Журнал - The Engine Yearbook 2005

Подождите немного. Документ загружается.

Cover supported by:

EYB2005fctest 7/9/04 5:21 pm Page 1

!IRLINEHERITAGE0ARTSMANAGEMENTFOCUS

WWWAIRLIANCECOM

BUTBUSINESSIS

LOOKINGUPIN

/iÊ LÕÃiÃÃÊ V>ÌiÊ ÛiÀÊ ÌiÊ

>ÃÌÊ viÜÊ Þi>ÀÃÊ >ÃÊ LiiÊ Ì}Ê

ÌÊ >Õ}Ê >LÕÌ]Ê LÕÌÊ Óää{Ê `ÃÊÊ

«ÀÃiÊ >ÃÊ >Ê «ÀvÌ>LiÊ Þi>ÀÊ vÀÊÊ

>ÀiÃÊ Ì>ÌÊ V>Ê ÃÕVViÃÃvÕÞÊÊ

VÌÀÊ VÃÌÃ°Ê Ê ÀiÊ ÞÕÊ Ài>`ÞÊ

ÌÊ i«Ê ÌÕÀÊ Ì}ÃÊ >ÀÕ`Ê >`ÊÊ

vÕÀÌiÀÊ Ài`ÕViÊ ÞÕÀÊ Ã«>ÀiÊ «>ÀÌÃÊ

ÛiÃÌi̶

Ê

7iÊV>Êi«°

-AYBETHEREHASNT

BEENMUCHTOSMILE

ABOUTINTHELAST

FEWYEARS

framecheck2005 9/9/04 2:03 pm Page 3

Commercial aero-engine MRO outlook

— a new dawn? 2

Cutting total ownership costs with

the PW6000 8

Reducing maintenance costs on

the V2500 12

Managing the costs of engine ownership 16

Engine maintenance costs 20

Engine trading and value trends 26

When should part-life engines be built? 30

Sharing the customer’s vision 34

Managing the maintenance of

leased engines 38

Upgrading GE’s maturing engines 44

The aero-engine aftermarket and

opportunities in gas path diagnostics 48

Are your engines really as healthy as

they seem? 54

Filtration technology for gas turbine

engine fuel and lubrication systems 60

Economic aspects of maintaining

engine efficiency 64

Advanced repair and coating technologies 68

Titanium impeller welding 72

The latest in aerospace testing equipment 76

Automated repair and overhaul of

aero-engine components 80

Third-generation high-speed grinders 84

Adding capabilities to suit customer need 88

Engine overhaul survey — worldwide 92

Non-overhaul specialist engine repair

companies 103

Directory of major commercial aircraft

turboprops 110

Directory of major commercial aircraft

turbofans 112

CONTENTS

An Aviation Industry Press publication

EDITOR

Paul Copping

paulc@aviation-industry.com

STAFF WRITERS

Martin Fendt

martinf@aviation-industry.com

Niall O’Keefe

niallo@aviation-industry.com

PRODUCTION MANAGER

Phil Hine

philh@aviation-industry.com

CIRCULATION & SUBSCRIPTIONS

Dino D’amore

dinod@aviation-industry.com

AREA SALES MANAGER EUROPE, ASIA & AFRICA

Gary Gilmour

garyg@aviation-industry.com

PUBLISHING & SALES ASSISTANT

Pervinder Singh

pervinders@aviation-industry.com

PUBLISHER & SALES MANAGER - USA

Simon Barker

simonb@aviation-industry.com

MANAGING DIRECTOR

Paul Copping

paulc@aviation-industry.com

The Engine Yearbook is published annually.

Aircraft Technology Engineering & Maintenance

(ISSN 0967-439X) is published 7 times per year

UK subscription cost is £100.

Overseas subscription cost is £115 or $185.

All subscriptions enquiries to:

Dino D’Amore: dinod@aviation-industry.com

All advertising enquiries to:

Simon Barker: simonb@aviation-industry.com

Published by Aviation Industry Press Ltd.

31 Palace Street, London SW1E 5HW, England

Tel: +44 (0) 20 7828 4376

Fax: +44 (0) 20 7828 9154

E-mail: atem@aviation-industry.com

Website: www.aviation-industry.com

Distributed by MSC Mailers, Inc., 25 Starlit Dr, Middlesex, NJ 08846

Periodicals Postage paid at Middlesex, NJ 08846.

POSTMASTER: Send US address corrections to

Pronto Mailers Association, 444 Lincoln Blvd., Middlesex, NJ 08846.

© 2004 Aviation Industry Press.

Printed in England by Headley Brothers Ltd.

All rights reserved. No part of this publication

may be reproduced by any means whatsoever without

express written permission.

Although care has been taken in the compilation of

this magazine, Aviation Industry Press does not take

responsibility for the views expressed herein.

AIP is a subsidiary of

Aviation Industry Group Ltd.

ENGINE YEARBOOK 2005

Cover image by Phil Hine

Sponsored by Lufthansa Technik

EYB2005 toc 7/9/04 5:20 pm Page 1

2

ENGINE YEARBOOK 2005

ENGINE YEARBOOK 2005

Commercial aero-engine MRO outlook

— a new dawn?

Aviation is facing significant

uncertainty with

fundamental challenges to

profitability, yields and

traditional business models.

David Stewart, principal,

AeroStrategy offers us some

clear thinking concerning

the aero-engine aftermarket

when the outlook would

appear to be uncertain.

O

ver the past few years,

AeroStrategy has developed a

commercial maintenance, repair

and overhaul (MRO) market forecast

with the assistance of more than 20

airlines and global MRO suppliers. Its

intention is to help dispel some of the

uncertainty, to address some of the

unresolved MRO concerns and to assist

in answering some basic questions,

such as: “When will demand spring

back? How many aircraft will be

permanently retired? How many

parked aircraft will return to service?

How will increasing engine size and

reliability influence demand? How

rapidly will the market grow? Which

aircraft types, engine models and

regions will lead the way?” Beyond

facts and figures, AeroStrategy also

provides its perspective on evolving

and critical supply-side trends which

will shape the engine MRO market for

years to come.

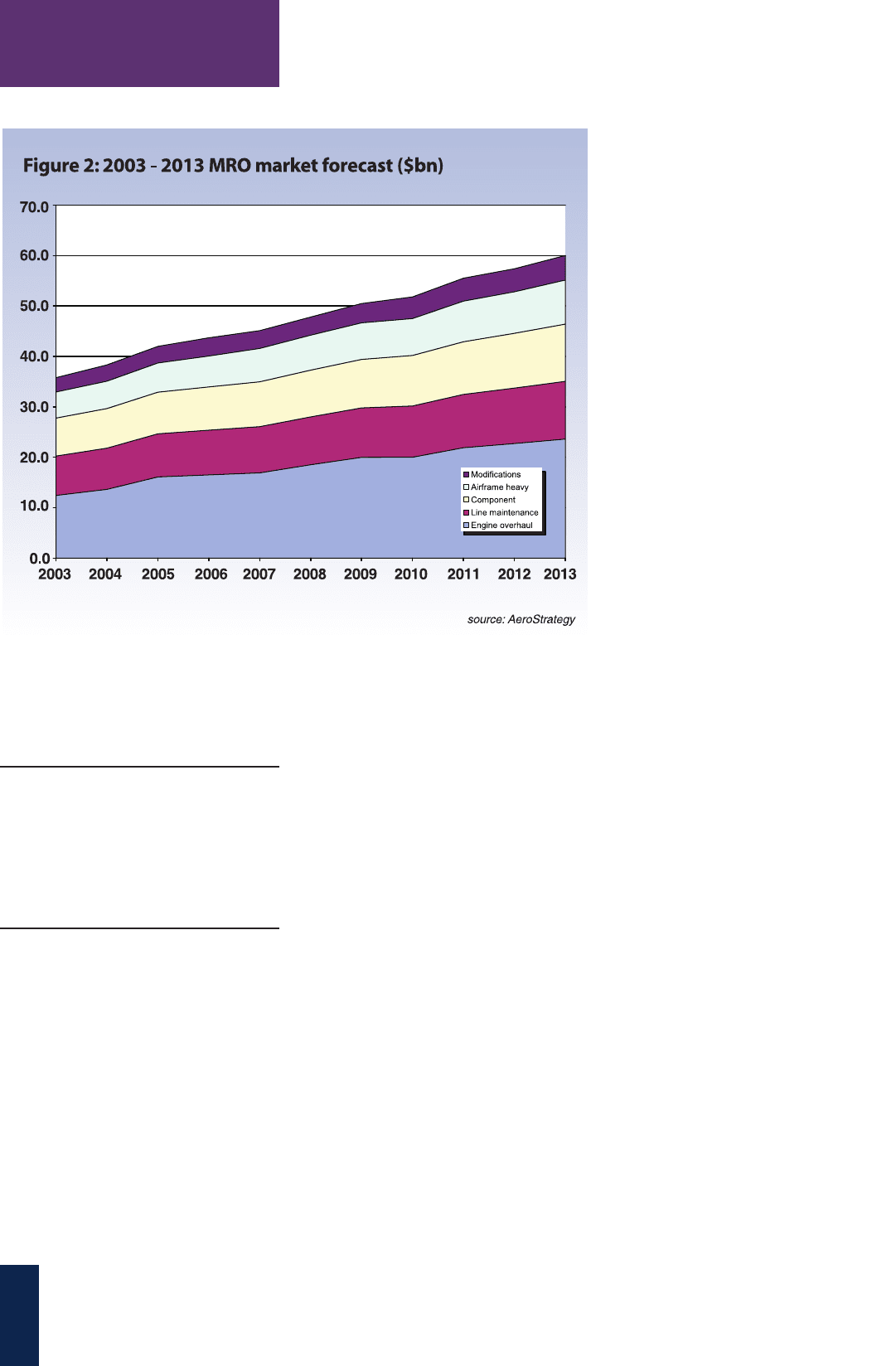

Market growth

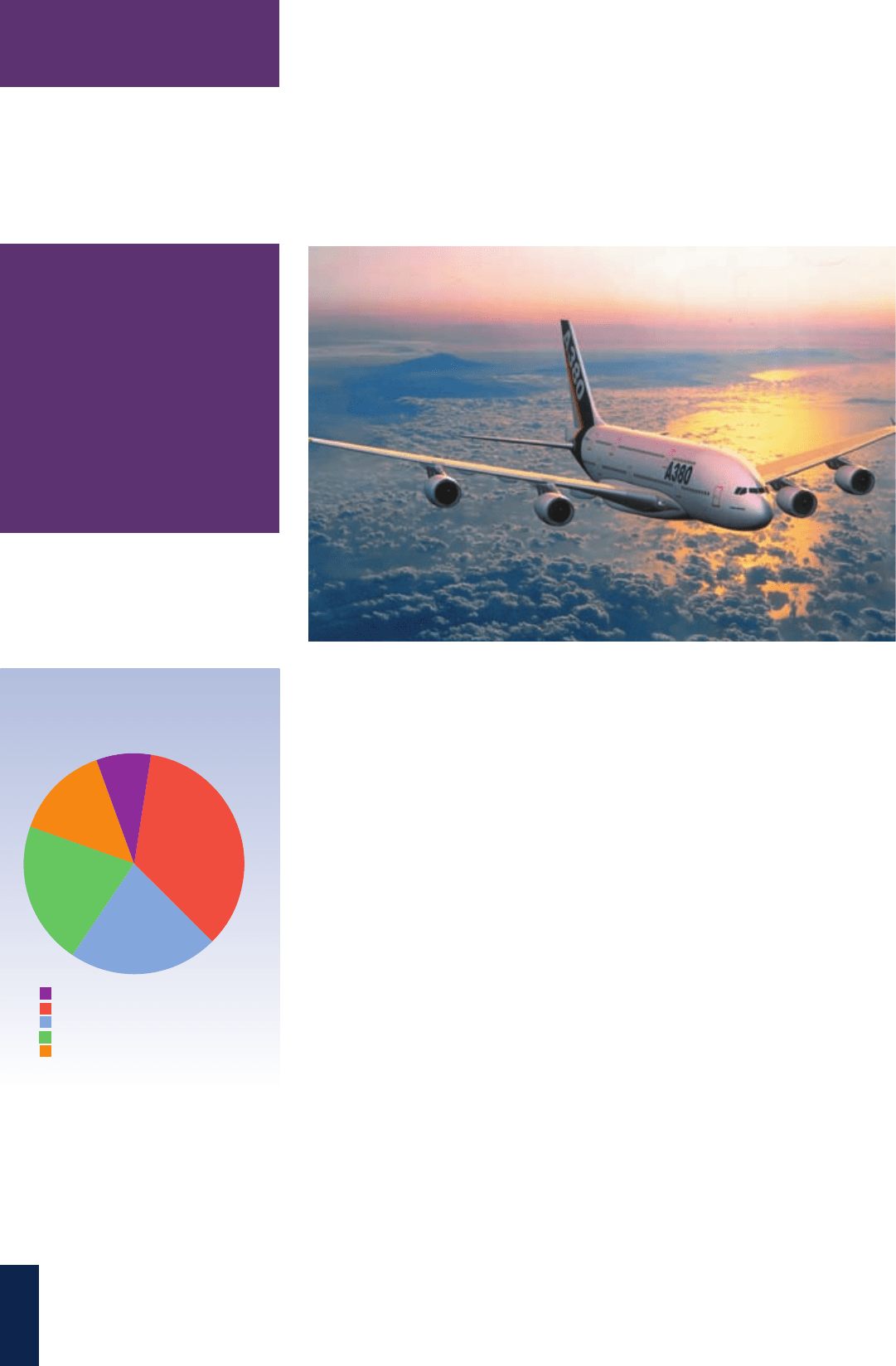

AeroStrategy estimates that commercial

jet aircraft with more than 35 seats

generated MRO demand worth $35.8

billion in 2003. This is spread across five

primary market segments: off-wing

engine overhaul; airframe heavy checks

(C and D checks); component overhaul

and repair; line maintenance (including

A, B and overnight checks); and major

airframe modifications, including cargo

conversions, avionic upgrades and IFE

modifications.

AeroStrategy calculates that MRO

demand will reach $60 billion in 2013,

implying an annual growth rate of 5.3

per cent (in constant 2003 US dollars,

not accounting for future changes in

labour rates or spare parts costs). Four

key trends underpin this prediction, as

follows:

● Air travel growth will average 4.7

per cent over the next decade,

fuelling an expansion in the active

air transport fleet from 16,000 in

2003 to 23,360 in 2013.

● The airline industry imperative to

contain MRO expenditures will be

challenged by the MRO

requirements generated by the

unprecedented number of aircraft —

in excess of 5,000 — delivered

between 1998 and 2002, that are

only now generating their first

heavy maintenance events.

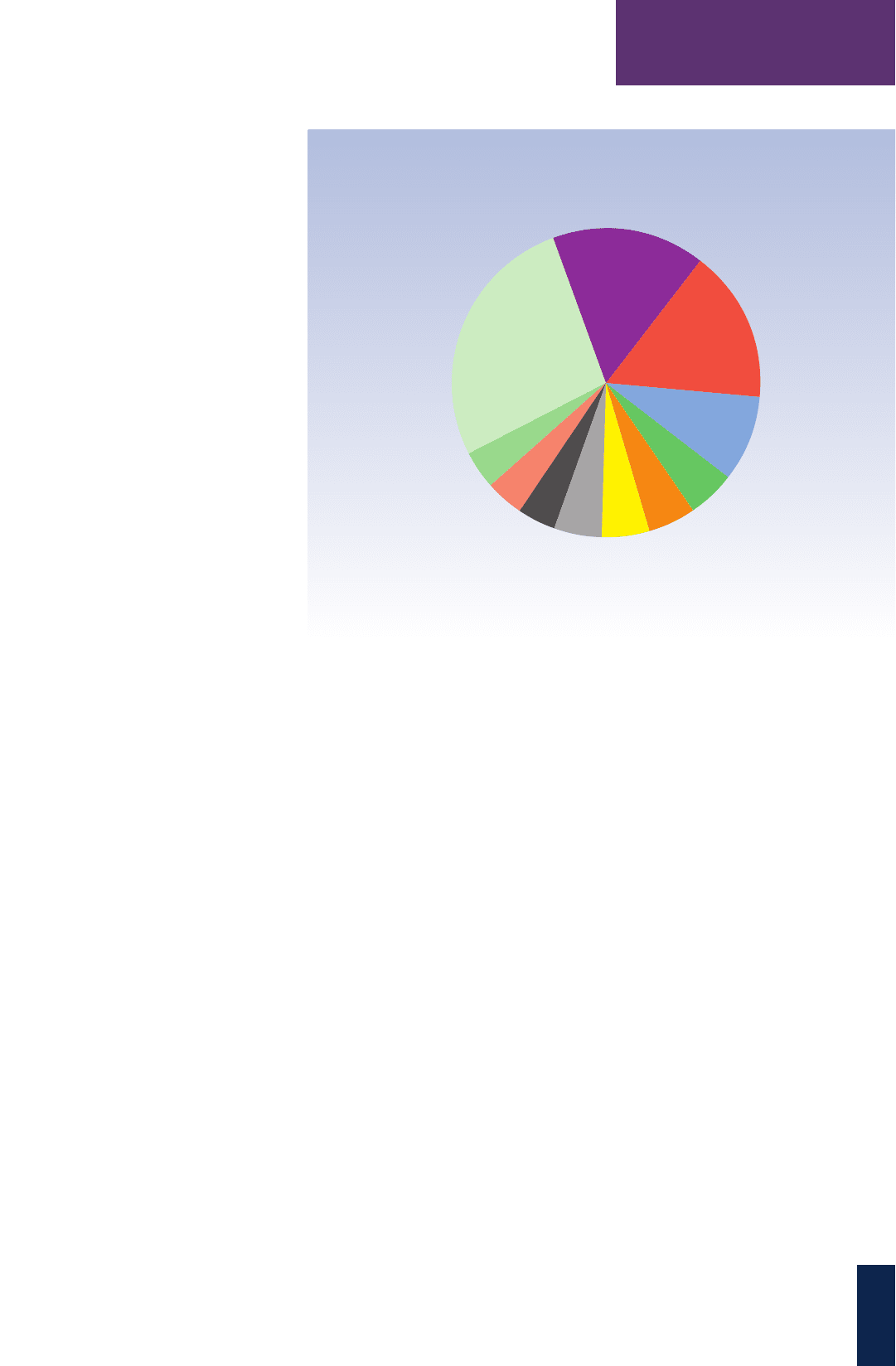

Figure 1:2003 Commercial

MRO market - $35.8b

source: AeroStrategy

Modifications

Engine overhaul

Line maintenance

Component

Airframe heavy

8%

35%

22%

21%

14%

EYB2005_1 7/9/04 8:34 am Page 2

framecheck2005 9/9/04 3:36 pm Page 3

4

ENGINE YEARBOOK 2005

ENGINE YEARBOOK 2005

● Over 600 of the 2,000-plus inactive

aircraft fleet will return to service in

the next four to five years, with

many of the young aircraft parked

during the 2001-2002 industry crisis

returning to passenger service and

with more than 200 parked aircraft

being converted to freighters.

● Daily aircraft utilisation will be

nearly 10 per cent higher in 10

years’ time. This will occur for three

reasons: the expansion of high-

utilisation low-fare carriers; the

pressures they place on traditional

airlines to increase the economic

productivity of their major assets;

and the fact that many airlines are

now operating at relatively

depressed levels of utilisation.

Demand for engine overhaul

For the sake of this forecast, engine

overhaul costs includes the costs of all

major engine shop visits and the costs

of changing the life-limited parts

(LLPs). It excludes the costs of minor

shop visits, inventory costs,

unscheduled events, one-off campaigns

and engine upgrade programmes.

Using this definition, engine overhaul

is the largest segment of the commercial

MRO market, currently valued at $12.4

billion. The largest engine submarkets

are the CF6-80C2, CFM56-3 and

PW4000-94, the only ones with activity

exceeding $1 billion each. Pratt &

Whitney engines, despite the rapid

reduction of the venerable JT8D fleet,

generate the highest proportion of

overhaul demand — 29 per cent, due to

their still sizable installed base. CFMI,

GE and Rolls-Royce engines generate

26, 24 and 14 per cent of overhaul

demand respectively.

For the period 2003-2013,

AeroStrategy forecasts that demand will

increase at 6.3 per cent per annum. This

high rate of growth is driven by a

number of key factors:

● Fleet growth: AeroStrategy’s forecast

shows an underlying aircraft fleet

growth of 3.8 per cent per annum

and engine fleet growth of 3.4 per

cent. In particular, the spate of

aircraft deliveries in the late 1990s

will provide the impetus for a jump

of over 20 per cent in shop visits in

the near future, from about 8,400 in

2003 to almost 10,300 in 2005. The

start of this sharp increase in

activity is already being witnessed,

most particularly in the CF34 market

where GE and its service centres

have begun to spool up for a

‘tsunami’ wave of shop visits.

● Engine utilisation growth: the drive

by low-fare carriers and traditional

airlines alike to improve asset

productivity means that average

engine utilisation will grow at about

one per cent per annum. The

combined impact of fleet and

utilisation growth results in a 4.9

per cent per annum rise in engine

utilisation.

● Improved reliability: this engine

utilisation increase is offset by

improved engine reliability. The

average time between shop visits for

the entire engine fleet is set to

increase from 8,900 hours to 10,400

hours over the 10-year forecast

period. This results in the number

of shop visits showing a lower rate

of growth of 4.4 per cent per

annum.

● Increased shop visit cost: the

average shop visit cost for the fleet

In 2013,CFMI engines will

generate most engine overhaul

demand at 27.5 per cent,closely

followed by GE (26 per cent), Pratt

and Whitney (19 per cent) and

Rolls-Royce (16 per cent).

EYB2005_1 7/9/04 8:39 am Page 4

5

ENGINE YEARBOOK 2005

ENGINE YEARBOOK 2005

is expected to rise from about $1.5m

to $1.75m. This increase results from

the growing number of new, large

and sophisticated engines such as

the GE90, Trent 700/800 and

PW4000-112 that will start

experiencing shop visits, and the

fact that many of the engines

delivered in the late 1990s will be

facing their first significant LLP

replacement requirements at the

back-end of the forecast period.

The fastest growing engine models

include the CF34-3B, CFM56-5B, CFM56-

7 and V2500 — no surprise, given the

growth of regional airlines and the robust

outlook for the preferred aircraft of the

low-fare carriers, the A320 family and the

737NG. A few larger engines — the CF6-

80E, GE90 and Trent 700/800 — will see

significant growth as well. Overhaul

spending on these extremely reliable and

relatively young engines will rise by

more than 15 per cent per annum, as

their first shop visits for LLP replacement

take place later in the forecast period.

By 2013, six engines will each

generate more than $1 billion per year

in MRO demand, with the CF6-80C2

leading the way, followed by the

CFM56-3, CFM56-5B, CFM56-7,

PW4000-94 and V2500-A5/D5. Partially

offsetting this growth is the inevitable

decline in some currently significant

engine markets. The JT8D, JT9D, CF6-

50 and RB211-524 will be hit by a

double whammy — not only will the

associated aircraft rapidly retire, they

will also create a supply of cheap

surplus engines that will, in some

instances, make them cheaper to replace

than to overhaul.

In 2013, CFMI engines will generate

most engine overhaul demand at 27.5

per cent, closely followed by GE (26 per

cent), Pratt and Whitney (19 per cent)

and Rolls-Royce (16 per cent).

Engine overhaul supply

On the supply side, the OEMs have

already developed a strong aftermarket

presence, albeit with varying strategies.

Led by GE, they account for a total of

43 per cent of the aftermarket. In the

future, AeroStrategy expects the OEMs

to maintain this strong position because

of the strategic advantages that they

have and seek, such as:

● Their ability to make the significant

investments required to support the

overhaul of today’s highly

sophisticated engines;

● Control and development of

technical information and repair

schemes;

● Control of spare parts, which

represent about 60 per cent of the

cost of engine overhaul;

● Their ability to bundle new engine

sales with long-term support

contracts; and

● Retaining an established global

network of support facilities.

Airlines and airline-affiliated

suppliers similarly account for 44 per

cent of the aftermarket although 30

per cent is ‘in-house’ work and 14

per cent is for third parties.

AeroStrategy expects the amount of

engine overhaul accomplished by

airlines to decline over the next

decade for the simple reason that

airlines will find it increasingly hard

to justify the very-high investment

required to establish engine overhaul

capability, especially for the new,

large engine models.

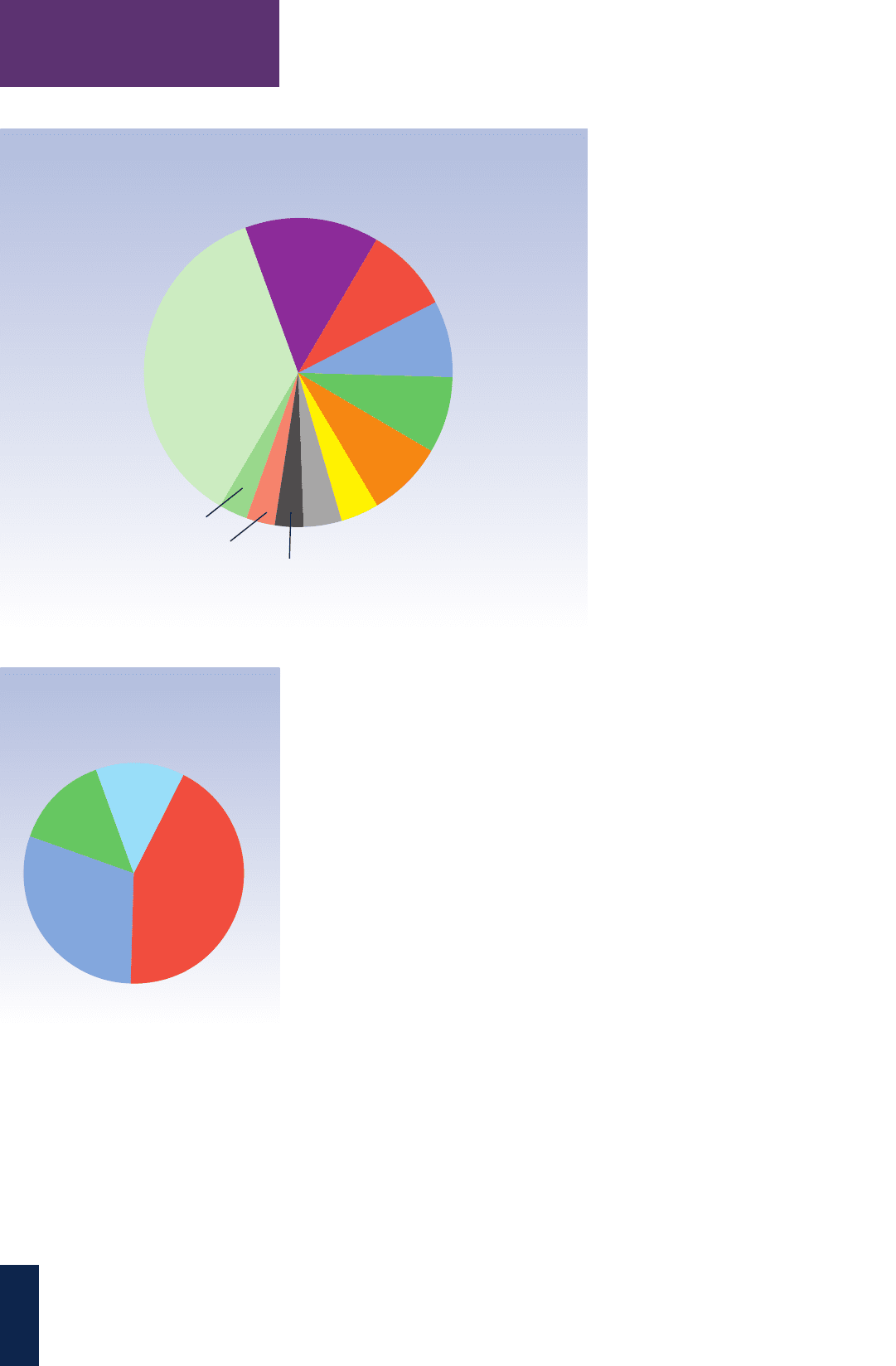

Figure 3: Engine overhaul demand by engine ($12.4b)

source: AeroStrategy

CF6-80C2

16%

CFM56-3

16%

PW4000-94

9%

JT8D-200

5%

JT9D

5%

V2500

5%

RB211-535

5%

CFM56-5C

4%

PW2000

4%

RB211-524GH

4%

Other

27%

EYB2005_1 7/9/04 8:40 am Page 5

6

ENGINE YEARBOOK 2005

ENGINE YEARBOOK 2005

Independent suppliers, led by MTU and

IHI, have 13 per cent of the market. The

growth and competitiveness of the OEMs

and airline-affiliated suppliers during the

1990s caused difficult times for the

independents, and their market share

declined. It would appear that life for the

independents will not get any easier over

the next decade given the high entry

barriers in the engine overhaul market,

especially for the newer engines.

However, independents such as Standard

Aerospace and MTU (both now under

new ownership) who combine financial

strength and excellent performance will

remain strong competitors.

Market trends

Several developments are reshaping the

engine overhaul market. First and

foremost in the minds of many is parts

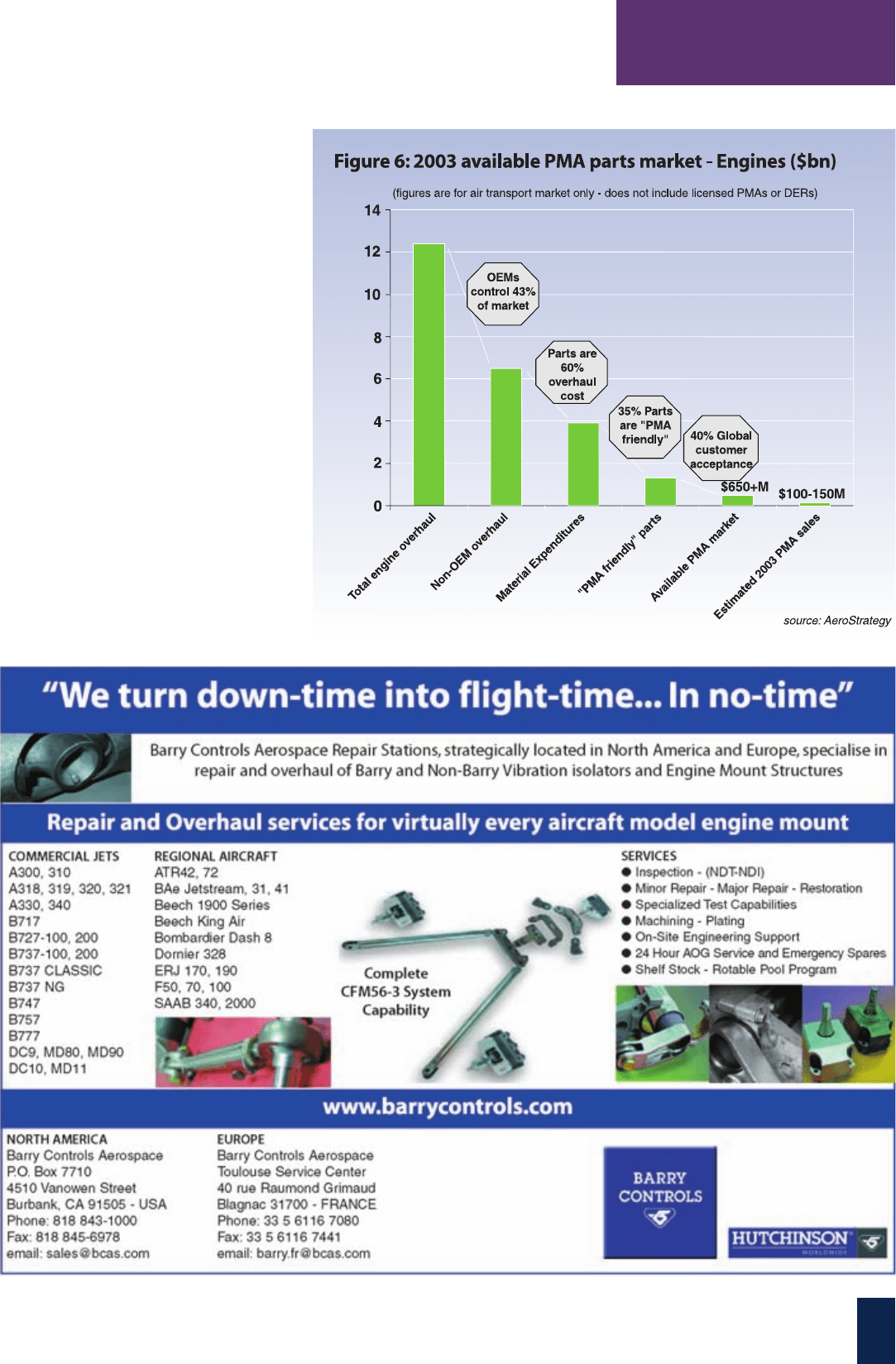

manufacturing approval (PMA). With

airlines pressuring OEMs to keep spare

part prices down and service levels up,

the penetration of PMA parts will persist.

Engine PMA parts, once consigned to

burner cans, accessories and low value-

added parts, have entered the gas path in

many locations where high-value parts

are found. AeroStrategy estimates that the

available market for engine PMA today is

$650m, of which PMA suppliers will

capture about $150m. AeroStrategy

analysis also shows the potential impact

of PMA on OEM parts volumes is

relatively low, primarily because of a

combination of the relatively low number

of parts that are suitable for PMA and a

continuing uncertainty among some

airlines on the acceptability of PMA. The

real threat of PMA to OEMs is pricing

pressure. The PMA phenomenon,

combined with an increase in use of DER

repairs, will challenge OEMs to rethink

the “razor-razor blade” paradigm—where

spare parts profits subsidize engine

development—that has long underpinned

the aero-engine business.

Secondly, OEMs are continuing to use

licensed service centre networks and joint

ventures to enhance their positions in the

aftermarket rather than invest in their

own facilities. Consider two recent

examples: the establishment of N3, a joint

venture between Rolls-Royce and

Lufthansa Technik, and GE’s licensing of

several well-known suppliers to service

the CF34 in competition with its own

maintenance centers. These moves

occurred while OEMs were closing engine

overhaul facilities, suggesting they are

emphasising return on assets over revenue

growth. The clear benefit of this approach

by the OEMs is protecting their control of

spare parts distribution while enabling

them to build greater local presence across

the globe with less required investment.

Thirdly, mergers and acquisitions among

independent suppliers will continue apace.

Witness the Carlyle Group investing in

Avio, KKR purchasing MTU and 3i buying

SR Technics. Some consolidation will

probably occur at the “second-tier” of the

engine sector, possibly creating new,

independent entities that can more

effectively compete with the OEMs.

Finally, most industry observers

believe that the engine overhaul sector

is suffering from over-capacity. Whilst

some of this slack will be recouped via

the expected increase in demand in the

short-term, profit margins for some

engine models will suffer until supply-

demand imbalances are rectified.

Conclusion

The outlook for the commercial engine

MRO market over the next 10 years is a

story with two strong themes: demand

growth driven by fleet demographics and

Figure 4: Engine demand by engine type ($23.6b)

source: AeroStrategy

CF6-80C2

14%

CFM56-3

9%

PW4000-94

8%

CFM56-7

8%

V2500

8%

CFM56-5B

4%

GE90

4%

CFM56-5C

3%

Other

36%

CF34-3

3%

Trent 800

3%

Figure 5: 2003 engine overhaul

supply share ($12.4b)

source: AeroStrategy

OEM

8%

In-house

30%

Airlines

3rd party

14%

Independents

13%

EYB2005_1 7/9/04 8:40 am Page 6

7

ENGINE YEARBOOK 2005

ENGINE YEARBOOK 2005

significant changes in supply. Airlines have

become significantly more focused on costs

and value. What they require from

suppliers is still evolving. What is certain

is that they will seek to reduce the

projected 6.3 per cent annual growth in

engine MRO expenditures through greater

outsourcing, innovative commercial

agreements, closer management of repair

scope and greater use of alternative parts

and repair sources. In addition, airline

alliances such as SkyTeam and Star will

increasingly seek to use joint purchasing

and work sharing to realize cost synergies.

MRO providers must adapt to succeed.

As airlines increasingly focus on the

transportation aspect of their business,

MRO providers can count on heightened

demand for broad aircraft support

capabilities, enhanced asset management

skills and improved productivity. In the

final analysis, the new value propositions

yet to be developed by an increasingly

global supplier base will make the

biggest impact on the future size and

shape of the MRO industry. ■

EYB2005_1 9/9/04 11:00 am Page 7

8

ENGINE YEARBOOK 2005

ENGINE YEARBOOK 2005

Cutting total ownership

costs with the PW6000

Pratt & Whitney expects to

regain a position of

prominence in the market for

100-passenger airliners due

to the low capital and

maintenance costs of its new

PW6000 engine.Tom Pelland,

PW6000 programme

director, explains why.

“T

he PW6000 will maximise

airline profitability by

lowering acquisition and

maintenance costs,” says Tom Pelland,

PW6000 programme director. “The

engine will provide low cost of

ownership because it has significantly

fewer parts than comparable engines.”

The PW6000 will not have to make a

shop visit until six to eight years after

entering service. Pratt & Whitney

designed the engine to keep engines on-

wing for 10,000 to 12,000 flight cycles

and 15,000 hours.

Pelland says the PW6000 is the only

engine designed specifically for low

acquisition and maintenance costs in the

100-passenger market segment. “An engine

with low capital costs and low

maintenance costs is more optimal for

shorthaul operations than a complex

engine that may be more fuel efficient.

Both the low acquisition cost and low

maintenance costs are made possible by an

engine design that minimises the number

of parts and maximises time on wing.”

The PW6000 is on track for FAA

certification in the fourth quarter of

2004 and entry into service as early as

December 2005 on the Airbus A318.

Two versions of the engine are to be

certified: the PW6122A with 22,000lb

(10,000kg) of thrust; and the PW6124A

with 24,000lb (11,000kg) of thrust.

The PW6000 series is designed to

provide robust engines for aircraft

operating in the demanding shorthaul,

quick-turnaround environment.

Aircraft powered by the PW6000 will

make one- to two-hour flights as many

as 10 to 12 times a day. The design of

the PW6000 reflects the suggestions

and recommendations of customers.

From the beginning of the development

programme, Pratt & Whitney gave

customers a significant role in the

design, development and testing of the

engine.

Pratt began soliciting feedback from

customers from programme launch in

September 1998. Many of the ideas for

improved maintainability came from a

series of customer focus events. Pratt

says customers made it clear from the

beginning that they wanted an engine

with low acquisition and maintenance

costs and extended time on-wing. The

company responded with an engine

design based on the concept of

simplicity.

The PW6000’s simplicity starts with a

configuration that includes only 15

stages — a fan, four low-pressure

compressor stages, six high-pressure

compressor stages, one high-pressure

turbine stage and three low-pressure

turbine stages. This compares with 18

stages on the Pratt & Whitney JT8D-

200 and as many as 19 on other

competitors’ engines. With fewer stages,

the engine has 30 per cent fewer airfoils

than competitive engines. This means

significantly lower maintenance costs

since experience has shown that airfoils

account for 60 per cent of maintenance

material costs on most P&W engines.

This is especially important with

regard to the airfoils used in high

volume at engine overhaul. The

PW6000 has only half as many of these

high-volume airfoils as its major

competitor. These are the parts in the

hot section of the engine - high-dollar,

high-volume parts that are significant

drivers of total maintenance costs.

Maintenance is also simplified

because of the design of the line

replaceable units (LRUs), which are

replaced while the engine is on-wing.

The LRUs are arranged in a single

EYB2005_1 7/9/04 8:41 am Page 8