Citibank: basic of corporate finance

Подождите немного. Документ загружается.

6-18 CORPORATE VALUATION – RISK

v-1.1 v.05/13/94

p.01/14/00

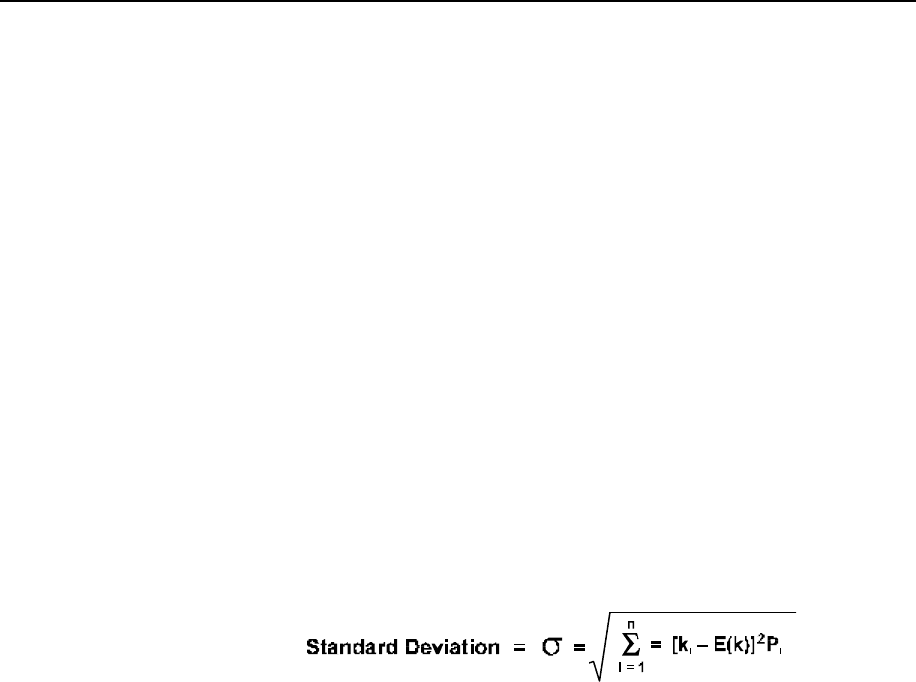

As you can see, the standard deviation of Project A's possible cash

flows is considerably less than the standard deviation of Project B's. In

other words, Project A's possible cash flows, on average, deviate less

from the expected cash flow.

Lower standard

deviation means

less volatility

Project A has the same expected cash flow as Project B, but with

considerably less volatility (or spread) among the possible cash flows.

Project A is considered less risky than Project B and, therefore, the

better investment.

Standard

deviation of

expected

returns

The method for calculating the standard deviation of a set of possible

returns is to take the square root of the variance of that set of returns.

For example, the standard deviation for the possible stock returns of

XYZ Corporation would be s = (4,335)

½

= 65.84%.

The formula for the standard deviation of expected returns is:

Summary

In this section, we discussed the use of the statistical measures of

variance and standard deviation to measure the risk associated with

a project or investment. The variance is the sum of the squared

deviations from the possible cash flows or expected returns that have

been weighted by the probability of each deviation's occurrence.

Standard deviation (the square root of the variance) is preferred by

analysts because it is easier to use as a measure of risk. A lower

standard deviation indicates less volatility among possible cash flows

or returns and, therefore, a lower amount of risk.

Before continuing to the section on "Portfolio Risk," please complete the Practice

Exercise which follows.

www.LisAri.com

CORPORATE VALUATION – RISK 6-19

v.05/13/94 v-1.1

p.01/14/00

PRACTICE EXERCISE 6.2

Directions: For Project X and Project Y, use the information provided in the payoff

matrices to calculate the variation and the standard deviation. After you

have completed every exercise on this page, compare your answers to the

correct ones on the next page.

1. For Project X, the expected cash flow is $22,000.

(1) (2) (3) (4) (5) (6)

Estimate

Number

Probability

P

1

Possible

Cash Flow

CF

1

Deviation

CF

1

–E(CF)

Deviation

Squared

[CF

1

–E(CF)]

2

(2) x (5)

Weighted

Deviation

1

2

3

0.20

0.50

0.30

$16,000

22,000

26,000

________

________

________

________

________

________

Variance =

________

________

________

_____________

For Project X the standard deviation is ________________________

2. For Project Y, the expected cash flow is $26,000.

(1) (2) (3) (4) (5) (6)

Estimate

Number

Probability

P

1

Possible

Cash Flow

CF

1

Deviation

CF

1

–E(CF)

Deviation

Squared

[CF

1

–E(CF)]

2

(2) x (5)

Weighted

Deviation

1

2

3

0.20

0.50

0.30

$15,000

22,000

40,000

_______

_______

_______

_______

_______

_______

Variance =

_______

_______

_______

_____________

For Project Y the standard deviation is ________________________

www.LisAri.com

6-20 CORPORATE VALUATION – RISK

v-1.1 v.05/13/94

p.01/14/00

ANSWER KEY

1. For Project X, the expected cash flow is $22,000.

(1) (2) (3) (4) (5) (6)

Estimate

Number

Probability

P

1

Possible

Cash Flow

CF

1

Deviation

CF

1

–E(CF)

Deviation

Squared

[CF

1

–E(CF)]

2

(2) x (5)

Weighted

Deviation

1

2

3

0.20

0.50

0.30

$16,000

22,000

26,000

-6,000

0

4,000

36,000,000

0

16,000,000

Variance =

7,200,000

0

4,800,000

12,000,000

For Project X the standard deviation = (variance)

½

= (12,000,000)

½

= 3,464.10

2. For Project Y, the expected cash flow is $26,000.

(1) (2) (3) (4) (5) (6)

Estimate

Number

Probability

P

1

Possible

Cash Flow

CF

1

Deviation

CF

1

–E(CF)

Deviation

Squared

[CF

1

–E(CF)]

2

(2) x (5)

Weighted

Deviation

1

2

3

0.20

0.50

0.30

$15,000

22,000

40,000

-11,000

-4,000

14,000

121,000,000

16,000,000

196,000,000

Variance =

24,200,000

8,000,000

58,800,000

91,000,000

For Project Y the standard deviation = (variance)

½

= (91,000,000)

½

= 9,539.4

www.LisAri.com

CORPORATE VALUATION – RISK 6-21

v.05/13/94 v-1.1

p.01/14/00

PORTFOLIO RISK

Up to now, the discussion has focused on the methods used to identify

and measure risk associated with individual investment securities. Large

investors such as mutual funds, pension funds, insurance companies, and

other financial institutions own stocks of many different companies —

government regulations require that they do so. Individual investors also

purchase the stock

of several different firms rather than invest with one company. In this

section, we explain the reasons why investors prefer to vary their stock

holdings.

Portfolio Diversification

The collection of investment securities held by an investor is

referred to as a portfolio. Diversification is the strategy of investing

with several different industries. If an investor maintains a portfolio

that holds Ford Motor Company, Exxon, and IBM stocks, that

investor is said to have a portfolio diversification.

Focus on

expected return

of a portfolio

An investor with a diversified portfolio is not overly concerned when

an individual security in the portfolio moves up or down. The main

concern is the riskiness and overall return of the portfolio.

Therefore, the risk and return of each security needs to be analyzed in

terms of how that security affects the risk and return of the entire

portfolio.

The method for calculating the expected rate of return of a portfolio

of stocks can be illustrated with an example.

Example

An investor has invested $10,000 in a portfolio of stocks. The

amount invested and the expected rate of return for each stock in that

portfolio is as follows:

• $2,000 invested in General Motors, which is expected to earn a

14% rate of return

www.LisAri.com

6-22 CORPORATE VALUATION – RISK

v-1.1 v.05/13/94

p.01/14/00

• $5,000 invested in Ford Motor Company, which is expected to

generate a 17% return

• $3,000 invested in Chrysler Motors, which is expected to earn

an 18% return

Now, let's arrange the portfolio in a payoff matrix.

Stock Amount

(W

i

)

Weight

(k

i

)

Expected

Return

(W

i

x k

i

)

Weighted

Return

GM

Ford

Chrysler

$2,000

5,000

3,000

0.20

0.50

0.30

14%

17%

18%

Expected

Return E (k

p

) =

2.80

8.50

5.40

16.70%

Figure 6.11: Payoff Matrix for Stock Portfolio

The expected return of the portfolio is calculated using almost the

same method as we use to calculate the expected return for a range of

possible returns of an individual stock. The only difference is that the

weights in a portfolio are derived from the percentage of an

individual investment relative to the total amount invested in the

portfolio. In this example, the total portfolio investment is $10,000;

the investment in General Motors stock is $2,000 or 20% of the

portfolio. Therefore, the portfolio weight of GM stock in the

payoff matrix is .20. The weights always total 1.0.

Calculating risk

for portfolio of

stocks

Unlike the portfolio's expected return, the riskiness of the portfolio

is not a weighted average of the standard deviations of the individual

stocks in the portfolio. The portfolio's risk will be smaller than the

weighted average of the standard deviations because the variations in

the individual stocks will be offsetting to some degree.

Example

Let's consider an example to illustrate the concept of offsetting

variations. The rates of return over a five year period for two stocks

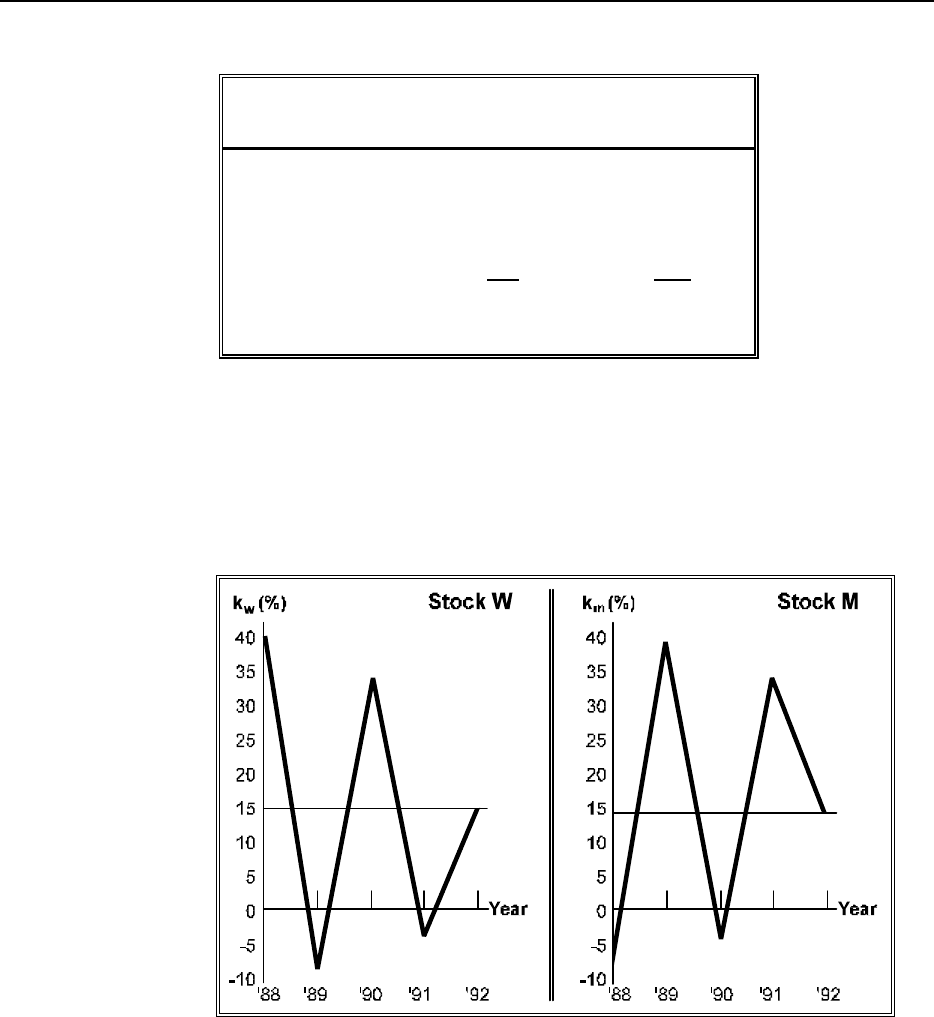

(W and M) are listed in Figure 6.12.

www.LisAri.com

CORPORATE VALUATION – RISK 6-23

v.05/13/94 v-1.1

p.01/14/00

Stock W

k

w

(%)

Stock M

k

M

(%)

1988

1989

1990

1991

1992

Average Return

Standard Deviation

40

-10

35

-5

15

15

22.6

-10

40

-5

35

15

15

22.6

Figure 6.12: Rates of Return for Stocks W and M over Five Years

In Figure 6.13 you can see the rates of return for both stocks plotted

on graphs. Notice the patterns of rate variation.

Figure 6.13: Rates of Return for Stock W and Stock M

Offsetting

variations

If held individually, both stock W and stock M would have a high level

of risk. As you can see from the graphs, a rise in the rate of return in

stock W is offset by an equal fall in the rate of return of stock M.

Imagine the profile of a portfolio where each of these stocks r

epresents 50% of the total investment.

www.LisAri.com

6-24 CORPORATE VALUATION – RISK

v-1.1 v.05/13/94

p.01/14/00

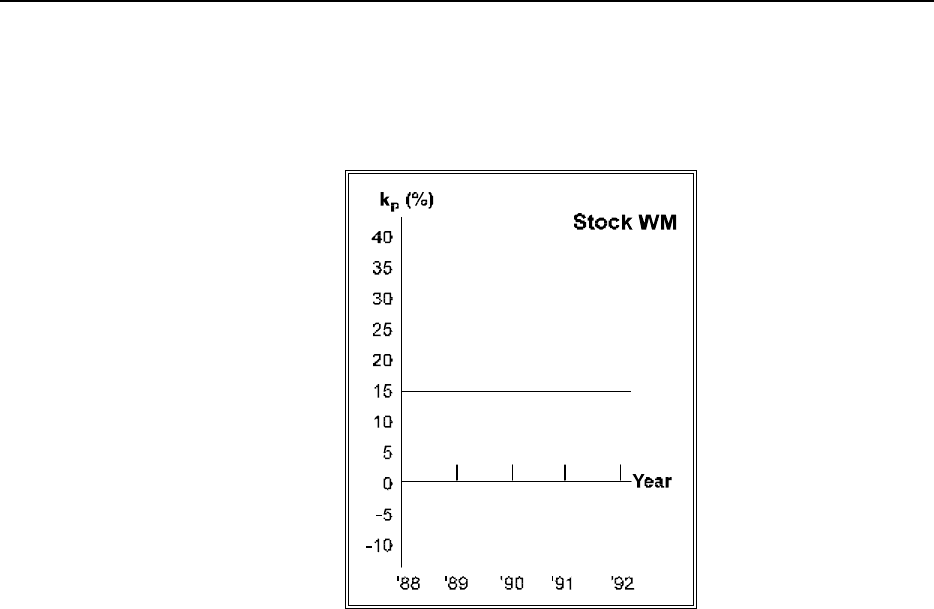

The rate of return distribution for portfolio WM is shown in

Figure 6.14.

Figure 6.14: Rate of Return Distribution for Portfolio WM

Risk-free

portfolio

Portfolio WM shows a 15% rate of return for each year, with no

risk at all. The reason that stock W and stock M can be combined to

form a risk-free portfolio is that their returns move in opposition to

each other.

Correlation

coefficient

In statistics, the tendency of two variables to move together is

called correlation. The correlation coefficient (r) is the measure

of this tendency. To learn how to calculate the correlation

coefficient, consult any beginning statistics text. All of the

examples in this workbook will have the correlation coefficient

already calculated. You should become familiar with what the

correlation coefficient represents and how it is used.

Value of r

The correlation coefficient (r) ranges between +1.0 to -1.0. Let's

see what the values represent.

• If r = +1.0 (perfectly positively correlated), the two variables

move up and down in perfect synchronization.

• If r = -1.0 (perfectly negatively correlated), the two variables

always move in exact opposite directions.

www.LisAri.com

CORPORATE VALUATION – RISK 6-25

v.05/13/94 v-1.1

p.01/14/00

• If r falls between +1.0 and -1.0, correlation occurs in varying

degrees.

• If r = 0.0, the two variables are not related to each other –

changes in one variable are independent of changes in the other.

In the example, stock W and stock M have a correlation coefficient of

-1.0 (perfectly negatively correlated). Diversification with these two

stocks creates a risk-free portfolio.

If two stocks in a portfolio are perfectly positively correlated (r =

+1.0), and if the standard deviations for the stocks are not equal,

diversification does not eliminate any risk. The portfolio of the two

stocks will have the same risk as holding either stock on its own.

Impossible to

eliminate all

risk

Portfolios with two perfectly negatively correlated stocks (r =

-1.0) or two perfectly positively correlated stocks (r = +1.0) are

extremely rare. In fact, most pairs of stocks are positively

correlated, but not perfectly. On average, the correlation coefficient

for the returns of two randomly selected stocks would be about

+0.6. For most pairs of stocks, the correlation coefficient will be

between +0.5 and +0.7. For this reason, it is impossible to eliminate

all risk by combining stocks into a portfolio.

Example

We used portfolio WM to illustrate a point. Let's look at a more

realistic example. Consider stock W and stock Y. The rates of return

for the two stocks and for a portfolio equally invested in the two

stocks are listed in Figure 6.15. The standard deviations for each set

of returns, and the portfolio as a whole, have already been

calculated. The correlation coefficient is r = +0.65.

www.LisAri.com

6-26 CORPORATE VALUATION – RISK

v-1.1 v.05/13/94

p.01/14/00

Stock W

k

w

(%)

Stock Y

k

y

(%)

Portfolio WY

k

p

(%)

1988

1989

1990

1991

1992

Average Return

Standard Deviation

40

-10

35

-5

15

15

22.6

28

20

41

-17

3

15

22.6

34

5

38

-11

9

15

20.6

Figure 6.15: Return Rates and Standard Deviation for Stocks W

and Y and Portfolio WY

You can see that stock W, stock Y, and portfolio WY each have an

average return of 15%. The average return on the portfolio is the same

as the average return on either stock. The standard deviation is 22.6 for

each stock and 20.6 for the portfolio. Even though the two stocks are

positively correlated (+0.65), the risk is reduced by combining the

stocks into a portfolio. A stock analyst might say that combining the

two stocks "diversifies away some of the risk."

Diversification

eliminates some

risk

This example illustrates that the risk of the portfolio as measured by

the standard deviation is not the average of the risk of individual

stocks in the portfolio. Typically, if the correlations among individual

stocks are positive, but less than +1.0, some of the risk may be

eliminated.

Positive

correlation

between same-

industry

companies

It is important to recognize that companies in the same industry

generally have a more positive correlation coefficient for expected

returns than companies in different industries. For example, you

would expect the correlation between the returns of Ford Motor

Company and the returns of General Motors to be more positive than

the correlation between the returns of Ford Motor Company and

IBM. Thus, a two-stock portfolio of companies within the same

industry is probably riskier than a two-stock portfolio of companies

operating in different industries. Portfolios should be diversified

between industries as well as companies to eliminate the maximum

amount of risk.

www.LisAri.com

CORPORATE VALUATION – RISK 6-27

v.05/13/94 v-1.1

p.01/14/00

Systematic and Unsystematic Risk

Expected vs.

uncertain return

To evaluate the risk associated with an individual security or a

portfolio of securities, the realized return to investors must be

broken into two parts:

1) Expected return

2) Uncertain return

Expected return

based on

current market

factors

For a stock (equity security), the expected return is the part that

investors and analysts can predict. These predictions are based on

information about current market factors that will influence the stock

in the future. We discussed this process in Unit Two in our

discussion on interest rates. By studying external and internal factors

that affect a company's operations, analysts can assess how each

factor may affect the company. The stock price of a company is

determined by expectations of a company's future prospects based on

the influence of all factors.

Uncertain

return

influenced by

unexpected

factors

The other part of the return of a stock is the uncertain or risky part

that comes from unexpected factors arising during the period. For

example, an unexpected research breakthrough may cause a

company's stock to rise; a sudden, unexpected rise in inflation rates

may cause a company's stock to fall.

Company

specific,

diversifiable

risk

These two parts of the realized return translate into two types of risk:

(1) risk specific to a single company or a small group of companies,

and (2) risk that affects all companies in the market.

In the stock W and stock Y example, when we created a diversified

portfolio to eliminate some of the risk associated with each stock,

we eliminated the company-specific risk. This type of company-

specific, diversifiable risk is called unsystematic risk.

www.LisAri.com