ACCA F2 Management Accounting - 2010 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 125

Paper F2

Management Accounting

CHAPTER

6

Accounting for overheads

Contents

1 Definitionandpurposeofabsorptioncosting

2 Stagesinabsorptioncosting

3 Overheadapportionment

4 Apportionmentofservice departmentcosts

5 Overheadabsorption

6 Underabsorbedandoverabsorbedoverheads

7 Fixedandvariableoverheads

Paper F2: Management accounting

126 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Definition and purpose of absorption costing

Introduction to absorption costing

The treatment of direct and indirect expenses

Definition of absorption costing

The purpose of absorption costing

1 Definition and purpose of absorption costing

1.1 Introduction to absorption costing

This chapter describes the basic principles and methods of absorption costing.

Absorption costing is a method of costing in which overhead costs are added to the

cost of cost units, and a ‘full cost’ is calculated. The full cost of an item is the prime

cost plus a share of overhead costs.

The absorption costing method can be used in either manufacturing industries or

service industries, but it is more commonly associated with costing for

manufacturing. This is because in manufacturing there are usually large quantities

of inventory, and work-in-progress and finished goods are normally valued (or

‘costed’) to include some production overhead costs.

The absorption costing method therefore focuses mainly on production costs and

the treatment of production overheads.

1.2 The treatment of direct and indirect expenses

In cost accounting, direct and indirect costs are treated differently.

Direct costs are charged directly to the cost of production. They are directly

identified with cost units, batches of production, a production process or a job or

a contract.

Overheads are indirect costs, and cannot be identified directly with specific cost

units, jobs or processes etc. They are therefore recorded as overhead costs, and a

distinction is made between production overheads, administration overheads

and sales and distribution (marketing) overheads.

Overhead costs can then be treated in either of two ways.

Method 1 – Marginal costing. They might be treated as period costs, and

charged as an expense against the period in which they are incurred, without

any attempt to add a share of the overhead costs to the cost of units of

production.

Method 2 – Absorption costing. They might be shared out between cost units or

processes. Overhead costs might be charged to cost units in addition to direct

costs, so that the cost of goods sold (the cost of cost units) includes a fair share of

overhead costs.

Chapter 6: Accounting for overheads

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 127

$ per unit

Direct material costs A

Direct production labour cost B

Production overheads C

Full production cost

(A + B + C) = D

Administration overhead E

Sales and distribution overhead F

Full cost of sale

D + E + F

This chapter deals with absorption costing. In absorption costing, a share of

overhead costs is added to direct costs, to obtain a ‘full cost’ or a ‘fully absorbed

cost’ for cost units. This chapter explains the methods that are used to calculate the

amount of overhead costs to add to unit costs in order to obtain a full cost per unit.

Marginal costing is explained in a later chapter.

1.3 Definition of absorption costing

Absorption costing is based on the idea that the cost of a product or a service should

be:

its direct costs (direct materials, direct labour and sometimes direct expenses)

plus a share of overhead costs.

Absorption costing is therefore a system of costing in which a share of overhead

costs is added to direct costs, to obtain a full cost. This might be:

a full production cost, or

a full cost of sale.

An absorption costing system might be used to decide the full production cost of

the product, so that only a share of production overheads is added to product costs.

Administration overheads and selling and distribution overheads are simply

charged as an expense to the period in which they occur.

Income statement: absorption costing

$000 $000 $000

Sales 950

Cost of inventory at the beginning of the period 80

Production cost of items manufactured in the period:

Direct materials 280

Direct labour 120

Direct expenses (if any) 0

Production overhead added to cost (‘absorbed’) 240

640

720

Less: Cost of inventory at the end of the period (120)

Production cost of items sold 600

Gross profit 350

Administration overhead 100

Selling and distribution overhead 200

300

Net operating profit 50

Paper F2: Management accounting

128 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Inventory valuation is an important feature of absorption costing, because the cost

of production in any period depends partly on the valuation of opening and closing

inventory, including work-in-progress and finished goods inventory.

In some costing systems, a share of administration overhead and selling and

distribution overhead might be added to the full production cost, to obtain a full

cost of sale. However, it is not common practice to calculate a full cost of sale,

because it has only limited value as management information.

1.4 The purpose of absorption costing

There are several reasons why absorption costing is sometimes used, and

production overhead costs are added to direct costs to calculate the full production

cost of products (or services).

There is a view that inventory should include a fair share of production

overhead cost. This view is applied in financial accounting and financial

reporting. It can therefore be argued that inventory should be valued in a similar

way in the cost accounting system. (However, inventory valuations may differ

between the cost accounts and the financial accounts.)

There is also a view that in order to assess the profitability of products or

services, it is appropriate to charge products and services with a fair share of

overhead costs. Unless products contribute sufficiently to covering indirect costs,

its ‘profitability’ might be too low, and the business as a whole might not be

profitable.

Criticisms of absorption costing

There are criticisms of absorption costing. The main criticisms are as follows:

Absorption costing does not provide reliable information about profitability.

Methods of charging overhead costs to products, as we shall see, are not

‘scientific’, and rely on fairly arbitrary assumptions.

There are better methods of measuring profitability, such as marginal costing.

There are also better ways of providing cost information to help managers make

decisions (relevant costs). Marginal costing and relevant costs are explained in

later chapters.

When absorption costing was first used in manufacturing, well over 100 years ago,

total overhead costs were fairly small compared with direct costs. Manufacturing

was labour-intensive, and direct labour costs were a significant proportion of total

costs. Adding a share of overheads to product costs, usually in proportion to the

cost of direct labour or direct labour time, was therefore a reasonable method of

dealing with overhead costs.

In a modern manufacturing environment, however, direct labour is a fairly small

proportion of total costs. Most work in production now consists of the ‘support’

activities of indirect labour employees, and the cost of this labour is an overhead

cost. Overhead costs are high compared to direct labour costs. As a consequence, it

is often argued that a costing system should use a different approach to overhead

costing, and try to present overhead costs in a way that is more useful to

Chapter 6: Accounting for overheads

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 129

management for information purposes. One such technique, activity based costing,

is outside the scope of the syllabus.

Paper F2: Management accounting

130 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Stages in absorption costing

Cost centres and general expenses

Allocation, apportionment and absorption (recovery)

Overhead cost allocation

2 Stages in absorption costing

2.1 Cost centres and general expenses

In a system of absorption costing, each item of overhead cost is charged either:

to a cost centre, or

as a general expense.

The cost centres might be:

a cost centre in the production function (production overhead)

a cost centre in administration (= administration overhead)

a cost centre in sales and distribution (= sales and distribution overhead).

The cost centres in the production function might be:

a department engaged directly in production work (a production department), or

a department or service section engaged in support activities, such as inventory

management, production planning and control, quality control, repairs and

maintenance, and so on (= ‘service departments’).

In a system of absorption costing, overheads are charged to products or services on

the basis of this structure of cost centres and general expenses.

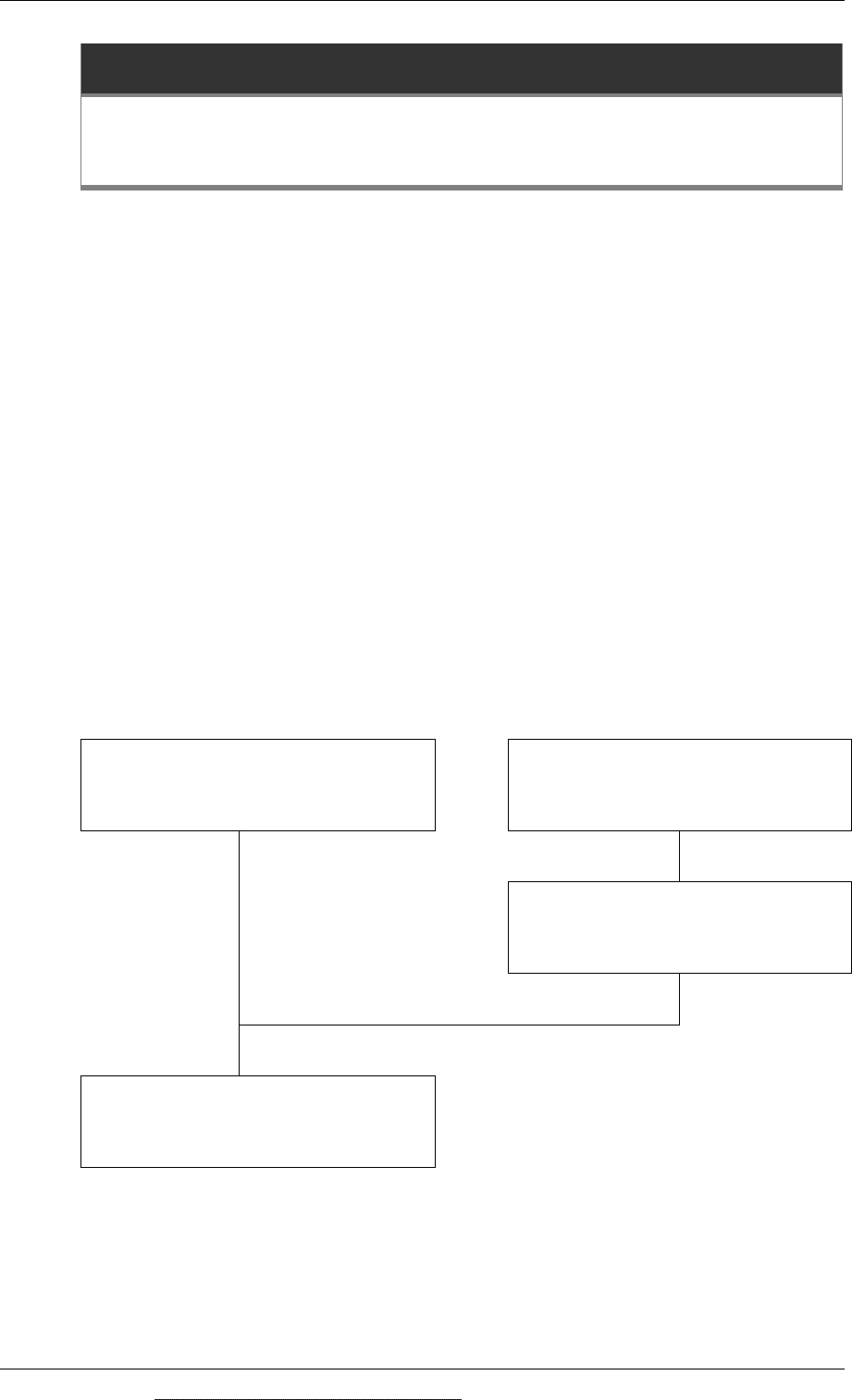

2.2 Allocation, apportionment and absorption (recovery)

There are three main stages in absorption costing for charging overhead costs to the

cost of production and cost units:

Allocation. Overheads are allocated to cost centres. If a cost centre is responsible

for the entire cost of an item of expenditure, the entire cost is charged directly to

the cost centre.

Apportionment. Many overhead costs are costs that cannot be allocated directly

to one cost centre, because they are shared by two or more cost centres. These

costs are apportioned between the cost centres. ‘Apportionment’ means sharing

on a fair basis.

Absorption (also called overhead ‘recovery’). When overheads have been

allocated and apportioned to production cost centres, they are charged to the

cost of products manufactured in the cost centre. The method of charging

Chapter 6: Accounting for overheads

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 131

overheads to cost units is to establish a charging rate (an absorption rate or

recovery rate) and to apply this rate to all items of production.

Allocation

Overhead costs are recorded. Initially

they are allocated to a cost centre or

recorded as a general expense

Apportionment

Overhead costs are shared between the

departments or activities that benefit

from them

Absorption

(Overhead recovery)

Overheads are added to the cost of cost

units, using a fair basis for charging

(absorption costing only)

2.3 Overhead cost allocation

Many items of indirect cost cannot be charged directly to a cost unit (a unit of

product or service), but they can be charged directly to a cost centre (for example, a

department or work group). Items of expense that can be identified with a specific

cost centre should be charged in full as a cost to the cost centre. The process of

charging costs directly to cost centres is called cost allocation.

In absorption costing for a manufacturing company, overhead costs may be

allocated to:

production departments or production centres: these are cost centres that are

directly engaged in manufacturing the products

service departments or service centres: these are cost centres that provide

support to the production departments, but are not directly engaged in

production, such as engineering, repairs and maintenance, the production stores

and materials handling department (raw materials inventory), production

planning and control, and so on

administration departments

selling departments and distribution departments.

Production overheads are the overhead costs of both the production departments

and the service departments.

Overhead costs that cannot be directly allocated to a cost centre must be shared

(apportioned) between two or more cost centres.

For example:

The salary of the manager of the production planning department can be

allocated directly as a cost of the production planning cost centre, which is a

service department cost centre within production.

Paper F2: Management accounting

132 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Similarly the rental cost of equipment used by engineers in the maintenance

department can be allocated directly as a cost of the maintenance department,

which is also a service department cost centre within production.

If the machining department has its own electricity power supply, electricity

charges for the machining department can be allocated directly to the

department, which is a production department cost centre.

The salary of a supervisor in the finishing department can be allocated directly

to the finishing department, which is also a production department cost centre.

The cost of security guards for the manufacturing site cannot be allocated to any

specific department or cost centre; therefore security guard services are likely to

be recorded as a general production overhead expense, and the cost is allocated

to ‘security services’.

Chapter 6: Accounting for overheads

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 133

Overhead apportionment

The apportionment of shared costs between cost centres

The basis of apportionment

3 Overhead apportionment

3.1 The apportionment of shared costs between cost centres

Some costs cannot be allocated in full to a cost centre, because they are shared by

two or more cost centres. These are divided between the cost centres on a fair basis.

The process of dividing the shared costs is called apportionment.

Shared costs may be divided between administration cost centres and selling and

distribution cost centres, as well as production centres and service centres.

However, examination questions on absorption costing will usually concentrate on

production overhead costs.

The apportionment of production overhead costs might be in two stages:

sharing (or dividing) general costs between production centres and service

centres

then sharing the costs of the service centres between the production centres.

Production overhead costs allocated

and apportioned to direct

production departments

Production overhead costs

allocated and apportioned to

service departments

Service department overheads

apportioned to direct production

departments

All production overheads now

allocated or apportioned to direct

production departments

After this has been done, all the production overhead costs have been allocated or

apportioned to the production centres. The total overhead costs of each production

centre should be:

(1) costs allocated directly to the production centre, plus

(2) shared costs apportioned to the production centre, plus

Paper F2: Management accounting

134 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

(3) a share of the costs of each service department, apportioned to the production

centre.

3.2 The basis of apportionment

Shared overhead costs should be apportioned on a fair basis between cost centres.

For each item of shared expense, a ‘fair’ basis for apportionment must be selected.

Choosing the basis of apportionment for each cost is a matter of judgement, but

there is often an ‘obvious’ basis to choose. For example, the rental cost of a building

and the insurance costs for the building will be apportioned between the cost

centres that use the building. The basis of apportionment will probably be to share

the costs in relation to the floor space used by each cost centre.

In some cases, however, it might not be clear what the most suitable basis of

apportionment should be, and the choice is then simply a matter of judgement and

preference.

At the end of the apportionment process, all overhead costs should be allocated or

apportioned to a cost centre.

Example: apportionment of shared costs

A manufacturing company has two production departments, Machining and

Assembly, and two service departments, Repairs and Quality Control. The following

information is available about production overhead costs.

Total

Machining

Assembly

Repairs

Quality

control

$ $ $ $ $

Indirect labour cost 15,500

5,000

5,000

3,500 2,000

Indirect materials 5,300

1,500

2,400

1,000 400

Factory rental 14,400

Power costs 4,800

Depreciation (note 1) 14,000

Building insurance 1,800

Equipment insurance 4,200

60,000

Note: Depreciation is a charge for the use of items of plant and equipment, such as

machinery.

Indirect labour and indirect material costs have been allocated directly to these four

cost centres. The other overhead costs are shared between the cost centres and so

cannot be allocated directly.

Other information

Total

Machining

Assembly

Repairs

Quality

control

Cost of plant/equipment ($) 70,000 40,000 15,000 5,000 10,000

Floor area (square metres) 1,800

500

900

100 300

Kilowatt hours (000s) 800

600

100

50 50