Simon Benninga. Financial Modelling 3-rd edition

Подождите немного. Документ загружается.

218 Chapter 6

What does the lessor do if the lessee has to record the lease on his

balance sheet? If the lessee has (in an accounting sense) bought the asset

with 100 percent loan fi nancing, then the lessor must have (in the same

sense) sold the asset with 100 percent loan fi nancing. This is the essence

of the FASB 13 treatment of the lessor.

Reconciling the Tax and Accounting Treatments of Leases

The tax treatment and the accounting treatment of leases are very similar

in spirit. It is therefore logical to expect that whenever a lease is classifi ed

under the FASB 13 rules as a capital lease, it should be classifi ed by the

IRS as a sale. Thus, if the world were a rational place, lessees would put

leases on their books only if the IRS decided to treat leases as sales.

However, the world is a funny place. It turns out to be fairly simple to

keep a lease off the lessee’s balance sheet, have the IRS treat it as a true

lease, and still have all the parties involved feel as if they had transferred

all of the economic benefi ts of ownership from the lessor to the lessee.

See the references for further reading.

7

The Financial Analysis of Leveraged Leases

7.1 Overview

In Chapter 6 we analyzed the lease-versus-purchase decision from

the points of view of both the lessee (the long-term user of the asset)

and the lessor (the asset’s owner, who rents it out to the lessee). In

this chapter we analyze leveraged leasing: In a leveraged lease the

lessor fi nances the purchase of the asset to be leased with debt. From

the point of view of the lessee, there is no difference in the analysis of

a leveraged or a nonleveraged lease. From the lessor’s point of view,

however, the cash fl ows of a leveraged lease present some interesting

problems.

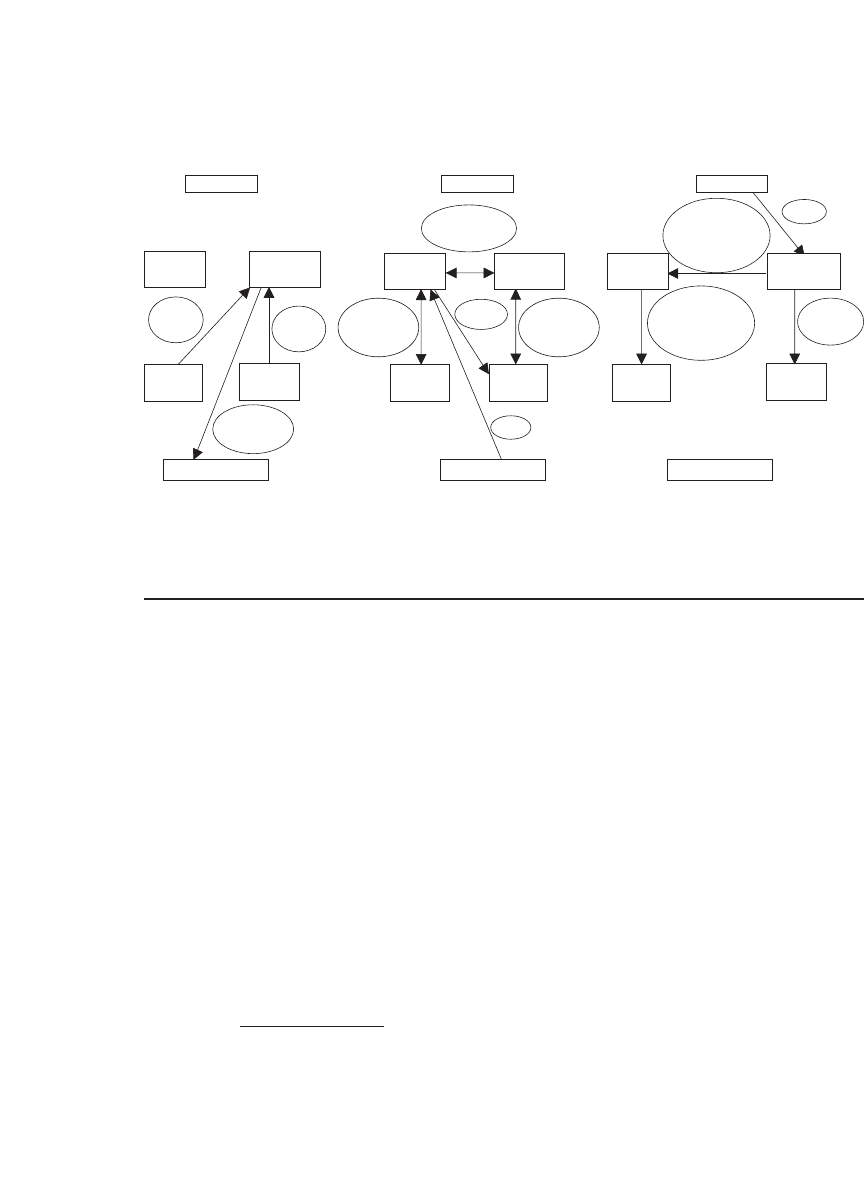

At least six parties are typically involved in a leveraged lease: the

lessee, the equity partners in the lease, the lenders to the equity partners,

an owner trustee, an indenture trustee, and the manufacturer of the asset.

In most cases, a seventh party is also involved: a lease packager (a broker

or leasing company). Figure 7.1 illustrates the arrangements among the

six parties of a typical leveraged lease.

The two major problems related to the analysis of leveraged leases are

these:

1. The straightforward fi nancial analysis of the lease from the point of

view of the lessor. This concerns the calculation of the cash fl ows obtained

by the lessor, and a computation of these cash fl ows’ net present value

(NPV) or internal rate of return (IRR).

2. The accounting analysis of the lease. Accountants use a method

called the multiple phases method (MPM) to calculate a rate of return

on leveraged leases. The MPM rate of return is different from the inter-

nal rate of return (IRR). In an ordinary fi nancial context this difference

should be of no concern, since the effi cient-markets hypothesis tells us

that only cash fl ows matter. However, in a less than effi cient world,

people tend to get very concerned about how things look on their fi nan-

cial statements. Since the accounting rate of return on the lease is diffi cult

to compute, we will use Excel to calculate it; then we will analyze the

results.

220 Chapter 7

7.2 An Example

We can explore these issues by considering an example, roughly based

on an example given in appendix E of FASB 13, the accounting profes-

sion’s magnum opus on accounting for leases.

A leasing company is considering the purchase of an asset whose cost

is $1,000,000. The asset will be purchased with $200,000 of the company’s

equity and with $800,000 of debt. The interest on the debt is 10 percent,

so that the annual payment of interest and principal over the 15-year

term of the debt is $105,179.

1

The company will lease the asset out for $110,000 per year, payable at

the end of each year. The lease term is 15 years. The asset will be depreci-

ated over a period of eight years, using the standard IRS depreciation

schedule for assets with a seven-year life.

2

The depreciation schedule for

such assets is as follows:

Purchase Price Agreements Rent Payments

Lessee Lessee Lessee

Owner

trustee

Indenture

trustee

Owner

trustee

Indenture

trustee

Owner

trustee

Indenture

trustee

Lessor:

equity

Lessor:

equity

Lessor:

equity

Lessor:

lenders

Lessor:

lenders

Lessor:

lenders

Manufacturer Manufacturer Manufacturer

Equity

funds

Purchase

price

Debt

funds

Trust

agreement

Trust

agreement

Bonds

Title

Assignment

of rent

Debt

service

Excess of

rent over

debt service

Excess of

rent over

debt service

Rent

Figure 7.1

Leveraged leasing.

1. Using Excel: =PMT(10%,15,-800000) gives 105,179.

2. The depreciation schedule we use is referred to as the modifi ed cost recovery system

(MACRS) depreciation. More information can be obtained from an introductory

fi nance text or from many Web sites (one example: http://www.real-estate-owner.com/

depreciation-chart.html).

221 The Financial Analysis of Leveraged Leases

Year Depreciation (%)

1 14.28

2 24.49

3 17.49

4 12.5

5 8.92

6 8.92

7 8.92

8 4.48

Because the asset will be fully depreciated at the time it is sold (year 16),

the whole anticipated residual value ($300,000) will be taxable. Since the

company’s tax rate is 40 percent, the after-tax cash fl ow from the residual

is (1 − 40%)

*

300,000 = $180,000.

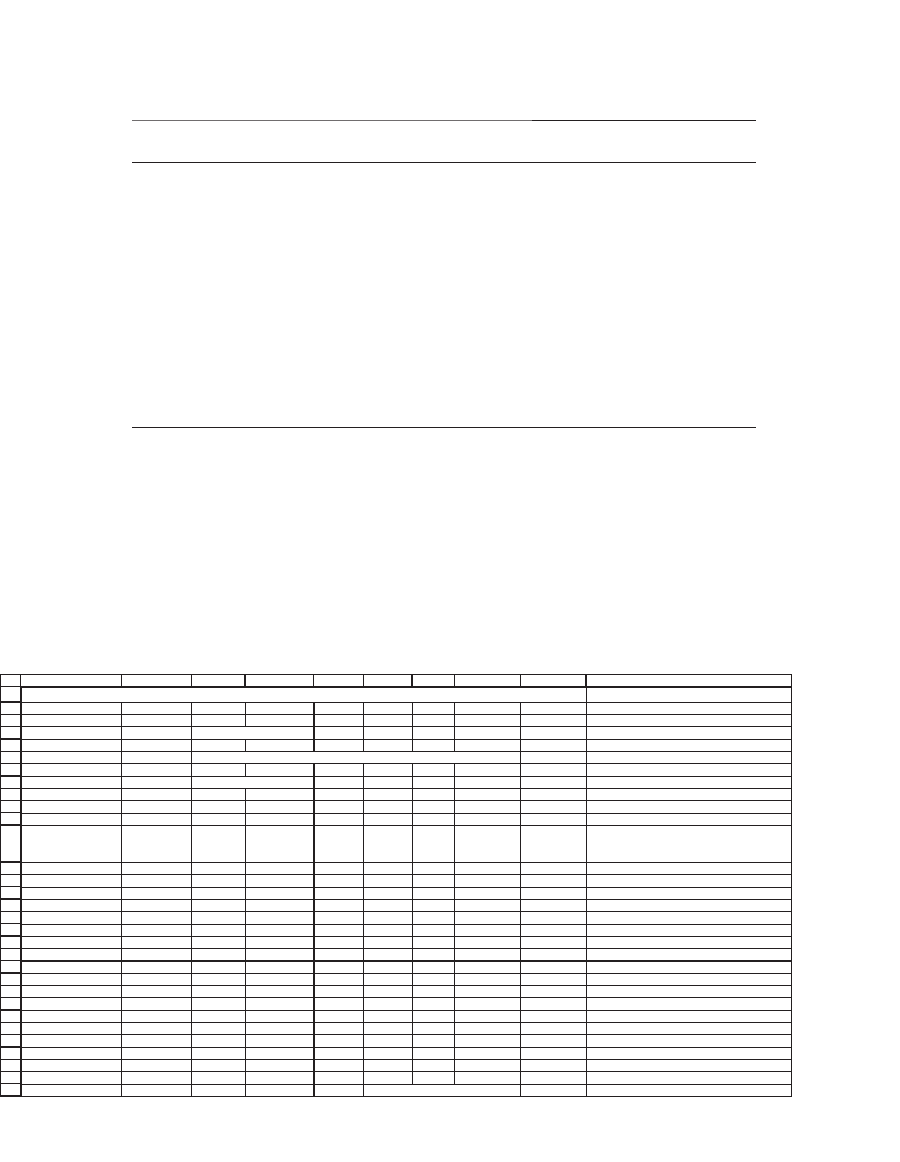

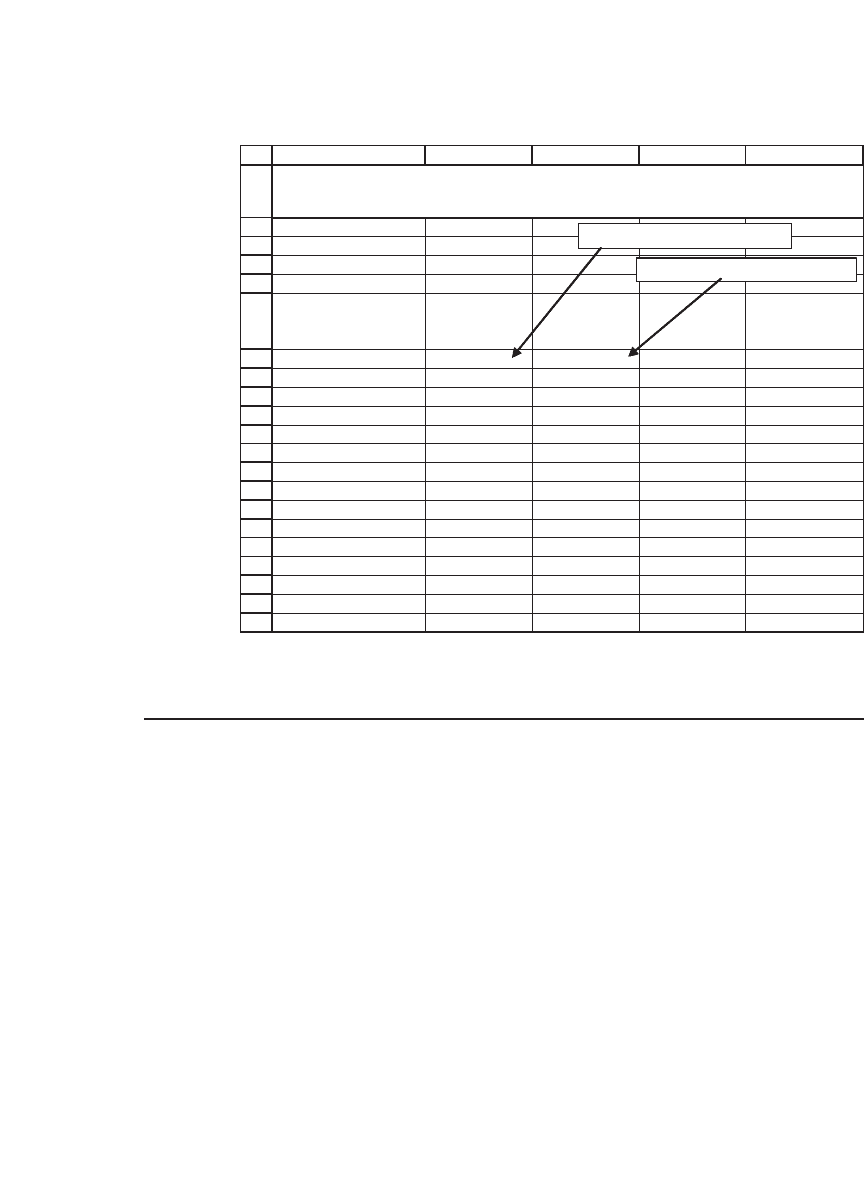

These facts are summarized in the following spreadsheet, which also

derives the lessor’s cash fl ows:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

ABCDEFGHI J

Cost of asset 1,000,000

Lease term 15

Residual value 300,000 <-- Realized year 16

Equity 200,000

Debt 800,000 <-- 15-year term loan, equal payments of interest and principal

Interest 10%

Annual debt payment 105,179 <-- =PMT(B7,B3,-B6)

Annual rent received 110,000

Tax rate 40%

Year

Equity

Invested

Rental or

salvage

Depreciation

Principal

at start

of

year

Loan

payment

Interest

Repayment

of principal

Cash flow to

equity

-200,000 -200,000

1 110,000 142,800 800,000 105,179 80,000 25,179 49,941 <-- =(1-tax)*C14+tax*D14-(1-tax)*G14-H14

2 110,000 244,900 774,821 105,179 77,482 27,697 89,774

3 110,000 174,900 747,124 105,179 74,712 30,467 60,666

4 110,000 125,000 716,657 105,179 71,666 33,513 39,487

5 110,000 89,200 683,144 105,179 68,314 36,865 23,827

6 110,000 89,200 646,280 105,179 64,628 40,551 22,352

7 110,000 89,200 605,728 105,179 60,573 44,606 20,730

8 110,000 44,800 561,122 105,179 56,112 49,067 1,186

9 110,000 512,056 105,179 51,206 53,973 -18,697

10 110,000 458,082 105,179 45,808 59,371 -20,856

11 110,000 398,711 105,179 39,871 65,308 -23,231

12 110,000 333,403 105,179 33,340 71,839 -25,843

13 110,000 261,565 105,179 26,156 79,023 -28,716

14 110,000 182,542 105,179 18,254 86,925 -31,877

15 110,000 95,617 105,179 9,562 95,617 -35,354

16 300,000 180,000

IRR of cash flows 12.46% <-- =IRR(I13:I29)

BASIC LEVERAGED LEASE EXAMPLE

222 Chapter 7

The last column gives the cash fl ow to the equity owners of the

asset. A typical year’s cash fl ow for the equity owner is calculated as

follows:

Cash fl ow (t) = (1 − Tax) Rent + Tax

*

Depreciation(t)

− (1 − Tax)Interest(t) − Principal repayment(t)

The explanation is as follows:

Item Explanation

+ (1 − Tax)

*

Rent

Equity owners get the rental from the

asset, net of any taxes.

+ Tax

*

Depreciation

Equity owners get the tax shield from

the depreciation of the asset.

− (1 − Tax)

*

Interest

The interest on the debt is tax

deductible.

− Repayment of debt

principal

Repayment of debt principal is not tax

deductible.

+ (1 − Tax)

*

Residual value

This item only occurs in the last year;

the residual is usually fully taxed, since

the depreciation has been taken on the

whole value of the asset.

Cash fl ow (t) = (1 − Tax)

*

Rent + Tax

*

Depreciation(t)

− (1 − Tax)

*

Interest(t)

− Principal repayment(t)

The cash fl ow in a typical year

(excluding the residual).

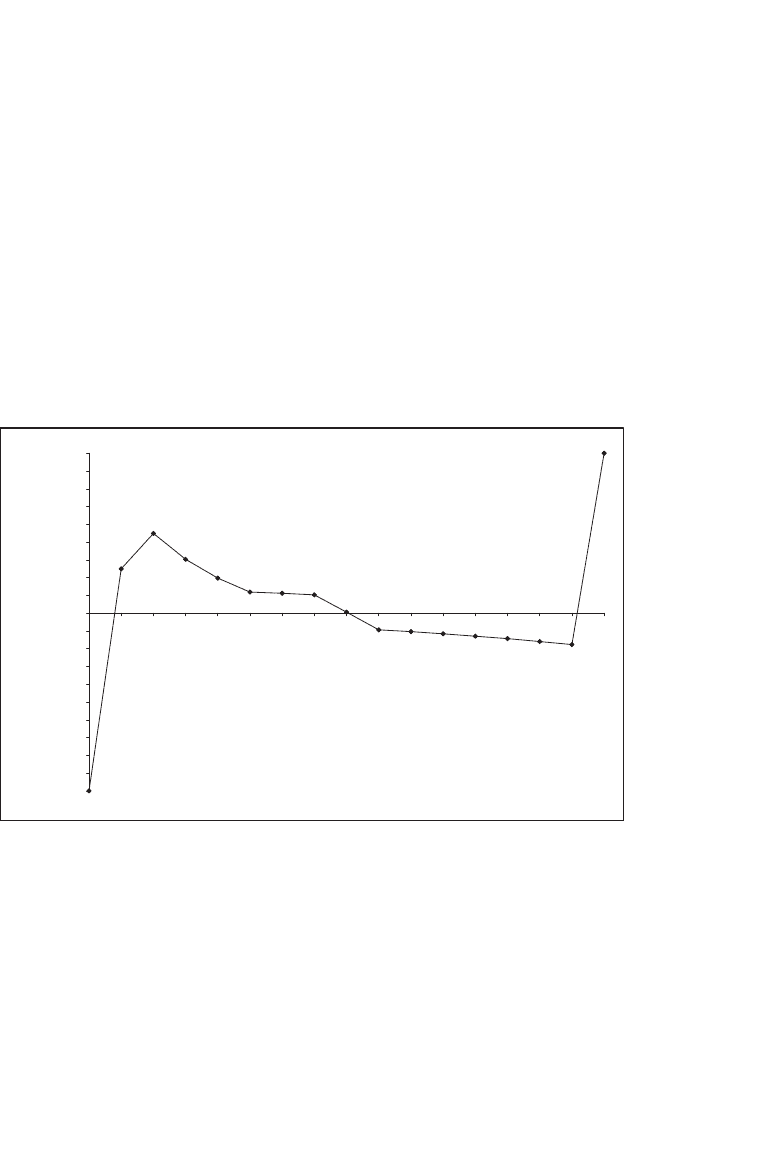

The cash fl ows of the typical long-lived leveraged lease are usually

positive at the beginning of the lease term, and then decline over time,

turning positive again at the end, when the residual value is received.

There are three reasons for this phenomenon:

•

The cash fl ow that stems from depreciation typically ends or falls off

rapidly before the end of the lease term. The more accelerated the depre-

ciation method is, the larger the depreciation allowances (and hence the

223 The Financial Analysis of Leveraged Leases

larger the depreciation tax shields) will be at the beginning of the asset’s

life.

•

In the later years of the lease, the portion of the annual debt payments

devoted to interest (tax-deductible) falls, while the portion of the annual

debt payments that constitutes a repayment of principal (not tax deduct-

ible) rises.

•

Finally, of course, we anticipated a large cash fl ow from the realization

of the asset’s residual value at the end of the lease term.

Cash Flows from Leveraged Lease

-200,000

-180,000

-160,000

-140,000

-120,000

-100,000

-80,000

-60,000

-40,000

-20,000

Cash flow ($)

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Year

7.2.1 Digression: Computing the Interest Payments and Principal Repayments

In the preceding lease cash-fl ow spreadsheet, we computed the interest

payments and principal repayments on the $800,000 debt by building a

loan table (explained in Chapter 1, p. 12). We could also build this table

by using the two Excel functions IPMT and PPMT, which compute the

interest and principal payments on a term loan. An illustration is in the

following spreadsheet:

224 Chapter 7

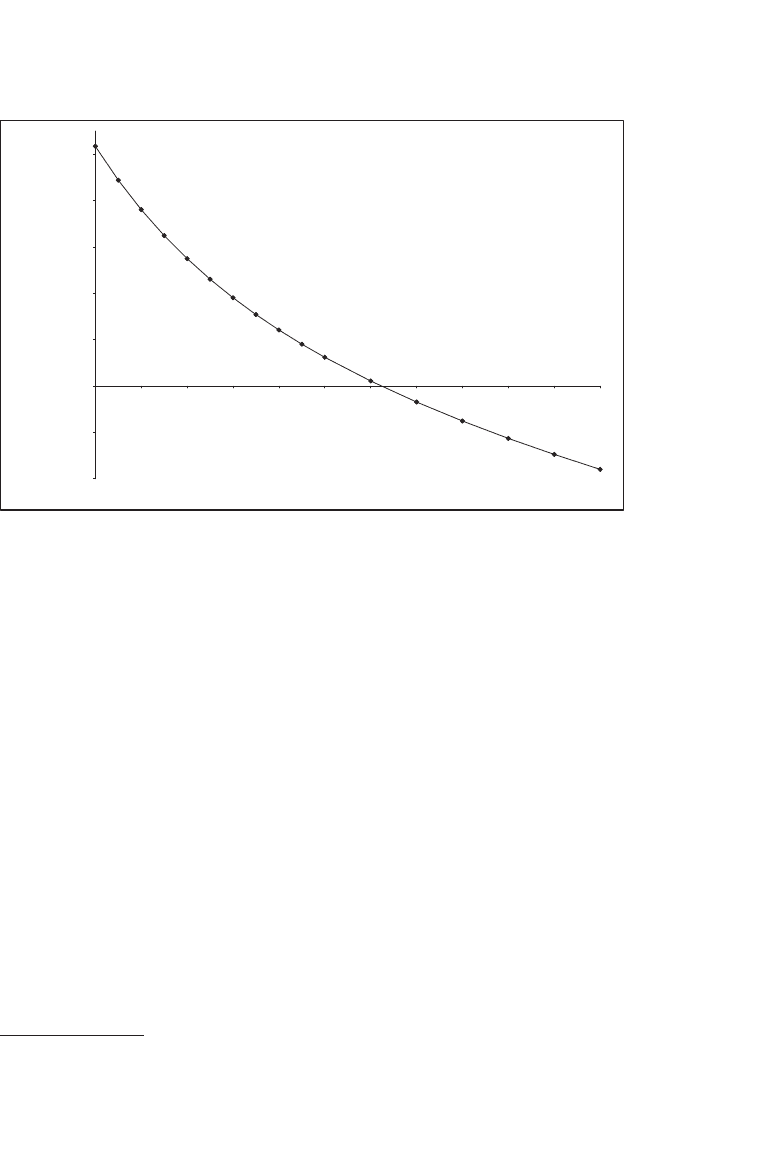

7.3 Analyzing the Cash Flows by NPV or IRR

What do we make of the leveraged-lease cash fl ows? One way of viewing

the cash fl ows (probably the best, at least in theory) is to take their net

present value (NPV) at some appropriate risk-adjusted discount rate. If

we analyze the cash-fl ow components, we see that the primary riskiness

stems from three sources:

•

The lessee may default on the rental.

•

Tax rates can change, affecting the tax shields from depreciation and

the cash fl ow from the interest payments.

•

The residual value is highly uncertain.

The following graph shows the NPV of the cash fl ows at various interest

rates:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

ABCDE

Debt 800,000

Debt term (years) 15

Interest 10%

Year

Interest

payment on

debt

Debt

principal

re

payment

Total

payment

1 80,000 25,179 105,179 <-- =B7+C7

2 77,482 27,697 105,179

3 74,712 30,467 105,179

4 71,666 33,513 105,179

5 68,314 36,865 105,179

6 64,628 40,551 105,179

7 60,573 44,606 105,179

8 56,112 49,067 105,179

9 51,206 53,973 105,179

10 45,808 59,371 105,179

11 39,871 65,308 105,179

12 33,340 71,839 105,179

13 26,156 79,023 105,179

14 18,254 86,925 105,179

15 9,562 95,617 105,179

COMPUTING THE LOAN PAYMENTS

USING IPMT AND PPMT

=IPMT($B$4,A7,$B$3,-$B$2)

=PPMT($B$4,A7,$B$3,-$B$2)

225 The Financial Analysis of Leveraged Leases

Note that since the cash fl ows are after-tax, the relevant basis for com-

parison is an after-tax interest rate. Suppose, for example, that the lessor

feels highly certain about all the cash fl ows and therefore wants to

compare the cash fl ows to his loan rate of 10 percent. Then, since the

lessor’s tax rate is 40 percent, the appropriate discount rate for compari-

son is (1 − 40 percent)

*

10 percent = 6 percent; at this rate the lease cash

fl ows have an NPV of $38,068.

Lessors are often uncomfortable with net present value. They prefer

internal rate of return as a measure of the acceptability of the lease. Since

the cash fl ows of the leveraged lease have three changes in sign, it is—in

principle—possible that they have three IRRs.

3

Since the IRR is the

interest rate for which the net-present-value graph crosses the x-axis, we

can use Excel to determine graphically how many IRRs there are. The

graph shows that for a very large range of reasonable interest rates, there

is only one IRR. We are thus safe in using IRR(cash fl ows,0) to deter-

mine that the internal rate of return of the lease cash fl ows is 12.46

percent.

Are There Multiple IRRs? (No!)

This chart shows the NPV of the leveraged-lease cash flows

for various discount rates

-40,000

-20,000

0

20,000

40,000

60,000

80,000

100,000

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20% 22%

Discount rate

NPV

3. Cash-fl ow sign changes: From negative in year 0 to positive in year 1; from positive in

year 8 to negative in year 9; from negative in year 15 to positive in year 16.

226 Chapter 7

7.4 What Does the IRR Mean?

Asking what the IRR means is relevant both to an economic understand-

ing of the meaning of the internal rate of return and to the discussion in

section 7.5 of the accounting determination of the income from a lever-

aged lease.

To illustrate the complexities, we stray for a moment from our original

example to study a much simpler example. Consider an investment of

$100,000 that has positive cash fl ows only for the next fi ve years:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

AB C DE F

Year

Cash

flow

0 -100,000

1 31,000

2 22,000

3 16,000

4 22,000

5 35,000

IRR 8.097% <-- =IRR(B3:B8,0)

Year

Investment at

beginning of

p

eriod

Cash flow at end of

year

Income

Repayment

of

investment

1 100,000 31,000 8,097 22,903 <-- =C15-D15

2 77,097 22,000 6,242 15,758

3 61,339 16,000 4,966 11,034

4 50,305 22,000 4,073 17,927

5 32,378 35,000 2,622 32,378

UNDERSTANDING THE IRR

CASH FLOW ATTRIBUTION TABLE

Attribution of cash flow

=B16-E16 =$B$11*B16

What is the meaning of the IRR of 8.097 percent? If we think of the

initial investment of $100,000 as a loan to the project, then each year’s

cash fl ow is attributable to

1. Income on the investment outstanding at the beginning of the

year. In rows 15–19 we compute this by taking the project’s IRR

times the investment at the beginning of the period. This method

parallels the computation of the annual interest on a loan illustrated on

page 224.

227 The Financial Analysis of Leveraged Leases

2. Repayment of the investment. This is the remainder of the cash fl ow

after the income and parallels the repayment of the loan in the same

loan table.

Of course, at the end of the fi ve years, all the principal must be repaid.

The IRR is the “rate of interest” that exactly repays the “loan” (that is, the

investment) with its “interest payments”(the income) over the life of the

project.

Here is an example:

Investment at beginning of period 1 (i.e.,

the initial investment)

100,000

Cash fl ow for period 31,000

8.097 percent

*

Investment at beginning of

period

8,097

Cash fl ow available for repayment of

investment

22,903

Investment at beginning of period 2

= Investment at beginning of previous

period

− Cash fl ow available for repayment in

period 1

100,000 − 22,903 = 77,097

Note the last line in our cash-fl ow attribution table: At the beginning of

year 5, we still have $32,378 of investment left; the cash fl ow of $35,000

for year 5 suffi ces exactly to pay the income of $2,622 on this investment

and to repay the investment itself. At the beginning of year 6, there is no

investment left! (This result, of course, is not a miracle—it’s the way we

calculated the internal rate of return.)

There’s another way to calculate the investment at the beginning of

each period: As the following spreadsheet shows, the investment at the

beginning of each period is the present value of all remaining future cash

fl ows, where we use the project’s IRR as the discount rate: