ACCA F2 Management Accounting - 2010 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

Chapter 5: Accounting for materials and labour

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 105

Example

A company uses the economic batch quantity formula to decide the batch

production quantities for an item of material. Due to improvements in efficiency in

the factory, the production capacity (speed of production) is increased.

Required

What will be the effect of the increase in order cost on:

(a)

the economic batch quantity (EBQ)

(b)

total annual set-up costs

(c)

total annual holding costs?

Answer

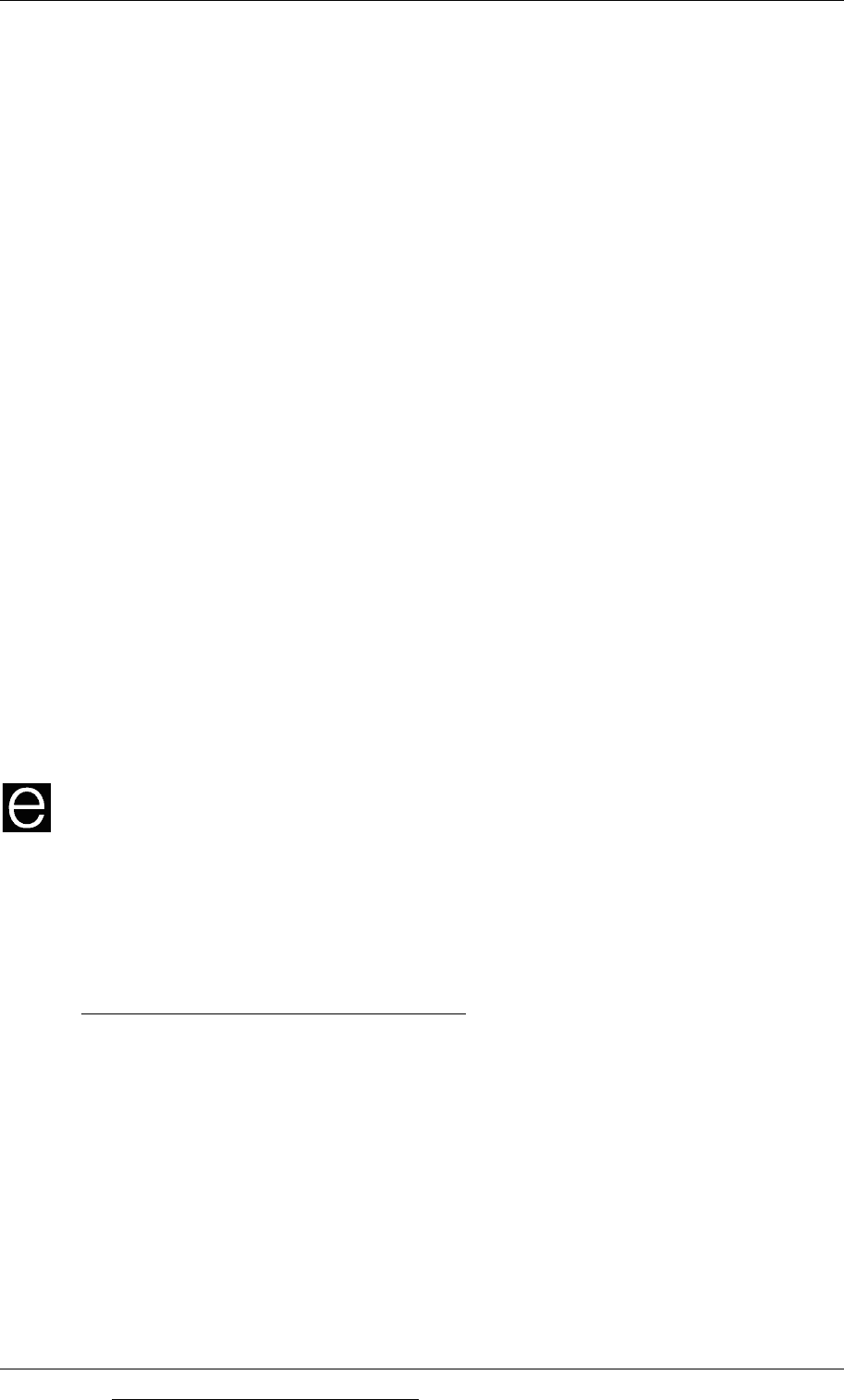

Economic batch quantity (EBQ) =

2CoD

C

H 1 −

D

R

⎛

⎝

⎜

⎞

⎠

⎟

An increase in output capacity means an increase in the value of R.

An increase in the value of R increases the value of (1 – D/R).

An increase in the value of (1 – D/R) increases the value below the line in the EBQ

formula

The EBQ will therefore become smaller.

(a)

A reduction in the EBQ will result in an increase in set-up costs, because there

will be more batches each year. Given no change in the set-up cost per batch,

total set-up costs must therefore be higher.

(b)

If the order quantity is the EBQ, total annual set-up costs and total annual

holding costs are the same. If total annual set-up costs increase, it follows that

total annual holding costs will also rise. Although the batch quantity is lower,

the maximum inventory level (Q (1 – D/R) is higher.

Paper F2: Management Accounting

106 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

(c)

Inventory reorder level and other warning levels

Reorder level

Maximum inventory level

Minimum inventory level

4 Inventory reorder level and other warning levels

So far, it has been assumed that when an item of materials is purchased from a

supplier, the delivery from the supplier will happen immediately. In practice,

however, there is likely to be some uncertainty about when to make a new order for

materials in order to avoid the risk of running out of inventory before the new order

arrives from the supplier. There are two reasons for this.

There is a supply ‘lead time’. This is the period of time between placing a new

order with a supplier and receiving the delivery of the purchased items. The

length of this supply lead time might be uncertain and might be several days,

weeks or even months.

The daily or weekly usage of the material may not be a constant amount. During

the supply lead time, the actual usage of the material may be more than or less

than the average usage.

However, the examination syllabus specifies that you will only be examined about

situations where the demand during the lead time is constant; therefore only the

length of the supply lead time might be uncertain.

Running out of an item of inventory (or stock) is called a

stock-out. (However, you

might come across the unusual term ‘inventory-out’ in your examination.)

When there is a stock-out of a key item of materials, there might be a hold-up in

production and a disruption to the production schedules. This in turn may lead to a

loss of sales and profits.

Management responsible for inventory control might to know:

when a new order for each item of materials should be made, in order to avoid

any stock-out.

whether the inventory level for each item of materials appears to be too high or

too low.

In an inventory control system, there may be warning levels for inventory, warning

management that:

the materials item should now be reordered (the reorder level)

the inventory level is too high (a maximum inventory level) or

the inventory level is getting dangerously low (a minimum inventory level).

It is assumed that it is management policy to avoid running out of any item of

inventory. In other words, it is assumed that there will be no

stock-out of any

material item.

Chapter 5: Accounting for materials and labour

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 107

The material item must be re-ordered when the inventory level falls to the

reorder quantity: If the item is not reordered at this point there will be some risk

of a stock-out during the supply lead time, before the new purchase quantity is

received.

If the inventory level is higher than the maximum inventory level, something

unusual must have happened. For example the supplier might have delivered a

new order quantity much sooner than usual (and much sooner than expected) or

demand for the item must be below even the expected minimum.

If the inventory level falls below the minimum level, this should act as a warning

to the stores manager that there might be a stock-out. The stores manager might

need to check with the supplier about why there is a delay in the delivery, and

how soon a new delivery of the material item can be expected.

4.1 Reorder level

A new quantity of materials should be ordered when current inventory reaches the

reorder level for that material.

If the supply lead time (time between placing an order and receiving delivery) is

constant or certain, the reorder level is:

[Demand for the material item per day/week] × [Lead time in days/weeks]

If the supply lead time is uncertain or not constant, but demand during the lead

time is constant, there should be a safety level of inventory. The

reorder level

should be

:

[Demand for the material item per day/week] × [Maximum supply lead time in

days/weeks]

Safety inventory

The reorder level is therefore set at the maximum expected consumption of the

material item during the supply lead time. This is more than the average usage

during the supply lead time. As a result, more inventory is held that is needed on

average.

If the order quantity is Q, the average inventory level is Q/2 + ‘safety inventory’.

Safety inventory is the average amount of inventory held in excess of average

requirements in order to remove the risk of a stock-out (or ‘inventory out’). The size

of the safety inventory is calculated as follows:

Units

Reorder level

(Demand per day ×

Maximum lead time)

A

Average usage in the lead time period

(Demand per day ×

Average lead time)

B

Safety inventory (A – B)

The cost of holding safety inventory is the size of the safety inventor multiplied by

the holding cost per unit.

Paper F2: Management Accounting

108 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

4.2 Maximum inventory level

The inventory level should never exceed a maximum level. If it does, something

unusual has happened to either the supply lead time or demand during the supply

lead time.

When demand during the supply lead time is constant, the maximum inventory

level is:

Reorder level + Reorder quantity – [Demand for the material item per day/week ×

Minimum supply lead time in days/weeks]

This maximum level should occur at the time that a new delivery of the item has

been received from the supplier. The supply lead time is short; therefore there are

still some units of inventory when the new delivery is received.

4.3 Minimum inventory level

The inventory level could be dangerously low if it falls below a minimum warning

level. When inventory falls below this amount, management should check that a

new supply will be delivered before all the inventory is used up, so that there will

be no stock-out.

When demand during the supply lead time is constant, the minimum (warning)

level for inventory is:

Reorder level – [Demand for the material item per day/week × Average lead time in

days/weeks]

Example

A company uses material item BC56. The reorder quantity for this material is 12,000

units. Weekly usage of the item is 1,500 units per week, but there is some

uncertainty about the length of the lead time between ordering more materials and

receiving delivery from the supplier.

Supply lead time (weeks)

Average 2.5

Maximum 3

Minimum 1

Required

Calculate the reorder level, the maximum inventory level and the minimum

inventory level for material item BC56.

Chapter 5: Accounting for materials and labour

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 109

Answer

Re-order level

= [Demand for the material item per day/week] × [Maximum lead

time in days/weeks]

Demand per week 1,500 units

Maximum lead time (weeks) 3 weeks

Re-order level 4,500 units

Maximum inventory level

= Reorder level + Reorder quantity - [Demand for the

material item per day/week × Minimum lead time in days/weeks]

Units

Re-order level 4,500

Reorder quantity 12,000

Demand per week 1,500 units

Minimum lead time (weeks) × 1 week

(1,500)

Maximum inventory level 15,000

Minimum inventory level = Reorder level - [Demand for the material item per

day/week × Average lead time in days/weeks]

Units

Re-order level 4,500

Demand per week 1,500 units

Average lead time (weeks) × 2.5 weeks

Subtract:

(3,750)

Minimum inventory level 750

Paper F2: Management Accounting

110 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Labour costs: direct and indirect labour costs

Elements of labour costs

Direct and indirect labour costs

Recording labour costs

5 Labour costs: direct and indirect labour costs

5.1 Elements of labour costs

Labour costs consist of:

the basic wages and salaries of employees

additional payments for overtime working

bonuses and other payments on top of basic pay and overtime (such as

contributions paid by the employer into a pension scheme for its employees).

5.2 Direct and indirect labour costs

In an earlier chapter, it was explained that a distinction is made in cost accounting

between direct labour employees and indirect labour employees. Direct labour

employees are those who work directly on the goods or services produced by the

entity.

The general rule is that direct labour costs are the costs of direct labour employees

and indirect labour costs are the costs of indirect labour employees. However, there

are some exceptions to this general rule, and some costs of direct labour employees

are treated as indirect labour costs. Two exceptions are:

the cost of idle time

the cost of overtime premium.

Idle time

Idle time is time when employees are paid and are available to work, but are not

doing any active work The cause of idle time could be a breakdown in production

equipment or a delay in the delivery of materials from a supplier. Idle time might

also occur when there are no orders from customers, and there will be no more

work until the next order arrives.

Idle time should be treated as an indirect labour cost. However, in order to treat idle

time as an indirect cost, the cost accounting system must be able to identify the

amount of time that is lost as idle time. To do this, idle time must be recorded on

labour time sheets (which are often used to document the use of labour time, for the

purpose of cost accounting).

Chapter 5: Accounting for materials and labour

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 111

Overtime premium

When hourly-paid employees work hours in excess of their normal working hours,

they are usually paid ‘overtime’ at a higher rate of pay per hour than the basic rate.

The total rate of pay per hour is the basic rate per hour plus an overtime

‘premium’.

Total overtime hourly rate = Basic hourly rate + Overtime premium.

For example, if the basic rate of pay is $20 per hour and overtime is paid at time and

a half (100% + 50% = 150% of the basic rate), the overtime premium is $10 per hour

and the total overtime pay is $30 per hour.

In costing systems, it is usual to separate the labour cost at the basic rate per hour

from the cost of the overtime premium. This is because overtime premium costs are

usually treated as an indirect labour cost (an overhead cost) and should be

measured separately.

Example

During one week, Masha works 46 hours. This includes 8 hours of overtime

working. Her basic rate of pay is $10 per hour and overtime is paid at time and a

half, the overtime rate per hour is $10 × 150% = $15, consisting of the $10 basic rate

plus a premium of $5 per hour.

Her weekly cost is calculated as follows, keeping the overtime premium separate

from the basic pay for the hours worked.

$

Basic pay – 46 hours × $10 460

Overtime premium (8 hours × $10 × 50%) 40

Total weekly pay 500

The reason why overtime premium is usually treated as an indirect labour cost is

that when employees are paid for working hours of overtime, it is a matter of

chance what work they are doing in normal hours and what work they do in

overtime. It is therefore ‘unfair’ to charge the work done in overtime directly with

the overtime premium.

The main rules about whether

production labour costs should be treated as a direct

labour cost or as an indirect labour cost can be summarised as follows.

Direct labour costs Indirect labour costs

Direct labour

employees

Basic wage or salary for

hours worked

Overtime premium only if

the overtime hours are

worked specifically at a

customer’s request

In most cases, the overtime

premium cost of hours worked in

overtime

Paper F2: Management Accounting

112 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Direct labour costs Indirect labour costs

In most cases, all other costs of

direct labour employees. This

includes:

•

the cost of all hours recorded

as ‘idle time’ – time spent

doing nothing

•

the cost of other hours spent

away from direct production

work, such as time spent on

training courses.

Indirect labour

employees

All labour costs of indirect labour

employees

5.3 Recording labour costs

In a cost accounting system, there must be a system for relating the cost of labour to

work that is done. There are various ways in which labour time might be recorded,

but the main methods are:

payroll records

time sheets or similar time records

Payroll records can be used to:

identify employees as direct labour or indirect labour employees

charge the labour costs of each employee to the department (cost centre) where

he or she is employed.

Time sheets

or similar time recording systems can be used within a cost centre to

record the time spent by each employee on different activities or tasks (or as idle

time). Time sheets are not necessary if an employee does the same work all the time.

For example, it is not necessary to prepare time sheets for a machine worker if the

employee spends all his time working at the same machine producing the same

items of output.

However, time sheets are needed if employees spend time on more than one cost

item, so that their labour cost has to be allocated to the different cost items. For

example, a manufacturing centre might product two products, Product A and

Product B, and a direct labour employee might spend time working on both

products. Time sheets can be used to record the time spent on each product, so that

the labour cost can be allocated to each product according to the amount of time

spent on each. Similarly time sheets are needed to work out the labour cost of

specific jobs or contracts: the time spent by employees on each job or contract

should be recorded, so that the cost of the time can be allocated and the labour cost

for each job or contract can be calculated.

Accounting for labour costs

Within a cost accounting system, indirect and direct labour costs are recorded and

charged to the appropriate cost centres and cost units. The records of labour costs

Chapter 5: Accounting for materials and labour

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 113

are included within the double-entry cost accounting system (where such a costing

system is used).

Accounting for labour costs with ‘ledger entries’ in a cost accounting system is

explained in a later chapter.

Paper F2: Management Accounting

114 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Labour costs: remuneration methods

Calculating the cost of labour

Time-based systems

Piecework systems

Incentive schemes

6 Labour costs: remuneration methods

6.1 Calculating the cost of labour

The labour cost of a product, service, job or activity is calculated as the cost of

paying the employees to do the work. Labour costs are allocated between different

jobs or activities on the basis of the time spent working on each job or activity.

Many employees are paid a fixed salary each month. Their costs are allocated to the

departments they work in and to the activities they perform on a time basis. For

example, if an employee spends half his time on one type of activity and half of his

time on another activity, the cost of his labour will be divided 50:50 between the two

activities.

Some employees are paid by the hour, and a few are paid a piecework rate. The

labour costs of these employees can be measured and charged to the units of work

they produce.

6.2 Time-based systems

When employees are paid an hourly rate, their basic pay (per week or month) is

calculated as follows:

Basic pay = Hours worked × Rate of pay per hour

Production records should kept of the time spent by these employees on specific

jobs or batches of production, so that the labour cost for this work can be measured

accurately.

As explained earlier, any overtime premium for overtime working is usually treated

as an indirect labour cost. (Overtime premium is charged as a direct cost only when

the overtime is worked for a specific purpose, for example to meet specific demands

by a customer for meeting a delivery date.)