Simon Benninga. Financial Modelling 3-rd edition

Подождите немного. Документ загружается.

658 Chapter 24

1. They are consistent with the risk-free interest rate; therefore,

qq

R

UD

+==

11

106.

2. The state prices give the same NPV for the project as that calculated

by the cost of capital.

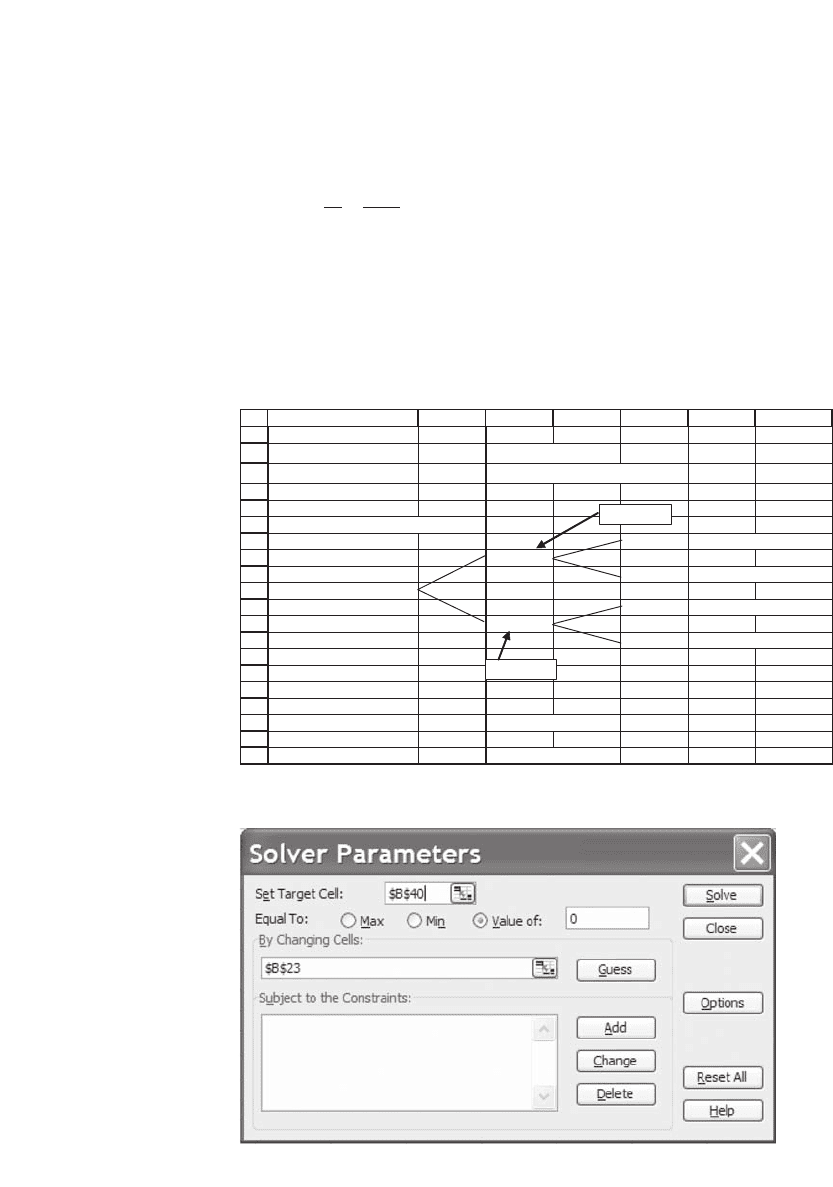

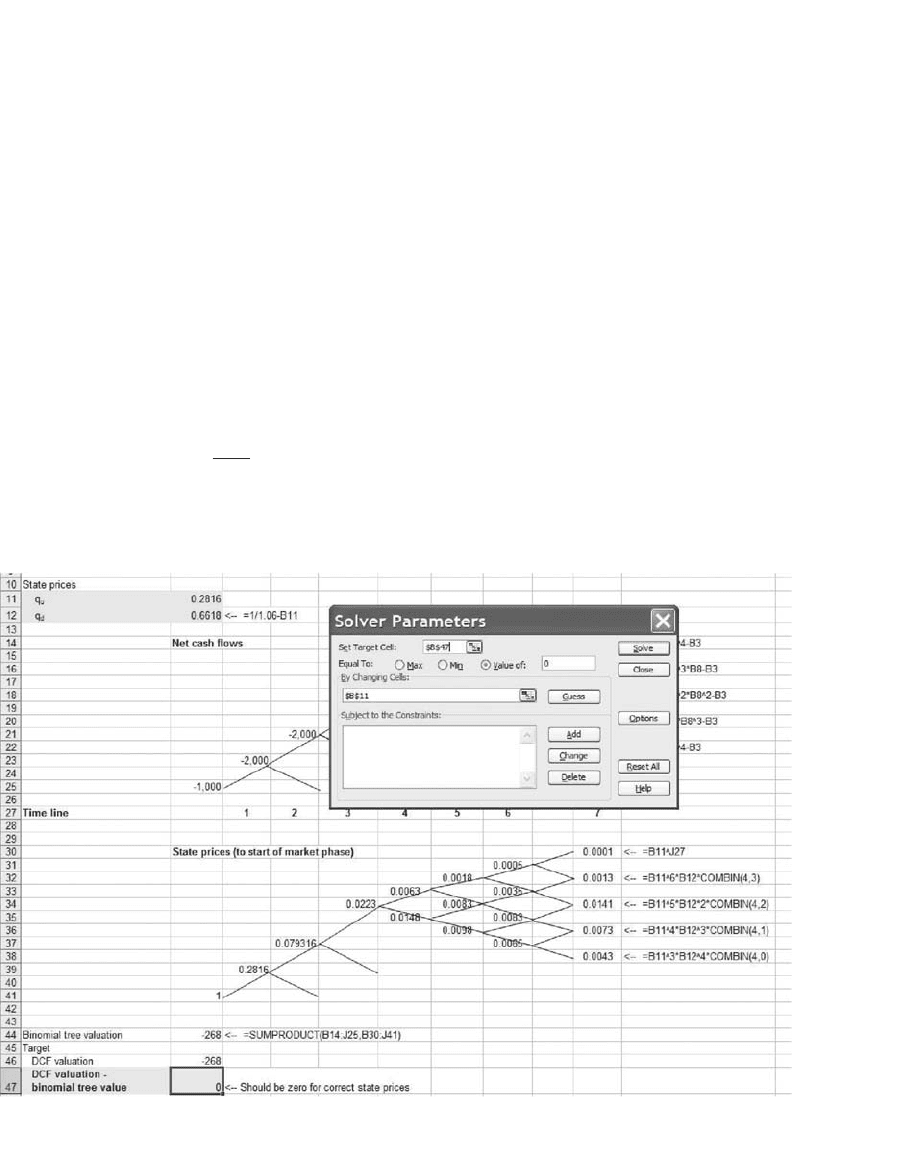

The second requirement means that we have to use the Excel Solver

to determine the state prices. Here’s what the solution looks like (the

discussion of how Solver was used follows this spreadsheet picture):

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

ABCDEF

State prices

q

U

0.4241 <-- =1/(1+B3)-B23

q

D

0.5193 <-- Determined by Solver

Project state-by-state discounting

26.9797 <-- =E6*B22^2

42.4105

17.6187 <-- =E8*B22*B23

-50

17.6187 <-- =E10*B22*B23

-25.9646

-16.1798 <-- =E12*B23^2

State-by-state NPV 12.48 <-- =SUM(A27:E33)

Target cell

G

<-- =B38-B18(0.00)

=C7*B22

=C11*B23

To determine the state prices, we use the Solver (Tools|Solver):

659 Real Options

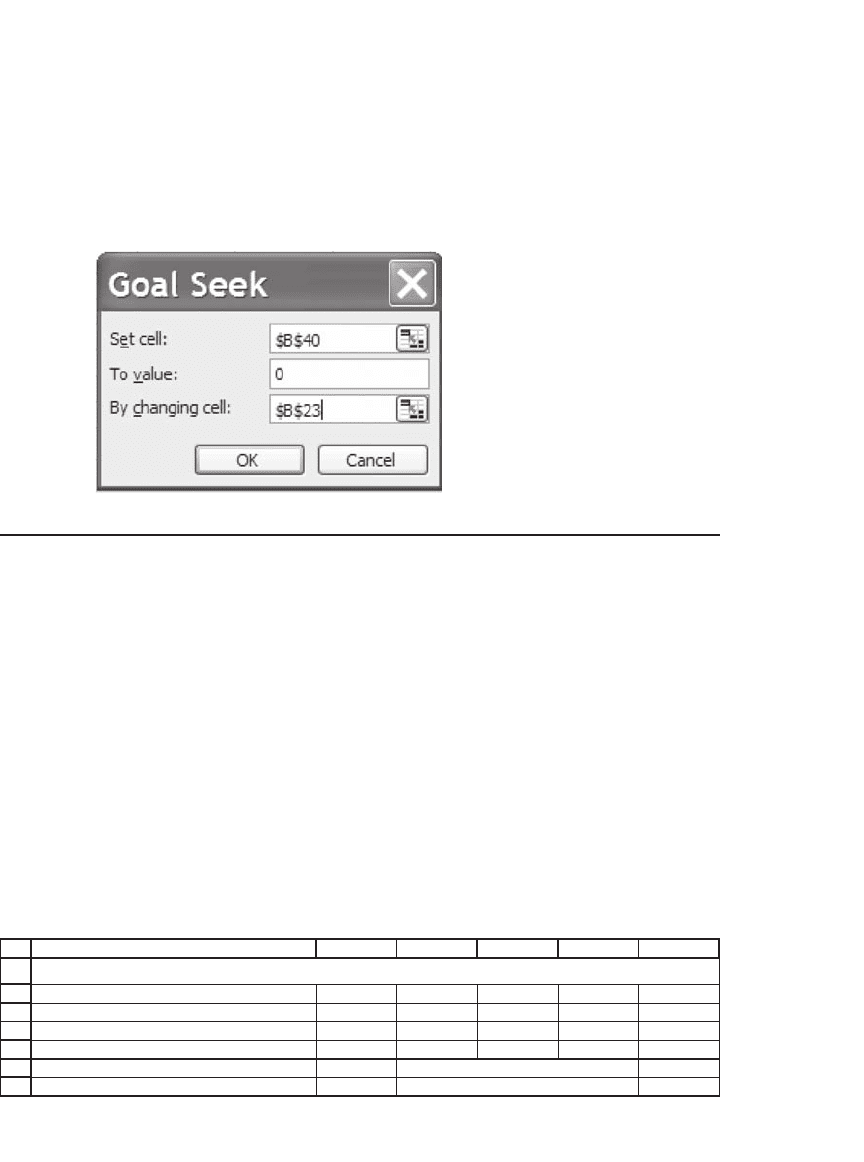

You can also use Goal Seek (Tools|Goal Seek) to get the same result.

However, Excel’s Goal Seek does not remember its previous settings,

meaning that each time you repeat this calculation you will have to reset

the cell references. Here’s what the Goal Seek dialogue box looks like:

24.4 Valuing the Abandonment Option as a Series of Puts

The preceding example shows how and why the abandonment option

can have value. It also illustrates another, more troublesome, feature of

the abandonment option, namely, that it may be very diffi cult to value.

While it is diffi cult enough to project expected cash fl ows, it is even more

diffi cult to project state-by-state cash fl ows and state prices for a complex

project.

A possible compromise in the valuation of an abandonment option is

to value a project as a series of cash fl ows plus a series of Black-Scholes

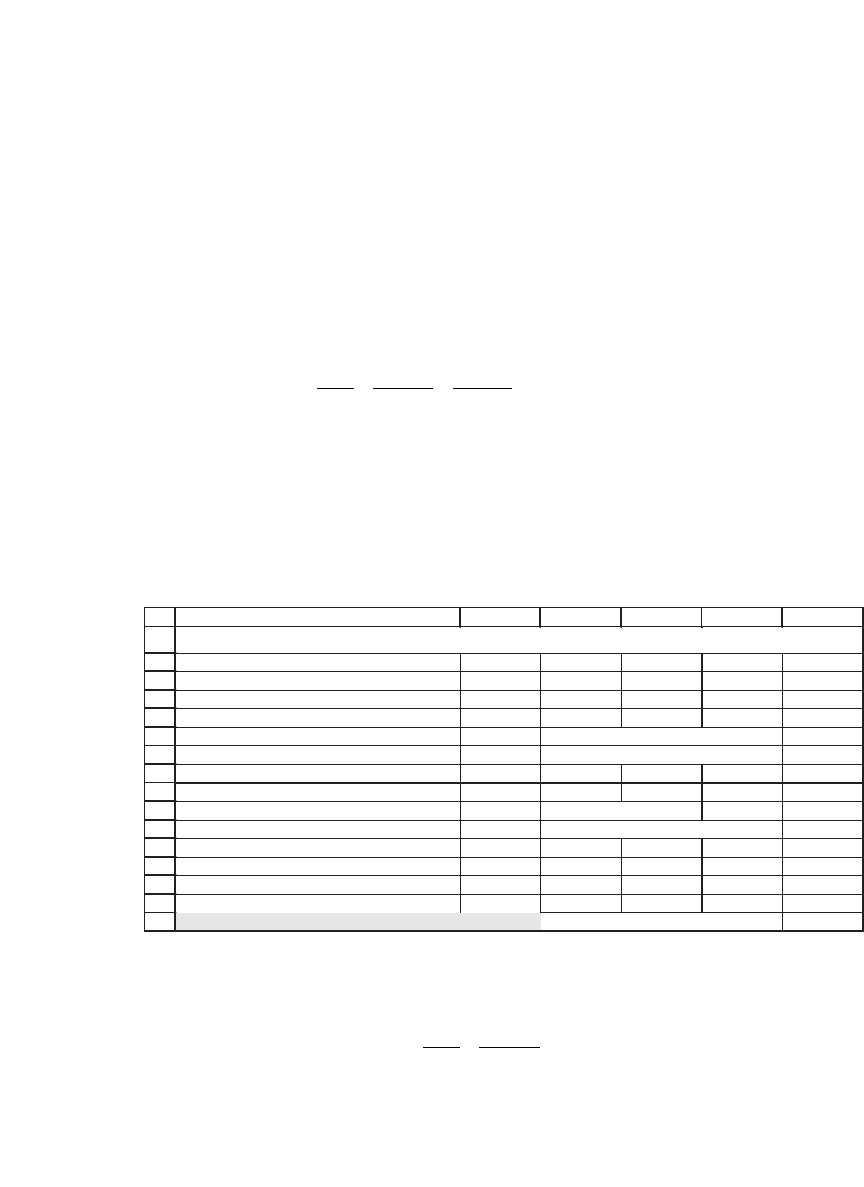

put options. Consider the following example: You are valuing a four-year

project with the expected cash fl ows given in the following spreadsheet

and with a risk-adjusted discount rate of 12 percent. As you can see, the

project has a negative NPV:

1

2

3

4

5

6

7

BACDE

Pro

F

ject cash flows

Year

01234

Cash flow -750 100 200 300 400

Risk-adjusted discount rate 12% The project's cost of capital

NPV without options -33.53 <-- =B4+NPV(B6,C4:F4)

STANDARD DCF PROJECT VALUATION

660 Chapter 24

Suppose that we can abandon the project at the end of any of the next

four years, selling the equipment for 300. Although this abandonment

option is an American option and not a Black-Scholes option, we value

it as a series of Black-Scholes put options. In each case we suppose that

we fi rst get the year-end cash fl ow; we then value the abandonment

option on the remaining project value.

•

End of year 1: The asset’s expected value at the end of year 1 will

be the discounted value of its future expected cash fl ows:

702 44

200

112

300

112

400

112

23

.

.(.)(.)

=+ +

. The abandonment option means that

we can get $300 for the asset during the next three years. Suppose that

the value has a volatility of 50 percent; then valuing this option as a

Black-Scholes put with one year to maturity gives its value as 19.53. The

following spreadsheet uses the VBA function BSPut defi ned in Chapter

19:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

BACDE

F

Project cash flows

Year 01234

Cash flow -750 100 200 300 400

Risk-adjusted discount rate 12% The project's cost of capital

NPV without options -33.53 <-- =B4+NPV(B6,C4:F4)

Valuing the year-1 abandonment put

Value of project, end year 1 702.44 <-- =NPV(B6,D4:F4)

Abandonment value 300 Like strike price in put formula

Time to option maturity (years) 3

Risk-free rate 6%

Sigma 50%

Put value 19.53 <-- =bsput(B10,B11,B12,B13,B14)

ABANDONMENT VALUE--DETAILS OF YEAR-1 CALCULATION

•

End of year 2: We have a put option with exercise price $300 on an

asset worth

586 73

300

112

400

112

2

.

.(.)

=+

. Valuing the abandonment option as

a Black-Scholes put with two years to exercise gives its value (when

σ = 50 percent) as 17.74.

661 Real Options

•

End of year 3: We have a put option with exercise price $300 on an

asset worth

357 14

400

112

.

.

=

. The option has one more year remaining to

its life and is worth 32.47.

•

End of year 4: The asset is worthless in terms of future anticipated cash

fl ows, but it can be abandoned for $300 (this is thus its scrap or salvage

value). The abandonment option is worth $300.

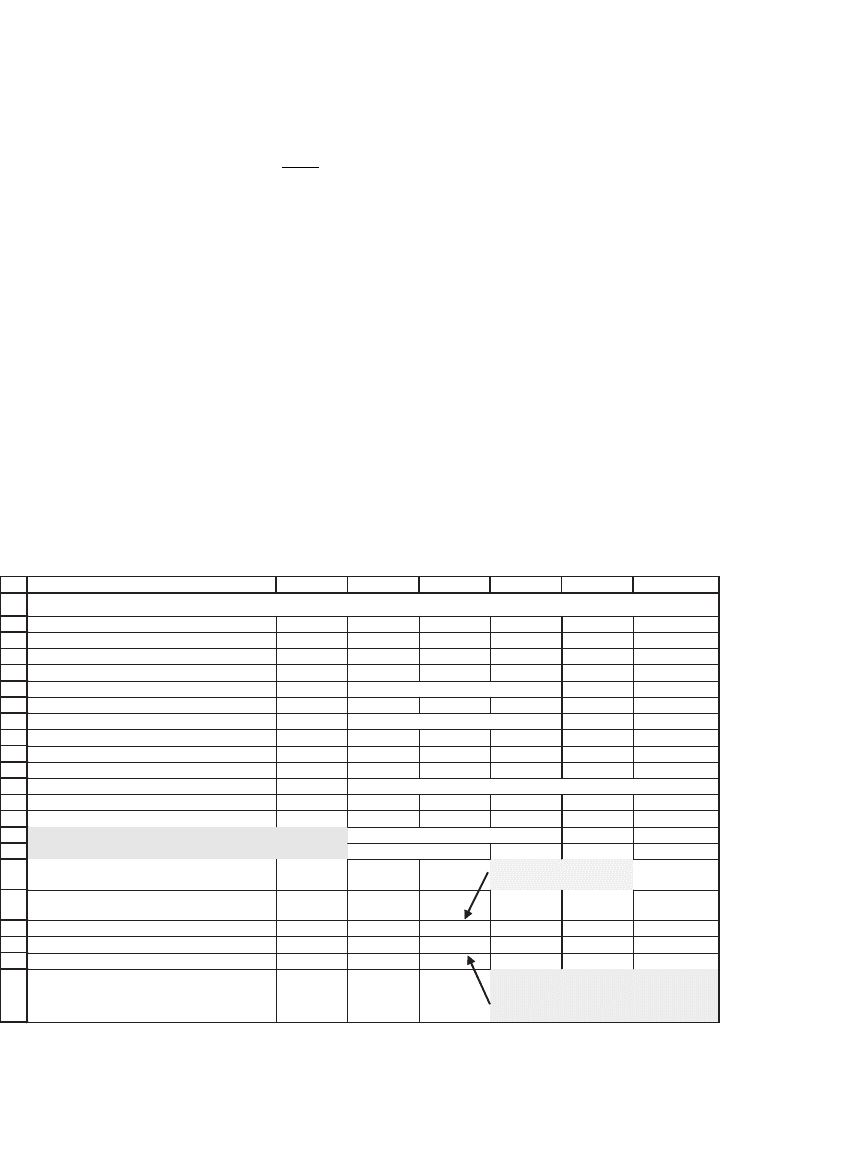

In the next spreadsheet the asset has been valued as the sum of

•

The present value of the future expected cash fl ows. As we showed, this

is −$33.53.

•

The present value (at the risk-free rate) of a series of Black-Scholes

puts. This value is $299.10.

The total value of the project is −$33.53 + $299.10 = $265.57.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

BACDEF

G

Project cash flows

Year 01234

Cash flow -750 100 200 300 400

Risk-adjusted discount rate 12% The project's cost of capital

NPV without options -33.53 <-- =NPV(B6,C4:F4)+B4

Sigma 50%

Risk-free rate 6%

Abandonment value 300 Project can be abandoned at end of any year for this amount

NPV of cash flows at RADR -33.53 <-- =B8

Value of abandonment option 299.10 <-- =NPV(B11,C20:F20)

Adjusted present value 265.57 <-- =B15+B14

End-year value of remaining cash flows 702.44 586.73 357.14 0.00

Put option value 19.53 17.74 32.47 300.00

Function in cell D19:

=NPV($B$6,E4:$F$4)

Function in cell D20:

=bsput(D19,$B$12,$F$3-

D3,$B$11,$B$10)

PRICING AN ABANDONMENT OPTION AS A SERIES OF PUTS

662 Chapter 24

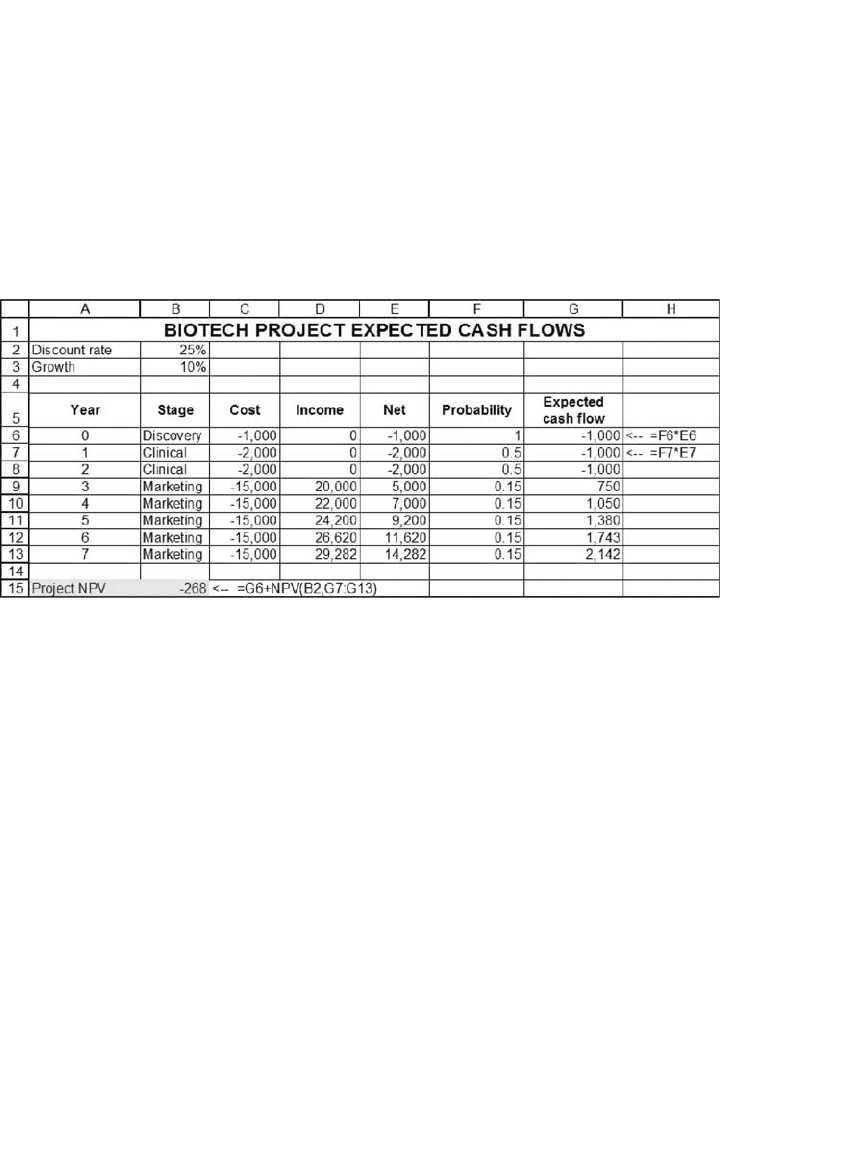

24.5 Valuing a Biotechnology Project

4

One of the interesting features of the biotech industry is the existence

of highly valued fi rms that have no revenues. It is common understanding

that the value of those fi rms is in their future cash fl ow opportunities.

Therefore, understanding the translation of qualitative investment

opportunities into quantitative valuation is of great importance when

valuating those fi rms. In this section we use the real-option method to

value a biotechnology project and to illustrate the application of the

real-option approaches.

Consider the following story.

5

A fi rm is considering the initiation of

research into a new drug. It knows that there are three stages to the

drug’s development:

1. In the discovery phase the fi rm does preliminary research about the

viability of the idea. This research takes one year and costs $1,000 at

the beginning of the year, with 50 percent probability that the results

will be positive enough to proceed to the next stage of research.

2. If the discovery phase yields success, then the drug goes into the clini-

cal phase, in which the drug is tested. This stage lasts one year, costs

$2,000 at the beginning of the year, and with a probability of 30 percent

yields enough positive results to proceed to the next stage.

3. If the drug passes the clinical phase successfully, then it goes into the

market stage, in which it is sold. This phase costs $15,000 per year (at the

beginning of each year) and on average lasts fi ve years. On average, a

successful drug can be expected to start the marketing phase with income

of $20,000. This income grows with annual mean 10 percent and standard

deviation σ = 100 percent.

The expected return on a project of this type is 25 percent. We assume

that this is the cost of capital of the project in the case of a discounted-

cash-fl ow (DCF) valuation.

4. A version of this example originally appeared in Benninga and Tolkowsky (2002).

5. We have made the story simple enough to fi t an understandable spreadsheet. For a

somewhat more complicated story in the same spirit, see Kellogg and Charnes

(2000).

663 Real Options

24.5.1 The Expected Value of the Project Using Traditional Discounted-

Cash-Flow Analysis

If we estimate the value of this project using traditional discounted-cash-

fl ow analysis, we get a negative net present value for the project:

Since the project’s net present value is negative, the DCF approach

indicates that it should not be undertaken.

24.5.2 Using a Real-Options Approach

An alternative method for estimating the present value of proceeds is

to plot the project’s cash fl ows on a binomial tree. This is done in the

following spreadsheet:

664 Chapter 24

We use the Excel function Sumproduct to do this computation.

24.5.3 A Note about the State Prices

The net present value of the proceeds from this project is the product

of the net cash fl ows and the appropriate state prices:

NPV CF q q

jt

j

t

t

U

j

D

tj

=∗∗∗

⎛

⎝

⎜

⎞

⎠

⎟

==

−

∑∑

00

7

()()

Number of

paths to node

,,

where CF

jt

denotes the proceeds from the project at date t and state j,

and where j is the number of up moves. As explained in Chapter 17, in the

665 Real Options

standard binomial model, the state price for a node is

()() ,qq

t

j

U

j

D

nj

∗

⎛

⎝

⎜

⎞

⎠

⎟

−

where n is the time at which the node occurs, j is the number of Up steps

needed to get to the node, and

t

j

⎛

⎝

⎜

⎞

⎠

⎟

is the number of paths to reach the

node. The latter expression is computed in Excel by using the function

Combin(n,j). However, for the preceding real-options model, the number

of paths to each node is slightly different, since the beginning of the tree

(the initial and clinical states) are accessible via only one path.

In the preceding spreadsheet, the prices q

U

and q

D

were computed

(using Solver) so that the present value of the project on the binomial tree

equals that of the DCF valuation and that the equilibrium condition,

qq

UD

+=

1

106.

holds. Here’s the Solver screen:

666 Chapter 24

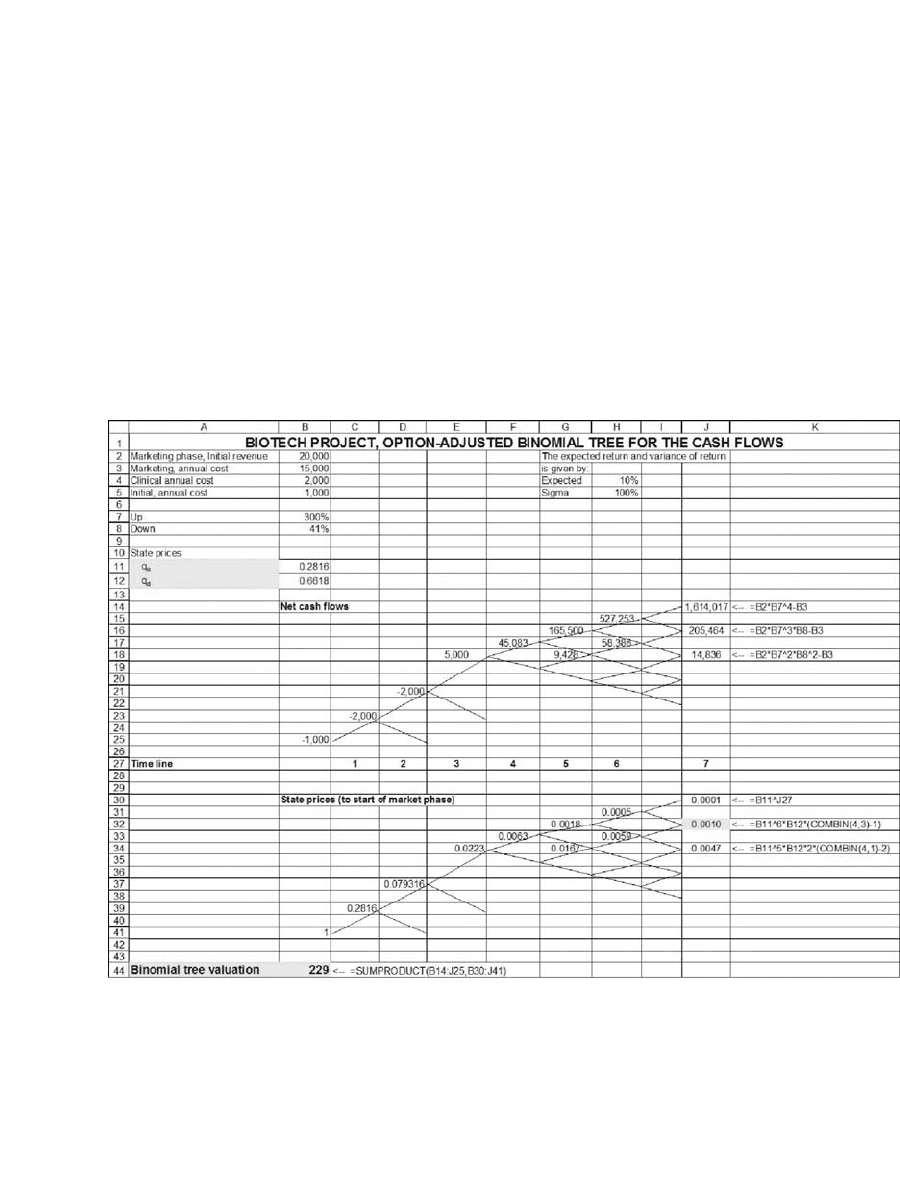

24.5.4 The Real-Options Approach

The real-options approach to R&D recognizes that at each stage in the

project the managers can choose whether to continue the project or not.

They do this by comparing the value and costs of continuation. In option

terminology, at each stage, the manager exercises her continuation option

if the value from exercising the option exceeds the exercise price. In the

following spreadsheet, we have eliminated obvious negative cash fl ows

from the marketing stage, taking care to also eliminate the subsequent

cash fl ows and to make an adjustment to the state prices:

24.5.5 Another Note about State Prices

When we eliminate states in the real-option approach, we must also

adjust the number of paths to each node to account for the fact that some

states are no longer reachable. This has been done in the preceding

667 Real Options

spreadsheet. For example, the state in cell J7 (highlighted) is now reach-

able by one fewer path.

24.6 Conclusion

Recognizing that capital budgeting should include option aspects of

projects is clear and obvious. Valuing these options is often diffi cult. In

this chapter we have tried to emphasize the intuitions and—insofar as is

possible—to give some implementation of the valuation.

Exercises

1. Your company is considering purchasing 10 machines, each of which has the follow-

ing expected cash fl ows (the entry in B4 of −$550 is the cost of the machine):

You estimate the appropriate discount rate for the machines as 25 percent.

a. Would you recommend buying just one machine, if there are no options

effects?

b. Your purchase manager recommends buying one machine today and then—after

seeing how the machine operates—reconsidering the purchase of the other nine

machines in six months. Assuming that the cash fl ows from the machines have a

standard deviation of 30 percent and that the risk-free rate is 10 percent, value

this strategy.

2. Your company is considering the purchase of a new piece of equipment. The equip-

ment costs $50,000, and your analysis indicates that the PV of the future cash fl ows

from the equipment is $45,000. Thus the NPV of the equipment is −$5,000. This

estimated NPV is based on some initial numbers provided by the manufacturer plus

some creative thinking on the part of your fi nancial analyst.

The seller of the new piece of equipment is offering a course on how it works.

The course costs $1,500. You estimate that

•

The σ of the equipment’s cash fl ows is 30 percent.

•

The risk-free rate is 6 percent.

•

You will have another half year after the course to purchase the equipment at

the price of $50,000.

Is it worth taking the course?

3

4

FEDCBA

43210raeY

CF of sing 004003002001055-enihcamel