CIMA CO2 Official Learning System - Fundamentals of Financial Accounting

Подождите немного. Документ загружается.

ACCOUNTING FOR NON-CURRENT ASSETS

REVISION QUESTIONS C2

170

Question 5

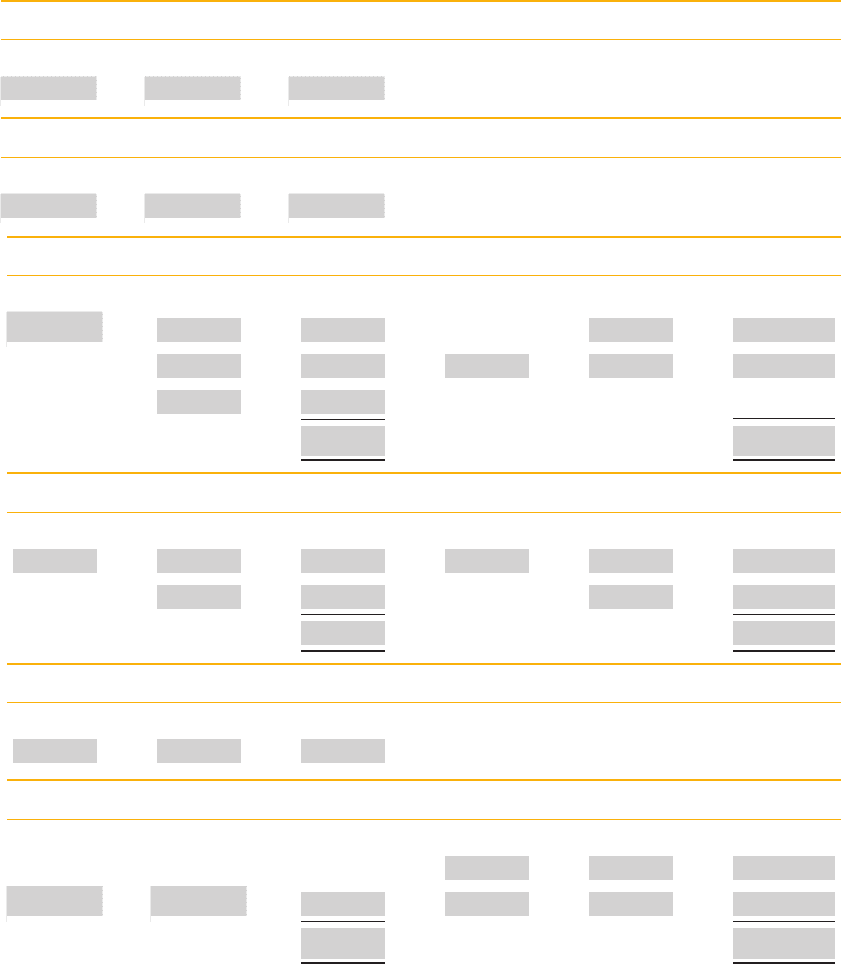

Your organisation maintains a non-current asset register that contained the following

details at 1 April 20X7:

Cost at 1 April 20X7 ($)

Accumulated depreciation at 1

April 20X7 ($)

Land 120,000 Nil

Buildings 80,000 18,000

Plant

Machine A 60,000 27,000

Machine B 40,000 24,000

Machine C 26,000 11,700

Machine D 18,000 13,500

Offi ce equipment

Computer 20,000 7,200

Scanner 1,000 600

Printers (2) 600 250

Small tools 1,200 300

Buildings are depreciated at 2.5 per cent per annum on cost. The cost of small tools is esti-

mated annually, the value at 31 March 20X8 being $800. Plant is depreciated at 7.5 per cent

per annum on cost, and offi ce equipment is depreciated at 7.5 per cent per annum on cost.

During the year ended 31 March 20X8, the following transactions occurred:

(i) Machine E was purchased by cheque for $17,000.

(ii) Machine C was sold for $13,000 to A Jones, on credit.

(iii) The computer memory was upgraded by the manufacturer at a cost of $2,000.

(iv) The scanner was repaired at a cost of $300.

(v) Machine F was purchased by cheque for $42,300 including sales tax at 17.5 per

cent. The purchase price included delivery and installation of $1,200 plus sales tax,

and a 1-year maintenance contract of $2,000 plus sales tax.

(vi) The total on the non-current asset register at 1 April 20X7 was compared with the

ledger accounts, and it was discovered that one of the printers had been passed to a

supplier in part-payment of his debt during December 20X6, but had never been

removed from the non-current asset register. The cost of the printer was $400 and

depreciation of $200 had been charged up to 1 April 20X6.

Notes :

1. Ignore sales tax on all items except for those in transaction (v).

2. The organisation’s policy is to charge a full year’s depreciation in the year of purchase.

ACCOUNTING FOR NON-CURRENT ASSETS

171

FUNDAMENTALS OF FINANCIAL ACCOUNTING

Requirements

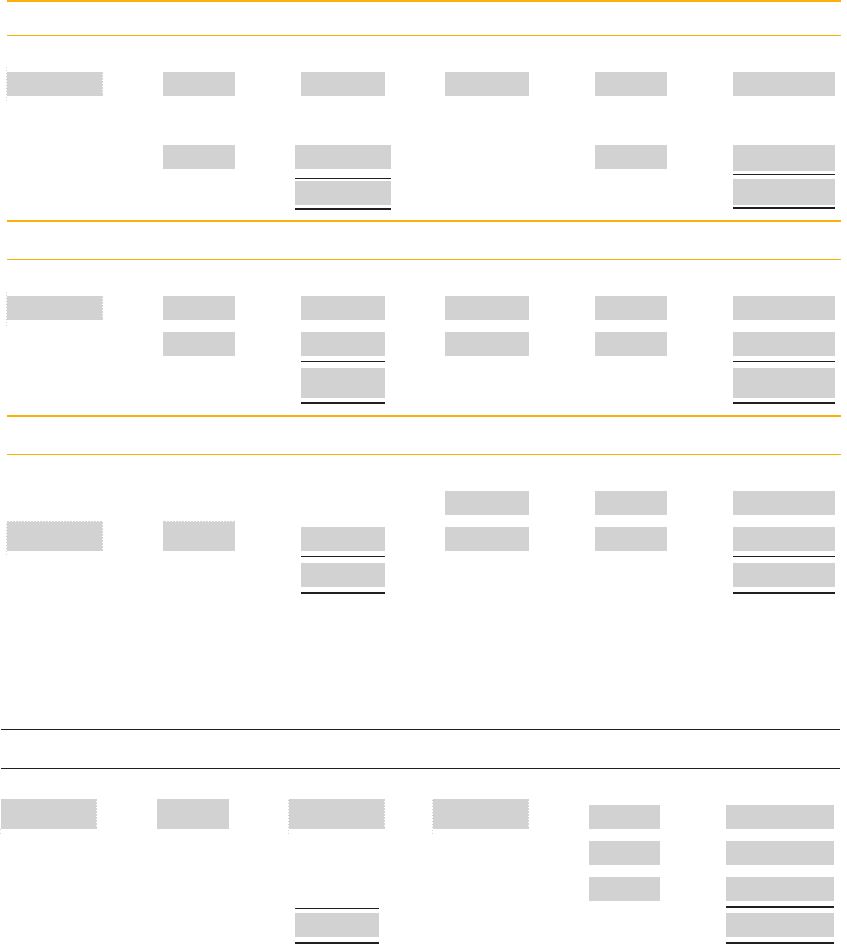

(a) Insert the fi gures in the non-current asset accounts (at cost) and the accumulated

depreciation accounts for each of the above categories of non-current asset, commenc-

ing with the totals in the non-current asset register on 1 April 20X7. Make entries for

additions, disposals, adjustments and depreciation for the year ended 31 March 20X8.

Ledger Accounts

Land at cost

$

Buildings at cost

$

Plant at cost

$ $

Offi ce equipment at cost

$ $

Small tools at cost

$

Buildings accumulated depreciation

$ $

ACCOUNTING FOR NON-CURRENT ASSETS

REVISION QUESTIONS C2

172

Plant accumulated depreciation

$ $

Offi ce equipment accumulated depreciation

$ $

Small tools accumulated depreciation

$ $

(b) Insert the fi gures in the non-current asset disposals account for the year ended 31

March 20X8.

Disposal of non-current assets

$ $

(c) Describe the information that could be held on a non-current asset register.

1. ________________

2. ________________

3. ________________

4. ________________

5. ________________

6. ________________

7. ________________

8. ________________

9. ________________

ACCOUNTING FOR NON-CURRENT ASSETS

173

FUNDAMENTALS OF FINANCIAL ACCOUNTING

10. ________________

11. ________________

12. ________________

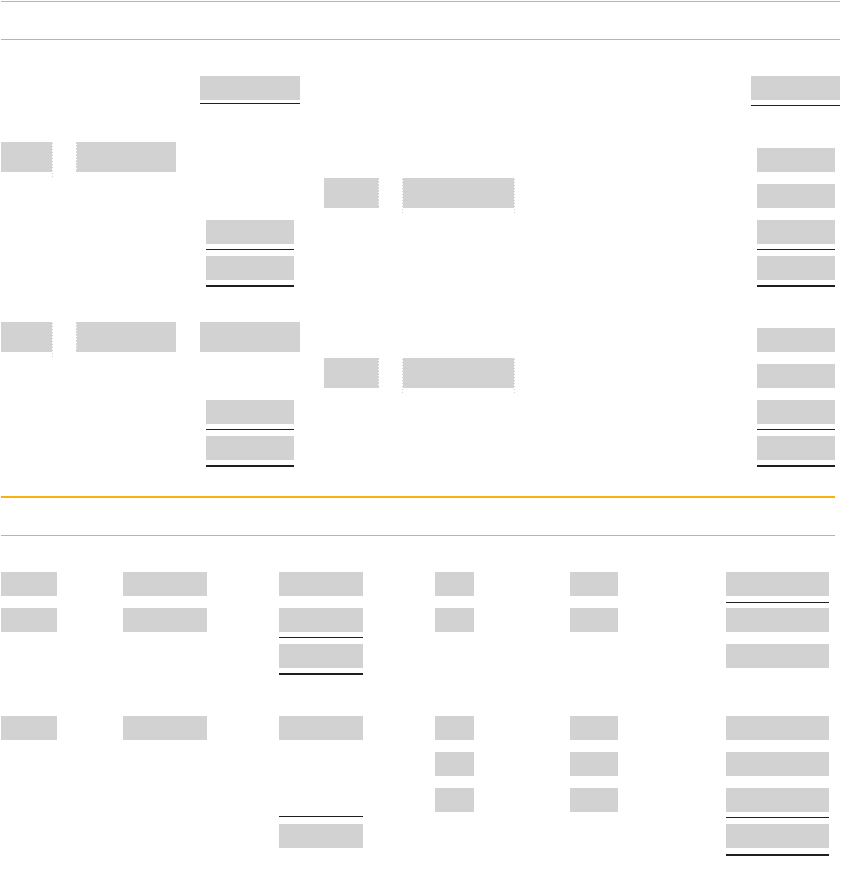

Question 6

(a) Depreciation is the systematic _____ of the cost of an asset, less its _______, over its

________. The purpose of depreciation is to ___ the cost of a non-current asset over

its _________ and thus match the ___ of an asset in a period with the ____________.

It is an example of the application of the ___ convention.

(b) A transport company started business on 1 January 20X7 and purchased truck A for

$80,000. Truck A was destroyed in a road accident on 1 March 20X8 and the insur-

ance company paid out $60,000 to the transport company.

On 1 April 20X8, truck B was purchased for $90,000.

On 1 July 20X8, car C was purchased for $20,000.

On 1 August 20X9, car C was traded in for car D, which cost $25,000, less a part-

exchange allowance on car C of $15,000.

The depreciation policy of the company is:

●

depreciate trucks at 40 per cent each year on a reducing-balance basis;

●

depreciate cars at 25 per cent each year using a straight-line basis;

●

assume a residual value for cars of 10 per cent of the original cost;

●

if a vehicle is owned for part of a year, calculate depreciation according to the number of

months for which the vehicle is owned.

The year end of the company is 31 December.

Including entries for each relevant year, and working to the nearest $, write up the fol-

lowing accounts using the ledger accounts provided.

Motor vehicles at cost

20X7 $ 20X7 $

20X8 20X8

Jan. Balance b/d

Dec. Balance c/d

20X9 20X9

Jan. Balance b/d

Dec. Balance c/d

ACCOUNTING FOR NON-CURRENT ASSETS

REVISION QUESTIONS C2

174

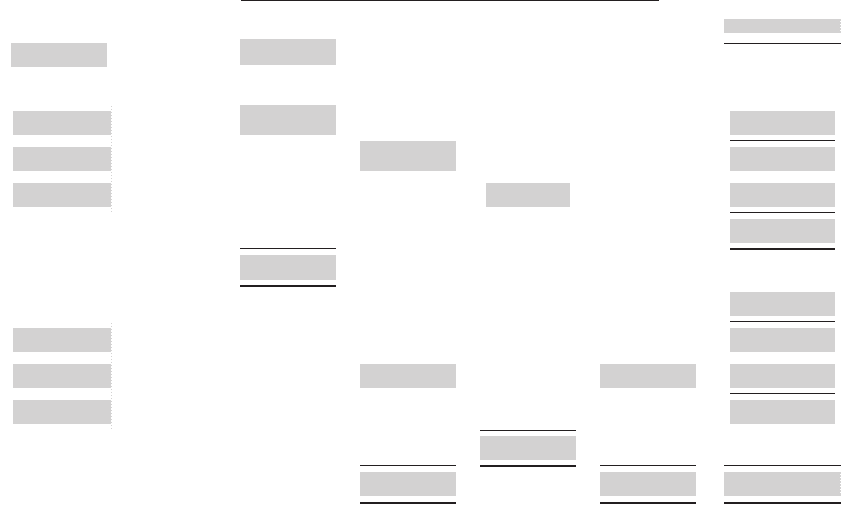

Accumulated depreciation on motor vehicles

20X7 $ 20X7 $

Dec. Balance c/d Dec. Depreciation charge – Income statement

20X8 20X8

Jan. Balance b/d

Dec. Balance c/d

Dec. Depreciation charge – Income statement

20X9 20X9

Jan. Balance b/d

Dec. Balance c/d

Dec. Depreciation charge – Income statement

Disposal of motor vehicles

20X8 $ 20X8 $

20X9 20X9

ACCOUNTING FOR NON-CURRENT ASSETS

175

FUNDAMENTALS OF FINANCIAL ACCOUNTING

Workings: Depreciation

Year acquired Truck A Truck B Car C Car D Total ($)

20X7 20X8 20X8 20X9

($) ($) ($) ($)

80,000 90,000 20,000 25,000

Depreciation charge 20X7

Depreciation charge 20X8

Written back on disposal

Depreciation charge 20X9

Written back on disposal

Balances c/d

This page intentionally left blank

177

Solution 1

1.1 Answer: (D)

The carrying amount of the disposed asset needs to be deducted from the non-

current asset register. The asset was sold for $1,250 less than its carrying amount,

thus its carrying amount must have been $4,000 $1,250 $5,250.

The balance can be calculated as follows:

$

Balance on the register 67,460

Less: carrying amount of the disposed asset (5,250)

62,210

1.2 The profi t or loss on disposal is the difference between the carrying amount at the

time of disposal and the disposal proceeds. An excess of disposal proceeds over car-

rying amount indicates a profi t on disposal, while an excess of carrying amount over

disposal proceeds indicates a loss on disposal.

The annual depreciation on the machine is calculated as:

Cost residual value

Useful life years

5 000 1 000

4

1 000

,,

, per year

Depreciation by 31 December 20X3 would be 3

$1,000 $3,000, therefore the

carrying amount of the machine at the date of disposal would be $2,000. Disposal

proceeds were $1,600, therefore there was a loss on disposal of $400.

1.3 Answer: (A)

The difference between the two records is $10,000, therefore the disposed asset must

have had a carrying amount of this amount. B and D are clearly wrong, and C would

produce a carrying amount of $20,000.

Solutions to Revision

Questions

6

ACCOUNTING FOR NON-CURRENT ASSETS

SOLUTIONS TO REVISION QUESTIONS C2

178

1.4 Answer: (A)

There is insuffi cient information to calculate the proceeds or the length of

ownership.

1.5

$

$9,000 0.7 0.7 0.7 3,087 (carrying amount)

Proceeds of sale (3,000)

Loss on disposal 87

1.6 Answer: (B)

Depreciation never provides a fund for the replacement of the asset, nor does it aim

to show assets at their fair values.

1.7

$

$5,000 0.8 0.8 0.8 2,560 (carrying amount)

Receipt (2,200)

Loss on disposal 360

1.8 Answer: (D)

Depreciation is not connected with the putting aside of money for the replacement

of the asset, nor does it aim to show assets at their fair values. The charging of

depreciation ensures that profi ts are not overstated.

1.9 Answer: (D)

Non-current assets should, except in certain circumstances, be depreciated over

their expected useful life. Answer A would almost never be appropriate. Assets are

rarely valued at their expected selling price – if this is more than their cost, this

would be imprudent, and if less than cost would contravene the ‘ going concern ’

convention, which is discussed in a later chapter. The method of depreciation is

irrelevant.

1.10 Answer: (D)

(A), (B) and (C) are all correct, in most situations.

1.11

$

Cost of machine 80,000

Installation 5,000

Training 2,000

Testing 1,000

88,000

ACCOUNTING FOR NON-CURRENT ASSETS

179

FUNDAMENTALS OF FINANCIAL ACCOUNTING

1.12

$

Cost 10,000

20X0 Depreciation (2,500)

7,500

20X1 Depreciation (1,875)

5,625

20X2 Depreciation (1,406)

4,219

20X3 Part-exchange (5,000)

Profi t 781

1.13

$ $

Carrying amount at 1 August 20X0 200,000

Less : depreciation (20,000)

Proceeds 25,000

Loss 5,000

Therefore carrying amount (30,000)

150,000

1.14 Answer: (D)

1.15

$

Cost 12,000

20X1 Depreciation (2,400)

9,600

20X2 Depreciation (2,400)

7,200

20X3 Depreciation (2,400)

4,800

Proceeds on disposal (5,000)

Profi t 200

1.16 Graph A Reducing-balance method of depreciation. Graph B Straight-line method

of depreciation.

1.17 Answer: (D)