Principles of Finance with Excel (Основы финансов c Excel)

Подождите немного. Документ загружается.

PFE Chapter 18, Stock valuation page 11

1

2

3

4

5

6

7

8

9

10

11

12

13

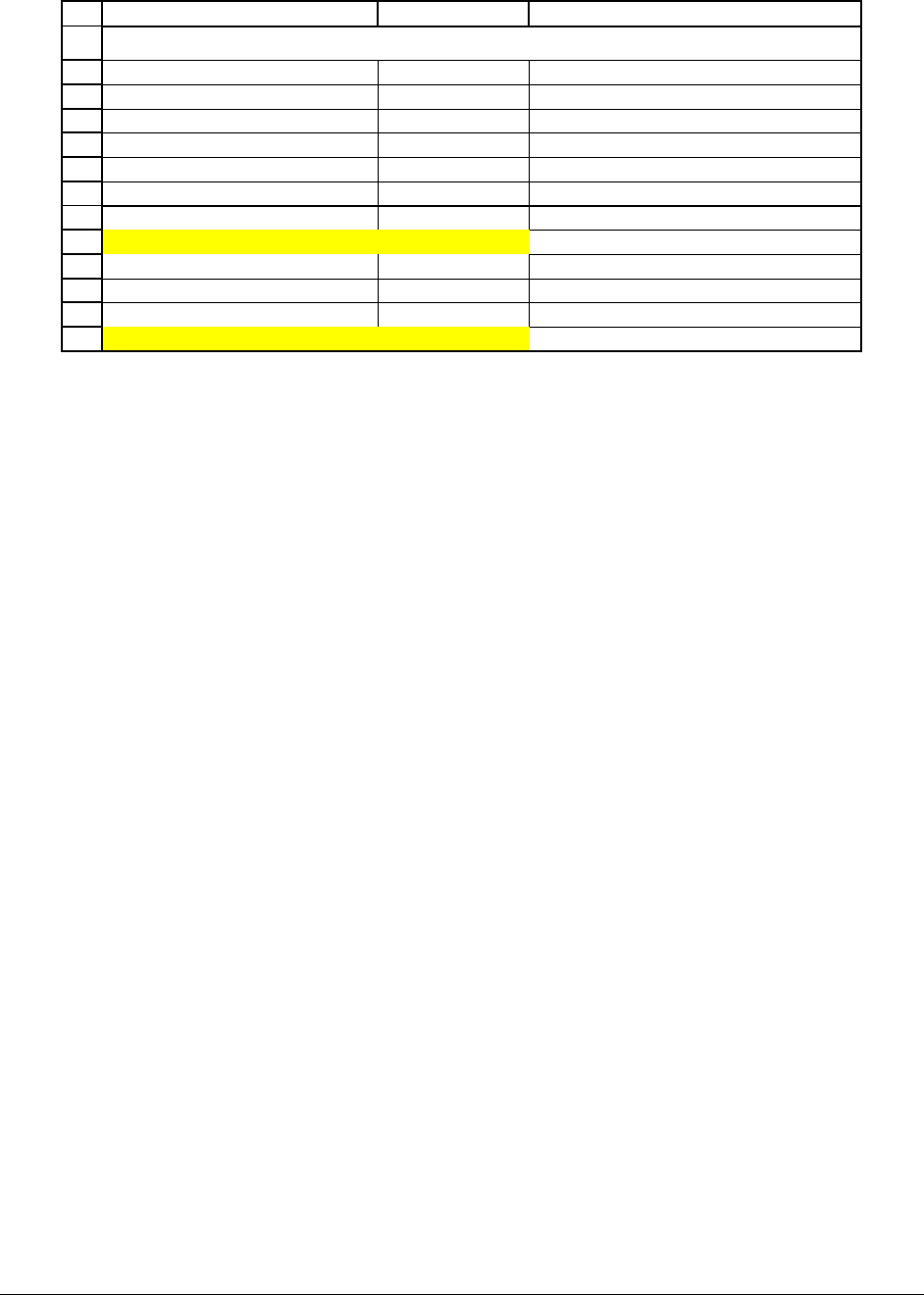

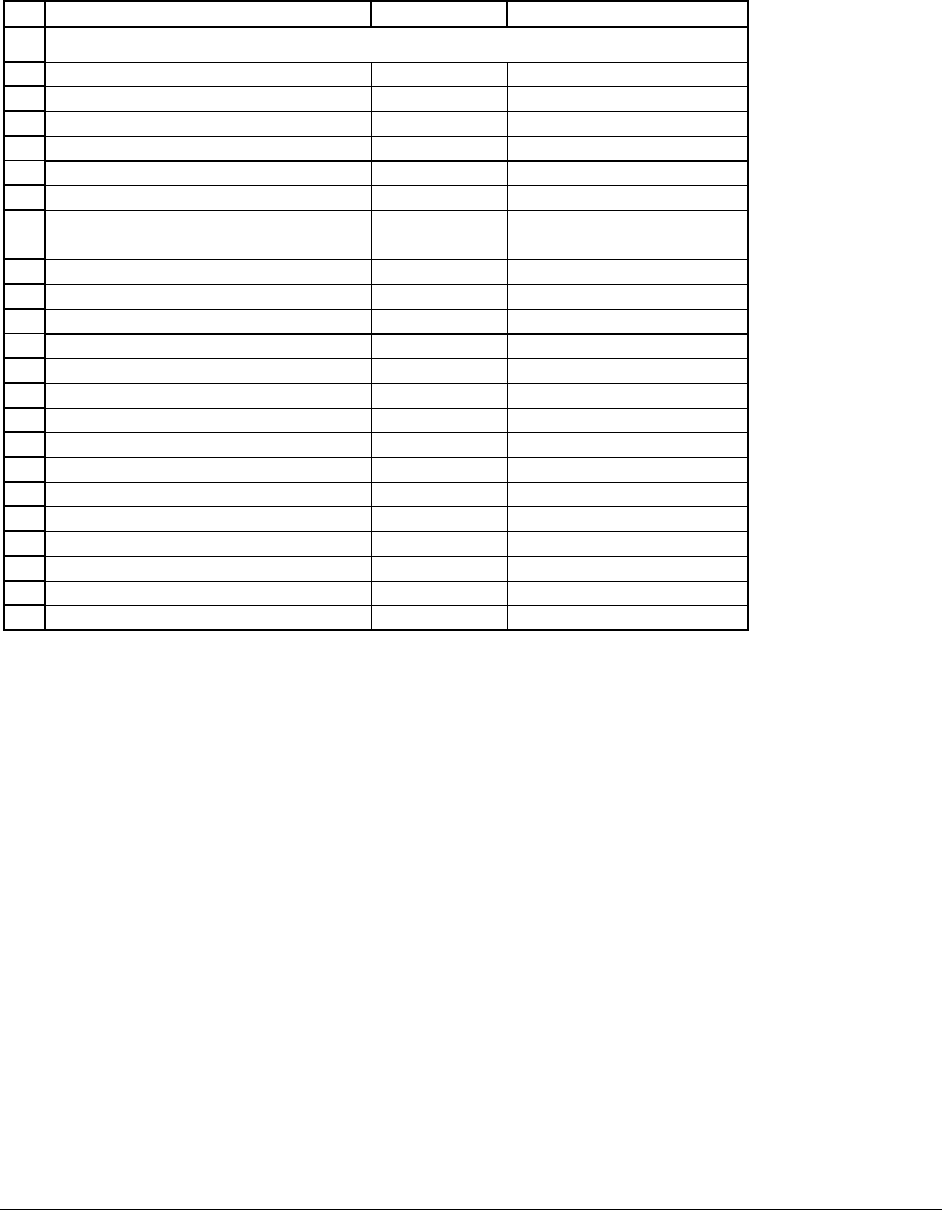

AB C

2003 FCF (base year) 2,000,000

Future FCF growth rate 8%

WACC 15%

End-2003 debt 10,000,000

End-2003 cash 1,000,000

Number of shares outstanding 1,000,000

Enterprise value 33,090,599 <-- =B2*(1+B3)/(B4-B3)*(1+B4)^0.5

Add cash 1,000,000 <-- =B6

Subtract debt -10,000,000 <-- =-B5

Value of equity 24,090,599 <-- =SUM(B9:B11)

Share value 24.09 <-- =B12/B7

VALUING ARNOLD CORP

Valuation method 2: Example 2—two FCF growth rates

In the valuation of Arnold Corp. in the previous subsection we assumed a FCF growth

rate which is unchanging over the future. This assumption is often suitable for a mature, stable

company, but it may not be appropriate for a company that is currently experiencing very high

growth rates. In this subsection we show how to perform a FCF valuation of a company for

which we assume two FCF growth rates—a high FCF growth rate for a number of years followed

by a subsequent lower FCF growth rate.

Xanthum Corp. has just finished its 2003 financial year. The company’s 2003 FCF was

$1,000,000. Xanthum has been growing very fast; you anticipate that for the coming 5 years the

FCF growth rate will be 35%. After this time, you anticipate that the FCF growth will slow to

10% per year, because the market for Xanthum’s products will become mature.

Xanthum has 3,000,000 shares outstanding and a WACC of 20%. It currently has

$500,000 of cash on hand which is not needed for operations; Xanthum also has $3,000,000 of

debt. To value the company, we apply the same valuation scheme as before, but this time we use

the two FCF growth rates:

PFE Chapter 18, Stock valuation page 12

()()

()

5

0.5

16

This factor "corrects"

for the fact that FC

The PV of the "high The PV of the "normal

growth" FCFs growth" FCFS

*1

11

tt

tt

tt

FCF FCF

Enterprise value WACC

WACC WACC

∞

==

↑

↑↑

⎡⎤

⎢⎥

⎢⎥

⎢⎥

=+ +

⎢⎥

++

⎢⎥

⎢⎥

⎢⎥

⎣⎦

∑∑

Fs occur

throughout the year.

There’s a valuation formula which can be derived using techniques described in the

appendix to Chapter 1:

()

5

2003 2003

In the spreadsheet this is called

1

"term 1" and is called "term1 factor"

1

1

1

11

1

1

1

1

1

high

high

high h

high

g

WACC

Enterprise value

g

FCFg FCFg

WACC

g

WACC

WACC

↑

+

+

=

⎛⎞

+

⎛⎞

⎜⎟

−

⎜⎟

++

+

⎜⎟

⎝⎠

+

⎜⎟

+

+

⎜⎟

−

⎜+ ⎟

⎝⎠

()

()

()

5

0.5

5

In the spreadsheet this is called

"term 2"

1

*1

1

igh

normal

normal

g

WACC

WACC g

WACC

↑

⎡⎤

⎢⎥

⎢⎥

⎢⎥

⎢⎥

⎢⎥

⎛⎞

+

⎢⎥

+

⎜⎟

⎢⎥

−

+

⎝⎠

⎢⎥

⎢⎥

⎢⎥

⎢⎥

⎢⎥

⎢⎥

⎣⎦

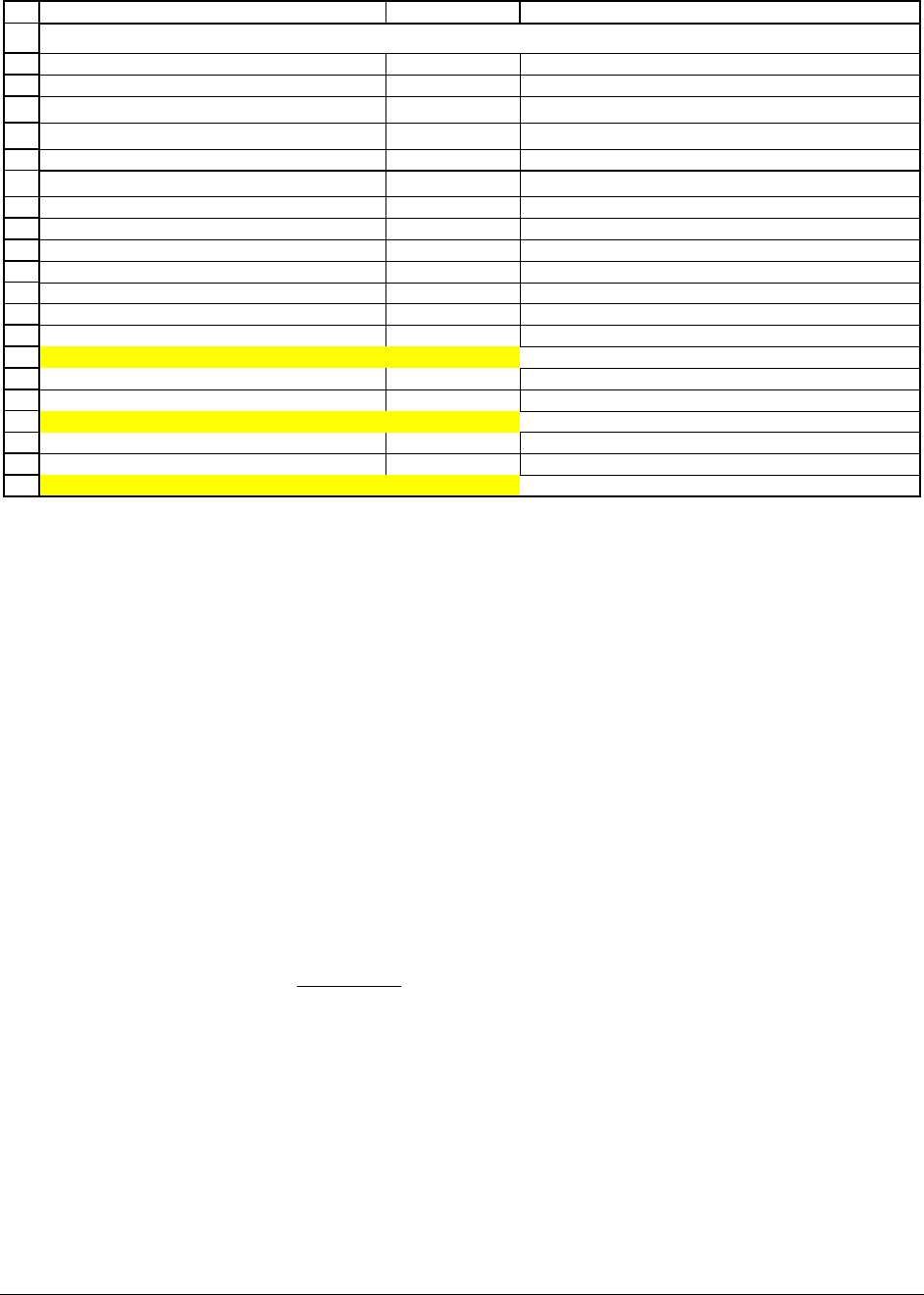

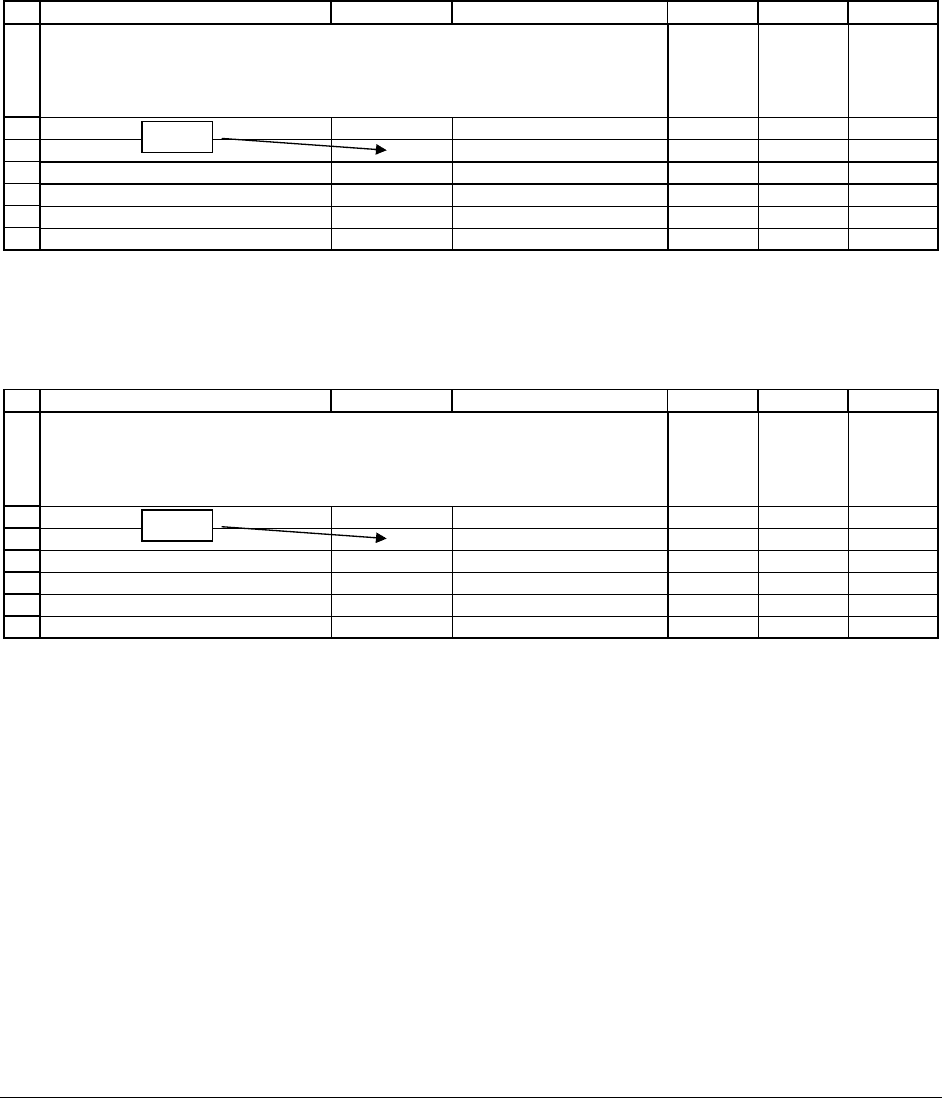

The spreadsheet below shows that Xanthum’s enterprise value is $27,040,649 (cell B15)

and that its per-share value is $8.18 (cell B21):

PFE Chapter 18, Stock valuation page 13

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

AB C

2003 FCF (base year) 1,000,000

High growth rate, g

high

35%

Normal growth rate, g

normal

10%

Number of high growth years 5

Term 1 factor: (1+g

high

)/(1+WACC)

113% <-- =(1+B4)/(1+B9)

WACC 20%

End-2003 debt 3,000,000

End-2003 cash 500,000

Term 1: PV of high-growth cash flows 7,218,292 <-- =B2*B7*(1-B7^B6)/(1-B7)

Term 2: PV of normal-growth cash flows 19,822,357 <-- =B2*(1+B4)^B6*(1+B5)/(B9-B5)/(1+B9)^B6

Enterprise value 27,040,649 <-- =SUM(B13:B14)

Add cash 27,540,649 <-- =B15+B11

Subtract debt -3,000,000 <-- =-B10

Value of equity 24,540,649 <-- =SUM(B16:B17)

Number of shares, end 2003 3,000,000

Share value 8.18 <-- =B18/B20

VALUING XANTHUM CORP

Valuation method 2: Example 3—using the terminal value in a real-estate project

In the previous two examples we discounted an infinitely-lived stream of cash flows.

Sometimes it makes more sense to discount a finite number of cash flows and then attribute a

terminal value to the project.

Here’s an example: Your Aunt Sarah has quite a bit of money. She’s been offered a

share in a partnership which is being set up by a local real estate agent. The partnership will buy

an existing building, called the Station Building, for $20 million. The agent is selling 25 shares,

for $800,000 each (

$20,000,000

$800,000

25

=

). Aunt Sarah has asked you to do some financial

analysis to determine whether this is a fair price for a partnership share in the Station Building.

Here’s what you discover:

PFE Chapter 18, Stock valuation page 14

• All income from the Station Building partnership will flow through to the shareholders,

who will pay taxes on the income at their personal tax rates. Aunt Sarah’s tax rate is

40%.

•

Station Building will be depreciated over 40 years, giving an annual depreciation of

$500,000 per year.

•

The building is fully rented out and brings up annual rents of $7 million. You do not

anticipate that these rents will increase over the next 10 years.

•

Maintenance, property taxes, and other miscellaneous expenses for Station Building cost

about $1 million per year.

•

The agent who is putting together the partnership has proposed selling Station Building

after 10 years. He estimates that the market price of the building will not change much

over this period—meaning that the market price of Station Building in year 10 is

anticipated to be $20 million, like its price today.

In your valuation of the Station Building shares, you see that the annual free cash flow

(FCF) to Aunt Sarah is $152,000 (cell B16 in the spreadsheet below). This FCF will be available

to her in years 1-10, and is based on the building’s profit before taxes of $5,500,000, which will

be spread equally among the partners.

The terminal value of the building is $20,000,000, which on a per-share basis is $800,000

(cell B19). At the time the building is sold in year 10, its accumulated depreciation is

$5,000,000, so that its book value is $15,000,000. To compute Aunt Sarah’s cash flow from this

terminal value, we deduct the per-share book value of the building ($600,000, cell B20) from the

sale price to arrive at taxes of $80,000 on the profit from the sale of the building (cell B22). The

PFE Chapter 18, Stock valuation page 15

cash flow from the sale is the $800,000 sale price minus the taxes--$720,000 as shown in cell

B23.

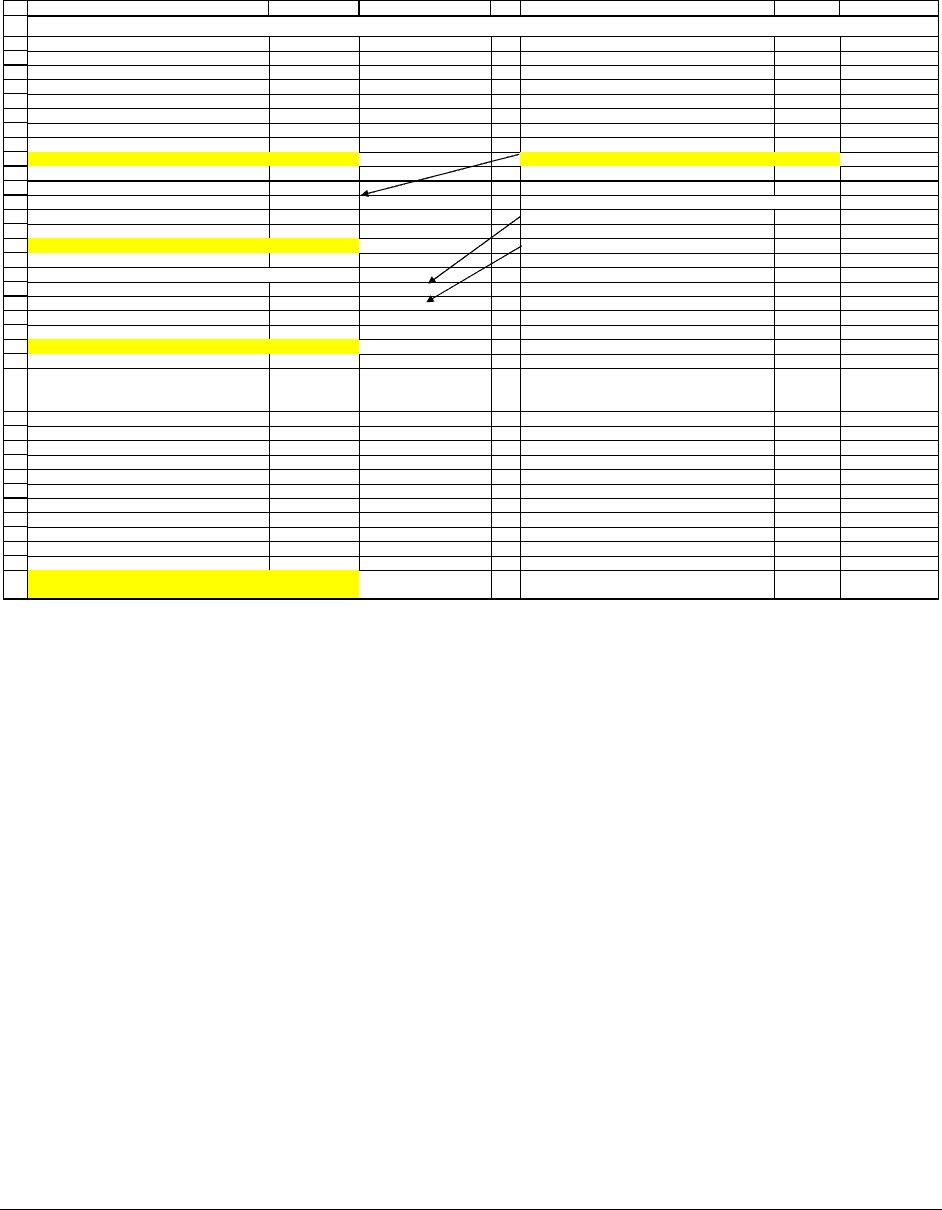

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

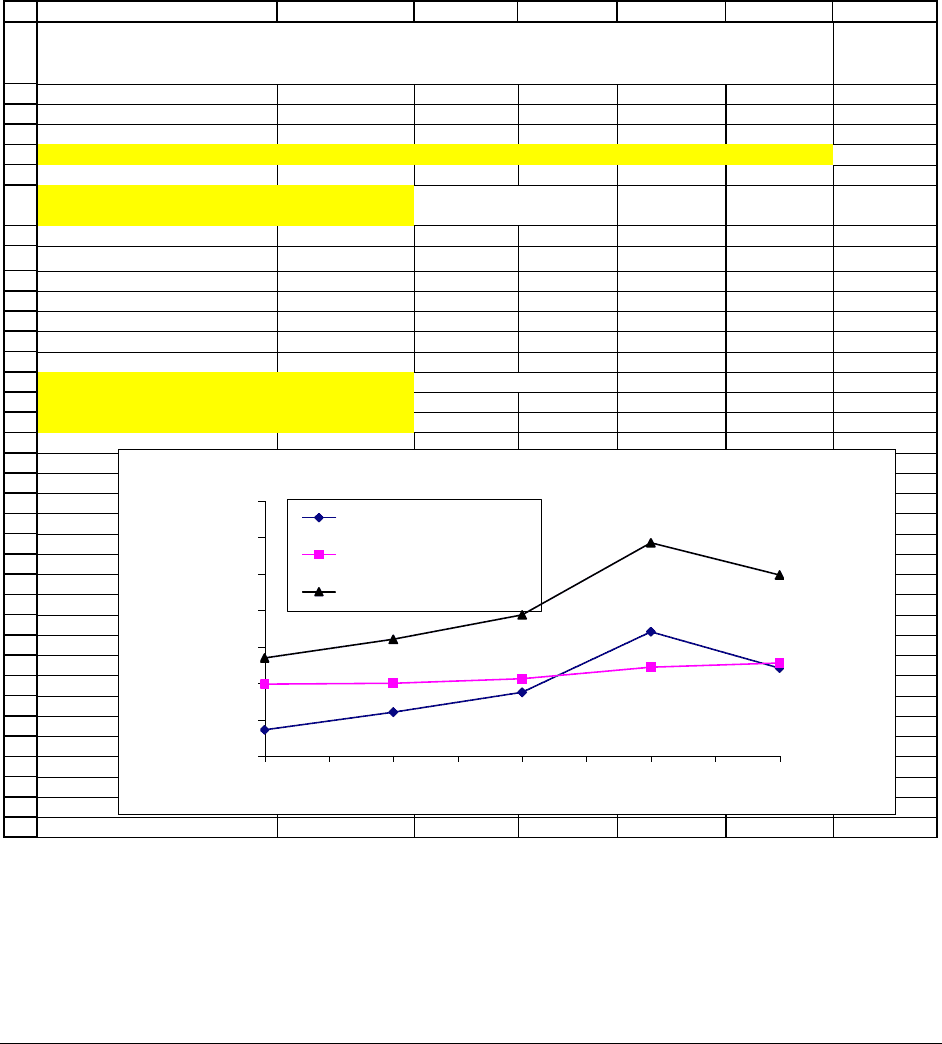

ABCDEFG

Building cost 20,000,000

Depreciable life (years) 40

Annual rents 7,000,000

Annual expenses 1,000,000

Annual depreciation 500,000 <-- =B2/B3

Profit and loss, Station Building as a whole

Aunt Sarah's tax rate 40% Annual rent 7,000,000

WACC 18% Minus annual expenses -1,000,000

Shares issued 25 Minus annual depreciation -500,000

Share price 800,000 Anticipated annual building profit before taxes 5,500,000 <-- =SUM(F7:F9)

Profit and loss, Aunt Sarah's share

Anticipated annual building profit before taxes 220,000 <-- =F10/B9

Terminal value, year 10, Station Building as a whole

Profit after taxes 132,000 <-- =(1-B7)*B13 Anticipated building market price 20,000,000 <-- =B2

Building depreciation, per share 20,000 <-- =B6/B9 Accumulated depreciation, year 10 5,000,000 <-- =B6*10

Free cash flow 152,000 <-- =B14+B15 Book value of building, year 10 15,000,000 <-- =B2-F15

Terminal value, year 10, Aunt Sarah's share

Anticipated building market price 800,000 <-- =F14/B9

Book value in year 10, per share 600,000 <-- =F16/B9

Profit from sale of building 200,000 <-- =B19-B20

Tax on profit 80,000 <-- =B7*B21

Terminal value: cash flow from sale 720,000 <-- =B19-B22

Year

Aunt Sarah's

anticipated

FCF

1 152,000 <-- =$B$16

2 152,000

3 152,000

4 152,000

5 152,000

6 152,000

7 152,000

8 152,000

9 152,000

10 872,000 <-- =$B$16+B23

Share value: Present value of Aunt Sarah's

free cash flows

$820,667.53 <-- =NPV(B8,B26:B35)

STATION BUILDING PARTNERSHIP--SHARE VALUATION

Cells B26:B35 show Aunt Sarah’s anticipated free cash flows from the building

partnership, including the terminal value. Discounting these cash flows at the WACC of 20%

values a partnership share at $820,667.53. Conclusion: Aunt Sarah should invest in the

building!

Valuation method 2: Example 4—using the terminal value to get around large FCF

growth rates

Our second example of using the terminal value involves the Formanis Corporation.

Formanis is in a growth industry and has had formidable FCF growth rates for the past several

PFE Chapter 18, Stock valuation page 16

years, and you anticipate that these rates will continue for years 1-5. However, after year 5 you

anticipate a big slowdown in Formanis’s FCF growth, as its industry matures.

Here are the relevant facts about Formanis:

•

The company’s FCF for the current year is $1,000,000.

•

You anticipate that the FCF for years 1-5 will grow at a rate of 25% per year.

•

You anticipate a growth rate of FCFs of 6% per year for years 6, 7, … (termed the “long-

term growth rate” in the spreadsheet below).

•

The company has 5 million shares outstanding.

The valuation formula is:

()

()()()()

()

()

()

35

12 4

2345

5

5

This is the terminal value:

an explanation is given in Chapter ??

1

1111

*1 -

1

*

-

1

FCF FCF

FCF FCF FCF

Formanis value

WACC

WACC WACC WACC WACC

FCF long term growth rate

WACC long term growth rate

WACC

↑

=+ + + +

+

++++

+

+

−

+

To value Formanis, we first predict the FCFs for years 1-5 (cells B9:B13 of the

spreadsheet). The present value of these FCFs is $6,465,787 (cell B20). The terminal value

represents the year-5 present value of the Formanis cash flows for years 6, 7, … . To compute

the terminal value, we assume that Formanis’s cash flows for these years grow at the long-term

growth rate:

()

()()

()

()

()

()

()

()

67 7

22

2

55

2

3

5

2

-5 , 6,7,...

...

1

11

*1 - . *1 - .

1

1

*1 - .

...

1

Terminal value year PV of Formanis FCFs years

FCF FCF FCF

WACC

WACC WACC

FCF long term growth rate FCF long term growth rate

WACC

WACC

FCF long term growth rate

WACC

F

=

=+ + +

+

++

++

=+

+

+

+

++

+

=

()

()

5

*1 -

-

CF long term growth rate

WACC long term growth rate

+

−

PFE Chapter 18, Stock valuation page 17

In cell B17 below the terminal value—assuming a long-term FCF growth rate of 6%—is

$17,025,596.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

ABC

Current FCF 1,000,000

Anticipated growth rate, years 1-5 25%

WACC 15%

Long-term growth rate, after year 5 6%

Number of shares outstanding 5,000,000

Year

A

nticipated

FCF

1 1,250,000 <-- =$B$2*(1+$B$3)

2 1,562,500 <-- =B9*(1+$B$3)

3 1,953,125 <-- =B10*(1+$B$3)

4 2,441,406

5 3,051,758

Terminal value calculation

FCF in year 5 3,051,758 <-- =B13

Terminal value 17,025,596 <-- =B16*(1+B5)/(B3-B5)

V

aluing Formanis Corporation

Present value of FCFs, years 1-5 6,465,787 <-- =NPV(B4,B9:B13)

Present value of terminal value 8,464,730 <-- =B17/(1+B4)^5

Value of Formanis 14,930,518 <-- =B21+B20

Per share value $2.99 <-- =B22/B6

FORMANIS CORPORATION

The value of Formanis (cell B22) is $14,930,518. The per-share value of Formanis is

$2.99 (cell B23).

The terminal value method illustrated for Formanis is often used:

•

It allows the stock analyst to distinguish between short-term growth and long-term

growth. Often short-term growth is a function of market performance, whereas long-term

growth is determined by macro-economic factors. For example in a new and rapidly

developing market, we might anticipate high short-term growth rates. But we would also

anticipate that as the market matures and becomes more saturated, the long-term growth

rates would approximate the growth of the economy as a whole.

PFE Chapter 18, Stock valuation page 18

• From an Excel point of view, the terminal value method allows us to do interesting

sensitivity analyses. For example, here is the per-share value of Formanis for a variety of

long-term growth rates and WACCs; we use the

Data Table technique described in

Chapter ???:

26

27

28

29

30

31

32

ABCDEF

Long-term growth rate ↓

$2.99

0% 2% 4% 6%

WACC →

15%

2.51 2.64 2.80 2.99

20% 2.11 2.22 2.35 2.50

25%

1.80 1.89 1.99 2.12

30%

1.55 1.62 1.70 1.81

Sensitivity analysis: Per share value of Formanis

with different WACC and long-term growth. Year 1-5 growth

rate = 25%

=B23

Varying the year 1-5 growth rate gives different values. In the table below, for example,

we’ve assumed that year 1-5 growth is 20%:

26

27

28

29

30

31

32

ABCDEF

Long-term growth rate ↓

$3.01

0% 2% 4% 6%

WACC →

15%

2.38 2.54 2.75 3.01

20% 2.00 2.13 2.30 2.51

25%

1.70 1.81 1.95 2.12

30%

1.46 1.55 1.66 1.81

Sensitivity analysis: Per share value of Formanis

with different WACC and long-term growth. Year 1-5 growth

rate = 20%

=B23

18.3. Valuation method 3: The price of a share is the present value of its

future anticipated equity cash flows discounted at the cost of equity

In the previous section we “backed into” the equity valuation of the firm, by first

calculating the value of the firm’s assets (the enterprise value plus initial cash balances), and then

subtracting from this number the value of the firm’s debts. In this section we present another

PFE Chapter 18, Stock valuation page 19

method for calculating the value of the firm’s equity—we directly discount the value of the

firm’s anticipated payouts to its shareholders.

As an example consider Haul-It Corp., which has a steady record of paying dividends and

repurchasing shares. The company has 10 million shares outstanding. Here’s a spreadsheet with

the valuation model:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

ABCDEFG

1998 1999 2000 2001 2002

Repurchases $1,440,000 $2,410,000 $3,500,000 $6,820,000 $4,830,000

Dividends $3,950,000 $3,997,000 $4,238,000 $4,875,000 $5,100,000

Total cash paid to equity holders $5,390,000 $6,407,000 $7,738,000 $11,695,000 $9,930,000

Compound annual

growth, 1998-2002

16.50% <-- =(F5/B5)^(1/4)-1

Haul-It's cost of equity, r

E

25.00%

V

aluation

Current equity payout $9,930,000 <-- =F5

Anticipated future growth 16.50%

Value of total equity 136,164,862 <-- =B12*(1+B13)/(B9-B13)

Number of shares outstanding 10,000,000

Value per share 13.62 <-- =B15/B16

HAUL-IT CORPORATION--EQUITY PAYOUT

HISTORY AND SHARE VALUATION

Haul-It Corporation--Payouts to Equity Holders

$0

$2,000,000

$4,000,000

$6,000,000

$8,000,000

$10,000,000

$12,000,000

$14,000,000

1998 1999 1999 2000 2000 2001 2001 2002 2002

Repurchases

Dividends

Total cash paid to equity holders

PFE Chapter 18, Stock valuation page 20

Between 1998 and 2002, Haul-It’s payouts to its equity holders have increased at an

impressive rate of 16.50% per year (cell B7). The company’s cost of equity r

E

is 25% (cell B9).

1

Assuming that future equity payout growth equals historical growth, Haul-It is valued at $136

million (cell B15), which gives a per-share value of $13.62.

The equity value of the company is the discounted value of the future anticipated equity

payouts:

() ()

() ()

()

()

()

()

2003 2004 2004

23

23

2002 2002 2002

23

2002

....

1

11

11 1

....

1

11

1 9,930,000 1.16

E

EE

E

EE

E

Equity payout Equity payout Equity payout

Equity value

r

rr

Equity payout g Equity payout g Equity payout g

r

rr

Equity payout g

rg

=+++

+

++

++ +

=+ + +

+

++

+

==

−

()

5

136,164,862

25.00% 16.50%

=

−

Dividing the equity value by the number of shares outstanding gives the estimated value

per share:

136,164,862

13.62

10,000,000

Equity value

Value per share

Shares outstanding

===

Why do finance professionals shun direct equity valuation?

Valuation method 3, the direct valuation of equity is so simple that it may surprise you

that it is rarely used. There are several reasons for this, none of which we can fully explain at

this point in the book:

•

The direct equity valuation method depends on projected equity payouts (that is,

dividends plus share repurchases), whereas Method 3 depends on projected free cash

1

At this point we do not discuss how we arrived at this cost of equity. For a recapitulation of cost of capital

techniques, see sections 18.??? – 18.???.