ACCA F5 Performance Management - 2010 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

Chapter 8: Quantitative analysis in budgeting

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 215

5.2 The learning curve model

The learning effect can be measured mathematically, and shown as a learning curve.

This learning curve model was developed from actual observations and analysis in

the US aircraft industry.

The learning curve is measured as a percentage learning effect. For example, for a

particular task, there might be an 80% learning curve effect, or a 90% learning curve

effect, and so on.

The mathematical significance of a learning curve

When there is a b% learning curve for the manufacture of a product, this means that

when cumulative output of the product doubles, the average time to produce all the

units made so far (the cumulative total produced to date) is b% of what it was

before.

For example, when there is an 80% learning curve, the cumulative average time to

produce units of an item is 80% of what it was before, every time that output

doubles.

The cumulative average time per unit is the average time for all the units made

so far, from the first unit onwards.

This means, for example, that if an 80% learning curve applies, the average time

for the first two units is 80% of the average time for the first unit.

Similarly, the average time for the first four units is 80% of the average time for

the first two units.

Example

The time to make a new model of a sailing boat is 100 days. It has been established

that in the boat-building industry, there is an 80% learning curve.

Required: Calculate:

(a) the cumulative average time per unit for the first 2 units, first 4 units, first 8

units and first 16 units of the boat

(b) the total time required to make the first 2 units, the first 4 units, the first 8

units and the first 16 units

(c) the additional time required to make the second unit, the 3

rd

and 4

th

units,

units 5 – 8 and units 9 – 16.

Paper F5: Performance management

216 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Answer

Total units

(cumulative)

Cumulative

average time

per unit

Total time

for all

units

Incremental

time for

additional units

Average time

for additional

units

days days days days

1 100 100.00 100.00

2 (× 80%)

80 160.00 60.00 60.00

4 (× 80%)

64 256.00 96.00 48.00

8 (× 80%)

51.2 409.60 153.60 38.40

16 (× 80%)

40.96 655.36 245.76 30.72

Example

The first unit of a new model of machine took 1,600 hours to make. A 90% learning

curve applies. How much time would it take to make the first 32 units of this

machine?

Answer

Average time for the first 32 units = 1,600 hours × 90% × 90% × 90% × 90% × 90%

= 944.784 hours

Total time for the first 32 units = 32 × 944.784 hours = 30,233 hours.

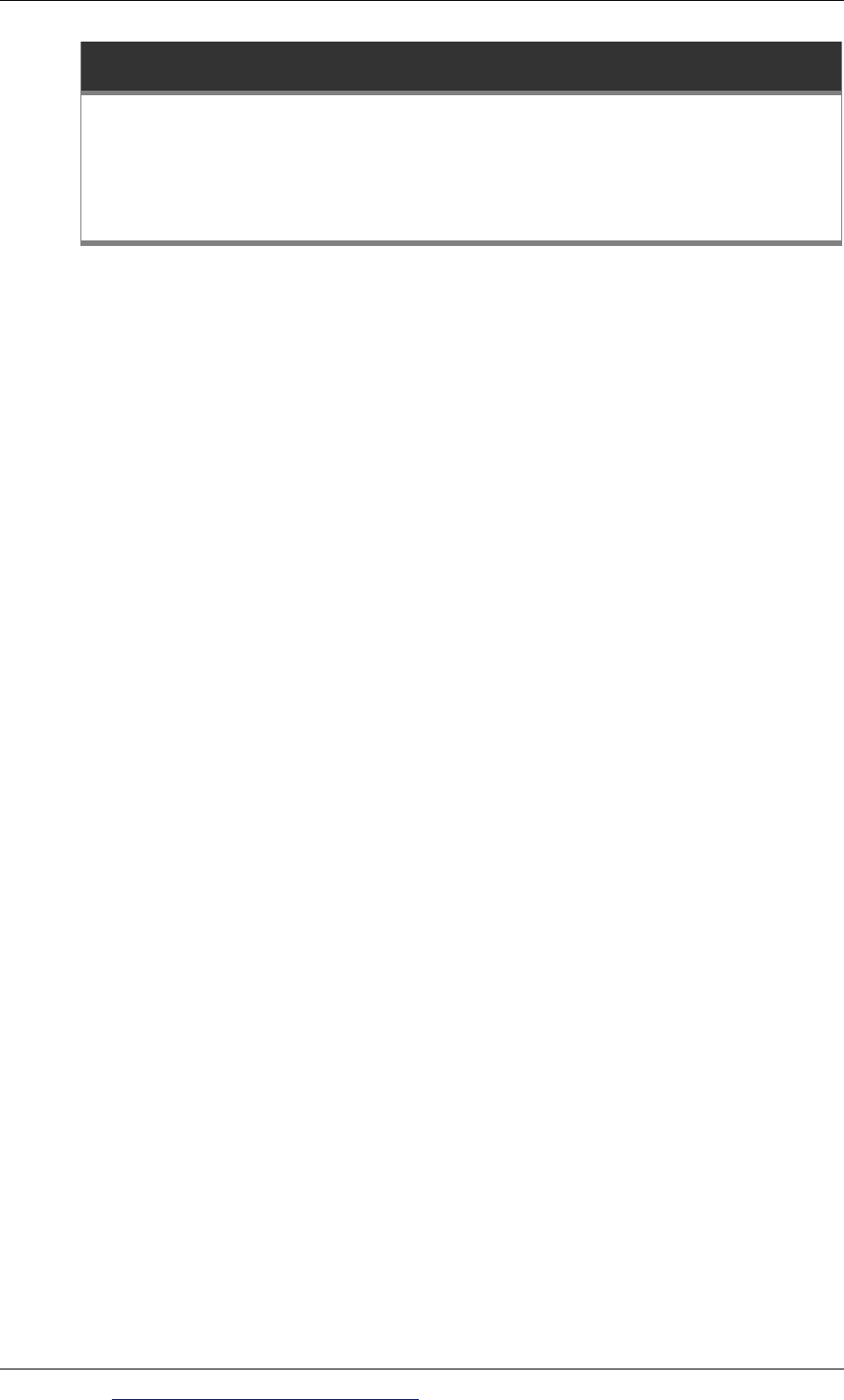

5.3 Graph of the learning curve

The learning curve can be shown as a graph. Two graphs are shown below.

The left-hand graph shows the cumulative average time per unit. This falls rapidly

at first, but the learning effect eventually ends and the average time for each

additional unit eventually becomes constant (a standard time).

The right hand graph shows how total costs increase. The total cost line is a curved

line initially, because of the learning effect.

Chapter 8: Quantitative analysis in budgeting

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 217

5.4 Formula for the learning curve

The learning curve is represented by the following formula (mathematical model):

Learning curve: y = ax

b

where

y = the cumulative average time per unit for all units made

x = the number of units made so far (cumulative number of units)

a = the time for the first unit

b = the learning factor.

This formula is given to you in the examination. You do not have to learn it, but you

must be able to use it.

The learning factor b =

Logarithm of learning rate

Logarithm of 2

The learning rate is expressed as a decimal, so if the learning curve is 80%, the

learning factor is: (logarithm 0.80/logarithm 2)

To use this formula you must be able to calculate logarithms. Make sure that your

calculator has a function for calculating logarithms (a ‘log’ button) and that you

know how to use it.

The logarithm of a number is the number expressed as a value to the power of 10.

For example the logarithm of 5 is 0.69897 because 5 is ten to the power 0.69897,

10

0.69897

.

The logarithm of 2 is 0.3010

The logarithm of 1 = 0.0000

The logarithm of a learning rate will always be a minus value, because the

learning is always less than 1 and its logarithm is less than 0.0000.

For example if the learning rate is 70%, the logarithm of 0.70 is – 0.1549, and

10

– 0.1549

is the same as 1/10

0.1549

.

Example

If there is an 80% learning curve, the learning factor is calculated as follows:

Logarithm 0.80

Logarithm 2

=

− 0.09691

0.30103

=−0.32193

The learning curve formula is therefore: y = ax

- 0.32193

It might help to remember that x

- 0.32913

is another way of writing

0.32193

x

1

Paper F5: Performance management

218 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Going back to the previous example, if the first unit takes 100 days and an 80%

learning curve applies, the cumulative average time to produce the first 8 units can

be calculated as:

0.32193

8

1

100 y ×=

= 100 (0.512)

= 51.20 days

Example

It will take 500 hours to complete the first unit of a new product. There is a 95%

learning curve effect.

Calculate how long it will take to produce the 7

th

unit.

Answer

The time to produce the seventh unit is the difference between:

the total time to produce the first 6 units, and

the total time to produce the first 7 units.

(1) Learning factor

Logarithm 0.95

Logarithm 2

=

− 0.02227639

0.30103

=−0.074

(2) Average time to produce the first 6 units

0.074

6

1

500 y ×=

= 500 (0.8758239)

= 437.9 hours per unit

(3)

Average time to produce the first 7 units

0.074

7

1

500 y ×=

= 500 (0.86589)

= 432.9 hours per unit

Chapter 8: Quantitative analysis in budgeting

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 219

(4) Time to produce the 7

th

unit

Hours

Total time for the first 7 units (7 × 432.9)

3,030.3

Total time for the first 6 units (6 × 437.9)

2,627.4

Time for the 7th unit 402.9

5.5 Conditions for the learning curve to apply

The learning curve effect will only apply in the following conditions:

There must be stable conditions for the work, so that learning can take place. For

example, labour turnover must not be high; otherwise the learning effect is lost.

The time between making each subsequent unit must not be long; otherwise the

learning effect is lost because employees will forget what they did before.

The activity must be labour-intensive, so that learning will affect the time to

complete the work.

There must be no change in production techniques, which would require the

learning process to start again from the beginning.

Employees must be motivated to learn.

The costs that are reduced as a result of the learning curve are those that vary with

labour time – labour costs and any overhead costs that vary with labour time. The

learning effect will not usually result in reductions in materials costs, for example,

because the usage of materials (ignoring losses through wastage) is not related to

labour efficiency.

Problems with using the learning curve

In practice, the learning curve effect is not used extensively for budgeting or

estimating costs (or calculating sales prices on a cost plus basis).

In a modern manufacturing environment production is highly mechanised and

therefore the learning curve effect does not apply.

For many products where skilled labour is required, production might have

reached a ’steady state’ so that there will be no further reductions in the average

times to produce the item.

Even with skilled, labour-intensive work, if there is a high rate of labour

turnover, the work force might not gain enough collective experience for a

learning effect to apply.

Paper F5: Performance management

220 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Other aspects of quantitative analysis in budgeting

Expected values (EVs) in budgeting

Spreadsheets in budgeting

Spreadsheets and ‘what if’ analysis

Dangers with using spreadsheets for budgeting

6 Other aspects of quantitative analysis in budgeting

6.1 Expected values (EVs) in budgeting

Just as expected values might be used in accounting for short-term decisions, they

might also be used in budgeting. An expected value is a weighted average value of

probable outcomes, where the likelihood of each different possible outcome can be

estimated as a probability.

Expected values can be a reliable basis for making estimates, where an outcome will

occur many times, and the EV becomes an estimate of the average. For example,

expected values might be used to estimate the average number of rejected items

from a process, or the average loss from a process.

Expected values are much less reliable as estimates for events or outcomes that will

happen only once (or a limited number of times) during the budget period. For

example, a budget estimate of sales volume for the period might be a 20%

probability of sales of $5,000,000, a 50% probability of $6,000,000 and a 30%

probability of $9,000,000. The expected value of sales would be $6,700,000 (0.20 ×

$5m + 0.50 × $6m + 0.30 × $9m).

However, this volume of sales is not one of the probable outcomes and is therefore

not expected to occur. Preparing a budget on the basis of expected sales of

$6,700,000 would therefore be inappropriate. It would possibly make more sense to

prepare a budget on the basis of the most likely sales ($6 million), and possible also

to prepare flexible budgets for sales of $5 million and $9 million).

The problems of using EVs for budgeting are therefore the same as the problems

with using EVs for short-term decision-making, as explained in an earlier chapter.

6.2 Spreadsheets in budgeting

Spreadsheets are used extensively in budgeting, because long and detailed

calculations can be made very quickly, and the same basic model can be used from

one year to the next. Examples of applications of spreadsheets in management

accounting include:

Preparing forecasts of sales, and forecasts of profit or loss

Cost estimation using linear regression analysis and the calculation of a

correlation coefficient and coefficient of determination

Chapter 8: Quantitative analysis in budgeting

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 221

Preparing financial plans, such as budgets

Comparing actual results with a plan or budget (control reporting).

Example

Here is a very simple example of a simple accounting calculation entered as text,

numbers and formulae in a spreadsheet.

Column C D

E F

Row

1

st

6 months

2

nd

6 months Year

4 Output (units) 10,000

15,000 = D4+E4

5 $

$ $

6 Variable costs =D4*F11

=E*F11 =D6+E6

7 Fixed costs 40,000

=D7 =D7+E7

8 Total costs =D6+D7

=E6+E7 =D8+E8

9

10 Average cost/unit =D8/D4

=E8/E4 =F8/F4

11 Variable cost/unit

3.00

This would appear on screen as follows:

Column C D

E F

Row

1

st

6 months

2

nd

6 months Year

4 Output (units) 10,000

15,000 25,000

5 $

$ $

6 Variable costs 30,000

45,000 75,000

7 Fixed costs 40,000

40,000 80,000

8 Total costs 70,000

85,000 155,000

9

10 Average cost/unit 7.00

5.67 6.20

11 Variable cost/unit

3.00

The figures can be re-calculated using different figures for output in each half of the

year, or different figures for fixed costs or the unit variable costs. All that is required

is an alteration to the number in cells D4, E4, D7 or F11.

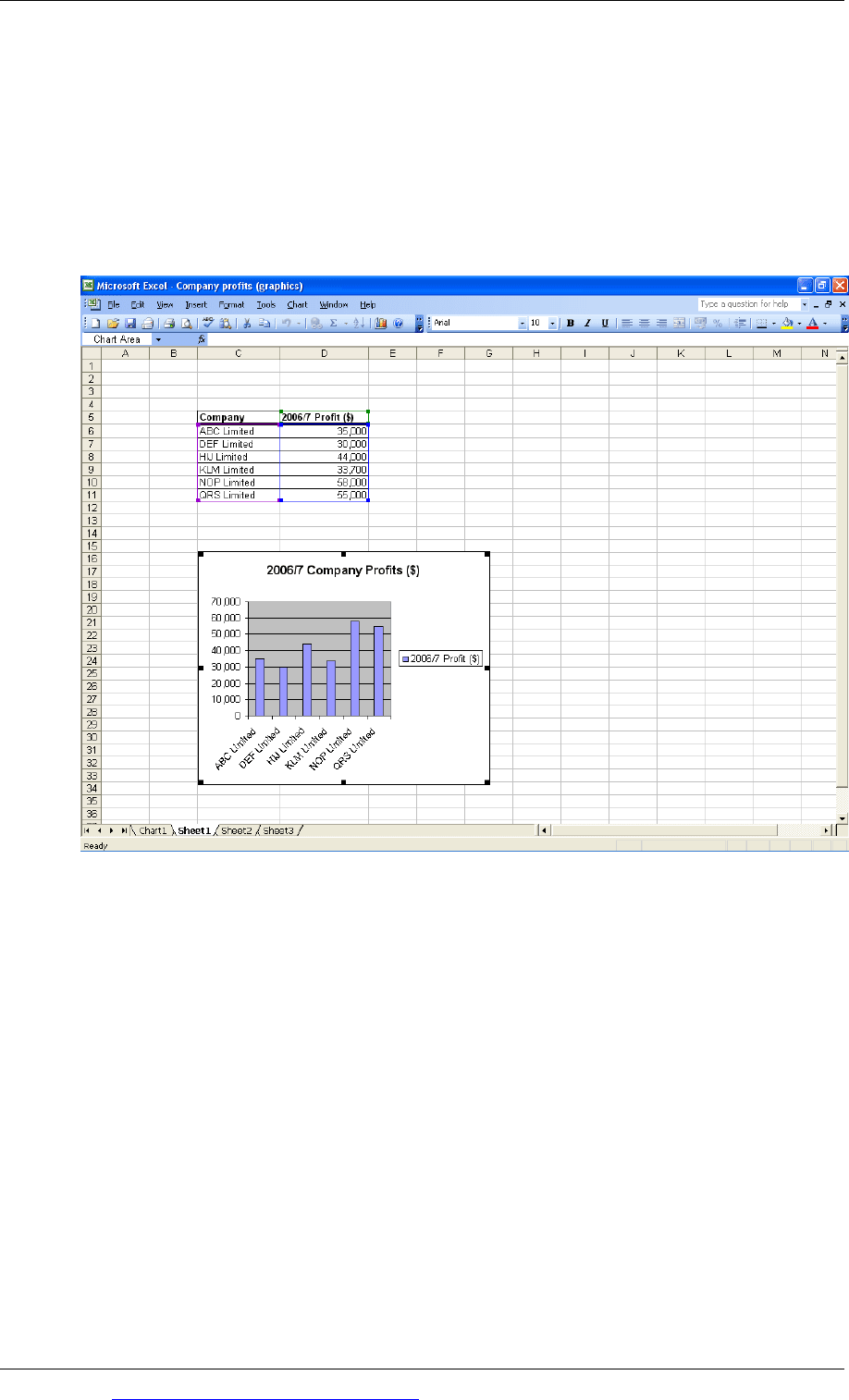

Graphical reproduction of spreadsheet data

The figures in a spreadsheet can be converted by the spreadsheet program into

graphical display format, and shown as graphs, bar charts or pie charts. This facility

can also be very useful for the preparation of management reports.

Paper F5: Performance management

222 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

For example, if a spreadsheet is used for linear regression analysis, it can be used to

show the line of best fit as a graph. Similarly, if a spreadsheet is used to prepare an

estimate of costs, the percentage of total costs made up by different items of cost

(direct materials, direct labour, production overheads etc) can be shown as a pie

chart or a bar chart.

The example below shows how the profits for six different companies can be shown

in the form of a graph using the ‘Chart Wizard’ facility in Microsoft Excel

6.3 Spreadsheets and ‘what if’ analysis

A useful feature of spreadsheets is the ability to carry out sensitivity analysis easily

and quickly. Each analysis of the sensitivity of the outcome to changes in a key

variable can be made quickly, by amending one or two items in the spreadsheet. A

task that could take hours if done by hand can be finished in a few minutes, or even

seconds, using a spreadsheet.

If a spreadsheet is used to prepare a budget, by changing some key assumptions

and seeing what happens to the profit, sensitivity analysis would provide

management with information about the sensitivity of the budget to changes in

different assumptions about unit costs, sales volumes or selling prices.

For example a budget in a spreadsheet model can be re-calculated changing the

assumption about sales volume from, say, ‘50,000 units in month 1 and rising by

1,000 units each month’ to ’48,000 units in month 1 and rising by 800 units in each

month’. This would need amendments to just two cells in the spreadsheet.

Chapter 8: Quantitative analysis in budgeting

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 223

6.4 Dangers with using spreadsheets for budgeting

Although spreadsheets are used extensively for budgeting, there are some common

problems (‘dangers’) with using them.

It can be easy to forget the assumptions on which a spreadsheet model is based.

A spreadsheet model might even be so large and complex that its users do not

know or do not understand the assumptions on which the model is based. It is

dangerous to use models without knowing ‘how the model works’.

Because it is so easy to make changes to a spreadsheet model for a budget and

produce a new version of a budget, there is a danger that a large number of

different versions of a budget might be produced, and managers might get

confused about which is the ‘official’ version.

Paper F5: Performance management

224 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP