CIMA CO2 Official Learning System - Fundamentals of Financial Accounting

Подождите немного. Документ загружается.

ACCOUNTING FOR NON-CURRENT ASSETS

SOLUTIONS TO REVISION QUESTIONS C2

180

Solution 2

●

This is a straight test of double-entry bookkeeping principles for non-current assets.

●

It requires a calculation of the accumulated depreciation of the disposed asset up to the

date of disposal in accordance with the method and policy stated in the question, and

then to calculate the depreciation charge for each of the 2 years.

●

The purchases and sales of vehicles do not involve purchases and sales accounts.

●

The sale proceeds are part of the calculation of the profi t or loss on disposal – do not use

this fi gure in transferring the asset at cost out of its ledger account.

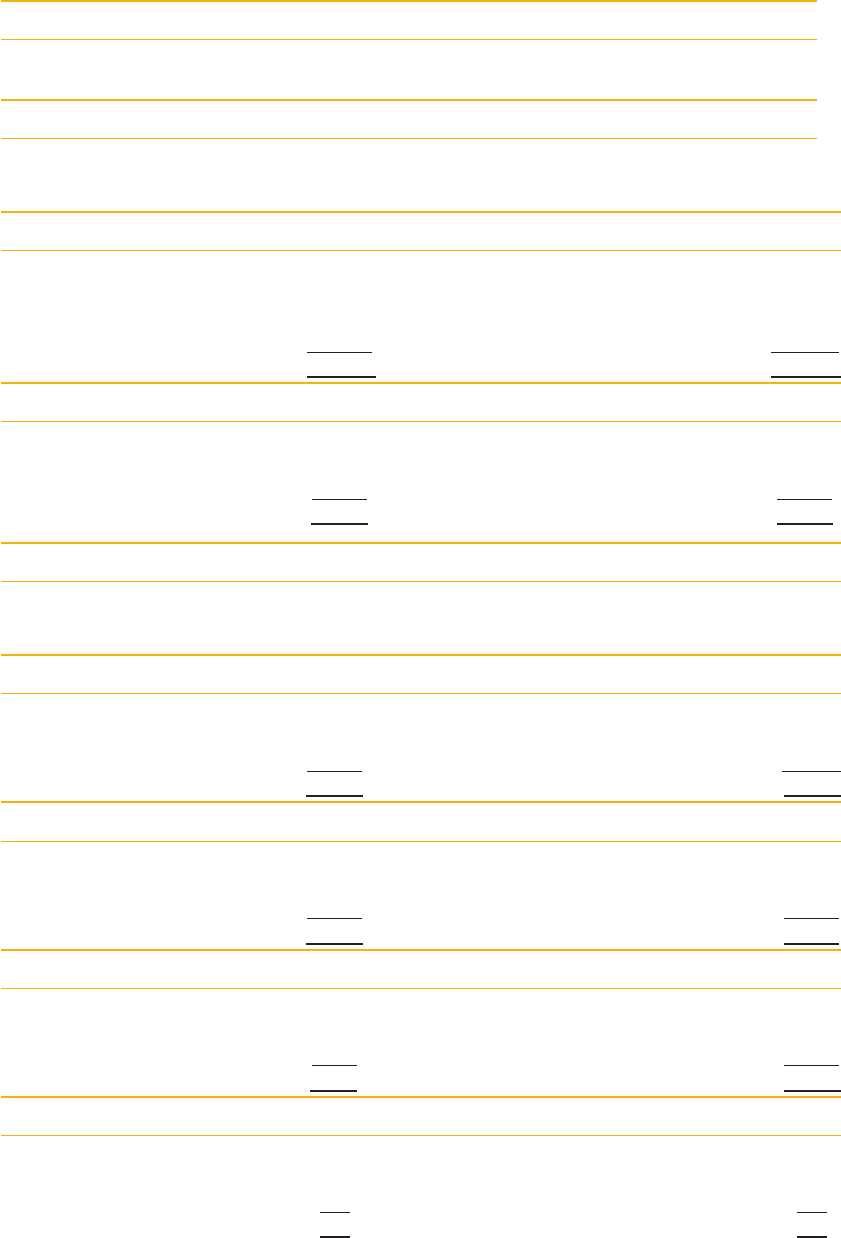

Motor vehicles at cost

$ $

1.10.X5 Balance b/d 10,000 24.04.X6 Disposal 4,000

31.01.X6 Bank

9,000 30.09.X6 Balance c/d 15,000

19,000 19,000

1.10.X6 Balance b/d 15,000 31.08.X7 Disposal 9,000

20.02.X7 Bank 12,000

31.08.X7 Bank 6,600

Disposal 7,400 30.09.X7 Balance c/d 32,000

41,000 41,000

1.10.X7 Balance b/d 32,000

Motor vehicles – accumulated depreciation

$ $

24.04.X6 Disposal [W1] 2,313 1.10.X5 Balance b/d 4,000

30.09.X6 Balance c/d 5,015 30.09.X6 Income statement [W2] 3,328

7,328 7,328

31.08.X7 Disposal [ W3] 2,250 1.10.X6 Balance b/d 5,015

30.09.X7 Balance c/d 10,074 30.09.X7 Income statement [W4] 7,309

12,324 12,324

1.10.X7 Balance b/d 10,074

Workings

$

Wl Year ended 30 September 20X3 ($4,000 @ 25%) 1,000

Year ended 30 September 20X4 ($3,000 @ 25%) 750

Year ended 30 September 20X5 ($2,250 @ 25%) 563

2,313

W2 ($15,000–($4,000–2,313)) @ 25% 3,328

W3 Year ended 30 September 20X6 ($9,000 @ 25%) 2,250

W4 ($32,000–($5015–2,250)) @ 25% 7,309

ACCOUNTING FOR NON-CURRENT ASSETS

181

FUNDAMENTALS OF FINANCIAL ACCOUNTING

Motor vehicles – disposal

$ $

24.04.X6 Motor vehicles cost 4,000 24.04.X6 Motor vehicles – acc. dep’n Bank 2,313

500

30.09.X6 Income statement 1,187

4,000 4,000

31.08.X7 Motor vehicle cost 9,000 1.08.X7 Motor vehicle – acc. dep’n 2,250

30.09.X7 Income statement 650 Motor vehicle cost 7,400

9,650 9,650

Solution 3

●

Identify the revenue items – for example tax and insurance – and exclude from the non-

current asset accounts.

●

A full year’s depreciation is to be charged on all assets in possession at the end of the

year.

(a)

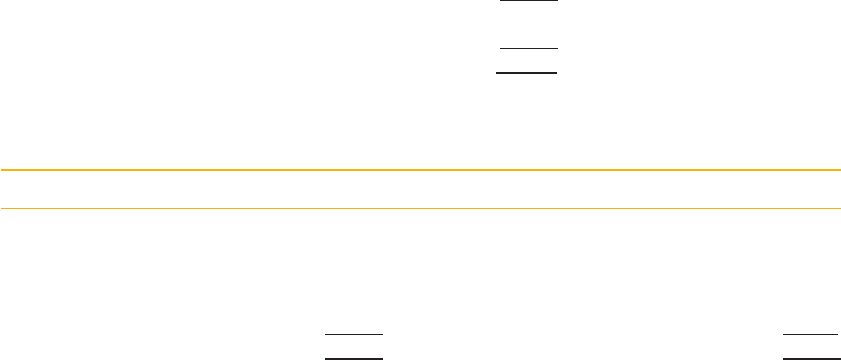

Motor vehicles at cost

$ $

1 Jan. Balance b/d 15,000 31 Jul. Disposal 9,000

1 Aug. Bank

9,500 31 Dec. Balance c/d 15,500

24,500 24,500

1 Jan. Balance b/d 15,500

Motor vehicles expenses

$ $

1 Aug. Bank 500 31 Dec. Income statement 156

Balance c/f 344

500 500

Plant and equipment at cost

$ $

1 Jan. Balance b/d 24,000 1 Apr. Disposal 5,600

1 Feb. Bank 7,500

14 Mar. Bank 11,500

1 Oct. Bank 5,000 31 Dec. Balance c/d 42,000

48,000 48,000

1 Jan. Balance b/d 42,400

Repairs and maintenance

$ $

1 Oct. Bank 10,000 31 Dec. Income statement 10,000

Motor vehicles – accumulated depreciation

$ $

31 Jul. Disposal 5,203 1 Jan. Balance b/d 9,000

31 Dec. Balance c/d 6,723 31 Dec. Income statement 2,926

11,926 11,926

1 Jan. Balance b/d 6,723

ACCOUNTING FOR NON-CURRENT ASSETS

SOLUTIONS TO REVISION QUESTIONS C2

182

Plant and equipment – accumulated depreciation

$ $

1 Apr. Disposal 4,480 1 Jan. Balance b/d 10,500

31 Dec. Balance c/d 14,500 31 Dec. Income statement 8,480

18,980 18,980

1 Jan. Balance b/d 14,500

Plant and equipment – disposal

$ $

1 Apr. Plant and

equipment at

cost

5,600 1 Apr. Plant and

equipment

accumulated

depreciation

4,480

31 Dec. Income

statement

880 1 Apr. Bank 2,000

6,480 6,480

Motor vehicles – disposal

$ $

31 Jul. Motor

vehicles at

cost

9,000 31 Jul. Motor vehicles

accumulated

depreciation

5,203

31 Jul. Bank 3,400

31 Dec. Income statement 397

9,000 9,000

(b) Income statement extract – year ended December 20X5

$

Depreciation charge for the year 11,406

Net profi t on disposal of assets (483)

Equipment repairs 10,000

Annual vehicle licence tax 100

Vehicle warranty (5 / 36×$400) 56

Solution 4

●

Set aside a separate page for workings, and label them clearly.

●

Remember to deduct the discount on the motor vehicle before calculating the amount of

sales tax to be added; remember also that the annual vehicle licence tax and insurance are

revenue expenses, and should not be included with the cost of the vehicle. The resulting

total needs to be added to the non-current asset register, not to the ledger accounts.

●

Deduct the cost and depreciation of the disposed plant from the ledger.

●

Calculate the value of offi ce equipment purchased by comparing the ledger total with

the non-current asset register total.

●

In Part (b), note that the motor vehicle is depreciated on an actual time basis.

ACCOUNTING FOR NON-CURRENT ASSETS

183

FUNDAMENTALS OF FINANCIAL ACCOUNTING

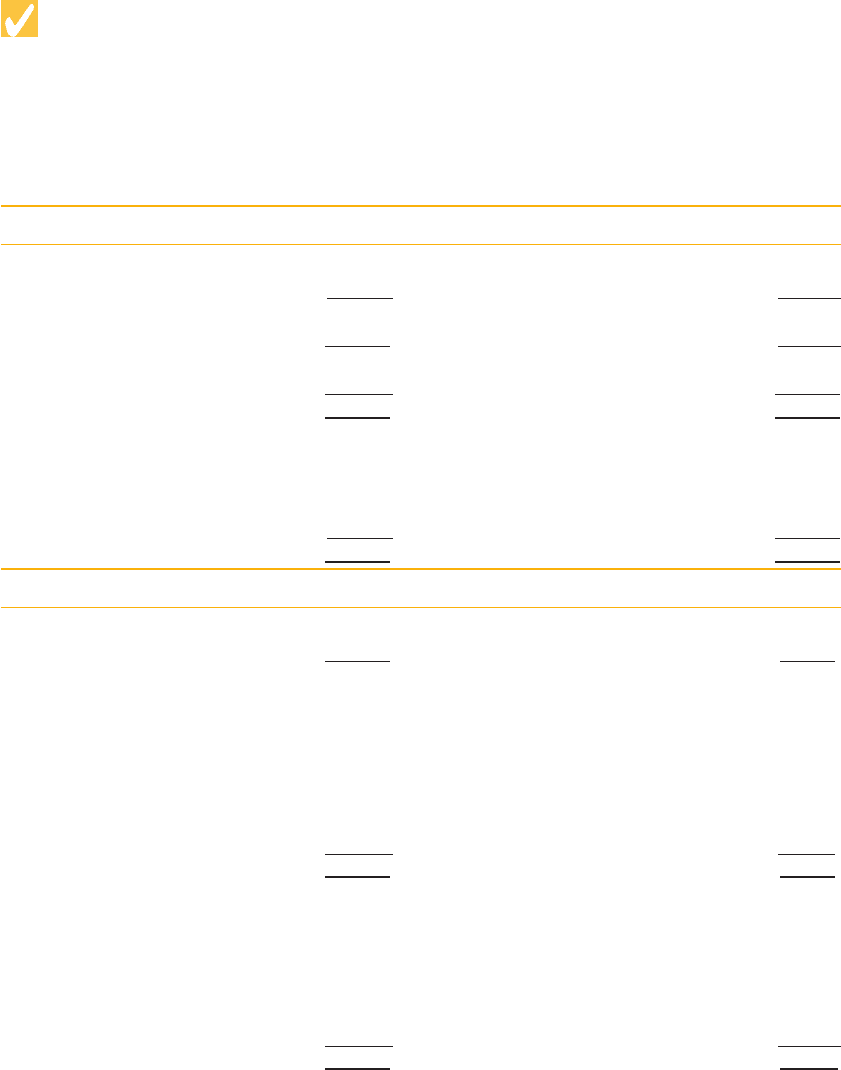

(a)

Motor vehicles

$

List price 24,000

Less : 20% (4,800)

19,200

Add : sales tax 17.5% 3,360

22,560

Add : Cost of painting name 100

Amount to add to non-current asset register 22,660

Plant and machinery Cost ($) Acc. dep’n ($)

Balance as per nominal ledger 120,000 30,000

Less : Disposal (30,000) (5,700)* (*i.e. ($30,000–$24,300))

90,000 24,300

Offi ce equipment

Revised nominal ledger balances Cost ($) Acc. dep’n ($) Carrying amount ($)

Motor vehicles 48,000 (12,000) 36,000

Plant and machinery 90,000 (24,300) 65,700

Offi ce equipment 27,500 (7,500) 20,000

165,500 (43,800) 121,700

Revised non-current asset register ($147,500 $22,660) 170,160

Therefore purchase of offi ce equipment was 48,460

(b) Depreciation for 20X4

Motor vehicles

25% $48,000 12,000

25% $22,660 3/12 1,416 (rounded)

13,416

Plant and machinery

10% $90,000 9,000

Offi ce equipment

10% $68,460 6,846

Solution 5

●

Remember to deduct the sales tax that is included in the price of machine F, as well as

the cost of the maintenance agreement (which is a revenue expense).

ACCOUNTING FOR NON-CURRENT ASSETS

SOLUTIONS TO REVISION QUESTIONS C2

184

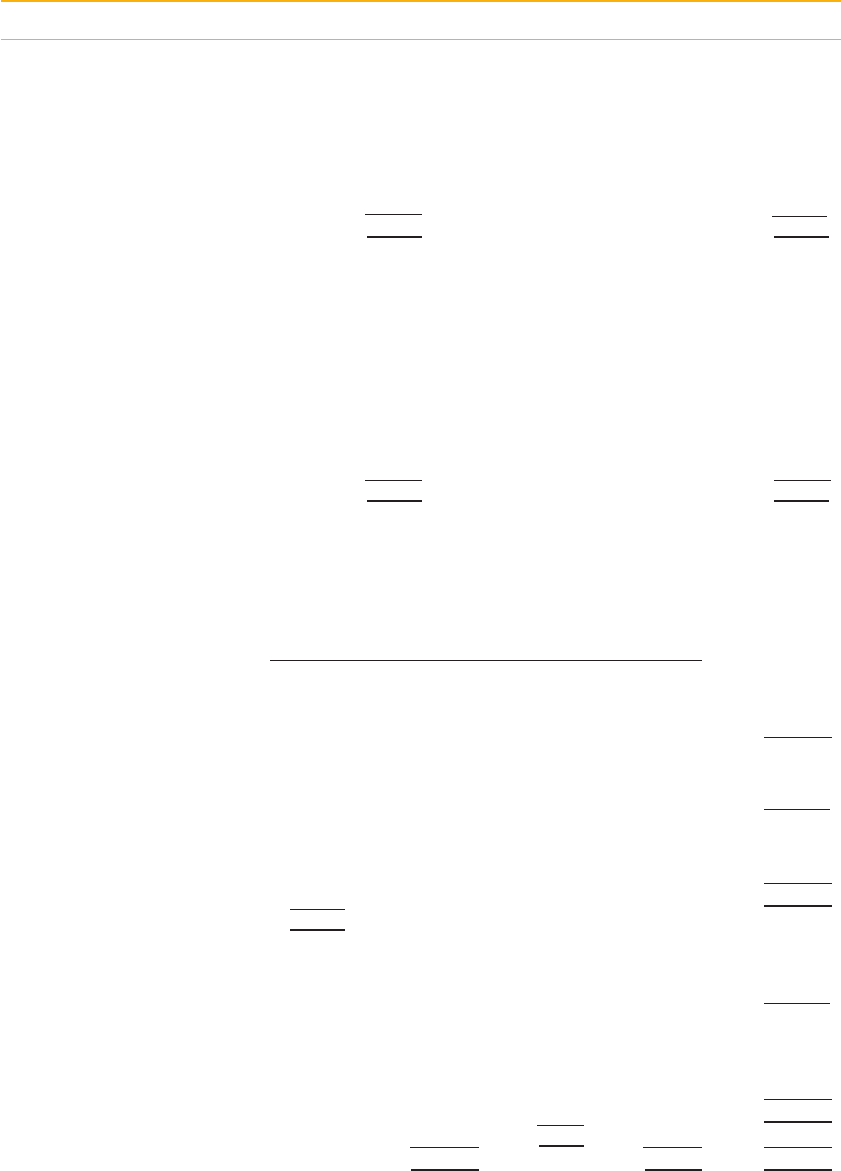

(a) Ledger Accounts

Land at cost

$

1/4/X7 Balance b/fwd 120,000

Buildings at cost

$

1/4/X7 Balance b/fwd 80,000

Plant at cost

$ $

1/4/X7 Balance b/fwd 144,000 Disposal a/c 26,000

Bank a/c 17,000 31/3/X8 Balance c/fwd 169,000

Bank a/c 34,000

195,000 195,000

Offi ce equipment at cost

$ $

1/4/X7 Balance b/fwd 21,600 31/3/X8 Adjustment 400

Bank 2,000 Balance c/fwd 23,200

23,600 23,600

Small tools at cost

$

1/4/X7 Balance b/fwd 1,200

Buildings – accumulated depreciation

$ $

1/4/X7 Balance c/fwd 18,000

31/3/X8 Balance c/fwd 20,000 31/3/X8 Income statement 2,000

20,000 20,000

Plant – accumulated depreciation

$ $

31/3/X8 Disposal a/c 11,700 1/4/X7 Balance b/fwd 76,200

Balance c/fwd 77,175 Income statement 12,675

88,875 88,875

Offi ce equipment – accumulated depreciation

$ $

31/3/X8 Adjustment 200 1/4/X7 Balance b/fwd 8,050

Balance c/fwd 9,590 31/3/X8 Income statement 1,740

9,790 9,790

Small tools – accumulated depreciation

$ $

1/4/X7 Balance b/fwd 300

31/3/98 Balance c/d 400 31/3/X8 Income statement 100

400 400

ACCOUNTING FOR NON-CURRENT ASSETS

185

FUNDAMENTALS OF FINANCIAL ACCOUNTING

Workings

Machine F $

Total cost 42,300

Inc. sales tax

(6,300)

Exc. sales tax 36,000

Less : maintenance (2,000)

Plant a/c 34,000

(b)

Disposal of non-current assets

$ $

31/3/X7 Plant at cost a/c 26,000 31/3/X7 Plant accumulated

depreciation a/c

11,700

A Jones 13,000

Loss on disposal

1,300

26,000 26,000

The offi ce equipment at cost and accumulated depreciation accounts could commence

with the balances after adjusting for the disposed printer, that is, $21,200 (offi ce equip-

ment at cost) and $7,850 (offi ce equipment accumulated depreciation).

(c) A non-current asset register should normally include:

1. a description of the asset;

2. the location of the asset;

3. the original cost of the asset;

4. the date of acquisition;

5. the purchase order reference;

6. the supplier’s name and address;

7. the estimated life of the asset;

8. the estimated residual value of the asset;

9. the rate and method of depreciation to be used;

10. the accumulative depreciation charged to date;

11. maintenance agreements and history;

12. insurance details.

ACCOUNTING FOR NON-CURRENT ASSETS

SOLUTIONS TO REVISION QUESTIONS C2

186

Solution 6

(a) Depreciation is the systematic allocation of the cost of an asset, less its residual value,

over its useful life.

(b) The purpose of depreciation is to allocate the cost of a non-current asset over its useful

life and thus match the cost of an asset in a period with the benefi t from its use. It is

an example of the application of the accruals concept.

Motor vehicles at cost

20X7 $ 20X7 $

Jan. Bank – Truck A 80,000 Dec. Balance c/d 80,000

20X8 20X8

Jan. Balance b/d 80,000 Mar. Disposal a/c – Truck A 80,000

Apr. Bank – Truck B 90,000

July Bank – Car C 20,000 Dec. Balance c/d 110,000

110,000 110,000

20X9 20X9

Jan. Balance b/d 110,000 Aug. Disposal a/c – Car C 20,000

Aug. Disposal a/c – Car C

part-exchange Car D

15,000

Bank – Car D 10,000 Dec. Balance c/d 115,000

135,000 135,000

Accumulated depreciation on motor vehicles

20X7 $ 20X7 $

Dec. Balance c/d 32,000 Dec. Depreciation charge –

Income statement

32,000

20X8 20X8

Mar. Disposal a/c – Truck A 35,200 Jan. Balance b/d 32,000

Mar. Depreciation charge

Truck A – Income

statement

3,200

Dec. Balance c/d 29,250 Dec. Depreciation charge –

Income statement

29,250

64,450 64,450

20X9 20X9

Jan. Balance b/d 29,250

Aug. Disposal a/c – Car C 4,875 Aug. Depreciation charge

Car C – Income

statement

2,625

Dec. Balance c/d 54,544 Dec. Depreciation charge –

Income statement

27,544

59,419 59,419

ACCOUNTING FOR NON-CURRENT ASSETS

187

FUNDAMENTALS OF FINANCIAL ACCOUNTING

Disposal of motor vehicles

20X8 $ 20X8 $

Mar. Vehicle cost a/c – Truck A 80,000 Mar. Accumulated

depreciation on

vehicle a/c –

Truck A

35,200

Dec. Income statement 15,200 Mar. Bank – proceeds

from Truck A

60,000

95,200 95,200

20X9 20X9

Aug. Vehicle cost

account – Car C

20,000 Aug. Accumulated

depreciation on

vehicle a/c –

Car C

4,875

Aug. Vehicle cost

account – Car C

part-exchange

Car D

15,000

Dec. Income statement 125

20,000 20,000

Workings: Depreciation

Year acquired Truckz A Truck B Car C Car D Total ($)

20X7 20X8 20X8 20X9

($)

80,000

($)

90,000

($)

20,000

($)

25,000

Depreciation charge 20X7

$80,000 40% (32,000) (32,000)

Depreciation charge 20X8

($80,000 $32,000)

40% 2/12

(3,200) (3,200)

$90,000 40% 9/12 (27,000) (27,000)

$20,000 90%

25% 6/12

(2,250) (2,250)

(29,250)

Written back on disposal 35,200

Depreciation charge 20X9

$20,000 90% 25%

7/12

(2,625) (2,625)

($90,000 $27,000)

40%

(25,200) (25,200)

$25,000 90% 25%

5/12

(2,344) (2,344)

(27,544)

Written back on disposal 4,875

Balance c/d (52,200) (2,344) (54,544)

This page intentionally left blank

7

Preparation of Financial

Statements with Adjustments