Citibank: basic of corporate finance

Подождите немного. Документ загружается.

6-28 CORPORATE VALUATION – RISK

v-1.1 v.05/13/94

p.01/14/00

Creating a diversified portfolio of stocks enables an investor to

eliminate nearly all unsystematic risk. The unexpected events that cause

unsystematic risk include things like strikes, lawsuits, winning or losing

major contracts, etc. Since these events that make up company-specific

risk are essentially random occurrences, diversification allows us to

eliminate them as risk factors. In other words, on average, the positive

events of all the companies in the portfolio tend to cancel out the

negative events.

Risk that

affects the

entire market

The other type of risk is called systematic risk (market risk or

undiversifiable risk). Systematic risk cannot be eliminated by

diversification because the unexpected events that create systematic

risk affect all companies in the market. Such events may include war,

inflation, recession, etc.

The risk of an individual security is not the primary concern of the

investor. The relevant riskiness of an individual security is its

contribution to the riskiness of a well-diversified portfolio. For

example, the riskiness of Ford Motor stock is the contribution that the

Ford stock makes to the overall riskiness of the portfolio in which it is

held.

Reduction of

unsystematic

risk

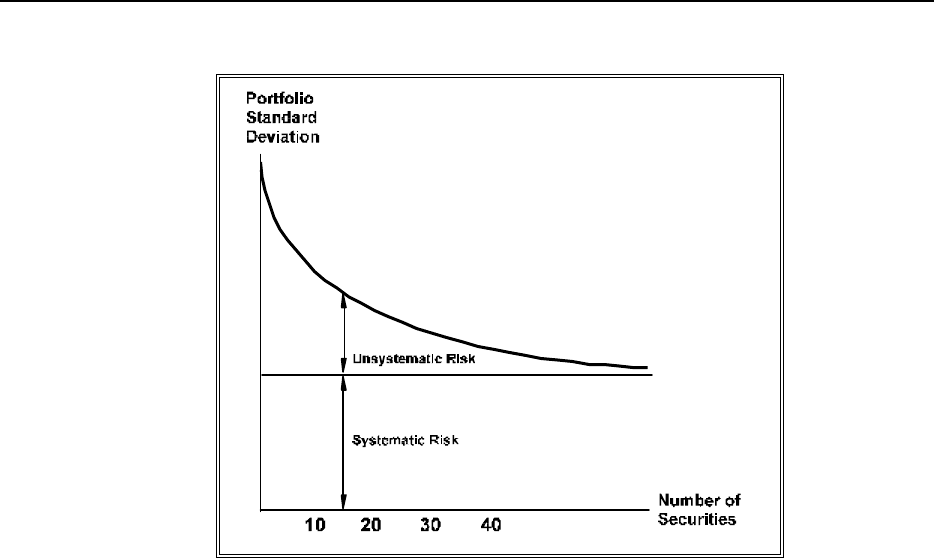

The graph in Figure 6.16 illustrates how the addition of securities

to the portfolio eliminates the unsystematic risk, while the systematic

risk remains constant. The standard deviation for the expected return

of the portfolio is on the vertical axis. The number of securities held

in the portfolio is on the horizontal axis.

www.LisAri.com

CORPORATE VALUATION – RISK 6-29

v.05/13/94 v-1.1

p.01/14/00

Figure 6.16: Reduction of Unsystematic Risk

You can see that as the number of securities increases, the amount

of unsystematic risk declines. Many studies have been completed to

determine the optimal size of a portfolio. Analysts say that over

95% of the unsystematic risk is eliminated in a portfolio of about

40 securities.

Market index

portfolio

A portfolio that contains all of the stocks in the market, based on

weight within the market, is often called the market portfolio. The

New York Stock Exchange (NYSE) lists over 1,500 different stocks.

The standard deviation for a market index portfolio containing all of

the NYSE stocks historically has been about 15.1% (s

M

= 15.1%).

This represents the amount of risk that can not be eliminated by

diversification and corresponds to the risk premium that is added to

the risk-free level of interest rates discussed in Unit Two.

www.LisAri.com

6-30 CORPORATE VALUATION – RISK

v-1.1 v.05/13/94

p.01/14/00

Summary

An investor with a diversified portfolio has invested with different

companies in several industries to reduce unsystematic (company-

specific) risk.

Events that affect the entire market, such as war, inflation, and

recession, contribute to the systematic or undiversifiable risk of

a portfolio.

The relevant risk of holding a security is the individual security's

contribution to the overall risk of the portfolio. Different securities

will affect the same portfolio differently. The same security will have

different contributions to different portfolios. Investors will not be

rewarded for assuming risk that could have been eliminated through

diversification. The type of risk that remains after diversification is

systematic (market) risk.

Please check your understanding of "systematic" and "unsystematic risk" in Practice

Exercise 6.3. In the next section you will see how to measure systematic risk.

www.LisAri.com

CORPORATE VALUATION – RISK 6-31

v.05/13/94 v-1.1

p.01/14/00

PRACTICE EXERCISE 6.3

Directions: Mark the correct answer to each question. Compare your solutions to the

correct answers in the Answer Key that follows on the next page.

3. Portfolio diversification is an important strategy for investors because it:

____ a) reduces expected returns.

____ b) increases expected returns.

____ c) reduces systematic risk.

____ d. reduces unsystematic risk.

4. The type of risk that investors are compensated for is:

____ a) total risk.

____ b) unsystematic risk.

____ c) systematic risk.

____ d) normal or expected return.

Use the following portfolio information for the next question.

Amount Expected

Security Invested Weight Return

Stock A $5,000 0.25 9%

Stock B $5,000 0.25 10%

Stock C $6,000 0.30 11%

Stock D $4,000 0.20 12%

5. What is the expected return on the portfolio?

____ a) 10.00%

____ b) 10.25%

____ c) 10.45%

____ d) 10.50%

www.LisAri.com

6-32 CORPORATE VALUATION – RISK

v-1.1 v.05/13/94

p.01/14/00

ANSWER KEY

3. Portfolio diversification is an important strategy for investors because it:

d) reduces unsystematic risk.

Portfolio diversification reduces unsystematic risk. It does not

reduce market risk (systematic risk).

4. The type of risk that investors are compensated for is:

c) systematic risk.

Investors can expect to be rewarded for assuming systematic

risk since they can diversify their portfolio to minimize or

eliminate unsystematic risk.

5. What is the expected return on the portfolio?

c) 10.45%

Weight x

Amount Expected Expected

Security Invested Weight Return Return

Stock A $5,000 0.25 9% 2.25%

Stock B $5,000 0.25 10% 2.50%

Stock C $6,000 0.30 11% 3.30%

Stock D $4,000 0.20 12% 2.40%

Expected Return 10.45%

www.LisAri.com

CORPORATE VALUATION – RISK 6-33

v.05/13/94 v-1.1

p.01/14/00

Beta

Standard deviation is used to measure the risk of an individual stock —

the type of risk that can be reduced by diversification. What is needed

is a method for measuring an individual stock's contribution to the

systematic risk of a portfolio.

Measure of

stock's

volatility

The beta coefficient (b) is the measure of a stock's volatility

relative to that of an average stock. In other words, it reflects the

degree to which the price of a stock tends to move with movements

in the market.

An average stock is defined as a stock that tends to move up and down in

step with the market as a whole. The market is often measured by using

an index such as the New York Stock Exchange (NYSE), the Standard

and Poor's 500 (S&P 500), or the Dow Jones Industrial average. These

indices serve as good representations of

the entire United States stock market. For example, the S&P 500 is

a weighted-average portfolio of the stocks of 500 of the largest and

most stable U.S. companies. It is often selected to represent the

movements of the entire U.S. stock market. Analysts use these indices

to measure the entire market because information for the companies in

an index is easily obtained, making analysis quicker and less expensive.

Covariability of

stock with the

market

The beta coefficient measures the covariability (relative movement)

of a stock as compared to a benchmark which, in this case, is the

market portfolio. An average-risk stock has a beta coefficient of 1.0.

This means that if the market moves up by 10%, the stock will, on

average, move up by 10%. Likewise, if the market moves down by

10%, the stock will, on average, fall 10%. Less than average-risk

stocks have betas between 0.0 and 1.0, whereas higher than average-

risk stocks have betas greater than 1.0.

www.LisAri.com

6-34 CORPORATE VALUATION – RISK

v-1.1 v.05/13/94

p.01/14/00

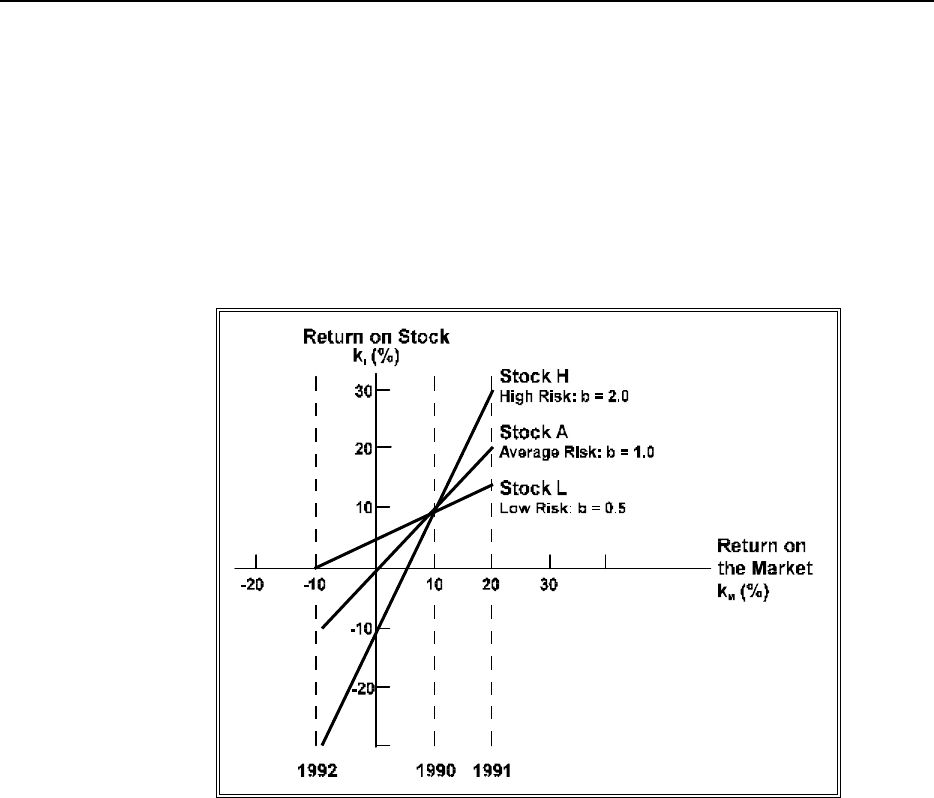

Example

You can see the covariability of three stocks by looking at the graph

in Figure 6.17. The vertical axis represents the return on each

individual stock, and the horizontal axis represents the return on the

market. Plotted on the graph are the returns for three stocks for the

years 1990, 1991, and 1992: H (for high risk), A (for average risk),

and L (for low risk).

Figure 6.17: Covariability of Stocks H, A, and L with the Market

In 1990, all three stocks had a 10% return — the same as the market's

return. In 1991, the market return rose to 20%. Stock A also earned

20%, Stock H soared to a 30% return, and Stock L earned a 15%

return. In 1992, the market fell to a -10% return. Stock A also fell to -

10%, while Stock H fell to -30% and Stock L earned a 0% return.

Stock H was twice as volatile as the market and, therefore, it carried

twice as much risk. Stock H's beta coefficient of 2.0

represents the risk. Stock A moved the same as the market moved and

has a beta coefficient of 1.0. The low-risk security, Stock L, moved

half as much as the market and, therefore, has a beta of 0.5.

www.LisAri.com

CORPORATE VALUATION – RISK 6-35

v.05/13/94 v-1.1

p.01/14/00

Beta is equal

to the slope

The slopes of the lines show how much the return of each stock

moves in response to movement in the return on the market as a

whole. A security's beta is equal to the slope on this type of graph.

There are several different ratings companies that calculate and

publish the beta coefficients for thousands of companies.

If a company with a beta coefficient greater than 1.0 is added to an

average-risk portfolio, the overall risk of the portfolio will increase. On

the other hand, adding a stock with a beta coefficient less than 1.0 will

reduce the overall risk of an average-risk portfolio.

Example

Let's analyze a simple example to organize what we have learned.

Suppose we have the following information for stock X and stock Y.

Standard

Deviation Beta

Stock X 40% 0.50

Stock Y 20% 1.50

We know the following about stock X and stock Y:

1) Beta represents systematic risk. Stock X has less systematic risk

than stock Y.

2) Standard deviation represents total risk. Stock X has more total

risk than stock Y.

3) Total risk equals systematic plus unsystematic risk. Stock X

must have more unsystematic risk than stock Y.

4) Investors earn a return on systematic risk. Stock Y will have a

higher expected return and a higher risk premium even though

its total risk is less than the total risk of stock X.

www.LisAri.com

6-36 CORPORATE VALUATION – RISK

v-1.1 v.05/13/94

p.01/14/00

Portfolio beta

calculation

The beta of a portfolio can be calculated if the information about

the beta of each stock in the portfolio and the amount invested in

each stock is known. The formula is a weighted average of the

individual stock beta coefficients.

m

b

P

= S = W

i

b

i

i = 1

Where:

b

P

= Beta coefficient of the portfolio

m = Number of securities in the portfolio

W

i =

Relative weight invested in each security

b

i =

Beta coefficient of security i

i = Each specific security

Example

To illustrate the use of the formula, suppose that a portfolio contains

the following stocks.

Amount Beta

Security Invested Coefficient

Stock A $1,000 0.80

Stock B $2,000 0.95

Stock C $3,000 1.10

Stock D $4,000 1.40

Sum of

weighted beta

coefficients

To calculate the portfolio beta coefficient, multiply each stock's

weight in the portfolio by its beta and add up the products. Two

columns have been added to the table: "Weight" — the relative weight

in the portfolio of each stock and "Weight x Beta" — the weighted

beta coefficients. The beta coefficient of the portfolio is the sum of

these products.

Amount Beta Weight x

Security Invested Weight Coefficient Beta

Stock A $1,000 0.10 0.80 0.08

Stock B $2,000 0.20 0.95 0.19

Stock C $3,000 0.30 1.10 0.33

Stock D $4,000 0.40 1.40 0.56

Portfolio Beta b

P

= 1.16

www.LisAri.com

CORPORATE VALUATION – RISK 6-37

v.05/13/94 v-1.1

p.01/14/00

Remember, the relative weight of a security is its percentage of the

total investment. These weights must add to 1.0.

For this example, the beta coefficient of the portfolio is 1.16.

Because the beta is larger than 1.0, this portfolio has greater

systematic risk than the market portfolio.

As mentioned earlier, investors are rewarded for bearing systematic risk.

The next step will be to calculate the amount of the reward.

Summary

Beta is a measure of the systematic risk for a security or a portfolio

relative to a market portfolio. Beta does not capture unsystematic,

diversifiable risk. The beta coefficient measures the covariability of

a security's or portfolio's volatility with the volatility of the market

as a whole.

Please check your understanding of "beta" in the Practice Exercise which follows. You will

then be ready to continue to the final section of this unit.

www.LisAri.com