Genshiro Kitagawa. Introduction to Time Series Modeling (Введение в моделирование временных рядов)

Подождите немного. Документ загружается.

xxii CONTENTS

14 Non-Gaussian State-Space Model 203

14.1 Necessity of Non-Gaussian Models 203

14.2 Non-Gaussian State-Space Models and State Estimation 204

14.3 Numerical Computation of the State Estimation Formula 206

14.4 Non-Gaussian Trend Model 209

14.5 A Time-Varying Variance M odel 213

14.6 Applications of Non-Gaussian State-Sp a ce Model 217

14.6.1 Processing of the outliers by a mixture of

Gaussian distributions 217

14.6.2 A non statio nary discrete proc e ss 218

14.6.3 A direct method of estimating the time-varying

variance 219

15 The Sequential Monte Carlo Filter 221

15.1 The Nonlinear Non-Gaussian State-Space Model and

Approximations of Distributions 221

15.2 Monte Carlo Filter 225

15.2.1 One-step-ahead pred ic tion 225

15.2.2 Filtering 225

15.2.3 Algorithm for the Monte Carlo filter 226

15.2.4 Likelihood of a model 226

15.2.5 Re-sampling method 227

15.2.6 Numerical examples 228

15.3 Monte Carlo Smoothing Method 231

15.4 Nonlinear Smoothing 233

16 Simulation 237

16.1 Generation of Uniform Random Numbers 237

16.2 Generation of Gaussian White Noise 239

16.3 Simulation Using a State-Spac e Model 241

16.4 Simulation with Non-Gaussian Model 243

16.4.1

χ

2

distribution 244

16.4.2 Cauchy distribution 244

16.4.3 Arbitrary distribution 244

A Algorithms for Nonlinear Optimization 249

B Derivation of Levinson’s Algorithm 251

CONTENTS xxiii

C Derivation of the Kalman Filter

and Smoother Algorithms 255

C.1 Kalman Filter 255

C.2 Smoothing 256

D Algorithm for the Monte Carlo Filter 259

D.1 One-Step-Ahead Predictio n 259

D.2 Filter 260

D.3 Smoothing 261

Answers to the Problems 263

Bibliography 277

Index 285

Chapter 1

Introduction and Preparatory Analysi s

In this chapter, various aspects of the classification of time series and the

objectives of time series modeling considered in th is book are discussed.

There are various types of time series, and it is very impo rtant to find out

the char a cteristics o f a time series by carefully looking at graphs of the

data befor e proceeding to the modeling and analysis phase. In the second

half of the chapte r, we shall consider various ways of pre-processing time

series that will be app lied before proceeding to time series modeling.

Finally, the organizatio n of the book is described.

1.1 Time Series Data

A record of phenomenon irregularly varying with time is c alled time

series. As examples of time series, we may consider meteorologica l data

such as atmo spheric pressur e , temperature, rainfall and the record s of

seismic waves; economic data such as stock prices and exchange rates;

medical data such as electroencephalogram a nd electrocardiograms, and

records of contr olling cars, ships and aircraft.

As a first step in the analysis of a time series, it is important to care-

fully examine graphs of the data. These su ggest various possibilities for

the next step in the analysis, together with a ppropriate strategies for sta-

tistical modeling.

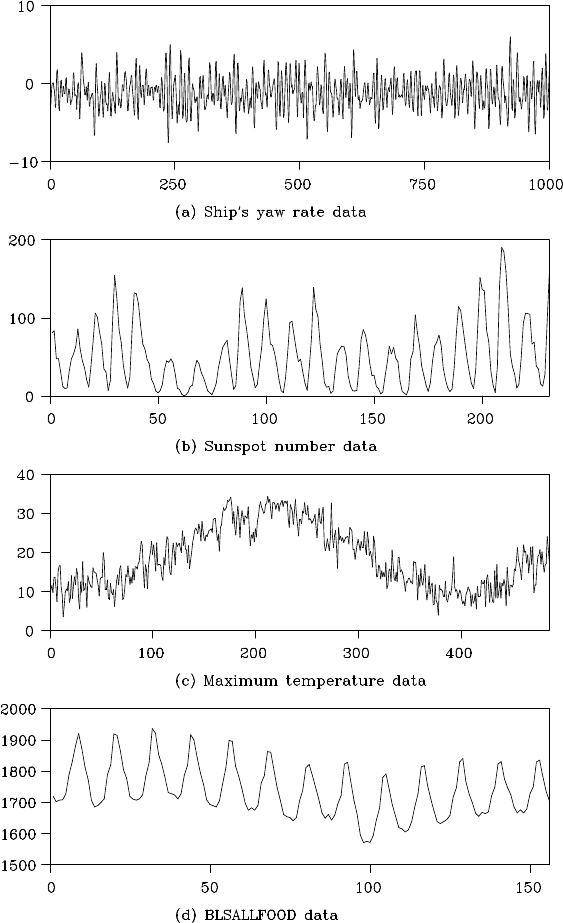

Figure 1.1 shows several typical time series that will be analyzed

in subsequent chapter s as numerical examples. The followings are th e

features of the time series depicted in Figures 1.1 (a)–(i).

Plot (a) shows a time series of the yaw rate of a ship under navigation

in the Pacific Oc ean, observed every second. T he yaw rate fluctuates

around 0 degrees per second, b e cause the ship is under the control of

course keeping system (offered by Prof. K. Ohtsu of Tokyo University

of Marine Science and Technology).

Plot (b) shows a series of annual sunspot numbe r (Wolfer sunspot

number). Similar patterns of in crease and dec rease have been o bserved

over a cycle approximately ten years in length.

1

2 INTRODUCTION AND PREPARATORY ANALYSIS

Figure 1.1: Examples of various time series.

TIME SERIES DATA 3

Figure 1.1: Examples of various tim e series (continued).

Plot (c) shows the daily maximum temperatures for Tokyo recorded

for 16 months. Irregular fluctuations around the predominant annual pe-

riod ( trend) are seen (source: Tokyo District Meteo rological Observa-

tory).

Plot (d) shows the monthly time series of the number of workers en-

gaged in food ind ustries in the United States, called the BLSALLFOOD

data. The data reveal typical features of economic time series that co n-

4 INTRODUCTION AND PREPARATORY ANALYSIS

Figure 1.1: Examples of various time series (continued).

sists of trend an d seasona l components. The trend component gradu-

ally varies and the seasonal c omponent repeats a similar annua l pattern

(source: the U.S. Burea u of Labor Statistics (BLS)).

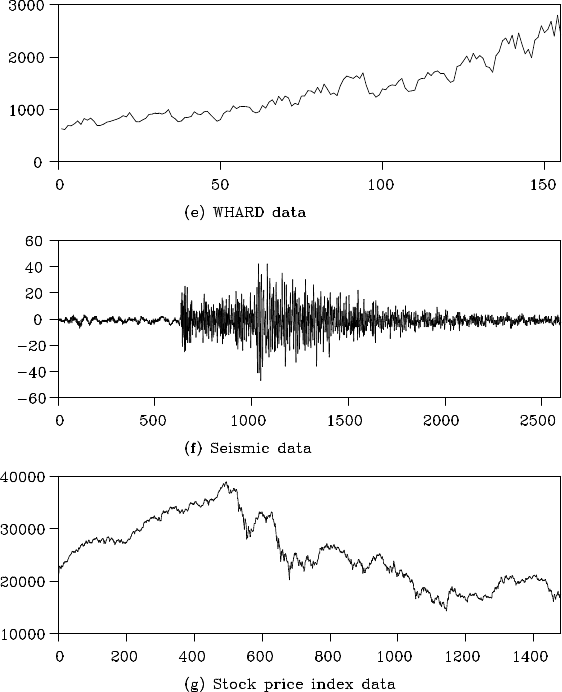

Plot (e) shows the monthly record of wholesale hardware data, called

WHARD data. This time series reveals typical characteristics of eco-

nomic data that increase at an almost fixed rate every ye ar, such tha t

the fluctuations around the trend gradually increase in magnitude over

time (source: U.S. Bureau of Labor Statistics).

Plot (f) shows the time series of East-West components of seismic

waves, recorded every 0.02 seconds. Because of the arrival of th e P-wave

(primary wave) and the S-wave (secondary wave), the variance of the

series changed significantly. Moreover, it can be seen that not on ly the

amplitude but also the freque ncy of the wave vary with time (Takanami

(1991)).

Plot (g) de picts the daily closing values of the Japanese stock price

index, Nikkei 2 25, quoted from January 4, 1988, to December 30, 1993.

It reveals a monotone increase in values until the end of 19 89, followed

by a gradual d ecrease with large re petitive fluctuations after the Bubble

crash in Japan in the 1990s. In the analysis of stock price data, we often

TIME SERIES DATA 5

Figure 1.1: Examples of various tim e series (continued).

apply various analysis m ethods after taking the difference of the log-

transformed data.

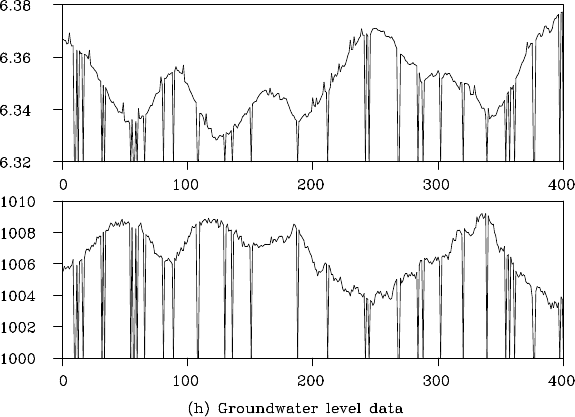

Plot (h) shows a bivariate time series of the groundwater level and

the atmospheric pressure that were observed at 10-min ute in tervals at

the obser vatory of the Tokai region, Japan, where a big earthquake was

predicted to occur. A part of the time serie s tha t takes values on the

horizontal axis, indicates missing observations, and some observations

that significantly deviate upward might be considered as outliers that oc-

curred due to malf unction of the observation device. To utilize the entire

informa tion contained in time series with ma ny missing and outlying ob-

servations recorded over many years, it is necessary to develop a method

6 INTRODUCTION AND PREPARATORY ANALYSIS

that can be applied to data with such missing and outlying observations

(offered by Dr. M. Takahashi and Dr. N. Matsumoto of National Institute

of Advanced Industrial Science and Technology).

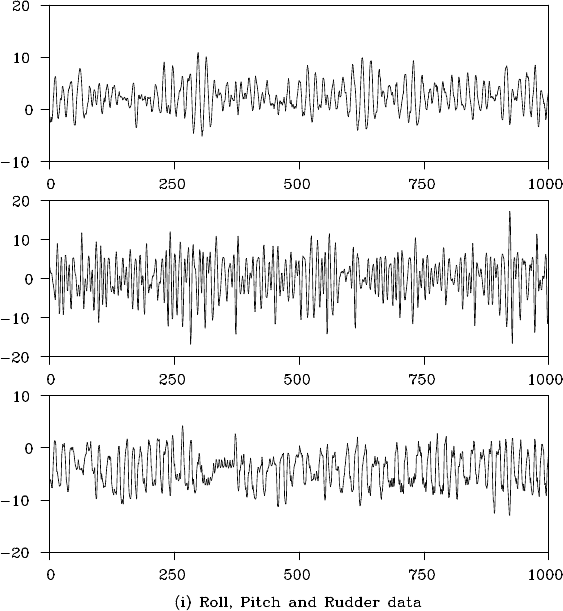

Plot (i) shows a m ultivariate time series of a ship’s rolling, pitching

and rudder angles recorded every second while navigating a cross the Pa-

cific Ocean. As for the rolling an d the rudder angles, both data show fluc-

tuations over a cycle of approximately 16 seconds. On the other hand, the

pitching angle varies over a sh orter cycle of 10 seconds or less (offered

by Prof. K. Ohtsu of Tokyo University of Marin e Science an d Technol-

ogy).

1.2 Classification of Time Series

As has been shown in Figure 1.1, there is a wide variety of time series

that can be classified into several categories from various viewpoints.

Continuous time series and discrete time series

Data continuously recorded, for example, by an analog device, are

called continuous time series. On the other hand, data observed a t cer ta in

intervals o f time, such as the atmospheric pressure measured hou rly, are

called discrete time series.

There a re two types of discrete time series; one where data observa-

tions are at equally spaced inte rvals and the othe r, where data observa-

tions are at unequally spaced intervals. Altho ugh the time series shown

in Figure 1.1 are connected con tinuously by solid lines, they are all d is-

crete time series. Her e after in this book, we consider only discrete time

series reco rded at equally spaced intervals, because time series that we

analyze on digital com puters are usually discrete time series.

Univariate and multivariate time series

Time series consisting of a single o bservation at e ach time point as

shown in Fig ures 1.1(a )–1.1(g) are called univariate time series. On the

other hand, time series that are obtaine d by simu ltaneously recording

two or more p henomena as the examples depicted in Figur e s 1.1(h)–

1.1(i) are called multivariate time series. However, it may b e difficult

to distinguish betwee n univariate and multivariate time series from their

nature; rather the distinction is made from the analyst’s viewpoint and b y

various oth e r factors such as the m easurement restriction and empirical

or theoretical knowledge about the subject. From a statistical modeling

point of view, variable selection itself is an important problem in time

series analysis.

CLASSIFICATION OF TIME SERIES 7

Stationary and nonstationary time series

A time series is a record of a phe nomenon irregularly varying over

time. In time series analysis, irregularly varying time series are generally

expressed by stochastic mod els. In some cases, a random phenomenon

can be co nsidered as a realization of a stochastic model with a time-

invariant structure. Such a time series is called a stationary time series.

Figure 1.1(a) is a typical example of a stationary time series.

On the other ha nd, if the stochastic structure of a time series itself

changes over time, it is called a nonstationary time series. As typical ex-

amples of n onstationary time series, consider the series in Figures 1.1(c),

(d), (e) and 1.1(g). It can be seen that mean values change over time in

Figures 1.1(c), ( d), (e) and 1.1(g) and the fluctuation around the mean

value changes over time in Figure 1.1(f).

Gaussian and non-Gaussian time series

When a distribution of a time series follows a normal distribution,

the time series is ca lled a Gaussian time series; oth erwise, it is called a

non-Gaussian time series. Most of the models considered in this book

are Gaussian models, under the assumption that the time series follow

Gaussian distributions.

As in the case of Figure 1.1(b) , the pattern of the time series is o cca-

sionally asymmetric so that the marginal distribution cannot be c onsid-

ered as Gaussian. Even in such a situation, we may obtain an approxi-

mately Gaussian time ser ie s by an app ropriate da ta transformation. This

method will be introduced in Section 1.4 and Section 4.5.

Linear and nonlinear time series

A time series that is expressible as the output of a linear model is

called a linear time series. In c ontrast, the output from a nonlinear model

is called a nonlinear time series.

Missing observations and outliers

In time series modeling of real-world problems, we sometime s need

to deal with missing observations and outliers. Some values of time se-

ries that have not been recorded for some re asons are called missing

observations in th e time series; see Figure 1.1(h). Outliers (outlying ob-

servations) might occur due to extraordinary behavior of the object, mal-

function of the observation device or errors in recording. I n the ground-

water level da ta shown in Figure 1.1(h), some data jumping up ward are

considered to be outliers.

8 INTRODUCTION AND PREPARATORY ANALYSIS

1.3 Objectives of Time Series Analy sis

This book presents statistical modeling methods for time series. The o b-

jectives of time series analysis considered in this book a re classified into

four categories; description, modeling, prediction and signal extraction.

Description: This includes methods that effectively express or sum-

marize the charac te ristics of time series. By drawing figures of time

series or by computing basic descriptive statistics, such as sample

autocorrelation functions, sample autocovariance functions and peri-

odograms, we may capture essential characteristics of the time series

and get a hint for time series modeling.

Modeling: In time series modeling, we capture the stochastic struc-

ture of time series by identifying an appropriate model. Sinc e there

are various types of time series, it is necessary to select an adequate

model class and to estimate parameters included in the mode l, de-

pending on the characteristics of the time series and the objective o f

the time series analysis.

Prediction: In the prediction of time series, based on the correlations

over time and among the variables, we can e stima te th e future behav-

ior of time series by using various information extracted from current

and past observations. In particular, in this book, we shall consider

methods of prediction and simulation based on the estimate d time se-

ries mod els.

Signal extraction: In signal extraction problems, we extract essential

signals or useful information from time series corresponding to the

objective of the analysis. To achieve that purpo se, it is important to

build models based on the salient characteristics of the object and the

purpose of the an a lysis.

1.4 Pre-processing of Time Series

For nonstation ary time series, we some times perform pre-pr ocessing of

the data before app lying the analysis metho ds that are introduced later in

this boo k. This section treats some methods of transfo rming nonstation-

ary time series into approximately stationary time series. In Chapter 11

and thereina fter, however, we shall introduce various methods for mod-

eling and analyzing nonstatio nary time series without pre-processing or

stationalization.