ACCA F5 Performance Management - 2010 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 185

Paper F5

Performancemanagement

CHAPTER

8

Quantitative analysis

in budgeting

Contents

1 Cost estimation: high/low method

2 Cost estimation: linear regression analysis

3 Correlation and the correlation coefficient

4 Time series analysis

5 The learning curve

6 Other aspects of quantitative analysis in

budgeting

Paper F5: Performance management

186 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Cost estimation: high/low method

Cost estimation: analysing fixed and variable costs

High/low analysis

High/low analysis when there is a step change in fixed costs

High/low analysis when there is a change in the variable cost per unit

1 Cost estimation: high/low method

1.1 Cost estimation: analysing fixed and variable costs

For the purposes of budgeting and decision-making, it is often necessary to prepare

an estimate of costs. For example, it is often necessary to estimate the total annual

costs of an activity or a responsibility centre, or the total annual costs of production

overheads or marketing overheads. One way of doing this is to estimate fixed costs

per period and variable costs per unit of activity from historical cost data.

If total costs can be divided into fixed costs or variable costs per unit of output or

unit of activity, a formula for total costs is:

y = a + bx

where

y = total costs in a period

x the number of units of output or the volume of activity in the period

a = the fixed costs in the period

b = the variable cost per unit of output or unit of activity.

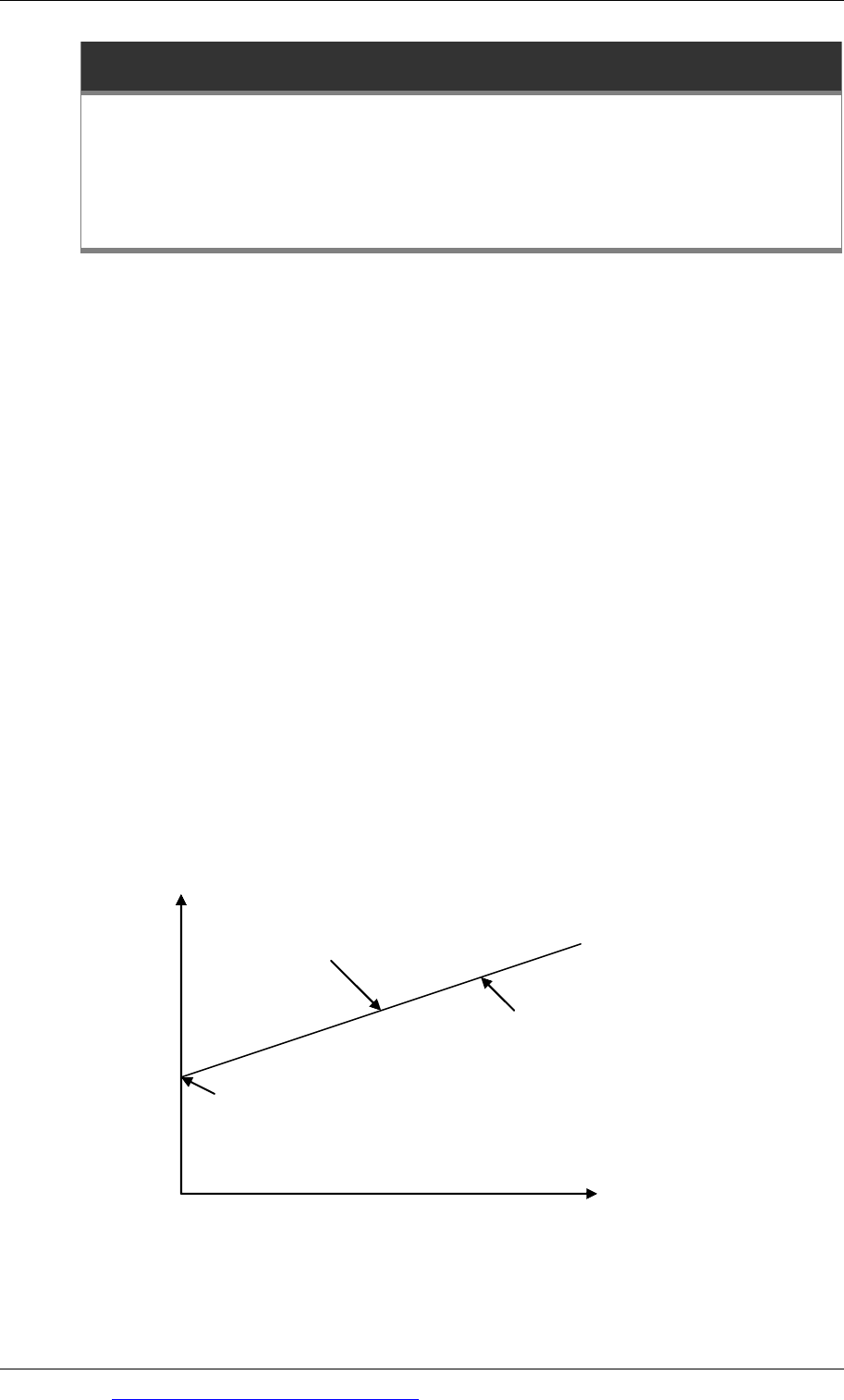

The linear cost function equation y = a + bx can be drawn on a cost behaviour graph

as follows.

Total

cost

y

gradient of cost function = b

(variable cost per unit)

cost function

y = a + bx

(total cost line)

a = fixed cost

Volume of activit

y

x

Chapter 8: Quantitative analysis in budgeting

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 187

Two methods of estimating fixed and variable costs from historical data for total

costs are:

high/low analysis

linear regression analysis.

1.2 High/low analysis

High/low analysis can be used to estimate fixed costs and variable costs per unit

whenever:

there are figures available for total costs at two different levels of output or

activity

it can be assumed that fixed costs are the same in total at each level of activity,

and

the variable cost per unit is constant at both levels of activity.

High/low analysis therefore uses two historical figures for cost:

the highest recorded output level, and its associated total cost

the lowest recorded output level, and its associated total cost.

It is assumed that these ‘high’ and ‘low’ records of output and historical cost are

representative of costs at all levels of output or activity.

The difference between the total cost at the high level of output and the total cost at

the low level of output is entirely variable cost. This is because fixed costs are the

same in total at both levels of output.

The method

There are just a few simple steps involved in high/low analysis.

Step 1

Take the activity level and cost for:

the highest activity level

the lowest activity level.

Step 2

The difference between the total cost of the highest activity level and the total cost of

the lowest activity level consists entirely of variable costs. This is because the fixed

costs are the same at all levels of activity.

Activity

level

$

High: Total cost of A

= TCa

Low: Total cost of B

= TCb

Difference: Variable cost of (A – B) units (A – B)

= TCa - TCb

From this difference, we can therefore calculate the variable cost per unit of activity.

Paper F5: Performance management

188 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Variable cost per unit = $(TCa – TCb)/ (A – B) units

Having calculated a variable cost per unit of activity, we can now calculate fixed

costs.

Step 3

Having calculated the variable cost per unit, apply this value to the cost of either the

highest or the lowest activity level. (It does not matter whether you use the high

level or the low level of activity. Your calculation of fixed costs will be the same.)

Calculate the total variable costs at this activity level.

Step 4

The difference between the total cost at this activity level and the total variable cost

at this activity level is the fixed cost.

Substitute in the ‘low’ equation Cost

$

Total cost of (low volume of activity) TCb

Variable cost of (low volume of activity) V

Therefore fixed costs per period of time TCb - V

You now have an estimate of the variable cost per unit and the total fixed costs.

The high/low method is a simple but important technique that you need to

understand. Study the following example carefully.

Example

A company has recorded the following costs in the past six months:

Month Activity

Total cost

Direct labour hours

$

January 5,800

40,300

February 7,700

47,100

March 8,200

48,700

April 6,100

40,600

May 6,500

44,500

June 7,500

47,100

Required

Using high/low analysis, prepare an estimate of total costs in July if output is

expected to be 7,000 direct labour hours.

Chapter 8: Quantitative analysis in budgeting

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 189

Answer

(1) Steps 1 and 2: Calculate the variable cost per hour

Take the highest level of activity and the lowest level of activity, and the total costs

of each. Ignore the other data for levels of activity in between the highest and the

lowest.

Hours

$

High: Total cost of 8,200 hours

= 48,700

Low: Total cost of 5,800 hours

= 40,300

Difference: Variable cost of 2,400 hours

= 8,400

Therefore variable cost per direct labour hour = $8,400/2,400 hours = $3.50.

(2) Steps 3 and 4: Calculate fixed costs

Substitute in the ‘high’ equation Cost

$

Total cost of 8,200 hours 48,700

Variable cost of 8,200 hours (× $3.50 per hour) 28,700

Therefore fixed costs per month 20,000

(3) Using the cost analysis: Prepare a cost estimate of total costs for 7,000 hours

Cost estimate for May Cost

$

Fixed costs 20,000

Variable cost (7,000 hours × $3.50 per hour) 24,500

Estimated total costs 44,500

The technique can be used any time that you are given two figures for total costs, at

different levels of activity or volumes of output, and you need to estimate fixed

costs and a variable cost per unit.

1.3 High/low analysis when there is a step change in fixed costs

High/low analysis can be used even when there is a step increase in fixed costs

between the ‘low’ and the ‘high’ activity levels, provided that the amount of the step

increase in fixed costs is known.

If the step increase in fixed costs is given as a money amount, the total cost of the

‘high’ or the ‘low’ activity level should be adjusted by the amount of the increase, so

that total costs for the ‘high’ and ‘low’ amounts are the same.

The high/low method can then be used in the normal way to obtain a fixed cost and

a variable cost per unit. The fixed cost will be either the fixed cost at the ‘high’ level

or at the ‘low’ level, depending on how you made the adjustment to fixed costs

before making the high/low analysis. You can then calculate the fixed costs at the

Paper F5: Performance management

190 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

other level of activity by adding or subtracting the step change in fixed costs, as

appropriate.

Example

A company has the following costs at two activity levels.

Activity Total cost

units $

17,000 165,000

22,000 195,000

The variable cost per unit is constant over this range of activity, but there is a step

fixed cost and total fixed costs increase by $15,000 when activity level equals or

exceeds 19,000 units.

Required

Using high/low analysis, calculate the total cost of 20,000 units.

Answer

There is an increase in fixed costs above 19,000 units of activity, and to use the

high/low method, we need to make an adjustment for the step fixed costs. Since

we are required to calculate the total cost for a volume of activity above 19,000

units, the simplest approach is to add $15,000 to the total cost of 17,000 units, so

that the fixed costs of 17,000 units and 22,000 units are the same and are also the

amount of fixed costs for 20,000 units.

(1) Steps 1 and 2: Calculate the variable cost per unit

Units

$

High: Total cost 22,000 units

= 195,000

Low: Adjusted total cost: $(165,000 + 15,000) 17,000 units

= 180,000

Difference: Variable cost of 5,000 units

= 15,000

Therefore variable cost per unit = $15,000/5,000 units = $3 per unit.

(2) Steps 3 and 4: Calculate fixed costs (above 19,000 units)

Substitute in the ‘high’ equation Cost

$

Total cost of 22,000 units 195,000

Variable cost of 22,000 units (× $3 per unit) 66,000

Therefore fixed costs (above 19,000 units) 129,000

Chapter 8: Quantitative analysis in budgeting

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 191

(3) Using the cost analysis: Prepare a cost estimate

Cost estimate Cost

$

Fixed costs (above 19,000 units) 129,000

Variable cost (20,000 units × $3) 60,000

Estimated total costs 189,000

The step increase in fixed costs is given as a percentage amount

When the step change in fixed costs between two activity levels is given as a

percentage amount, the problem is a bit more complex, and to use high/low

analysis we need a third figure for total cost, at another level of activity somewhere

in between the ‘high’ and the ‘low’ amounts.

Total fixed costs will be the same for:

the ‘in between’ activity level and

either the ‘high’ or the ‘low’ activity level.

High/low analysis should be applied to the two costs and activity levels for which

total fixed costs are the same, to obtain an estimate for the variable cost per unit and

the total fixed costs at these activity levels. Total fixed costs at the third activity level

(above or below the step change in fixed costs) can then be calculated making a

suitable adjustment for the percentage change.

Example

A company has the following costs at three activity levels.

Activity Total cost

units $

5,000 180,000

8,000 240,000

11,000 276,000

The variable cost per unit is constant over this range of activity, but there is a step

fixed cost and total fixed costs increase by 20% when the activity level exceeds 7,500

units.

Required

Estimate the expected total cost when the activity level is 7,000 units.

Answer

There is an increase in fixed costs above 7,500 units of activity, which means that

total fixed costs and the variable cost per unit are the same for 8,000 units and 11,000

units of activity. These activity levels should be used to estimate the variable cost per

unit and total fixed costs.

Paper F5: Performance management

192 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

(1) Steps 1 and 2: Calculate the variable cost per unit

Units

$

High: Total cost 11,000 units

= 276,000

‘In-between’ 8,000 units

= 240,000

Difference: Variable cost of 3,000 units

= 36,000

Therefore variable cost per unit = $36,000/3,000 units = $12 per unit.

(2) Steps 3 and 4: Calculate fixed costs (above 7,500 units)

Substitute in the ‘high’ equation Cost

$

Total cost of 11,000 units 276,000

Variable cost of 11,000 units (× $12 per unit)

132,000

Therefore fixed costs (above 7,500 units) 144,000

(3) Calculate fixed costs at activity levels below 7,500 units

Fixed costs increase by 20% above 7,500 units.

Fixed costs above 7,500 units are therefore 120% of fixed costs below 7,500 units.

Fixed costs below 7,500 units are therefore: $144,000 × (11/120) = $120,000.

(Note: Make sure that you understand the adjustment here. We do not subtract 20%

from fixed costs above 7,500 units!)

(4) Using the cost analysis: Prepare a cost estimate

Cost estimate Cost

$

Fixed costs (below 7,500 units) 120,000

Variable cost (7,000 units × $12) 84,000

Estimated total costs 204,000

1.4 High/low analysis when there is a change in the variable cost per unit

High/low analysis can also be used when there is a change in the variable cost per

unit between the ‘high’ and the ‘low’ levels of activity. The same approach is needed

as for a step change in fixed costs, as described above.

When the change in the variable cost per unit is given as a percentage amount, a

third ‘in between’ estimate of costs should be used, and the variable cost per unit

will be the same for:

the ‘in between’ activity level and

either the ‘high’ or the ‘low’ activity level.

Chapter 8: Quantitative analysis in budgeting

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 193

High/low analysis may be applied to the two costs and activity levels for which

unit variable costs are the same, to obtain an estimate for the variable cost per unit

and the total fixed costs at these activity levels. The variable cost per unit at the third

activity level can then be calculated making a suitable adjustment for the percentage

change.

Example

A company has the following costs at three activity levels.

Activity Total cost

units $

20,000 300,000

25,000 320,000

30,000 356,000

The fixed costs are constant over this range of activity, but there is a 10% reduction

in the variable cost per unit above 24,000 units of activity. This reduction applies to

all units of activity, not just the additional units above 24,000.

Required

Estimate the expected total cost when the activity level is 22,000 units.

Answer

The variable cost per unit is the same for both 25,000 units and 30,000 units.

High/low analysis should therefore be applied to these activity levels.

(1) Calculate the variable cost per unit above 24,000 units

Units

$

High: Total cost 30,000 units

= 356,000

‘In-between’ 25,000 units = 320,000

Difference: Variable cost of 5,000 units

= 36,000

Therefore variable cost per unit = $36,000/5,000 units = $7.20 per unit.

(2) Calculate the variable cost per unit below 24,000 units

The variable cost per unit above 24,000 units is 90% of the cost below 24,000 units.

The variable cost per unit below 24,000 units is therefore (× 100/90) of the cost

above 24,000 units.

Variable cost per unit below 24,000 units = $7.20 × 100/90 = $8

Paper F5: Performance management

194 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

(3) Calculate fixed costs

Substitute in the ‘low’ equation Cost

$

Total cost of 20,000 units 300,000

Variable cost of 20,000 units (× $8 per unit) 160,000

Therefore fixed costs (above 7,500 units) 140,000

(4) Using the cost analysis: Prepare a cost estimate

Cost estimate for 22,000 units Cost

$

Fixed costs 140,000

Variable cost (22,000 units × $8) 176,000

Estimated total costs 316,000