Principles of Finance with Excel (Основы финансов c Excel)

Подождите немного. Документ загружается.

PFE, Chapter 17, Efficiency page 30

In trying to implement this profitable information, you and other investors would drive its

profitability out of existence. This sounds obvious (and it is), but it’s a principle often

overlooked by investors.

Technical analysis—do previous prices predict future prices?

Its proponents claim that technical analysis is the art or science of using historical stock

price patterns to predict the future stock price. Finance professors think that technical analysis is

neither an art nor a science, but simply voodoo. They base this belief on the weak-form efficient

markets hypothesis and on tons of academic research.

Here’s a simple example of technical analysis: Based on an analysis of ABC’s historical

stock price, you’ve concluded that it fluctuates in a band between $25 and $35. When the price

gets close to $25, it inevitably goes up, and when the price gets close to $35, the stock price goes

down. This leads you to develop the following money-making strategy:

• Buy ABC when the price gets to $25.50; since this is very close to $25, the price will

have a very high probability of moving up. In any case you’ll have little to lose, since the

price can’t go below $25.

• Sell ABC when the price gets to $34.50; since this is very close to $35, the price has a

very high probability of moving down. In any case at $34.50 you have very little to gain.

This sounds like a money-making strategy, but on the other hand it’s self-defeating: If all

investors try to implement this strategy (and why shouldn’t they, since your analysis is based on

publicly-available information?), then the “price band” will narrow—no one will want to buy

ABC stock when it gets close to $34.50 or $25.50.

PFE, Chapter 17, Efficiency page 31

But now everyone will try to implement a profit strategy based on the new price band.

And so on and so on ...

The conclusion: There is no price band! It may be that ABC’s share price has been

between $25 and $35 in the past, but this says nothing about its share price in the future.

In fact you could make a broader conclusion: As long as there are many people trading

in a market, a strategy based only on past and current prices cannot be profitable.

Technical trading rules—another violation of weak-form efficiency

A technical trading strategy is a rule for buying and selling a stock based on the stock’s

previous price movements.

9

The weak-form efficiency hypothesis says that technical trading

rules won’t work.

The ABC example above (where ABC’s stock was assumed to trade in a band between

$25 and $35) is a simple example of a technical trading rule. Figure 17.4 gives a more

sophisticated example.

9

There are lots of good websites on technical trading. Here are a few: http://technicaltrading.com/,

http://www.stockcharts.com/education/What/TradingStrategies/MurphysLaws.html

.

PFE, Chapter 17, Efficiency page 32

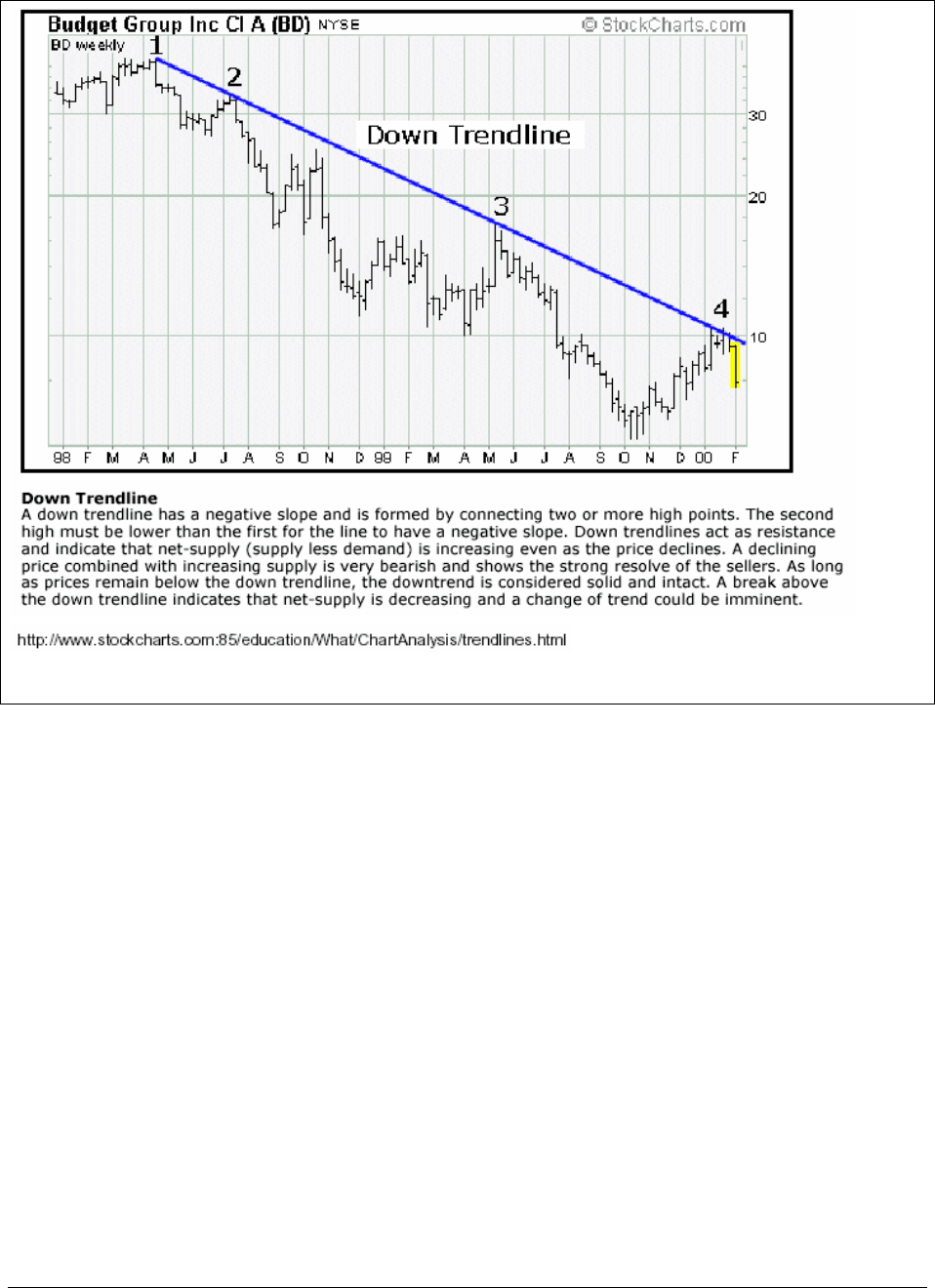

Figure 17.4: Technical analysis of Budget stock.

The down trendline explains the downturn in Budget Group’s stock price by connecting four

“price peaks.” The prediction and the associated trading rule is:

• When the stock price of Budget Group gets close to the down trendline, it will move

down. To exploit this information, you should buy when the price is farther away from

the trendline and sell when it is close to the line.

• If the stock price of Budget Group breaks through the down trendline “a change of trend

could be imminent.” This is the technical analyst’s escape hatch—the information

contained in the prices is true except when it’s not true.

PFE, Chapter 17, Efficiency page 33

Semi-strong form efficiency: sometimes true

Semi-strong form efficiency predicts that not just past prices, but all publicly-available

information, is incorporated in current security prices. This suggests, for example, that the

analysis of a firm’s financial statements is not going to help you make better investment

decisions.

Semi-strong market efficiency seems to be true ... occasionally. It’s a lot of work to

understand all the publicly-available information about a stock, and it’s quite common to see

cases where information existed, but it wasn’t incorporated into the stock price. The 3Com-Palm

story discussed in Section 17.3 above is a case in point. Only after some rigorous analysis of the

relation between 3Com and Palm and analysis of the cash reserves of 3Com could we conclude

that Palm’s price was overpriced relative to 3Com’s price. There has to be a lot at stake to

motivate investors to engage in this kind of research. If it’s worthwhile, then we would expect

semi-strong efficiency to prevail.

Strong-form efficiency: usually not true

The strong-form efficient markets hypothesis says that all information is incorporated

into securities prices. Hardly anyone believes that this is true. In fact it’s often illegal, since all

information includes proprietary information and inside knowledge—by law, insiders are

forbidden to trade on their information if it hasn’t been revealed to the public.

PFE, Chapter 17, Efficiency page 34

17.5. Efficient Markets Principle 4: Transactions costs are important

Transactions costs are all the various costs of buying and selling a security and also the

costs (monetary or otherwise) of understanding a security. When you buy a stock for $50, you

pay a brokerage commission. In the United States this commission is typically ½ percent. So

the purchase of a share of stock costs you $50.25 and its sale delivers you $49.75:

3

4

5

6

7

8

9

ABC

Buy commission 0.50%

Sell commission 0.50%

Stock price $50.00

Purchase price 50.25 <-- =B6*(1+B3)

Selling price 49.75 <-- =B6*(1-B4)

The result: If you think that the stock is worth $50.15, it won’t be worth your while to buy it:

Even though the stock’s price today is $50, less than what you think it’s worth, transactions costs

make it more expensive to buy the stock ($50.25) than you think it’s worth.

Similarly, suppose you own a share of the stock and suppose you think it’s worth only

$49.80. In the absence of transactions costs, it would be logical to sell the stock, but with a ½

percent transactions cost, you would be getting less than you think the stock is worth.

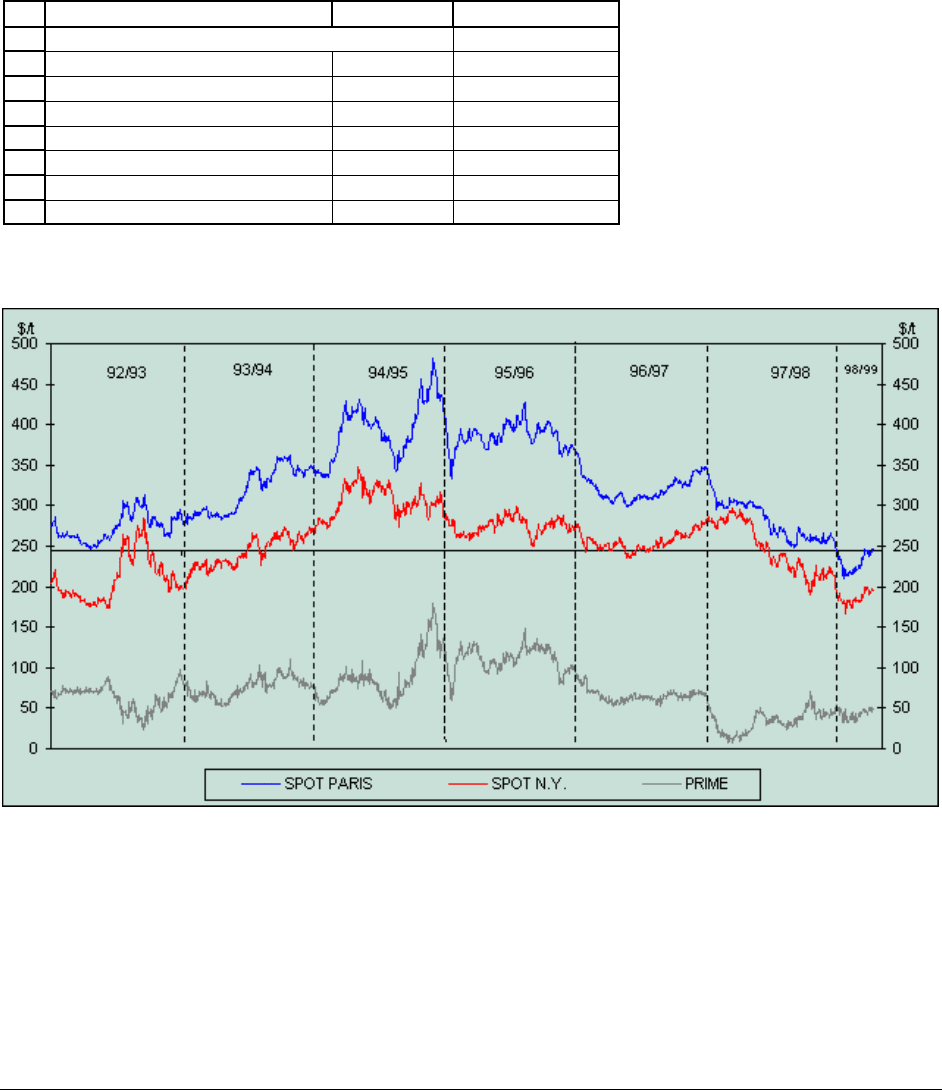

Here’s a more interesting example: Below are the prices of sugar in London and in New

York on 25 July 2003.

1

2

3

4

5

6

7

8

9

10

ABC

New York (dollars/pound) 0.0693

London (dollars/tonne) 208.30

pounds per tonne 2,200

London (dollars/pound) 0.0947 <-- =B3/B4

One container of sugar

Contains 21 tons

in pounds 46,200 <-- =21*B4

"Arbitrage profit" 1,172.64 <-- =(B5-B2)*B9

COMPARING SUGAR PRICES

IN LONDON AND NEW YORK

PFE, Chapter 17, Efficiency page 35

New York sugar is selling for 6.93 cents per pound, whereas sugar in London is selling

for $208.30 per “tonne.” Could there be an opportunity here to make money? In comparing the

prices, you have to make sure the units are the same; for example—a “tonne” is a metric ton,

1,000 kilograms (which equals 2,200 pounds). As you can see, the London price translates to

9.47 cents per pound.

It looks like there’s an arbitrage opportunity here: If we buy sugar in New York and sell

it in London, we can make over 2.5 cents per pound. Since a 20-foot container can hold 21 tons

of sugar (or 46,200 pounds—see cell B9 above), it looks like we could make almost $1,173

profit per container. And since a ship can hold hundreds of containers .... this must be a surefire

way to get rich!

But hold on—this couldn’t be. We must have forgotten the transaction costs:

• It costs money to ship sugar from New York to London. It costs approximately $1,000 to

ship a container of sugar from New York to London. This alone would almost eliminate

the arbitrage profit.

• It takes time to ship sugar from New York to London—somewhere between 10 days and

3 weeks, depending on the availability of shipping. So even if the freight costs are less

that $1,500, this isn’t an arbitrage—it’s a kind of educated gamble on the price

differentials between the two cities.

10

So: There might be a profit here, but it’s not certain. The transaction costs, the cost and

the time needed to ship the sugar from New York to London, will eat up most of the profits. Of

10

What we need is a forward or a futures contract: These are contracts which enable us to fix a price today for sugar

delivered in London at some point in the future. Such contracts exist, but they’re beyond the scope of this book.

For a good text, see John Hull, Options, Futures, and other Derivatives, Prentice-Hall (4

th

edition, 2000).

PFE, Chapter 17, Efficiency page 36

course, this is what you would expect in an efficient market: You can’t make money from things

which are easy to do.

Conclusion

Financial economists use the words “efficient markets” to describe a variety of rules

about financial asset prices which are so simple that they almost always have to be true. In this

chapter we’ve explored several of these asset pricing rules:

• One price for one asset. In an efficient financial market, assets which are the same ought

to have the same value and price.

• Price additivity of asset bundles: In an efficient market bundling two or more assets

together—whether its different kinds of apples in a bag or stocks in a mutual fund—

doesn’t change their value.

• Informational effects on prices: Generally-known information cannot be worth much,

and the more widely the information is known, the less it is worth. We explored three

versions of this principle. The weak-form efficiency principle says that the future asset

price cannot be predicted from knowledge of historical asset prices and the current asset

price. The semi-strong form efficiency principle says that publicly-known information—

not just prices, but published accounting data and other information which can (with

some work) be derived from the information—is worthless. Economists believe that

semi-strong efficiency holds frequently but not always. The strong-form efficiency

principle, which almost no one believes, says that all information—whether public or

not—is worthless.

PFE, Chapter 17, Efficiency page 37

• Transactions costs: These pesky critters can screw up the previous three principles,

because they interfere with arbitrage. Arbitrage, the buying and selling of assets with

profit, is the mechanism by which the three above principles are forced to hold.

Transactions costs, the cost of buying and selling an asset, or the cost of finding out

information about the asset, can make it more difficult to arbitrage and hence cause

market inefficiencies.

PFE, Chapter 17, Efficiency page 38

Exercises

Go back to the bond example of section?? Show that the annualized IRR of the bond is ???.

Now note that this rate is not the discount rate for the cash flows of the individual bonds (the ½

year and 1-year T-bills)! So are markets inefficient?

18

19

20

21

22

23

24

25

ABC

Chapter exercise: The YTM of the bond is

Date Price/CF

0 -963.56

0.5 23

1 1023

IRR 8.66%

Can you make money from this? Sugar prices (source: Bouche???)

PFE, Chapter 17, Efficiency page 39

THE FINANCIAL PAGE

GET SHORTY

by James Surowiecki

Issue of 2003-12-01

A few years ago, the Finance Ministry of Malaysia suggested that a certain group of troublemakers needed to be punished. Caning,

the Ministry said, would be the right penalty. And who were the malefactors being threatened with the rap of rattan? They weren’t

drug dealers or corrupt executives or even gum chewers. They were short sellers.

Short sellers are investors who sell assets (a company’s shares, say) that they have borrowed, in the hope that the price will fall; if it

does, they can buy the shares at a lower price, return them to the trader they borrowed them from, and pocket the difference. In

effect, they are betting against a company’s stock price. As a result, they have, historically, been regarded with great suspicion, and

though the Malaysian proposal was novel, the hostility behind it was not. Shorts have been reviled since at least the seventeenth

century. Napoleon deemed the short seller “an enemy of the state.” England outlawed shorting for much of the eighteenth and

nineteenth centuries. Just last year, Germany’s Finance Minister suggested that short selling should be banned during crises.

Across the world, short sellers continue to be seen as conniving sharpies, spreading false rumors and victimizing innocent

companies with what House Speaker J. Dennis Hastert once called “blatant thuggery.”

The United States, it’s true, hasn’t resorted to the rattan, but it still enforces a set of rules against short selling that have been in

place since the thirties, when shorts were seen as a cause of the Great Crash. In a country as optimistic and can-do as ours, there

seems to be something un-American about betting against stocks. That may be changing. The Securities and Exchange

Commission is now proposing an eighteen-month experiment in which the most onerous restrictions on short selling would be lifted

for three hundred big stocks. If the market for these stocks worked well, the old rules could eventually be lifted across the board.

And it’s about time.

“It’s easy to make short sellers wear the black hats,” James Chanos, the head of Kynikos Associates and one of the few pure short

sellers around, says. “Short selling is always an emotional issue. Executives have their egos tied to the price of their shares, so

when you take a position against them they take it personally.” But give the short sellers their due: they’re the canaries in the coal

mine, recognizing problems before others do. In the past few years alone, shorts sounded early alarms about blow-ups like Enron,

Tyco, and Boston Chicken; they also uncovered scams at lots of smaller companies that tried to cash in on the stock-market

hysteria of the late nineties. In general, the companies that short sellers target deserve it. The economist Owen Lamont studied a

group of companies that had clashed with short sellers—denouncing them in conference calls with investors, imploring shareholders

not to lend them stock, and so forth. He found that the average stock-market return for these companies over the next three years

was minus forty-two per cent, which suggests that their stock prices were as inflated as the shorts had claimed.

Even when short sellers aren’t uncovering malfeasance, their presence in the market is useful. If you think of a stock price as a

weighted average of the expectations of investors, restrictions on short selling skew that average by shutting out people with

contrary opinions. It’s a bit like setting a point spread for a football game by allowing people to bet only on one side. When a team of

Yale management professors did a study of forty-seven stock markets around the world, they found that markets with active short

sellers reacted to information more quickly and set prices more accurately. A traditional justification for short-selling regulations—

including the rule the S.E.C. wants to repeal, which prevents short selling when prices are already falling—is that they protect

markets from panics. Yet the study found no evidence of it. There’s a case to be made that in the late nineties restrictions on short

selling helped inflate the Internet bubble, by reducing any counterweight to the prevailing mania. This, in turn, worsened the

eventual crash.

If the S.E.C. does run its experiment, corporations are hardly going to drown in a deluge of short sales. Today, only two per c

ent of

all United States stock-market shares are shorted, and even with looser restrictions short selling is likely to remain uncommon. In

part, that’s because shorting stocks is simply harder than buying stocks: loans can be called in at any moment, and your potential

losses are unlimited. More important, shorting demands a willingness to challenge Wall Street’s foundational dogma: that stocks

should, and will, go up.

“I used to think that it should be as easy to go short as it is to go long,” Chanos, who was one of the first to see through Enron’s

hype, says. “After all, the two things seem to require the same skill set: you’re evaluating whether a company’s stock price reflects

its fundamental value. But now I think that they aren’t the same at all. Very few human beings perform well in an environment of

negative reinforcement, and if you’re a short, negative reinforcement is what you get all the time. When we come in every day, we

know that Wall Street and the news and ten thousand public-relations departments are going to be telling us that we’re idiots. You

don’t have that steady drumbeat of support behind you that you have if you’re buying stocks. You have a steady drumbeat on your

head.” By lifting the regulatory sanctions on short selling, the S.E.C. might help to weaken the social sanctions. The result should be

a better functioning market, which is in the interest of investors as a whole. Let corporations denounce short sellers all they want.

The case against these bears is a lot of bull.