ACCA F2 Management Accounting - 2010 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

Answers to practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 445

31 Current year and next year

(a) Contribution/sales ratio = 60%

Therefore variable costs/sales ratio = 40%.

Variable cost per unit = $20

Therefore sales price per unit = $20/0.40 = $50.

Contribution per unit = $50 – $20 = $30.

$

Budgeted contribution (8,000 × $30) 240,000

Budgeted fixed costs (8,000 × $25) 200,000

Budgeted profit, current year 40,000

(b) Sales price next year = $50 × 1.06 = $53 per unit

Variable cost per unit next year = $20 × 1.05 = $21

Therefore contribution per unit next year = $53 – $21 = $32

$

Target profit next year 40,000

Fixed costs next year (200,000 × 1.10) 220,000

Target contribution for same profit as in the current year 260,000

Therefore target sales next year = $260,000/$32 per unit = 8,125 units.

32 CVP

(a) Break-even point = $48,000/0.40 = $120,000 (sales revenue).

Margin of safety (in sales revenue) = $140,000 – $120,000 = $20,000.

Selling price per unit = $10.

Margin of safety (in units) = $20,000/$10 = 2,000 units.

(b) (i) The margin of safety is 6.25%. Therefore the break-even volume of sales

= 93.75% of budgeted sales = 0.9375 × $128,000 = $120,000

Budget

Break-

even

$

$

Sales 128,000

120,000

Profit 2,000

0

Total costs 126,000

120,000

This gives us the information to calculate fixed and variable costs, using

high/low analysis.

$

Revenue

$ Cost

High: Total cost at 128,000

=

126,000

Low: Total cost at 120,000

=

120,000

Difference: Variable cost of 8,000

=

6,000

Paper F2: Management accounting

446 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Therefore variable costs = $6,000/$8,000 = 0.75 or 75% of sales revenue.

Substitute in high or low equation Cost

$

Total cost at $128,000 revenue 126,000

Variable cost at $128,000 revenue (× 0.75) 96,000

Therefore fixed costs 30,000

(ii) At sales of $128,000, profit is $2,000.

The contribution/sales ratio = 100% – 75% = 25% or 0.25.

To increase profit by $3,000 to $5,000 each month, the increase in sales

must be:

(Increase in profit and contribution) ÷ C/S ratio

= $3,000/0.25

= $12,000.

Sales must increase from $128,000 (by $12,000) to $140,000 each month.

Alternative approach to the answer

$

Target profit 5,000

Fixed costs 30,000

Target contribution 35,000

C/S ratio 0.25

Therefore sales required ($35,000/0.25) $140,000

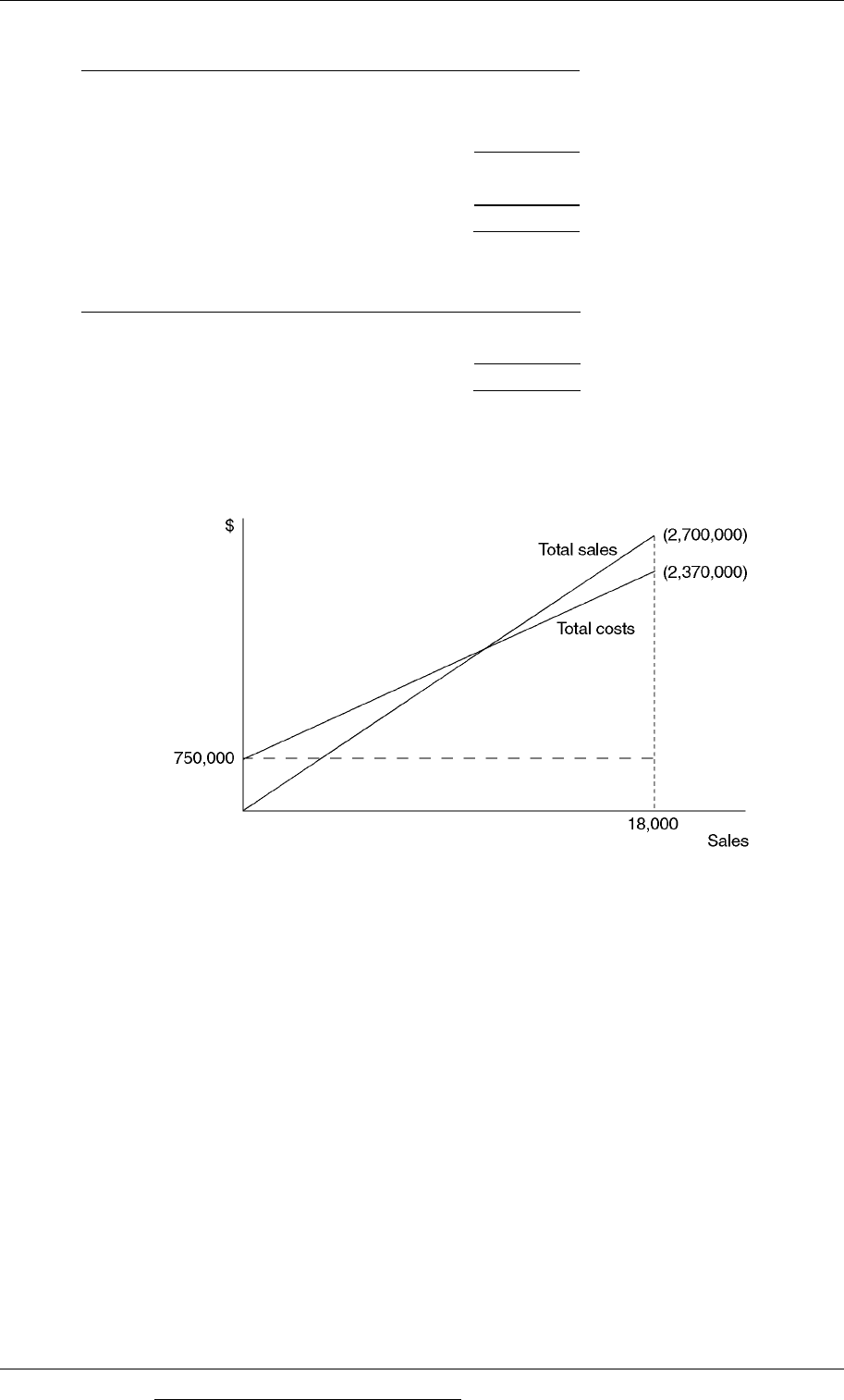

33 Break-even

Workings

Sales

Sales

(at $150)

Profit

units

$

$

18,000

2,700,000

(30,000)

12,000

1,800,000

330,000

Difference 6,000

900,000

360,000

An increase in sales from 12,000 units to 18,000 units results in an increase of

$900,000 in revenue and $360,000 in contribution and profit.

From this, we can calculate that the contribution is $60 per unit ($360,000/6,000) and

the C/S ratio is 0.40 ($360,000/$900,000). Variable costs are therefore 0.6 or 60% of

sales.

To draw a break-even chart, we need to know the fixed costs.

Answers to practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 447

Substitute in high or low equation

When sales are 18,000 units: $

Sales (at $150 each) 2,700,000

Variable cost (sales × 60%)

1,620,000

Contribution (sales × 40%)

1,080,000

Profit 330,000

Therefore fixed costs 750,000

When sales are 18,000 units: $

Fixed costs 750,000

Variable cost (see above) 1,620,000

Total costs 2,370,000

There is now enough information to draw a break-even chart.

(a)

(b) Break-even point = Fixed costs ÷ C/S ratio

= $750,000/0.40 = $1,875,000

Break-even point in units = $1,875,000/$150 per unit = 12,500 units.

If budgeted sales are 15,000 units, the margin of safety is 2,500 units (15,000 –

12,500).

This is 1/6 or 16.7% of the budgeted sales volume.

34 Machine

Relevant cost = Difference between sale value now and sale value if it is used. This

is the relevant cost of using the machine for the project.

Relevant cost = $17,500 - $10,000 = $7,500.

Paper F2: Management accounting

448 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

35 Relevant cost of labour

A total of 900 hours would have to be found by either working overtime at a cost of

$15 × 150% = $22.50 per hour, or diverting labour from other work that earns a

contribution of $5 per hour after labour costs of $15 per hour. The opportunity cost

of diverting labour from other work is therefore $20 per hour. This is less than the

cost of working overtime. If the contract is undertaken, labour will therefore be

diverted from the other work.

It is assumed that the 500 hours of free labour time (idle time) available would be

paid for anyway, even if the contract is not undertaken. The relevant cost of these

hours is therefore $0.

Relevant cost of labour

$

500 hours 0

900 hours (× $20) 18,000

Total relevant cost of labour 18,000

36 Domco

(a) 100% capacity each month = 112,000 units/0.80 = 140,000 units.

Using high/low analysis:

units

$

High: Total cost of 140,000

= 695,000

Low: Total cost of 112,000

= 611,000

Difference: Variable cost of 28,000

= 84,000

Therefore variable cost per unit = $84,000/28,000 units = $3.

Substitute in high equation Cost

$

Total cost of 140,000 units 695,000

Variable cost of 140,000 units (× $3) 420,000

Therefore fixed costs per month 275,000

(b)

Contribution/sales ratio = 60%

Therefore variable cost/sales ratio = 40%

The normal sales price per unit = $3/0.40 = $7.50

The contribution per unit at the normal selling price is $7.50 – $3 = $4.50 per

unit.

(c)

If the customer’s offer is accepted, the sales price for the 25,000 units will be

$7.50 – 20% = $6 per unit.

The contribution per unit for these units will be $6 – $3 = $3.

Answers to practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 449

The reduction in monthly sales at the normal price will be 1/5 × 25,000 = 5,000

units.

$

Increase in contribution from 25,000 units sold (25,000 × $3) 75,000

Loss of contribution from fall in other sales (5,000 × $4.50) 22,500

Net increase in profit each month 52,500

By accepting the new customer’s offer, the profit would increase by $52,500

each month. The offer should therefore be accepted.

37 Limiting factors

A B C D

$ $ $ $

Sales price 100

110

120 120

Variable cost per litre

54

55

59

66

Contribution per litre

46

55

61

54

Direct labour hours/unit 3

2.5

4 4.5

Contribution /direct labour hour $15.33

$22

$15.25 $12

Priority for manufacture/sale

2

nd

1

st

3

rd

4

th

The fixed overhead absorption rate is $8 per hour. This can be calculated from the

overhead cost and direct labour hours for any of the four products.

The budgeted labour hours for calculating this absorption rate was 1,600 hours,

therefore budgeted fixed costs are 1,600 hours × $8 = $12,800.

The output and sales that will maximise contribution and profit is as follows.

Product Litres Hours Contribution/litre Contribution/profit

$ $

B 150.0

375

55

8,250.0

A 200.0

600

46

9,200.0

C (balance) 92.5

370

61

5,642.5

1,345

23,092.5

Fixed costs (see above)

12,800.0

Profit

10,292.5

38 Proglin

Let the number of units of Mark 1 be x

Let the number of units of Mark 2 be y.

The objective function is to maximise total contribution: 10x + 15y.

Subject to the following constraints:

Direct materials 2x + 4y ≤

24,000

Direct labour 3x + 2y ≤

18,000

Sales demand, Mark 1 x ≤

5,000

Non-negativity x, y ≥

0

Paper F2: Management accounting

450 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

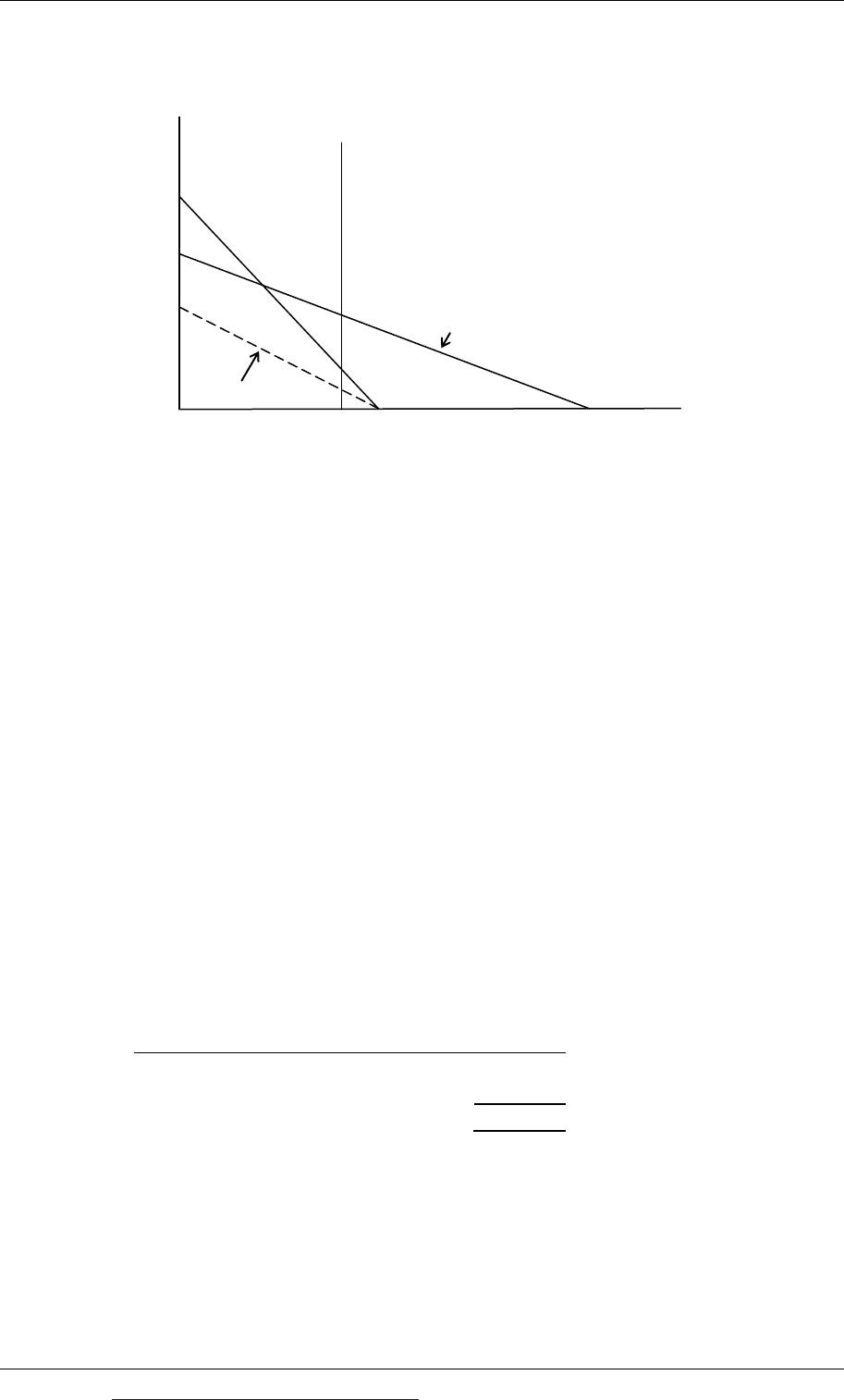

These constraints are shown in the graph below. The graph also shows an iso-

contribution line 10x + 15y = 60,000.

9000

6000

4000

0

3x + 2y = 18000

A

B

$

X = 5000

6000 5000

C

D

10x + 15y = 60,000

2x + 4y = 24000

12000

The feasible solutions are shown by the area 0ABCD in the graph.

Using the slope of the iso-contribution line, it can be seen that contribution is

maximised at point B on the graph.

At point B, we have the following simultaneous equations:

(1)

2x + 4y = 24,000

(2) 3x + 2y = 18,000

Multiply (2) by 2

(3) 6x + 4y = 36,000

Subtract (1) from (3)

4x = 12,000

Therefore x = 3,000

Substitute in equation (1)

2 (3,000) + 4y = 24,000

4y = 18,000

y = 4,500

The objective in this problem is to maximise 10x + 15y.

The total contribution where x = 3,000 and y = 4,500 is as follows

$

3,000 units of Mark 1 (× $10) 30,000

4,500 units of Mark 2 (× $15) 67,500

Total contribution 97,500

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 451

Paper F2

Management accounting

i

Index

A

Abnormal loss 208

Abnormal loss and loss with a scrap value 210

Absorbed production overheads:

cost ledger 173

Absorption 130

Absorption costing: 126, 184

advantages and disadvantages 190

criticisms 128

definition 127

purpose 128

Absorption rate 144

Accounting for abnormal gain 213

Accounting for abnormal loss 209

Accounting for labour costs 112

Accounting for normal loss: 206

cost ledger 207

Accounts in the cost ledger 162

Administration costs 27

Adverse variances 262

Allocation 130

Apportioning common processing costs 234

Apportionment 130, 133

Avoidable and unavoidable costs 324

B

Balance on an account 163

Basis of apportionment 134

Batch costing 197

Batch production 102, 197

Bin card 90

Break-even analysis 312

Break-even chart 317

Break-even point 312

Budget: 149, 240

committee 241

manual 241

period 240

process 243

Budgetary control 241, 252

Budgeting 240

Budgeting with one limiting factor 343

By-products 235

C

C/S ratio 309

Capacity utilisation ratio 118

Capacity variance 280

Closing inventory 168

Coefficient of determination r2 78

Composite cost units 200

Computerised inventory control system 90

Constraints 347

Constraints on a graph 351

Contribution 180, 307, 309

Contribution forgone 330

Contribution per unit 181

Paper F2: Management accounting

452 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Contribution/sales ratio 309

Control 14

Conversion costs 204

Correlation 74

Correlation coefficient r 77

Cost accounting 20

Cost accounting income statement 176

Cost and management accounting 22

Cost behaviour 42

Cost behaviour graph 46, 43

Cost centre 17, 39, 130

Cost estimation 49

Cost ledger 162

Cost ledger control account 170

Cost object 38

Cost of sales account 175

Cost unit 38

Cost variances 262

Costing system income statement 168

Costs of production and the WIP account 164

Cost-volume-profit analysis 306

Credit 163

CVP analysis 306

D

Data 12

Debit 163

Decision-making 62

Degrees of correlation 75

Delivery note 89

Depreciation charges 335

Differential cost 324

Differential piecework systems 115

Direct costs 33

Direct expenses 34

Direct labour: 34

rate and efficiency variances 269

budget 249

efficiency variance 269

employees 110

rate variance 269

Direct materials: 33

price and usage variances 265

usage variance 266

Double entry accounting for costs:

overheads 172

Double entry cost accounting system 163

E

Economic batch quantity (EBQ) 102

Economic order quantity (EOQ) 95

Efficiency variance 270, 280

EOQ:

changes in the variables in the formula 97

price discounts for large orders 100

Equivalent units: 218

FIFO method 225

weighted average cost method 221

Expected (EV): limitations 67

Expected value (EV): 63

decision-making 65

Expenditure variance 152, 273

F

Favourable variances 262

FIFO method of process costing 225

Finance costs 28

Financial accounting 21

Financial ledger control account 169

Finished goods 163

Finished goods account 175

Fixed budgets 252

Fixed costs 43

Fixed overhead: 155

absorption costing 155

Fixed overheads variances:

causes 282

Fixed production overhead capacity

variance 280

Fixed production overhead cost

variances 276

Fixed production overhead efficiency

variance 280

Fixed production overhead expenditure

variance 277

Fixed production overhead volume

variance 278

Flexed budgets 253, 255

Flexible budgets 255

Index

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 453

Full cost 36

Full cost of sale 127

Full production cost 127, 144

Functional budgets 242, 245

Functional costs 29

G

Goods received note 89

Gradual replenishment of inventory 102

Graph of linear cost function 50

H

High/low analysis: 50

charge in variable cost 56

step change in fixed costs 53

High/low method 49

Holding costs 94, 97

I

Idle time 110

Incentive schemes 116

Income statement 168

Incremental cost 324

Indirect costs 35, 126

Information: 12

attributes 13

Information for decision making 322

Interrelationships between variances 288

Inventory accounts 162

Inventory ledger record 90

Inventory records 89, 90

Inventory records:

monitoring physical inventory 91

Investment centre 17

Iso-contribution line 353

J

Job account 196

Job card 196

Job costing 194

Job sheet 196

Joint products 234

L

Labour budget 249

Labour costs 26, 110, 112

Labour efficiency:

ratio 118

variance 269

Labour rate variance 269

Labour turnover: causes 121, 271

Labour turnover rate 120

Limiting factor 340

Linear function for total costs 49

Linear programming: 346

graphical solution 351

Linear regression analysis 69

Losses and gains at different stages of

the process 230

M

Management accounting 20

Management control systems 20

Management information system 12

Manufacturing costs 27

Margin of safety 314

Marginal cost 42, 178

Marginal costing: 126

advantages and disadvantages 190

assumptions 179

reporting profit 181

uses 179

Marginal costing and absorption costing 184

Marketing costs 28

Master budget 241

Material costs 26

Materials: procedures and documentation 88

Materials inventory account 93

Materials price variance 265

Materials purchases budget 248

Materials requisition note 91

Materials return note 91

Materials usage budget 247

Paper F2: Management accounting

454 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Materials usage variance 266

Materials variances: causes 267

Maximum inventory level 108

Minimum inventory level 108

Mixed costs 44

N

Negative correlation 77

Net book value 335

Non-production costs 27

Non-production overheads:

absorption costing 147

cost legder 167

Normal loss 206

Notional annual charge 335

Notional value of an asset 335

O

Objective function 346, 353

One-off decision making 15

Opening inventory 168

Operating statement: 290

standard marginal costing 293

Operational planning 15

Opportunity cost 328, 325

Ordering costs 95, 97

Organisation structure 16

Over-absorbed fixed production overhead 277

Over-absorbed overhead 150

Over-absorption 150

Overhead absorption 144

Overhead absorption rate 144

Overhead apportionment 133

Overhead cost allocation 131

Overhead expenditure variances 278

Overhead recovery rate 144

Overheads 35, 126

Overheads budgets 250

Overtime premium 111

P

Payroll records 112

Perfect negative correlation 75

Perfect positive correlation 75

Performance reporting 262

Period costs 37

Perpetual inventory 90

Piecework systems 115

Planning 14, 15

Positive correlation 76

Predetermined overhead rate 149

Price discounts for large orders 100

Price variance 265

Prime cost 35

Principal budget factor 242

Probabilities and expected values 63

Process costing: 204

abnormal gain 213

inventory valuation 218

joint products and by-products 234

losses 206

Production and non-production costs 30

Production budget 246

Production costs 27

Production overhead expenditure variance 277

Production volume ratio 119

Productivity ratio 118

Profit centre 17

Profit/volume chart (P/V chart) 318

Purchase invoice 89

Purchase order 89

Purchase requisition 89

Purchasing procedures 89

R

Rate variance 269

Reciprocal method 136

Reciprocal method: simultaneous

equations technique 140

Reconciling budgeted and actual profit 290

Recovery 130

Recovery rate 144

Regression analysis 69

Relevant costs and decision making 323

Relevant costs and overheads 333