CIMA - C1 Fundamentals of Management Accounting

Подождите немного. Документ загружается.

30

1: Introduction to management accounting and costing ⏐ Part A Cost determination and behaviour

8 Which of the following would be classified as indirect labour?

A Assembly workers in a company manufacturing televisions

B A stores assistant in a factory store

C Plasterers in a construction company

D An audit clerk in a firm of auditors

9 In the composite code 374.152, the last three digits indicate the cost centre to be charged. This is:

A classification by responsibility

B cost classification

C objective classification

D subjective classification

10 The following information is available for product M for the month of December.

Production costs:

Variable $4 per unit

Fixed $6,000

The total production cost of producing 4,000 units of product M in December is $

11 Which of the following options describes the value of a benefit sacrificed when one course of action is chosen in

preference to an alternative?

A Relevant cost

B Differential cost

C Opportunity cost

D Sunk cost

51433 www.ebooks2000.blogspot.com

Part A Cost determination and behaviour ⏐ 1: Introduction to management accounting and costing

31

Answers to Quick Quiz

1 False. Cost accounting is mainly concerned with the preparation of management accounts for internal managers of an

organisation. Financial accounts are prepared for individuals external to an organisation eg shareholders, customers and

so on.

2 (a) Cost unit

(b) Cost centre

(c) Cost object

3 Historical cost

4 A

5 (a) Direct, indirect (overhead) costs

(b) Functional

(c) Variable

6 False. Fixed costs are unaffected by changes in the level of activity.

7 Sales commission Functional cost

Rent Fixed cost

Research and development costs Variable cost

8 B The others are direct labour.

9 C A code which indicates the cost centre to which the costs should be allocated is known as an objective

classification

10 $

Variable costs 4,000 × $4 16,000

Fixed costs

6,000

22,000

11 C Opportunity cost

Now try the questions below from the Question Bank

Question numbers Page

1–5 351

[

]

52433 www.ebooks2000.blogspot.com

32

1: Introduction to management accounting and costing ⏐ Part A Cost determination and behaviour

53433 www.ebooks2000.blogspot.com

33

Cost behaviour

Introduction

with changes in activity level (variable costs) and those that do not (fixed costs). This

chapter examines further this particular two-way split of cost behaviour and explains two

methods of splitting total costs into these two elements, the line of best fit (or scattergraph)

method and the high-low method.

You will need to rely on concepts covered in this chapter in the other chapters in this Study

Text (but particularly the next chapter) and in the remainder of your management accounting

studies both at the Certificate stage and at future examination levels.

Topic list

Learning outcomes

Syllabus references

Ability required

1 Cost behaviour and levels of activity B(i) B(1) Comprehension

2 Cost behaviour patterns B(ii), B(iii) B(1), B(2) Comprehension

3 Determining the fixed and variable elements

of semi-variable costs

B(iv) B(3) Application

In Chapter 1 we introduced the concept of the division of costs into those that vary directly

54433 www.ebooks2000.blogspot.com

34

2: Cost behaviour ⏐ Part A Cost determination and behaviour

1 Cost behaviour and levels of activity

Cost behaviour is the way in which a cost changes as activity level changes.

Cost behaviour is the 'Variability of input costs with activity undertaken. Cost may increase proportionately with

increasing activity (the usual assumption for variable cost), or it may not change with increased activity (a fixed cost).

Some costs (semi-variable) may have both variable and fixed elements. Other behaviour is possible; costs may increase

more or less than in direct proportion, and there may be step changes in cost, for example. To a large extent, cost

behaviour will be dependent on the timescale assumed.' CIMA Official Terminology

1.1 Levels of activity

The level of activity refers to the amount of work done, or the number of events that have occurred. Depending on

circumstances, the level of activity may refer to measures such as the following.

• The volume of production in a period

• The number of items sold

• The number of invoices issued

• The number of units of electricity consumed

1.2 Basic principle of cost behaviour

The basic principle of cost behaviour is that as the level of activity rises, costs will usually rise. It will probably cost

more to produce 2,000 units of output than it will cost to produce 1,000 units; it will usually cost more to make five

telephone calls than to make one call and so on. The problem for the accountant is to determine, for each item of cost,

the way in which costs rise and by how much as the level of activity increases.

For our purposes in this chapter, the level of activity will generally be taken to be the volume of production/output.

2 Cost behaviour patterns

2.1 Fixed costs

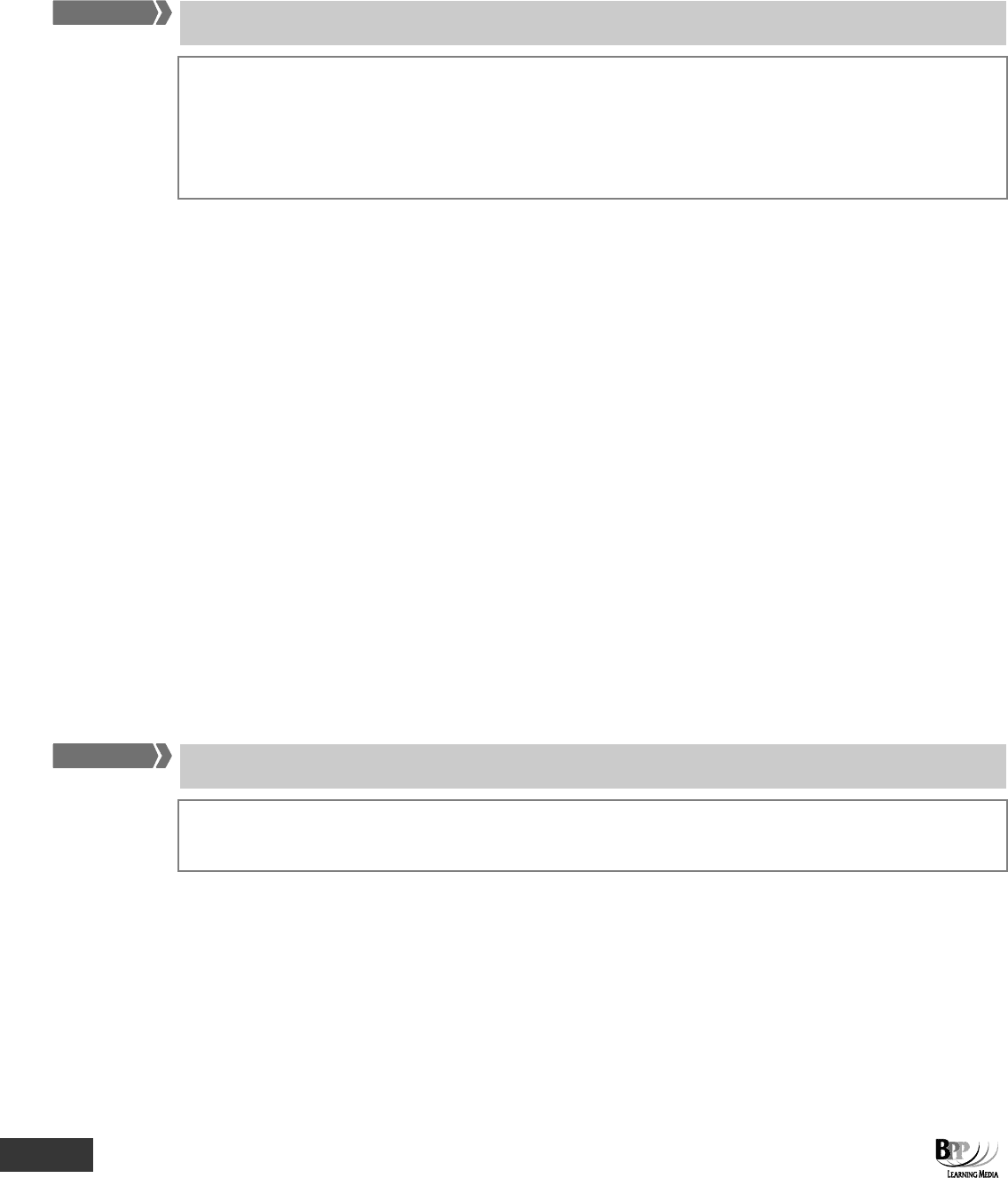

Costs which are not affected by the level of activity are fixed costs or period costs.

A fixed cost is a 'cost incurred for an accounting period, that, within certain output or turnover limits, tends to be

unaffected by fluctuations in the levels of activity (output or turnover)'. CIMA Official Terminology

decreases in the volume of output. Fixed costs are a period charge, in that they relate to a span of time; as the time span

increases, so too will the fixed costs. A sketch graph of a fixed cost would look like this.

FA

S

T F

O

RWAR

D

Key term

FA

S

T F

O

RWAR

D

Key term

We discussed fixed costs briefly in Chapter 1. A fixed cost is a cost which tends to be unaffected by increases or

55433 www.ebooks2000.blogspot.com

Part A Cost determination and behaviour ⏐ 2: Cost behaviour

35

Cost

$

Volume of output (level of activit

y

)

Fixed cost

G

raph of fixed cos

t

2.1.1 Examples of fixed costs

• The salary of the managing director (per month or per annum)

• The rent of a single factory building (per month or per annum)

• Straight line depreciation of a single machine (per month or per annum)

You now know that fixed costs are the same, no matter how many units are produced. Note, however, that as the

number of units increases, the fixed cost per unit actually decreases.

This concept may seem confusing at first and it's best to think in terms of numbers.

20X1 20X2

Fixed cost $50,000 $50,000

Number of units produced 500 1,000 Units have increased

Fixed cost per unit

($50,000/no. of units) $100 $50 Cost per unit has decreased

Even though the costs are fixed, we still sometimes look at the cost per unit. Don't let this confuse you – total fixed costs

are fixed and do not vary with activity levels.

2.2 Variable costs

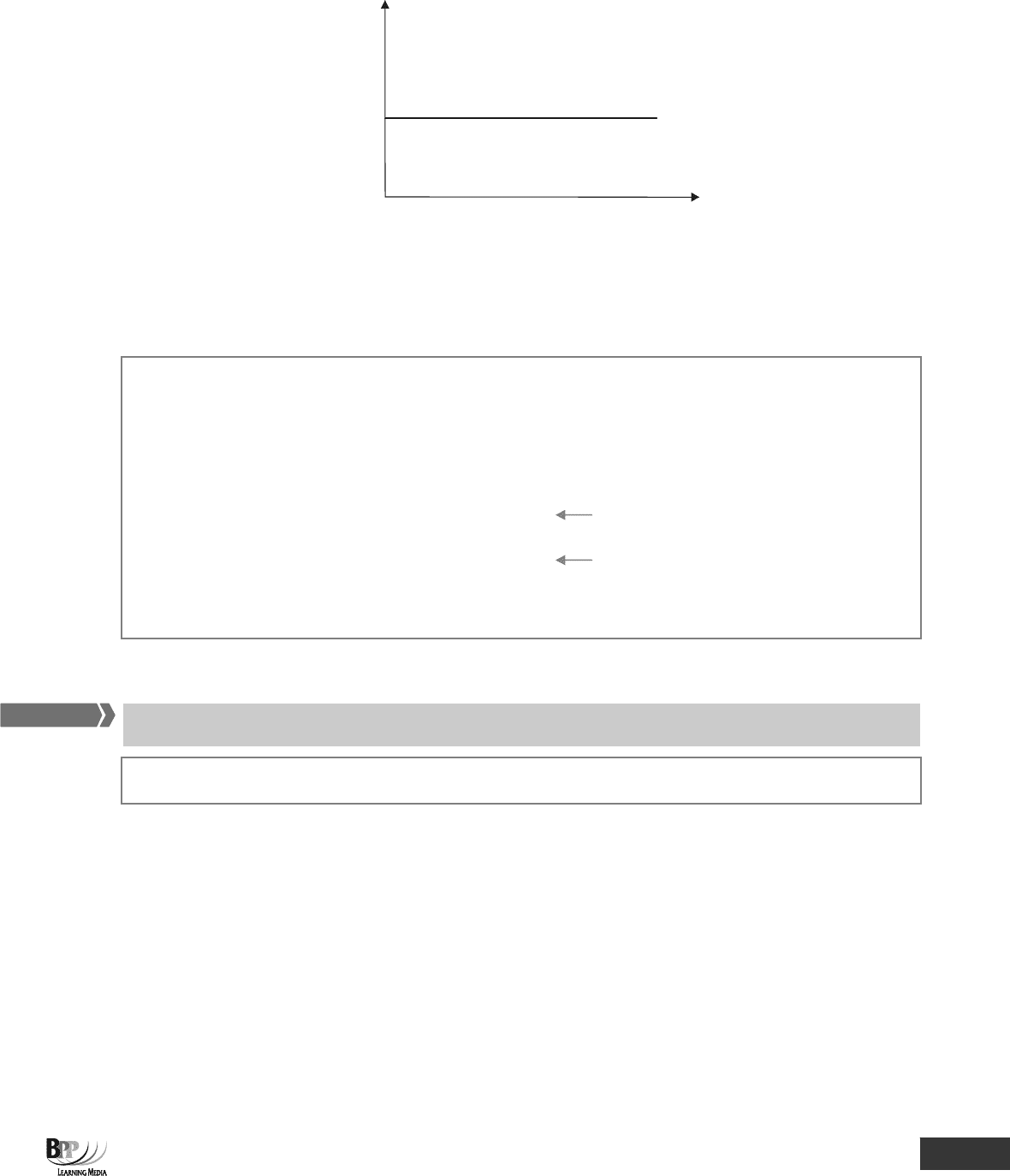

Variable costs increase or decrease with the level of activity.

A variable cost is a 'cost that varies with a measure of activity'. CIMA Official Terminology

We discussed variable costs briefly in Chapter 1. A variable cost is a cost which tends to vary directly with the volume of

output. The variable cost per unit is the same amount for each unit produced whereas total variable cost increases as

volume of output increases. A sketch graph of a variable cost would look like this.

FAST FORWARD

Key term

Assessment

focus point

56433 www.ebooks2000.blogspot.com

36

2: Cost behaviour ⏐ Part A Cost determination and behaviour

Cost

$

Volume of out

p

ut

G

raph of variable cost

2.2.1 Examples of variable costs

(a) The cost of raw materials (where there is no discount for bulk purchasing since bulk purchase discounts reduce

the unit cost of purchases).

(b) Direct labour costs are, for very important reasons which you will study in Chapter 7, usually classed as a variable

cost even though basic wages are often fixed.

(c) Sales commission is variable in relation to the volume or value of sales.

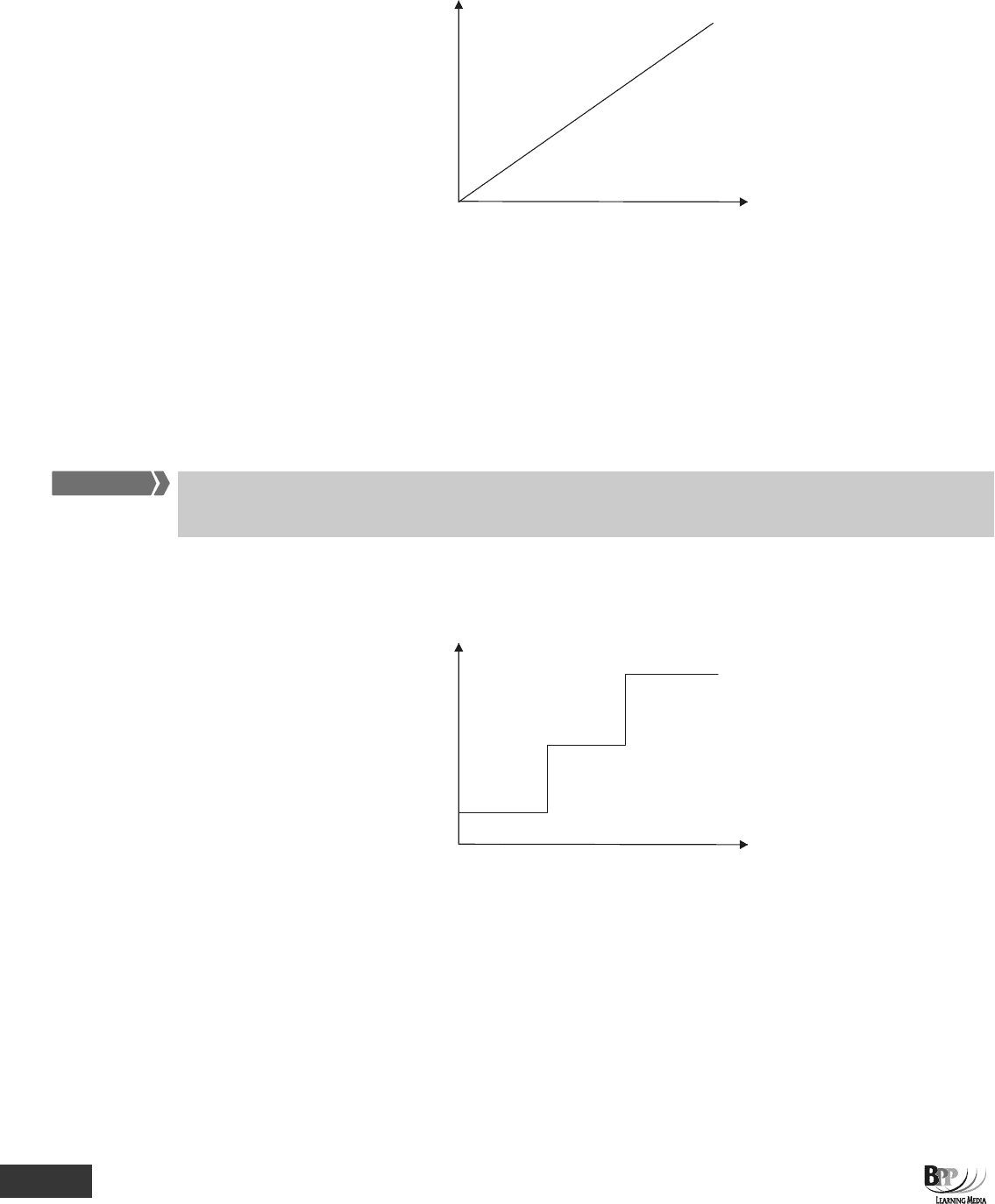

2.3 Step costs

A step cost is a cost which is fixed in nature but only within certain levels of activity. Depending on the time frame being

considered, it may appear as fixed or variable.

Consider the depreciation of a machine which may be fixed if production remains below 1,000 units per month. If

production exceeds 1,000 units, a second machine may be required, and the cost of depreciation (on two machines)

would go up a step. A sketch graph of a step cost could look like this.

Cost

$

Volume of out

p

ut

G

raph of step cost

2.3.1 Examples of step costs

(a) Rent is a step cost in situations where accommodation requirements increase as output levels get higher.

(b) Basic pay of employees is nowadays usually fixed, but as output rises, more employees (direct workers,

supervisors, managers and so on) are required.

FA

S

T F

O

RWAR

D

57433 www.ebooks2000.blogspot.com

Part A Cost determination and behaviour ⏐ 2: Cost behaviour

37

2.3.2 The importance of time scale

The time scale over which we consider the behaviour of what appears to be a step cost can actually result in its

classification as a fixed cost or a variable cost.

Over the short to medium term, a cost such as rent will appear as fixed, steps in the cost only occurring after a certain

length of time.

Many variable costs also appear fixed over a short period of time. For example, spending on direct labour (traditionally

classified as a variable cost) will be fixed in relation to changes in activity level as it takes time to respond to changes in

activity and alter spending levels.

Over longer periods of time, however, say a number of years, all costs will tend to vary in response to large changes

in activity level. For this reason fixed costs are sometimes called long-term variable costs. Costs traditionally classified

as fixed will become step costs as no cost can remain unchanged forever. And so as the time span increases, step

costs become variable costs, varying with the passing of time. For example, when considered over many years, rent

will appear as a variable cost, varying in the long term with large changes in the level of activity.

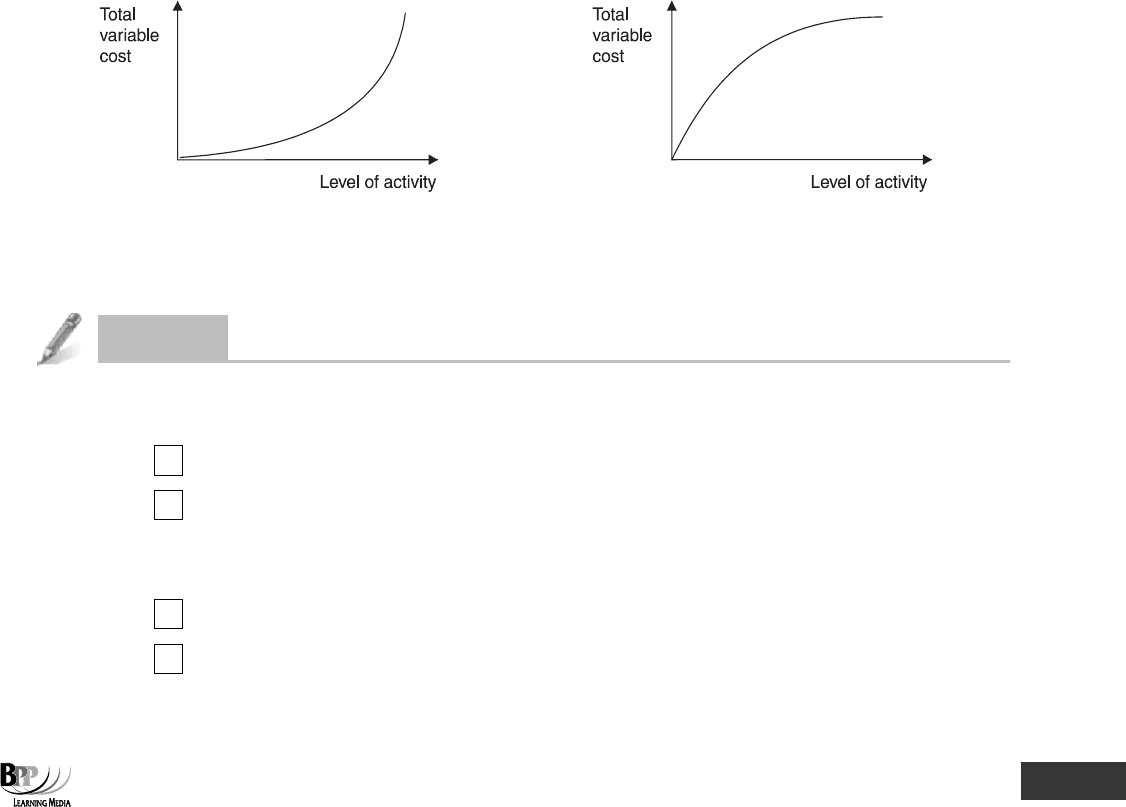

2.4 Non-linear variable costs

Although variable costs are usually assumed to be linear, there are situations where variable costs are curvilinear. Have

a look at the following graphs.

Graph (a) Graph (b)

Graph (a) becomes steeper as levels of activity increase. Each additional unit of activity is adding more to total variable

cost than the previous unit. Graph (b) becomes less steep as levels of activity increase. Each additional unit is adding

less to total variable cost than the previous unit.

Question

Cost behaviour patterns

The cost of direct labour where employees are paid a bonus which increases as output levels increase might follow the

cost behaviour pattern depicted in graph (a) above.

True

False

The cost of direct material where quantity discounts are available might follow the cost behaviour pattern in graph (b)

above.

True

False

58433 www.ebooks2000.blogspot.com

38

2: Cost behaviour ⏐ Part A Cost determination and behaviour

Answer

Graph (a)

9

True

Graph (b)

9

True

2.5 Semi-variable costs (or semi-fixed costs or mixed costs)

Semi-variable, semi-fixed or mixed costs are costs which are part-fixed and part-variable and are therefore partly

affected by a change in the level of activity.

A semi-variable cost is a 'cost containing both fixed and variable components and thus partly affected by a change in

the level of activity'. CIMA Official Terminology

2.5.1 Examples of semi-variable costs

(a) Electricity and gas bills. There is a basic charge plus a charge per unit of consumption.

(b) Sales representative's salary. The sales representative may earn a basic monthly amount of, say, $1,000

and then commission of 10% of the value of sales made.

The behaviour of a semi-variable cost can be presented graphically as follows.

Cost

$

Volume of out

p

ut

Variable part

Fixed part

G

raph of semi-variable cost

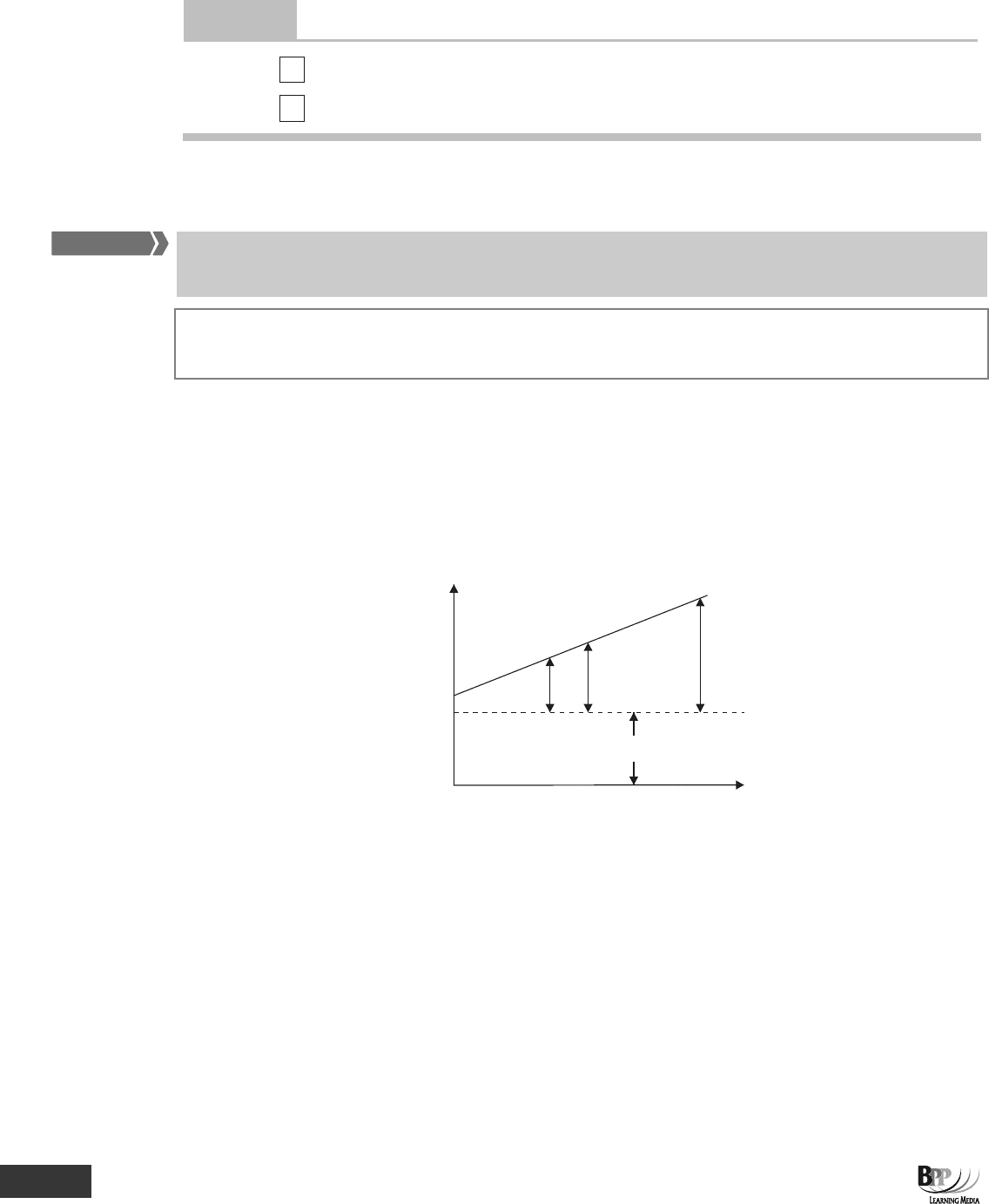

2.6 Cost behaviour and total and unit costs

If the variable cost of producing a unit is $5 per unit then it will remain at that cost per unit no matter how many units

are produced. However if the business's fixed costs are $5,000 then the fixed cost per unit will decrease the more units

are produced: one unit will have fixed costs of $5,000 per unit; if 2,500 are produced the fixed cost per unit will be $2; if

5,000 are produced the fixed cost per unit will be only $1. Thus as the level of activity increases the total costs per unit

(fixed cost plus variable cost) will decrease.

FAST FORWARD

Key term

59433 www.ebooks2000.blogspot.com

Part A Cost determination and behaviour ⏐ 2: Cost behaviour

39

In sketch graph form this may be illustrated as follows.

Cost

per

unit

$

Variable cost

Fixed cost

To t al co s t

Cost

per

unit

$

Cost

per

unit

$

N

u

m

be

r

o

f

u

nit

s

N

u

m

be

r

o

f

u

nit

s

N

u

m

be

r

o

f

u

nit

s

Question

Fixed, variable and mixed costs

Tick the appropriate box for each cost.

Fixed Variable Mixed

(a) Telephone bill

(b) Annual salary of the chief accountant

(c) The management accountant's annual

membership fee to CIMA (paid by the company)

(d) Cost of materials used to pack 20 units of

product X into a box

Answer

(a) Mixed

9

(b) Fixed

9

(c) Fixed

9

(d) Variable

9

2.7 Assumption about cost behaviour

2.7.1 The relevant range

The relevant range is 'activity levels within which assumptions about cost behaviour in breakeven analysis remain valid'.

CIMA Official Terminology

The relevant range also broadly represents the activity levels at which an organisation has had experience of

operating at in the past and for which cost information is available. It can therefore be dangerous to attempt to predict

costs at activity levels which are outside the relevant range.

Key term

60433 www.ebooks2000.blogspot.com