Principles of Finance with Excel (Основы финансов c Excel)

Подождите немного. Документ загружается.

PFE Chapter 19, Stock valuation page 2

Overview

In Chapter 17 we discussed the valuation of bonds. This chapter deals with the valuation

of stocks. Whereas the valuation of bonds is a relatively straightforward matter of computing

yields to maturity, the valuation of stocks is much more difficult. The difficulty lies both in the

greater uncertainty about the cash flows which need to be discounted in order to arrive at a stock

valuation and in the computation of the correct discount rate.

In this chapter we discuss four basic approaches to stock valuation:

• Valuation method 1, the efficient markets approach. In its simplest form the

efficient markets approach states that the current stock price is correct. A somewhat

more sophisticated use of the efficient markets approach to stock valuation is that a

stock’s value is the sum of the values of its components. We explore the implications

of these statements in Section 19.1.

• Valuation method 2, discounting the future free cash flows (FCF). Sometimes

called the discounted cash flow (DCF) approach to valuation, this method values the

firm’s debt and its equity together as the present value of the firm’s future FCFs. The

discount rate used is the weighted average cost of capital (WACC). This method is

the valuation approach favored by most finance academics. We discuss this approach

in Section 19.2 and discuss the computation of the WACC in Sections 19.5 and 19.6.

In this chapter we do not discuss the concept or the computation of the free cash

flow—this was done previously in chapters 6-7.

• Valuation method 3, discounting the future equity payouts. A firm’s shares can

also be valued by discounting the stream of anticipated equity payouts at an

PFE Chapter 19, Stock valuation page 3

appropriate cost of equity r

E

. The concept of equity payout (the sum of a firm’s total

dividends plus its stock repurchases) was previously discussed in Chapter 5.

• Valuation method 4, multiples. Finally we can value a firm’s shares by a

comparative valuation based on multiples. This very common method involves ratios

such as the price-earnings (P/E) ratio, EBITDA multiples, and more industry specific

multiples such as value per square foot of store space or value per subscriber.

With the exception of the multiple method 4, almost all of the material in this chapter is

also discussed elsewhere in this book. For example, the efficient markets approach to valuation

is also discussed in chapter 13, and the Gordon dividend model (which values a firm’s equity by

discounting its anticipated dividend stream) is also discussed in chapters 5 and 7. WACC

computations are to be found in Chapters 5 and 13. The purpose of this chapter is to bring

together these dispersed materials into a (hopefully coherent) whole.

Finance concepts discussed in this chapter

• Discounted cash flows, free cash flows (FCF)

• Cost of capital, cost of equity, cost of debt, weighted average cost of capital (WACC)

• Equity premium

• Beta, equity beta, asset beta

• Two-stage growth models

Excel functions used

• Sum, NPV, If

• Data table

PFE Chapter 19, Stock valuation page 4

19.1. Valuation method 1: The current market price of a stock is the correct

price (the efficient markets approach)

The simplest stock valuation is based on the efficient markets approach (chapter 13).

This approach says that the current market price of a stock is the correct price. In other words:

The market has already done the difficult job stock valuation, and it’s done this correctly,

incorporating all of the relevant information There’s a lot of evidence for this approach, as you

saw in chapter 13.

This valuation method is very simple to apply:

• Question: “IBM looks a bit expensive to me—it’s price has been going up for the last 3

months. What do you think: Is IBM’s stock price currently underpriced or overpriced?”

• Answer: “At Podunk U., we learned that markets with a lot of trading are in general

efficient, meaning that the current market price incorporates all the readily-available

information about IBM. So—I don’t think IBM is either underpriced or overpriced. It’s

actually correctly priced.”

Here’s another example of the use of this approach:

• Question: “I’ve been thinking of buying IBM, but I’ve have been putting it off. The

price has gone up lately, and I’m going to wait until it comes down a bit. It seems a bit

high to me right now.” What do you think?

• Answer: “At Podunk U. we would call you a contrarian . You believe that if the price of

a stock has gone up, it will go back down (and the opposite). But this technical approach

(see chapter 13) to stock valuation doesn’t seem to work very well. So if you want to buy

PFE Chapter 19, Stock valuation page 5

IBM, go ahead and do so now. There’s nothing in the price runup of the last couple of

months which indicates that there will now be a price rundown.”

Some more sophisticated efficient markets methods

Efficient markets valuations don’t always have to be as simplistic as the above examples.

In chapter 13 we looked at additivity, a fundamental tenet of efficient markets. The principle of

additivity says that the value of a basket of goods or financial assets should equal the sum of the

values of the components. Additivity can often be used to value stocks.

Here’s a very simple example: ABC Holding Corp., a publicly-traded company, owns

shares in two publicly traded companies. Besides owning these subsidiaries, ABC does little

else.

ABC HOLDING COMPANY

Owns:

60% of XYZ Widgets

50% of QRM Smidgets

ABC has 30,000 shares outstanding

XYZ Widgets

Market value of shares: $1,000,000

QRM Smidgets

Market value of shares: $875,000

Figure 19.1. Ownership structure of ABC Holding Company

PFE Chapter 19, Stock valuation page 6

What should be the value of a share of ABC Holding? The obvious way to do this is in

the following spreadsheet, which computes the share value of ABC to be $34.58:

1

2

3

4

5

6

7

8

9

ABCDE

Number of ABC shares 30,000

ABC owns shares in

Percentage

of shares

owned by

ABC

Market

value

Market value

of ABC

holdings

in company

XYZ Widgets 60% 1,000,000 600,000 <-- =B5*C5

QRM Smidgets 50% 875,000 437,500 <-- =B6*C6

Total value of ABC holdings 1,037,500 <-- =D6+D5

Per share value of ABC Holdings 34.58 <-- =D7/B2

ABC HOLDING COMPANY

Notice what this model is and is not telling you:

• Is telling you: If the market values of XYZ and QRM are correct, then the market value

of ABC should be $34.58. The formula works out to be:

[

]

[

]

60%* 50% *

ABC share

X

YZ value QRM value

number of

price

ABC shares

+

=

•

Is not telling you: The formula tells you a relation between the 3 share prices. It tells

you if the share prices are relatively correct, but it does not tell you if they are absolutely

correct. Example: After doing much work and research and applying the methods of the

previous Section, you come to the conclusion that, while the market valuation of QRM is

correct, the market value of XYZ ought to $1,600,000. Then you would conclude that

the share price of ABC ought to be $46.58.

PFE Chapter 19, Stock valuation page 7

1

2

3

4

5

6

7

8

9

ABCDE

Number of ABC shares 30,000

ABC owns shares in

Percentage

of shares

owned by

ABC

Market

value

Market value

of ABC

holdings

in company

XYZ Widgets 60% 1,600,000 960,000 <-- =B5*C5

QRM Smidgets 50% 875,000 437,500 <-- =B6*C6

Total value of ABC holdings 1,397,500 <-- =D6+D5

Per share value of ABC Holdings 46.58 <-- =D7/B2

ABC HOLDING COMPANY

Note that if ABC has some of its own overheads and if it doesn’t always pass through all

the dividends of its subsidiaries, its market price will be lower than $34.58, since the market

price of ABC will reflect not only the cost of the shares of its subsidiaries, but also its own

overheads. This looks a lot like the closed-end fund valuation problem discussed in chapter 13.

19.2. Valuation method 2: The price of a share is the discounted value of the

future anticipated free cash flows

Valuation method 1 of the previous section says that there is nothing to be gained by

second-guessing market valuations. In many cases, however, the finance expert (you!) will want

to do a basic valuation of a company and derive the value of a share from the discounted value of

the future anticipated free cash flows (FCF). This method, often called the discounted cash flow

(DCF) method of valuation, was discussed and illustrated in chapter 7. Figure 19.2 reminds you

of the definition of FCF and figure 19.3 gives a flow diagram of the FCF valuation method.

PFE Chapter 19, Stock valuation page 8

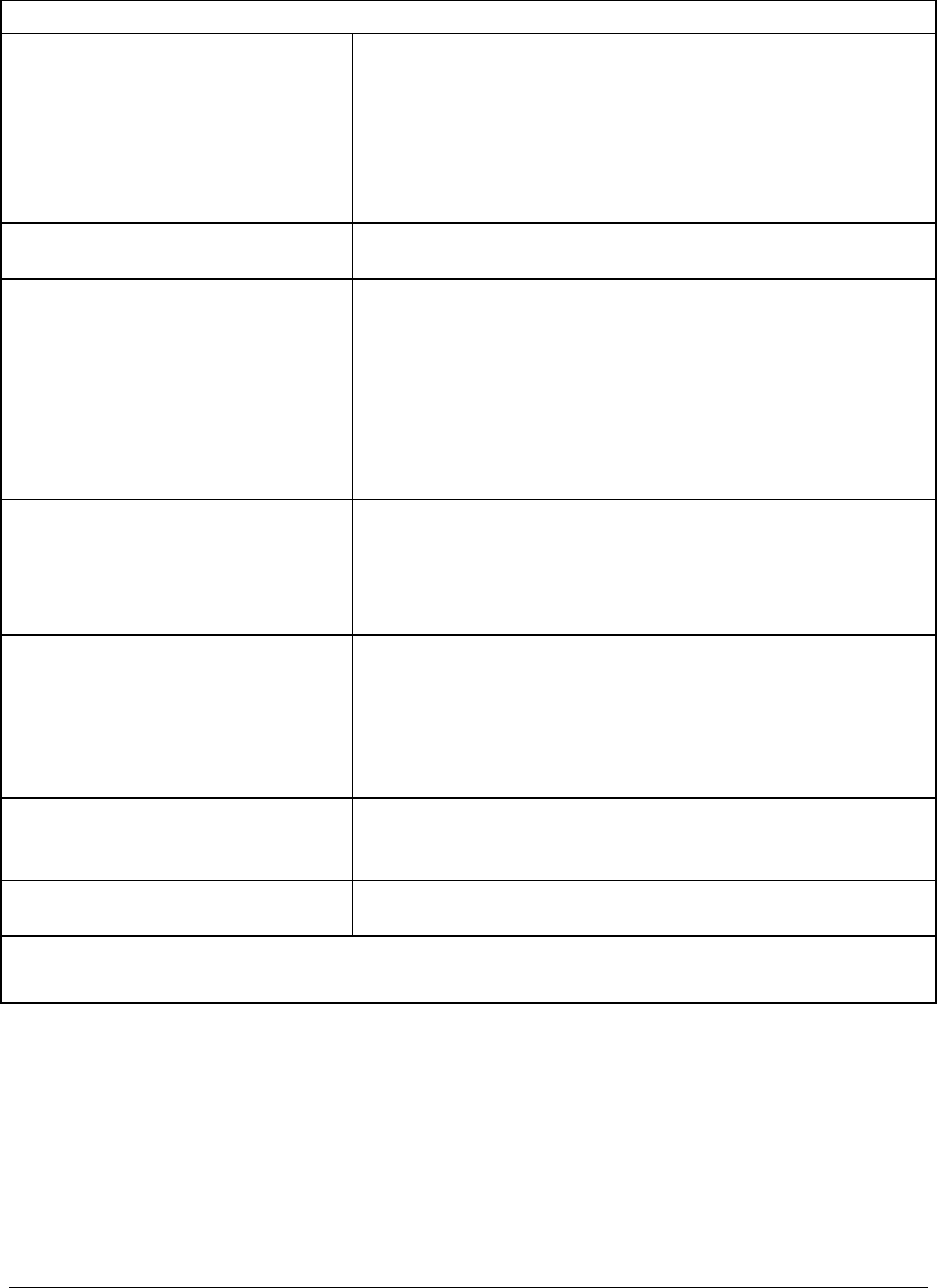

Defining the Free Cash Flow

Profit after taxes This is the basic measure of the profitability of the

business, but it is an accounting measure that includes

financing flows (such as interest), as well as non-cash

expenses such as depreciation. Profit after taxes does not

account for either changes in the firm’s working capital or

purchases of new fixed assets, both of which can be

important cash drains on the firm.

+ Depreciation This noncash expense is added back to the profit after tax.

+ after-tax interest payments (net) FCF is an attempt to measure the cash produced by the

business activity of the firm. To neutralize the effect of

interest payments on the firm’s profits, we:

• Add back the after-tax cost of interest on debt

(after-tax since interest payments are tax-

deductible),

•

Subtract out the after-tax interest payments on cash

and marketable securities.

- Increase in current assets When the firm’s sales increase, more investment is needed

in inventories, accounts receivable, etc. This increase in

current assets is not an expense for tax purposes (and is

therefore ignored in the profit after taxes), but it is a cash

drain on the company.

+ Increase in current liabilities An increase in the sales often causes an increase in

financing related to sales (such as accounts payable or taxes

payable). This increase in current liabilities—when related

to sales—provides cash to the firm. Since it is directly

related to sales, we include this cash in the free cash flow

calculations.

- Increase in fixed assets at cost An increase in fixed assets (the long-term productive assets

of the company) is a use of cash, which reduces the firm’s

free cash flow.

FCF = sum of the above

Figure 19.2. Defining the free cash flow. We have previously discussed FCFs and their use in

valuation in Chapters 5 - 7.

PFE Chapter 19, Stock valuation page 9

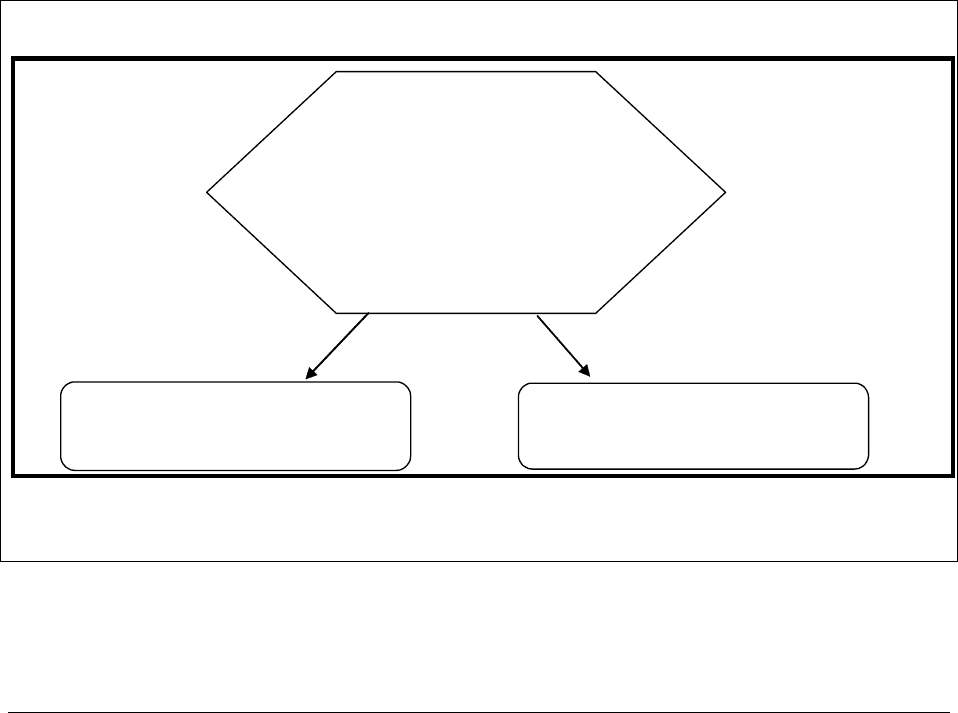

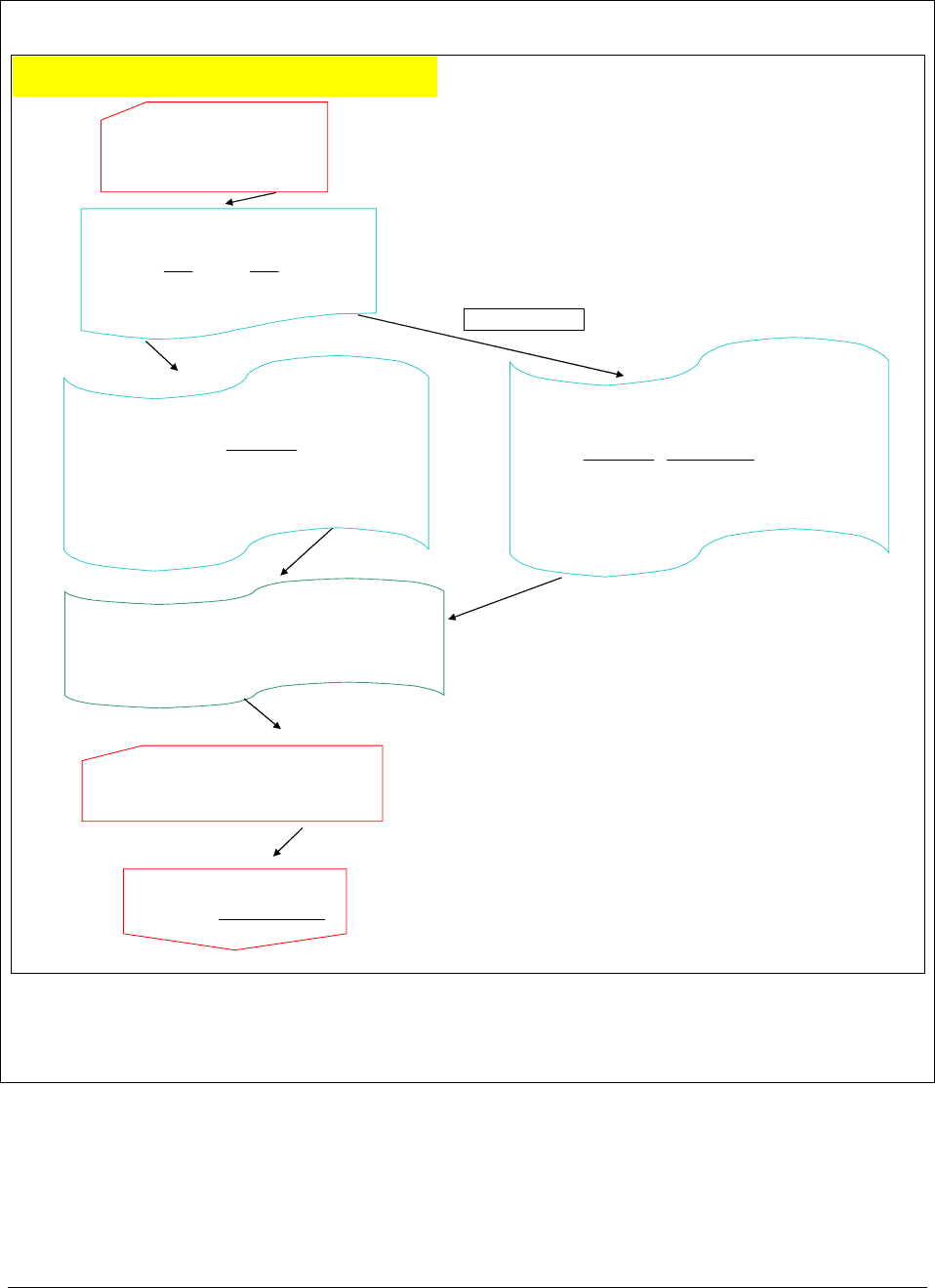

CALCULATING THE FIRM'S SHARE VALUE

FROM THE FREE CASH FLOWS AND WACC

Predict firm's future free cash flows (FCF).

In Chapters 8 & 9 we did this using a pro

forma model.

Compute the firm's weighted average cost of capital

(WACC):

Discount some of the free cash flows and the terminal value to get the

enterprise value of the firm:

The terminal value is what the firm will be worth on date N. We've

multiplied by (1+WACC)

0.5

because cash flows are assumed to occur in

mid

y

ea

r

.

Subtract debt value from firm value to get total equity

value:

Divide equity value by the number of

shares to derive the share value:

Total equity value

Share value

Number of shares

=

()()

()

0.5

1

*1

11

N

t

tN

t

Enterprise value

FCF

Terminal Value

WACC

WACC WACC

=

⎡⎤

=+ +

⎢⎥

++

⎢⎥

⎣⎦

∑

A

dd initial cash balances to enterprise value to get total value of the firm's

assets:

Equity value Total asset value Debt value=−

()

1

EDC

ED

WACC r r T

ED ED

=+−

++

ED

C

Where r is the cost of equity, r is the

cost of debt, and T is the firm's tax rate

Total asset value Enterprise value Initial cash=+

Discount the all future free cash flows to get the enterprise value of the

firm:

We've multiplied by (1+WACC)

0.5

because cash flows are assumed to

occur in mid

y

ea

r

.

()

()

0.5

1

*1

1

t

t

t

FCF

Enterprise value WACC

WACC

∞

=

⎡⎤

=+

⎢⎥

+

⎢⎥

⎣⎦

∑

Alternatively

Figure 19.3: Flow diagram for a FCF valuation

PFE Chapter 19, Stock valuation page 10

Valuation 2: Example 1—a basic example

It is 31 December 2003 and you are trying to value Arnold Corp, which finished 2003

with a free cash flow of $2 million. The company has debt of $10 million and cash balances of

$1 million You estimate the following financial parameters for the company:

•

The future anticipated growth rate of the FCF is 8%

•

The WACC of Arnold is 15%

You can now estimate the value of Arnold:

•

The enterprise value of Arnold is the present value of future anticipated FCFs discounted

at the WACC:

()

()

0.5

1

This factor "corrects"

for the fact that FCFs occur

This is the PV

throughout the year.

formula, assuming that

FCFs occur at year-end

*1

1

t

t

t

FCF

Enterprise value WACC

WACC

FCF

∞

=

↑

↑

⎡⎤

=+

⎢⎥

+

⎢⎥

⎣⎦

=

∑

()

()

()

()

()

0.5

2003

1

Future FCFs are expected

to grow at rate .

0.5

2003

This formula was

given in Chapter ???

1

*1

1

1

*1

t

t

t

g

g

WACC

WACC

FCF g

WACC

WACC g

∞

=

↑

↑

⎡⎤

+

+

⎢⎥

+

⎢⎥

⎣⎦

⎡⎤

+

=+

⎢⎥

−

⎣⎦

∑

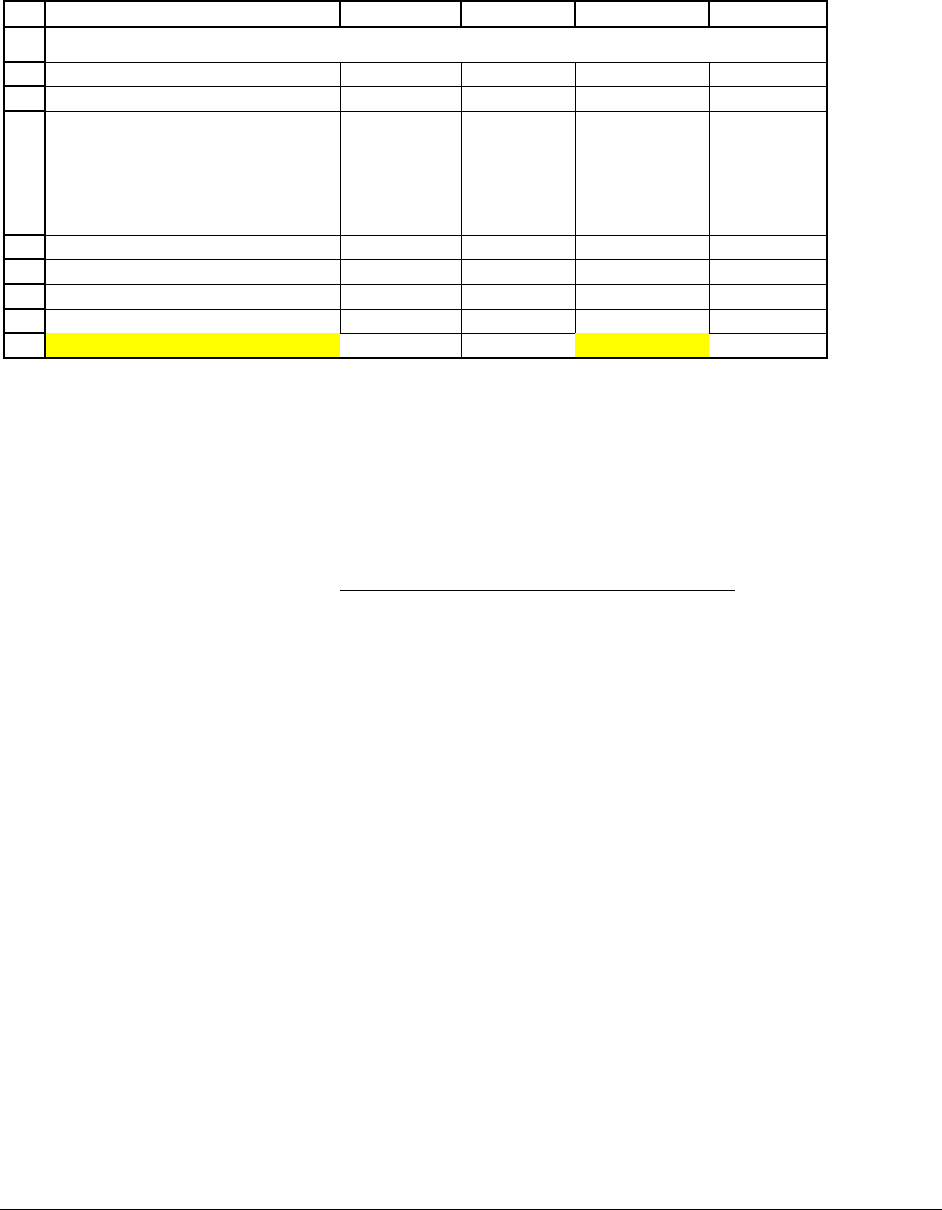

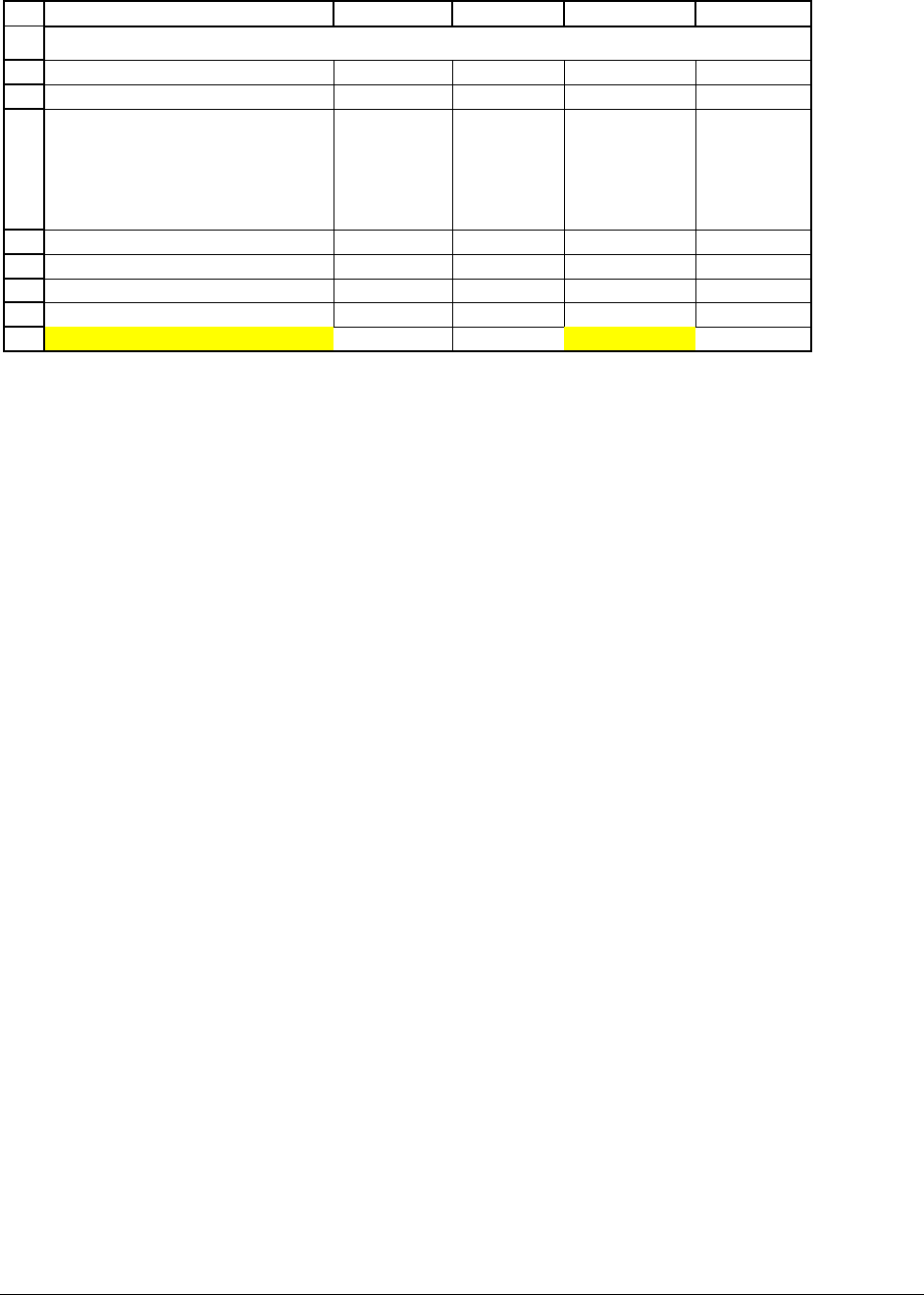

Doing the computations in an Excel spreadsheet shows that the enterprise value of Arnold

Corp. is $33,090,599 and that the estimated per-share value is $24.09:

PFE Chapter 19, Stock valuation page 11

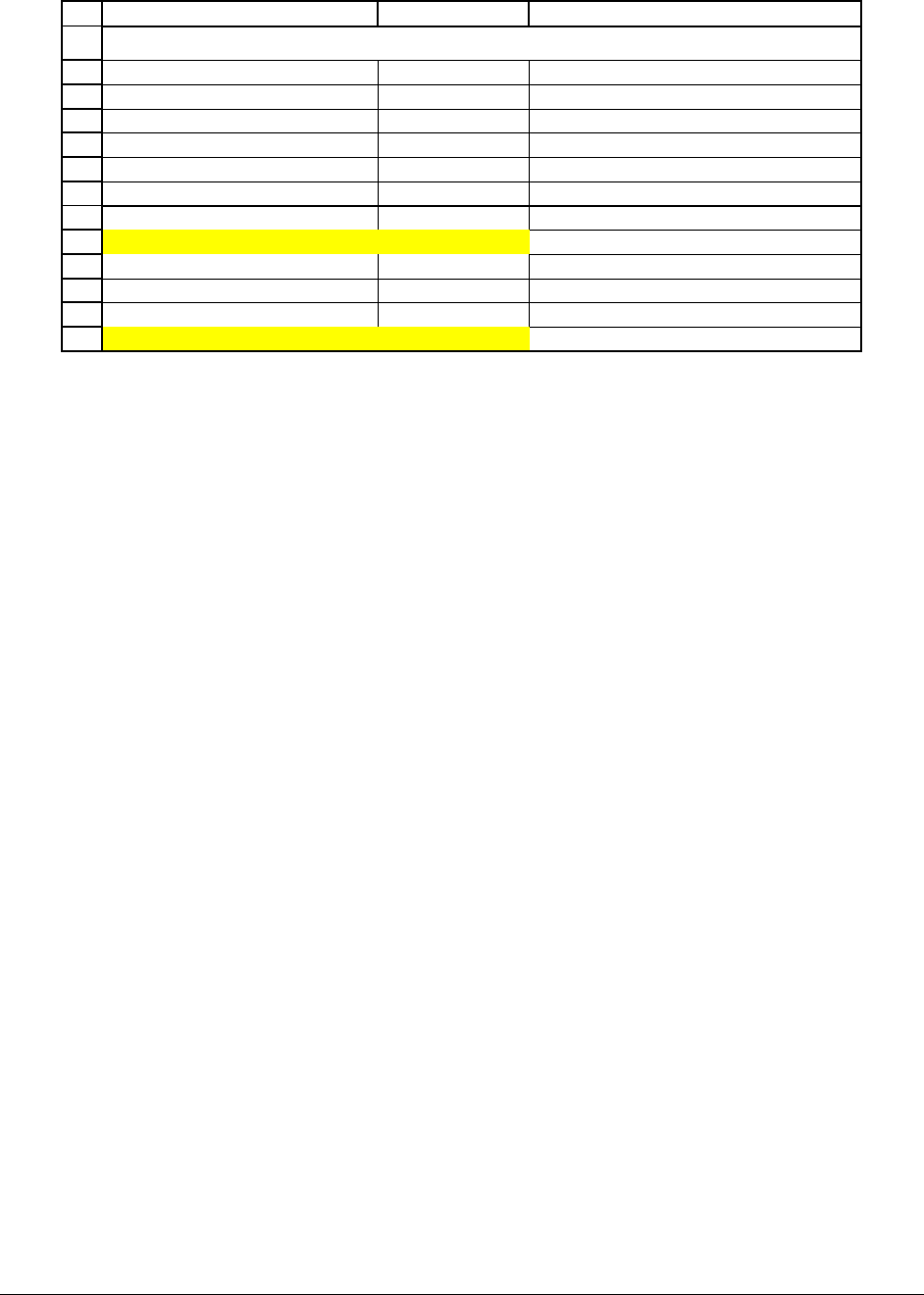

1

2

3

4

5

6

7

8

9

10

11

12

13

AB C

2003 FCF (base year) 2,000,000

Future FCF growth rate 8%

WACC 15%

End-2003 debt 10,000,000

End-2003 cash 1,000,000

Number of shares outstanding 1,000,000

Enterprise value 33,090,599 <-- =B2*(1+B3)/(B4-B3)*(1+B4)^0.5

Add cash 1,000,000 <-- =B6

Subtract debt -10,000,000 <-- =-B5

Value of equity 24,090,599 <-- =SUM(B9:B11)

Share value 24.09 <-- =B12/B7

VALUING ARNOLD CORP

Valuation method 2: Example 2—two FCF growth rates

In the valuation of Arnold Corp. in the previous subsection we assumed a FCF growth

rate which is unchanging over the future. This assumption is often suitable for a mature, stable

company, but it may not be appropriate for a company that is currently experiencing very high

growth rates. In this subsection we show how to perform a FCF valuation of a company for

which we assume two FCF growth rates—a high FCF growth rate for a number of years followed

by a subsequent lower FCF growth rate.

Xanthum Corp. has just finished its 2003 financial year. The company’s 2003 FCF was

$1,000,000. Xanthum has been growing very fast; you anticipate that for the coming 5 years the

FCF growth rate will be 35%. After this time, you anticipate that the FCF growth will slow to

10% per year, because the market for Xanthum’s products will become mature.

Xanthum has 3,000,000 shares outstanding and a WACC of 20%. It currently has

$500,000 of cash on hand which is not needed for operations; Xanthum also has $3,000,000 of

debt. To value the company, we apply the same valuation scheme as before, but this time we use

the two FCF growth rates: