own.

Paper P2: Corporate Reporting (International)

174 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

If the consolidated statement of financial position of the new group is prepared

using the ‘pooling of interests’ method, the shares of H are stated at nominal value

rather than fair value and there is no purchased goodwill. The statements of

financial position for each company and the consolidated statement of financial

position for the group would be as follows, immediately after the restructuring.

EntityH

EntityA EntityB

Group

$000

$000

$000

$000

Tangiblenon‐currentassets ‐

500

250

750

InvestmentinB

400

100

‐

‐

Netcurrentassets

‐

200

150

350

400

800

400

1,100

Sharecapital 400

200

100

400

Reserves

0

600

300

700

400

800

400

1,100

The group reserves are the pre-restructuring reserves of A and B ($900,000) minus

the nominal share capital of A.

The original IFRS 3 Business combinations was issued in 2004. It replaced IAS 22

which had permitted the use of the pooling of interests method of accounting in

certain circumstances. IFRS 3 prohibited the use of the pooling of interests method

for all types of business combination covered by the IFRS.

However, IFRS 3 (revised 2008) does not apply to business combinations involving

entities or business under common control, and so it does not apply to the creation

of a new holding company (where no cash transactions occur). The IASB has this

type of business combination under review.

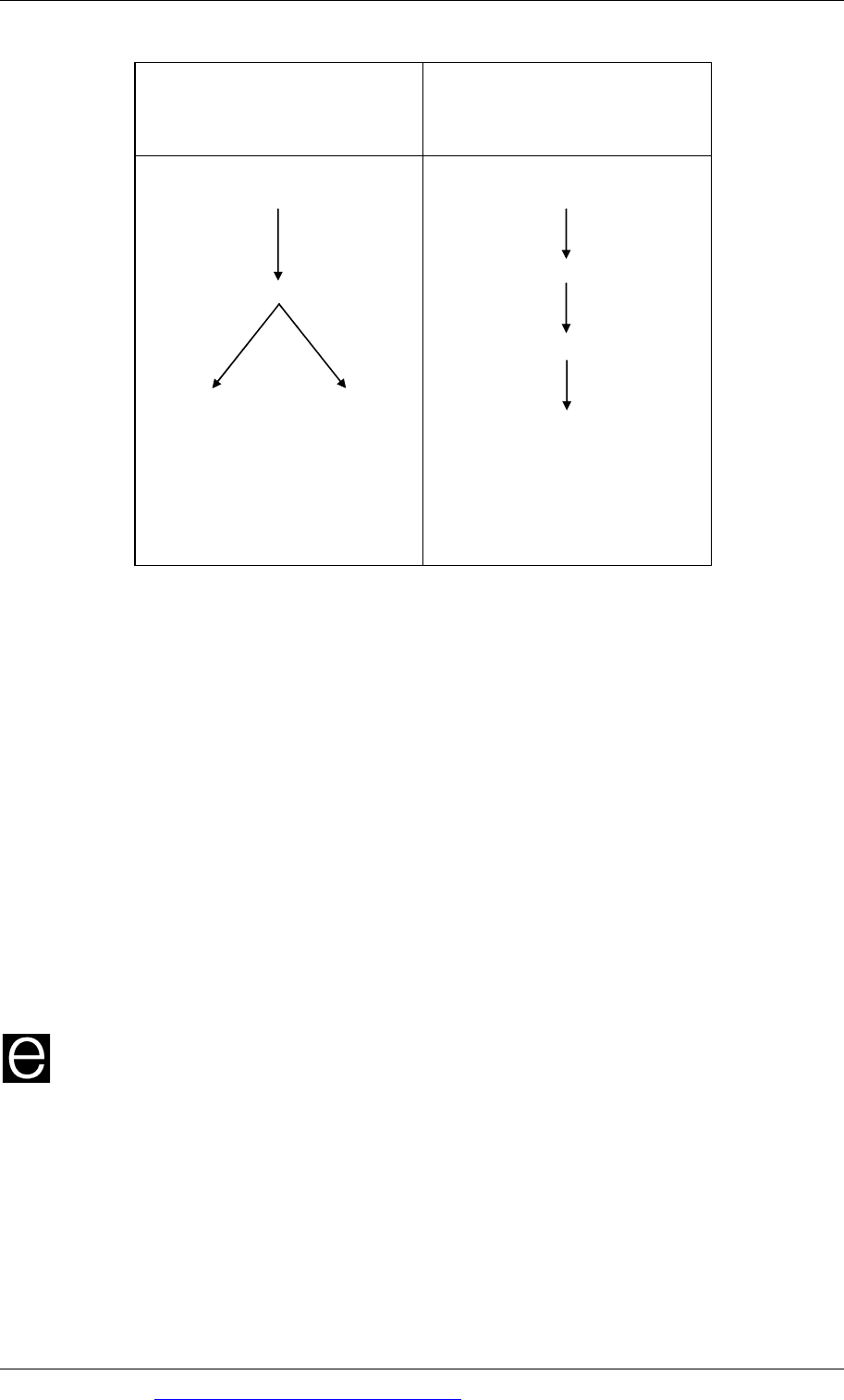

1.3 A change in ownership of companies within a group

When companies in a group are 100%-owned, it may be decided to reorganise the

group and transfer ownership of subsidiaries from one group company to another.

For example, a holding company H may own two subsidiaries, Entity A and Entity

B. It may be proposed that Entity A should buy the shares in Entity B from H, for

cash. As a result of this reorganisation, Entity B would become a subsidiary of

Entity A and a sub-subsidiary of H. There would also be a transfer of cash from

Entity A to H, in exchange for the shares in Entity B.

Chapter 7: Group reorganisations and restructuring

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 175

Current structure Proposed structure

Shareholders

H

100% 100%

A B

Shareholders

H

A

B

Company A buys the equity

capital of B from H for cash.

All companies continue to

operate.

In the proposed structure, there is a change in the ownership of Entity B, as it has

been transferred so that it is directly owned by Entity A, not H. The accounting

implications are as follows:

The reorganisation has not changed the assets of the group and so will not affect

the group financial statements.

In the individual accounts of H, there is a gain or loss in disposal of the shares in

Entity B. In H’s own financial statements, the cost of the investment in Entity B is

removed and replaced with the cash received, together with the resulting gain or

loss (in H’s reserves).

Accounting for a change of ownership within the group

Accounting for a change in ownership will be illustrated using the same example,

but with some illustrative figures.

Example

Suppose that the following data applies to the reorganisation described above, and

the partial goodwill method of accounting is used:

The cost of H's investment in B was $95. The investment was bought when the

fair value of the net assets of B was $87.

The issued capital of B is $70.

Half of the goodwill arising on the original acquisition of B is now impaired.

A pays H $100 to buy the share capital of B, when the net assets of B are valued

at $ 75. This cash is to be loaned by H to B on an inter-company account.

Paper P2: Corporate Reporting (International)

176 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Answer

The proposal does not change the initial value of the goodwill arising when H

purchased B. The original goodwill figure is 8 (95 - 87).

Half of this will be written off against group reserves as an impairment loss. The

remaining 4 is carried on the consolidated statement of financial position of the H

Group.

A gain on the disposal of the investment in Entity B will be recognised in the

individual financial statements of H, but as this is an inter-company profit, it will be

eliminated on consolidation.

Alternative change in ownership

An alternative situation is where a subsidiary becomes directly owned by the

parent, as can be seen in the diagram below.

Before: After:

Company A Company A

Company B

Company B Company C

Company C

This type of group reorganisation is often done when the parent company wishes to

sell Company B, but to retain company C. This reorganisation will have no effect on

the consolidated accounts because the group remains the same. It is the individual

companies whose accounts will change.

This transaction cannot normally be effected by a share-for-share exchange, because

the law in some countries does not allow a subsidiary to hold shares in a parent

company. Instead, Company B pays a special dividend called a ‘dividend in specie’

to the parent, which is effectively the cost of investment in Company C. Company B

must have sufficient distributable profits to do this.

Alternatively, Company A can pay cash to Company B in return for the investment

in Company C.

Chapter 7: Group reorganisations and restructuring

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 177

1.4 Divisionalisation within a group

Within a group, there may be operating divisions, and each division may be

established as a subsidiary company within the group. Each division may own

several sub-subsidiaries, each responsible for a different aspect of the division’s

overall operations.

When there is divisionalisation of operations within the group, it may be decided

from time to time to switch assets from one division to another. For example, it may

be decided to close down one division and transfer its operations to another

division.

Example

A holding company H owns two subsidiaries Entity A and Entity B. Each entity is a

separate operating division within the group. Entity B has recently been making

losses, and it is proposed that Entity B should be closed down. All its net assets will

be transferred to Entity A, for an agreed purchase price.

The proposed restructuring is shown below.

Current structure Proposed structure

Shareholders

H

100% 100%

A B

Shareholders

H

A

B

Company A buys the equity

capital of B from H for cash.

All companies continue to

operate.

Accounting for a divisional reorganisation

This is a divisionalisation restructuring or reorganisation. It does not affect the

ownership of Entity B. Entity B is still owned by H and the investment remains in

the statement of financial position of H. Entity B has simply transferred its assets,

liabilities and all business operations to Entity A, in exchange for cash. As a result,

Entity B is now a ‘shell’ company, containing just share capital and the cash from

the sale.

Paper P2: Corporate Reporting (International)

178 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

There is no effect on the group financial statements as the assets of the group are

unchanged.

There has not been a disposal of shares in Entity B by H, so the investment must

remain in the accounts of H.

The investment in Entity B in the individual H’s accounts will certainly have

suffered impairment, given that the trade of Entity B has been transferred to

Entity A.

If any goodwill arose when H acquired B, this will also be impaired, because the

business to which the goodwill relates has now been transferred.

Entity A has not bought the shares of Entity B. It has bought the net assets of B in

exchange for cash. Entity A will therefore include all of B’s net assets into its

own statement of financial position, as B’s business operations have now been

merged with A’s own.

Example

The following additional information relates to the example of the divisional

reorganisation above:

The cost of H's investment in B was $95. The investment was bought when the

fair value of the net assets of B was $87.

The issued capital of B is $70.

All the goodwill arising on the acquisition of B by H has been impaired.

The purchase consideration is $71. This will be accounted for as an inter-

company loan transaction between A and B.

Required

Explain and illustrate the impact on the group accounts of the proposed

restructuring, as far as the information given permits.

Answer

The accounting treatment of the divisional reorganisation is similar to accounting

for a transfer in the ownership of a subsidiary between companies in the group, as

described and illustrated earlier.

The proposal does not change the initial value of the goodwill arising when H

purchased A. This goodwill figure is 8 (95 - 87).

This will now be written off against group reserves as an impairment loss.

The purchase price for the net assets of B is likely to be different from the

carrying value of the assets in B’s accounts. There will be a gain for A on the

transaction and a loss for B, or a gain for B and a loss for A. These should be

eliminated on consolidation.

The inter- company loan will be eliminated on consolidation.

Chapter 7: Group reorganisations and restructuring

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 179

1.5 A demerger

A demerger occurs when a group is split into two or more smaller groups. Each of

the new smaller groups is owned by the shareholders of the original larger group.

Demergers are not common, but when they occur, there is often a strong

commercial or financial logic for the restructuring.

The original group may consist of subsidiaries in different industries. A

demerger would establish smaller groups, but each operating in an identifiable

industry.

When the original group operates in two or more completely different

industries, the market value of the group is often much less than the market

value of the two demerged smaller groups. Demergers will therefore often

‘unlock value’ for shareholders.

Each separate smaller group is able to pursue its own independent business

strategies in the future..

The nature of a demerger is illustrated in the following diagram

Current structure Proposed structure

Shareholders

H

A B

Subs Subs

Company A and its subsidiaries are in the

paints and chemicals industry.

Company B and its subsidiaries are in the

pharmaceuticals (‘drugs’) industry.

Shareholders

H B

A

Subs Subs

H transfers its interest in B and its

subsidiaries to H’s shareholders, thus

splitting the group into two mini groups.

•

H and its subsidiaries can now focus on

paints and chemicals.

•

B and its subsidiaries focus on

pharmaceuticals.

Note that from the shareholders

perspective they have the same interest as

before as they own both of the mini

groups.

Paper P2: Corporate Reporting (International)

180 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Accounting for a demerger

The accounting treatment in a demerger must recognise that H has in fact given its

investment in B to its shareholders so that they are now the legal owner. The

shareholders have given nothing in return, so effectively H has made a distribution

(or dividend) paid in the form of shares.

To account for the demerger, H must:

remove the cost of investment from its statement of financial position, and

charge the equivalent amount as a distribution to the shareholders.

This would be a transaction with the owners of the entity in their capacity as

owners; therefore the transaction is recorded directly in equity and reported in the

statement of changes in equity.

1.6 Why reorganise/restructure?

There may be various different reasons for any reorganisation or restructuring. In

principle, the underlying reason should be to improve the financial and commercial

position of the group.

Reasons for a change in ownership of companies within a group

When the ownership of a subsidiary within the group is transferred from one group

company to another, there is no impact on the consolidated financial statements (as

illustrated earlier). However, the individual accounts of the ‘buying’ and ‘selling’

group companies will be affected.

The main reason for such a reorganisation should therefore be to improve the

management of operations and improve the performance of the group as a whole.

In the example described earlier, a holding company H sold its shares in a

subsidiary B to another subsidiary, A. The effect of doing this is that Entity B will

come under the control of Entity A, instead of being directly controlled by H. The

commercial logic or reason for doing this may be as follows:

Entity B has been performing badly

Entity A has been successful, and its senior management are held in high esteem

by the management of H

Entity B and Entity A operate in similar industries (or the same industry)

It is therefore decided that the management of Entity B should be brought under

the control of the management of entity A, by making B a subsidiary of A.

This ‘management shake-up’ might be expected to improve the operating

performance of entity B.

However, there may be impairment of goodwill when the reorganisation occurs,

which reduces group reserves in the consolidated statement of financial position

and affects the group’s reported profit.

Chapter 7: Group reorganisations and restructuring

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 181

Reasons for a divisional restructuring

The reasons for a divisional restructuring may be similar: to improve the

management of operations and improve the performance of the group as a whole.

In the example described earlier, one division/subsidiary (Entity B) sold its net

assets to another division/subsidiary (Entity A). Entity A therefore takes over the

operating assets of B, but Entity B is left as a shell company with some cash. The

commercial logic or reason for doing this may be as follows:

Entity A and Entity B may operate in the same industry, or Entity B may be a

supplier to Entity A or a customer of Entity A. Transferring the net assets to

Entity B puts the combined operation under the direct control of the

management of Entity A.

Entity B might have been performing badly and Entity A may be performing

well. If so, the reorganisation will transfer control over the assets and operations

from ‘poor managers’ to ‘successful managers’, and the group might expect

performance to improve.

For example, the restructuring should lead to cost savings and higher group

profits.

Trade suppliers to Entity B may take confidence from the fact that they will now

be dealing with a more successful group company, and the credit risk may be

lower.

The holding company H might want to keep Entity B in existence as a shell

company, so that it can be used at some time in the future to acquire another

company or other assets, and so become an operating company again, except in

an entirely different area of business.

Example

This example illustrates another form of group restructuring involving a merger.

Entity K was incorporated 30 years ago by James and Sam (who are still the sole

shareholders) to import glass from Spain, France and Italy. The company has been

very successful. Three wholly-owned subsidiary companies (F, C and P) were set up

by Entity K to deal with different areas of operations. Competition in the European

Community market is changing, and James and Sam feel that their company should

expand into a larger market. For this reason, a merger is proposed with Mool, a

company which specialises in importing glass from Northern and Eastern Europe.

A joint meeting was arranged with the directors of both Entity K and Mool to

discuss various proposals to change the structure of K and the proposed merger

between K and Mool

The proposals are as follows:

A new holding company, Euroglass, is to be set up by James and Sam for the K

group. The ordinary shares in Entity K are to be exchanged on a share for share

basis with Euroglass. The same share exchange will be carried out with Mool to

effect the merger.

Paper P2: Corporate Reporting (International)

182 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

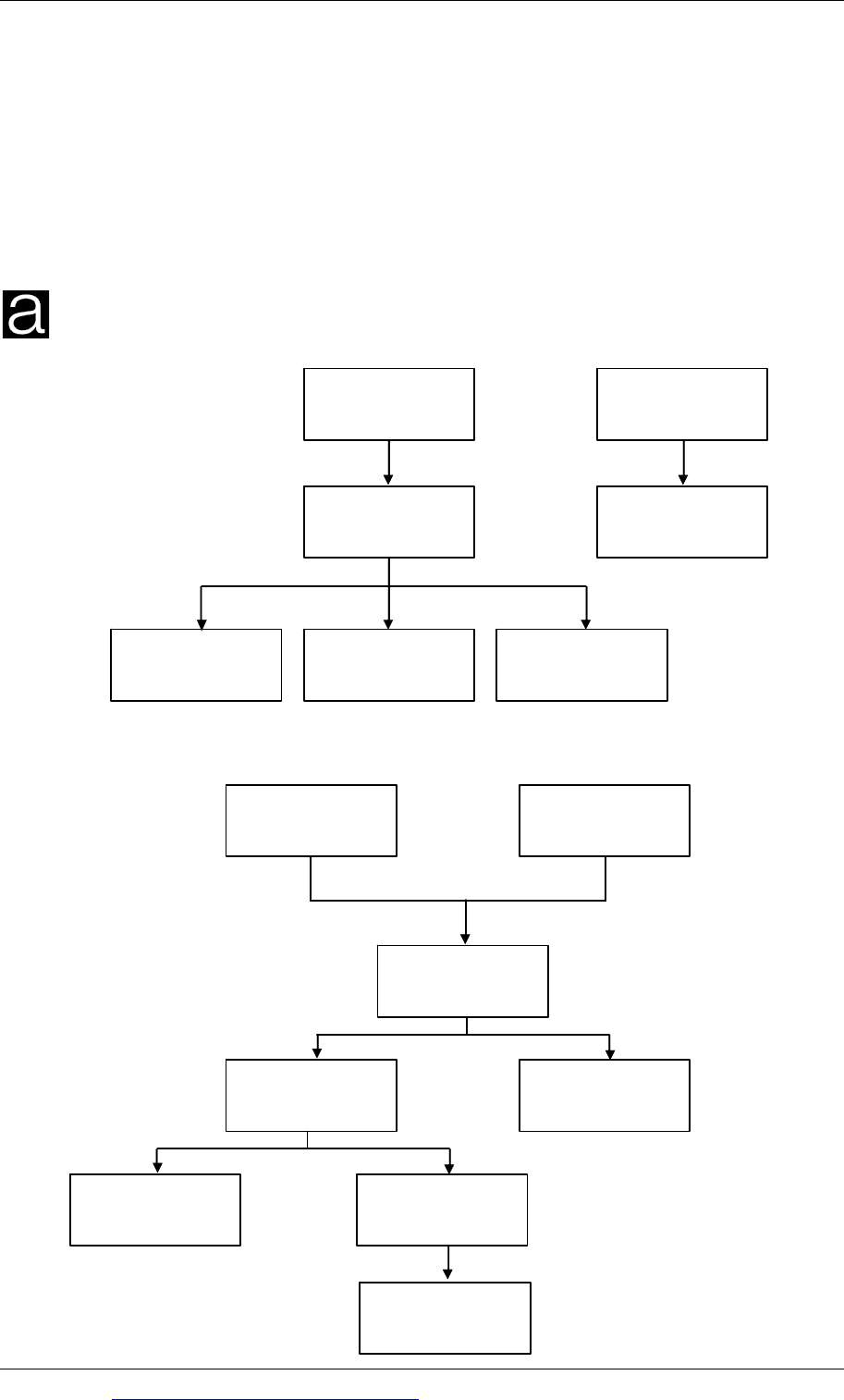

Ja mes and Sam

Entity K

Entity F

Ent it y C

Entity P

Shareholders

Mool

Ja mes an d Sam

Entit y K

Entity F

Entity C

Entity P

Mool

Shareholders

EUROGLASS

Mool

In addition, P is to become a wholly-owned subsidiary of C. This reorganisation

will be effected by the issue of ordinary shares in C.

Required

(a) Identify the structure both before and after the proposals, reflecting all the

relationships contained in the information above.

(b) Suggest any possible benefits that may arise from the revised structure.

Answer

Before

After