CIMA - C1 Fundamentals of Management Accounting

Подождите немного. Документ загружается.

40

2: Cost behaviour ⏐ Part A Cost determination and behaviour

2.7.2 Assumptions

It is often possible to assume that, within the normal or relevant range of output, costs are either fixed, variable or semi-

variable.

Question

Activity levels

Select the correct words in the following sentence.

The basic principle of cost behaviour is that as the level of activity rises, costs will usually (a) rise/fall/stay the same. In

general, as activity levels rise, the variable cost per unit will (b) rise/fall/stay the same, the fixed cost per unit will (c)

rise/fall/stay the same and the total cost per unit will (d) rise/fall/stay the same.

Answer

(a) Rise

(b) Stay the same

(c) Fall

(d) Fall

Question

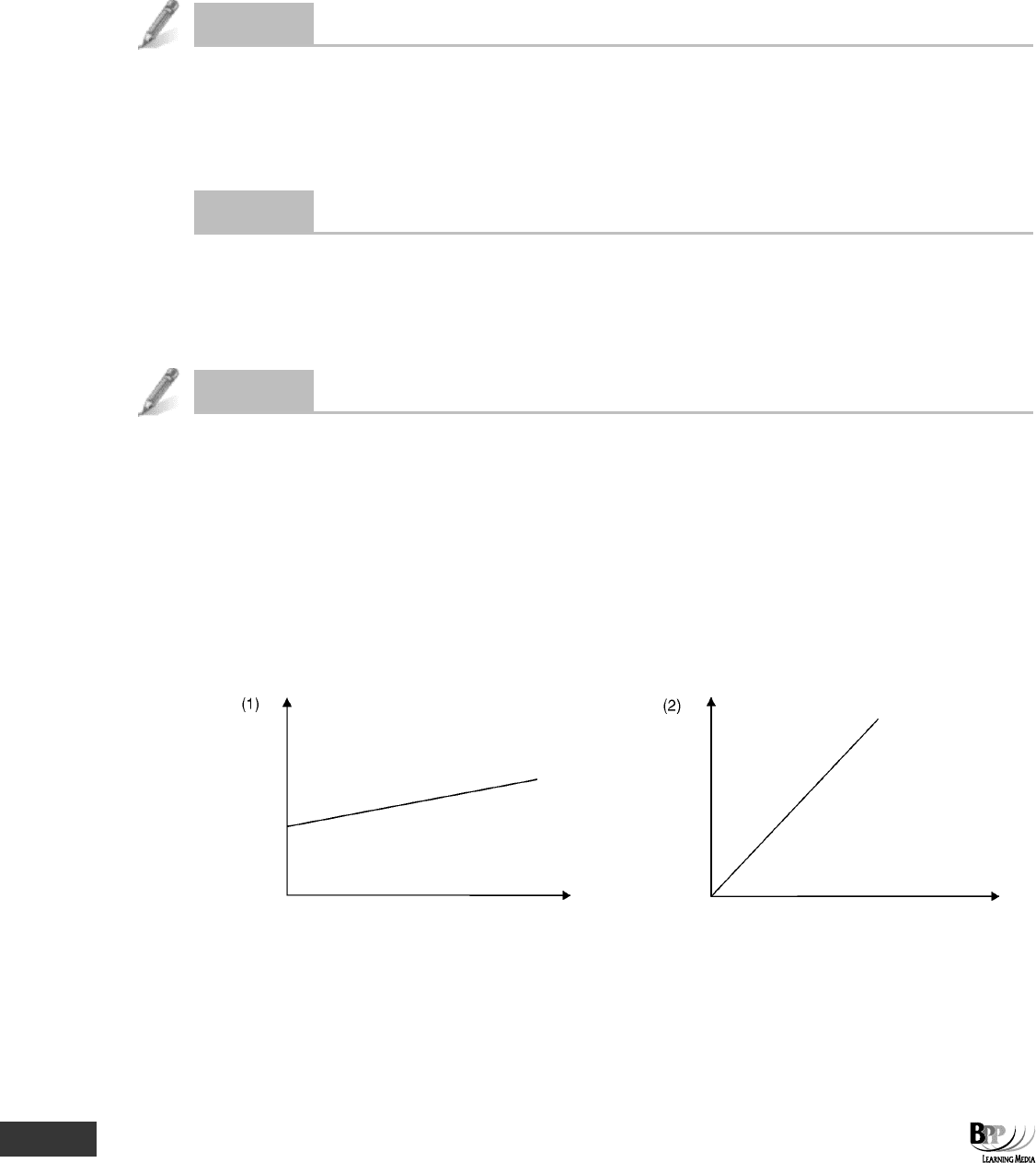

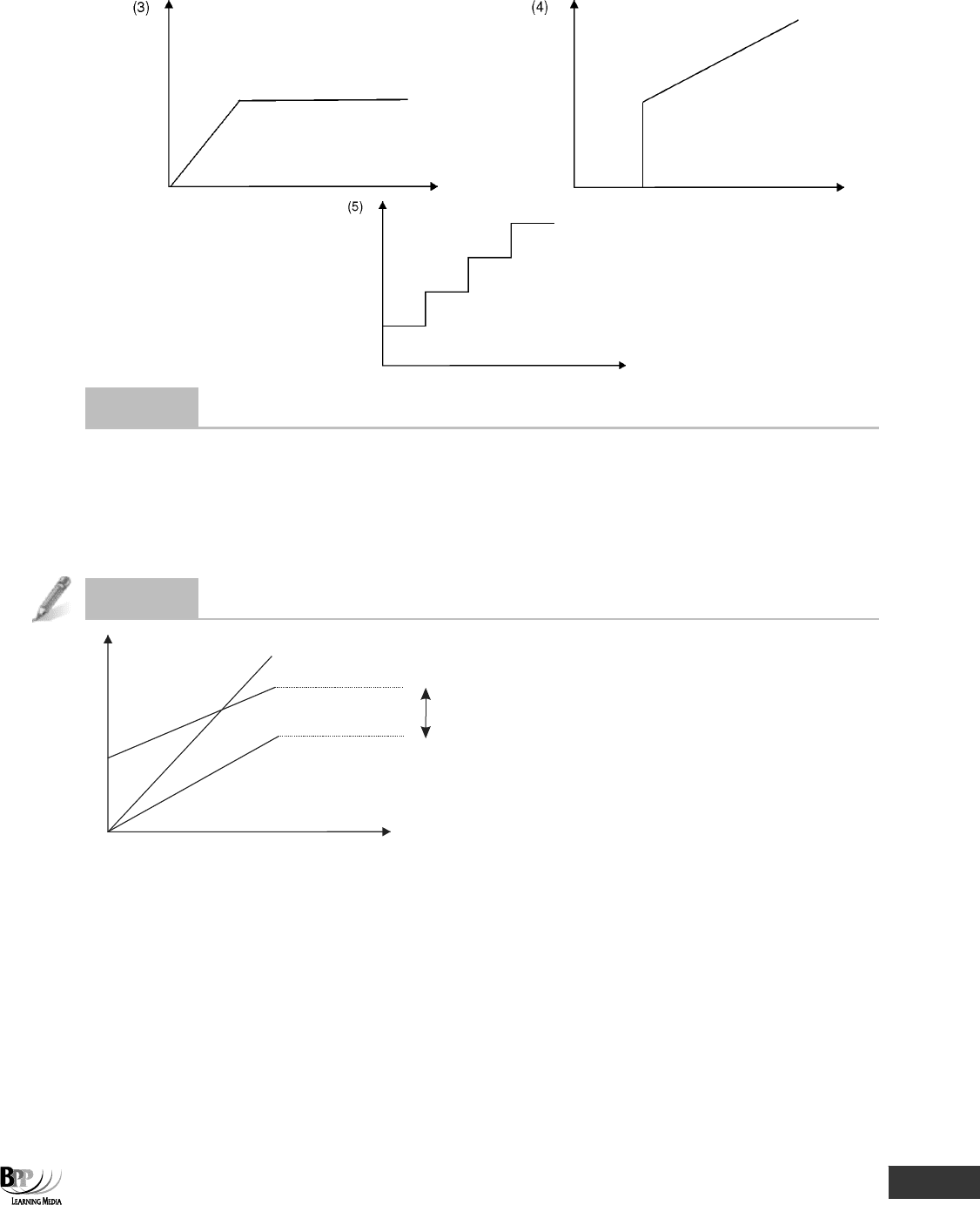

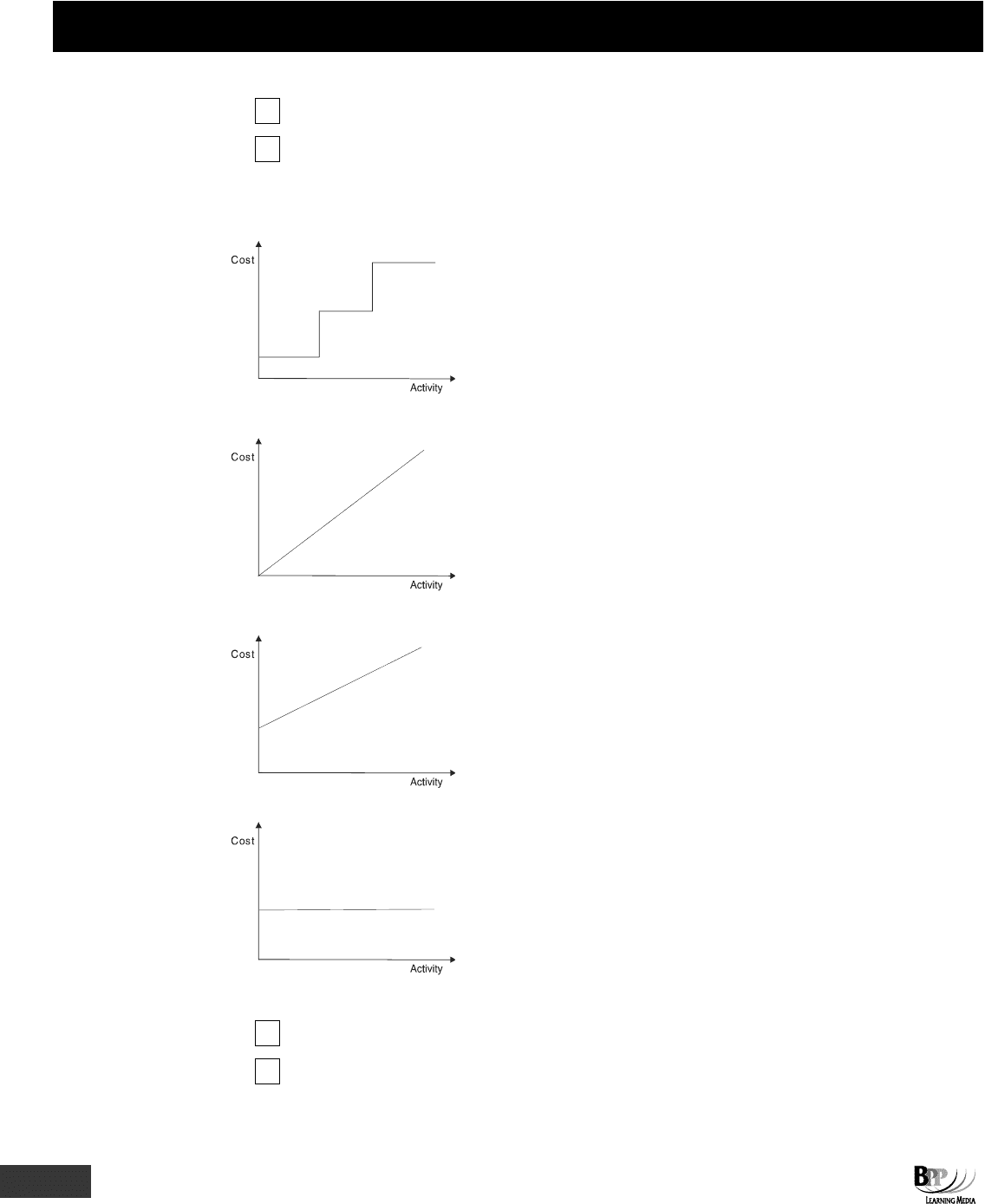

Cost behaviour graphs

Match the sketches (1) to (5) below to the listed items of expense. In each case the vertical axis relates to total cost, the

horizontal axis to activity level.

(a) Electricity bill: a standing charge for each period plus a charge for each unit of electricity consumed.

(b) Supervisory labour.

(c) Production bonus, which is payable when output in a period exceeds 10,000 units. The bonus amounts in total to

$20,000 plus $50 per unit for additional output above 10,000 units.

(d) Sales commission, which amounts to 2% of sales revenue.

(e) Machine rental costs of a single item of equipment. The rental agreement is that $10 should be paid for every

machine hour worked each month, subject to a maximum monthly charge of $480.

61433 www.ebooks2000.blogspot.com

Part A Cost determination and behaviour ⏐ 2: Cost behaviour

41

Answer

(a) Graph (1)

(b) Graph (5)

(c) Graph (4)

(d) Graph (2)

(e) Graph (3)

Question

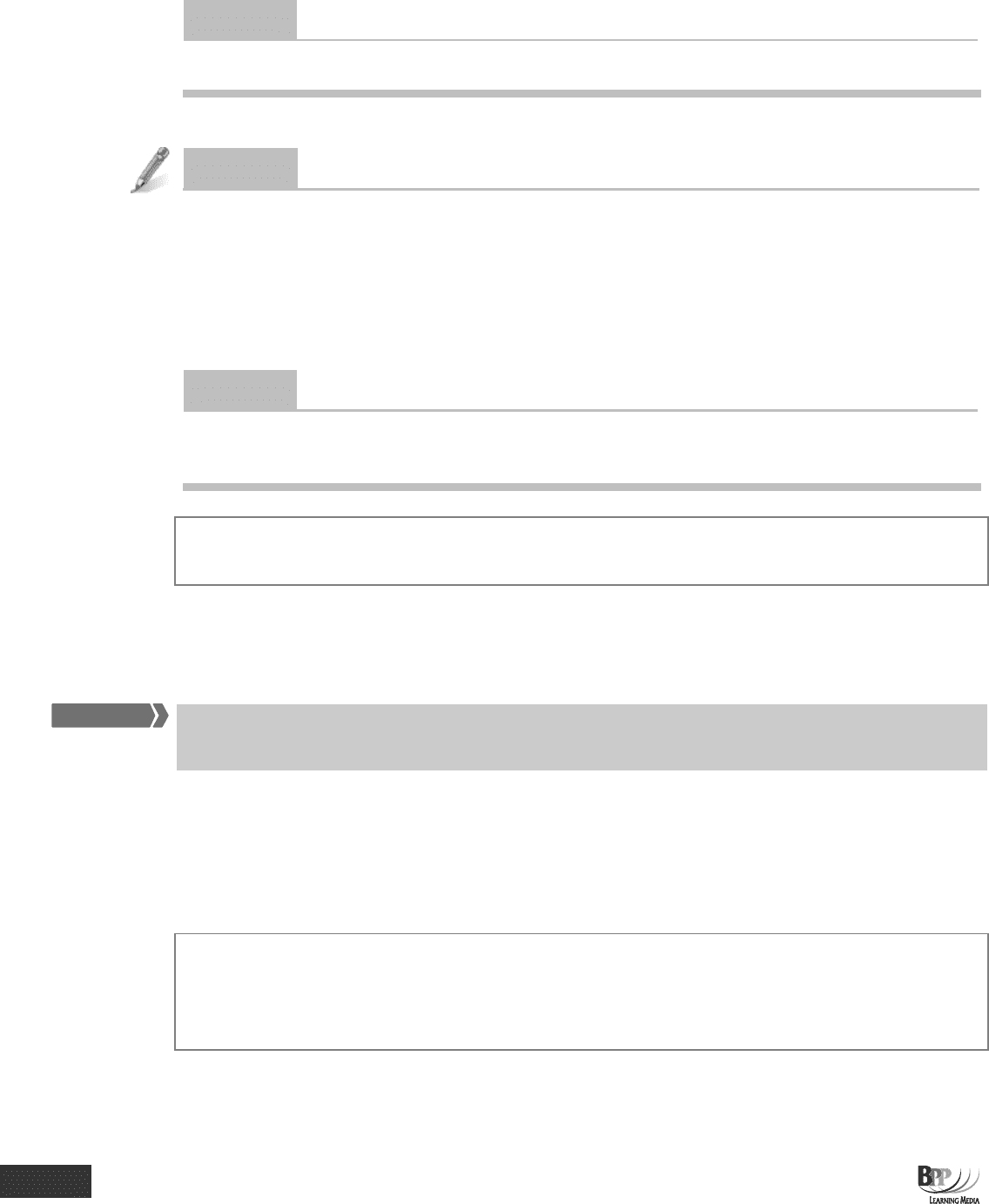

Behaviour graph

$

Units

Variable cost

Sales revenue

Total cost

In the above graph, what does the arrow represent?

A Fixed cost

B Contribution

C Profit

D Breakeven quantity in units

62433 www.ebooks2000.blogspot.com

42

2: Cost behaviour ⏐ Part A Cost determination and behaviour

Answer

A Total cost = Variable cost + Fixed cost

Question

Cost type

The staff at Underworld Co are paid a basic minimum wage plus an amount per item of inventory produced. What type of

cost are the staff wages?

A Fixed

B Variable

C Semi-variable

D Step

Answer

C Semi-variable. The basic minimum wage is the fixed element and the extra amount per item of inventory is the

variable element.

You may see graphical questions in your assessment. Always read the labels on the axes carefully before deciding what

the graph represents.

3 Determining the fixed and variable elements of semi-variable

costs

The fixed and variable elements of semi-variable costs can be determined by the high/low method or the 'line of best fit'

(scattergraph) method.

There are several ways in which fixed cost elements and variable cost elements within semi-variable costs may be

ascertained. Each method only gives an estimate, and can therefore give differing results from the other methods. The

main methods that you need to know about for your assessment are the high/low method and the line of best fit

(scattergraph) method.

3.1 High/low method

The high/low method is a 'method of estimating cost behaviour by comparing the total costs associated with two

different levels of output. The difference in costs is assumed to be caused by variable costs increasing, allowing unit

variable cost to be calculated. Following from this, since total cost is known, the fixed cost can be derived.'

CIMA Official Terminology

FA

S

T F

O

RWAR

D

Key term

Assessment

focus point

63433 www.ebooks2000.blogspot.com

Part A Cost determination and behaviour ⏐ 2: Cost behaviour

43

(a) Records of costs in previous periods are reviewed and the costs of the following two periods are selected.

(i) The period with the highest volume of activity

(ii) The period with the lowest volume of activity

(b) The difference between the total cost of these two periods will be the variable cost of the difference in

activity levels (since the same fixed cost is included in each total cost).

(c) The variable cost per unit may be calculated from this (difference in total costs

÷ difference in activity

levels), and the fixed cost may then be determined by substitution.

3.1.1 Example: the high/low method

The costs of operating the maintenance department of a computer manufacturer, Bread and Butter company, for the last

four months have been as follows.

Month Cost Production volume

$ Units

1 110,000 7,000

2 115,000 8,000

3 111,000 7,700

4 97,000 6,000

Required

Calculate the costs that should be expected in month five when output is expected to be 7,500 units. Ignore inflation.

Solution

(a)

Units

$

High output

8,000

total cost

115,000

Low output

6,000

total cost

97,000

Variable cost of

2,000

18,000

Variable cost per unit

$18,000/2,000 = $9

(b) Substituting in either the high or low volume cost:

High Low

$ $

Total cost 115,000 97,000

Variable costs (8,000 × $9)

72,000

(6,000 × $9)

54,000

Fixed costs

43,000

43,000

(c) Estimated maintenance costs when output is 7,500 units:

$

Fixed costs 43,000

Variable costs (7,500 × $9)

67,500

Total costs

110,500

An assessment question will probably not tell you that you need to use the high low method. You need to get used to

thinking for yourself, 'Can I use the high low method here?' Remember that you can use it to split out fixed and variable

elements. So, for example, a question may talk about total costs and then ask you about the variable element.

Assessment

focus point

64433 www.ebooks2000.blogspot.com

44

2: Cost behaviour ⏐ Part A Cost determination and behaviour

Question

High/low method

The Valuation Department of a large firm of surveyors wishes to develop a method of predicting its total costs in a

period. The following past costs have been recorded at two activity levels.

Number of valuations

Total cost

(V)

(TC)

Period 1

420

82,200

Period 2

515

90,275

The total cost model for a period could be represented as follows.

A TC = $46,500 + 85V

B TC = $42,000 + 95V

C TC = $46,500 – 85V

D TC = $51,500 – 95V

Answer

The correct answer is A.

Although we only have two activity levels in this question we can still apply the high/low method.

Valuations

Total cost

V

$

Period 2

515

90,275

Period 1

420

82,200

Change due to variable cost

95

8,075

∴ Variable cost per valuation = $8,075/95 = $85.

Period 2: fixed cost = $90,275 – (515 × $85)

= $46,500

Using good MCQ technique, you should have managed to eliminate C and D as incorrect options straightaway. The

variable cost must be added to the fixed cost, rather than subtracted from it. Once you had calculated the variable cost as

$85 per valuation (as shown above), you should have been able to select option A without going on to calculate the fixed

cost (we have shown this calculation above for completeness).

The high-low method was frequently tested in the form of multiple choice questions under the previous syllabus of this

paper. The information in questions often relates to two activity levels only. The high-low method is still an appropriate

method for identifying the fixed and variable elements of costs where two levels of activity are concerned – you still have

a high and a low activity level.

3.2 'Line of best fit' or scattergraph method

A scattergraph of costs in previous periods can be prepared (with cost on the vertical axis and volume of output on the

horizontal axis). A line of best fit, which is a line drawn by judgement to pass through the middle of the points, thereby

having as many points above the line as below it, can then be drawn and the fixed and variable costs determined.

Assessment

focus point

65433 www.ebooks2000.blogspot.com

Part A Cost determination and behaviour ⏐ 2: Cost behaviour

45

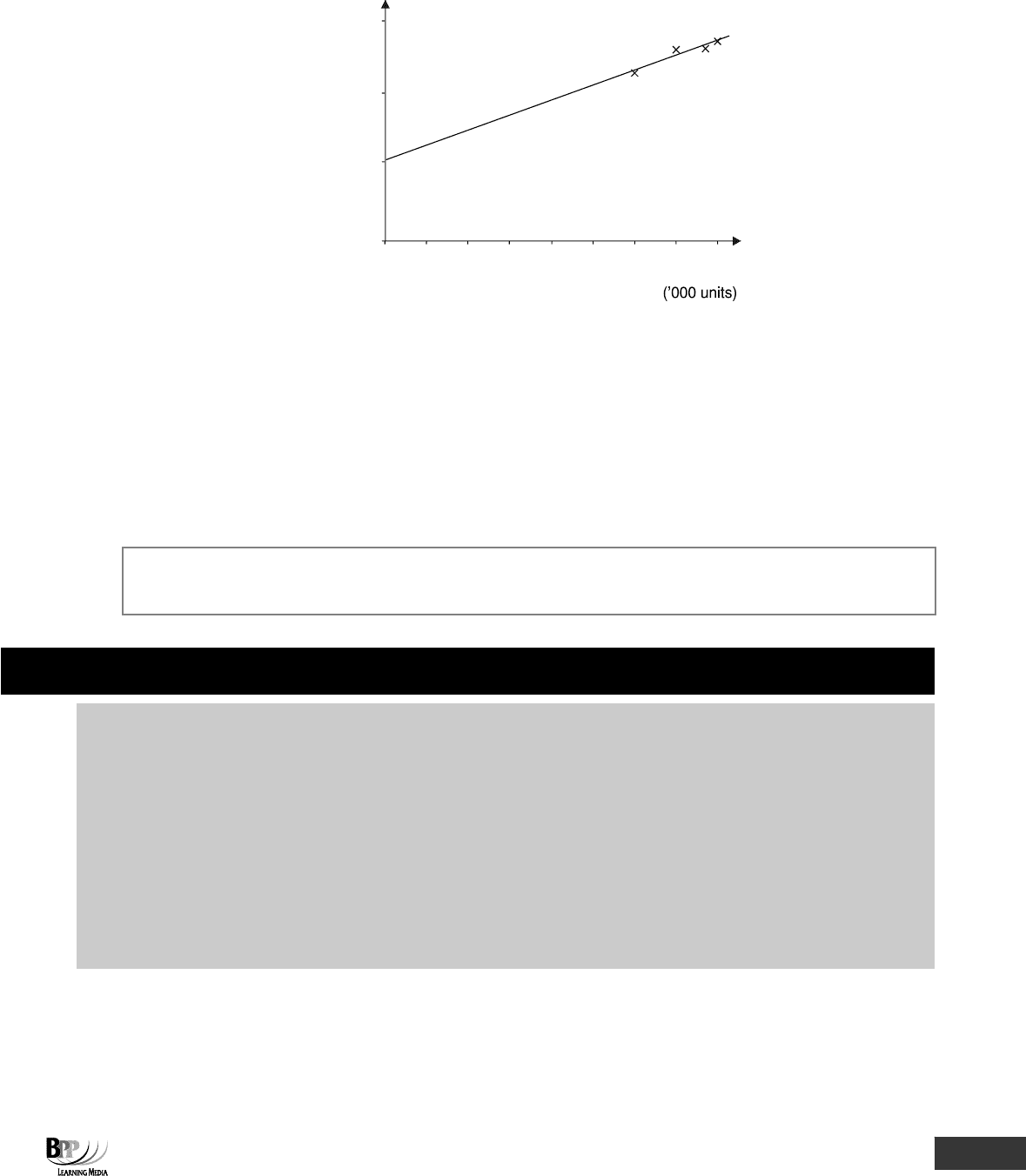

A scattergraph of the cost and volume data in Section 3.1.1 is shown below.

0

40

80

120

012345678

Volume of output

Cost

$

‘000

The point where the line cuts the vertical axis (approximately $40,000) is the fixed cost (the cost if there is no output). If

we take the value of one of the plotted points which lies close to the line and deduct the fixed cost from the total cost, we

can calculate the variable cost per unit.

Total cost for 8,000 units = $115,000

Variable cost for 8,000 units = $(115,000 – 40,000) = $75,000

Variable cost per unit = $75,000/8,000 = $9.375

Note that both the high-low method and the scattergraph method use historical data to predict future costs. The

problem with historical data is that it is not necessarily representative of future data. Management must remember this

when using the results of the high-low or scattergraph method.

Although you would not actually be required to draw a scattergraph, you could perhaps be required to answer a multiple

choice question about how the technique works, or its advantages and limitations.

Chapter Roundup

• Cost behaviour is the way in which a cost changes as activity level changes.

• Costs which are not affected by the level of activity are fixed costs or period costs.

• Variable costs increase or decrease with the level of activity.

• A step cost is a cost which is fixed in nature but only within certain levels of activity. Depending on the time frame being

considered, it may appear as fixed or variable.

• Semi-variable, semi-fixed or mixed costs are costs which are part-fixed and part-variable and are therefore partly

affected by a change in the level of activity.

• The fixed and variable elements of semi-variable costs can be determined by the high-low method or the 'line of best fit'

(scattergraph) method.

Assessment

focus point

66433 www.ebooks2000.blogspot.com

46

2: Cost behaviour ⏐ Part A Cost determination and behaviour

Quick Quiz

1 The basic principle of cost behaviour is that as the level of activity rises, costs will usually fall.

True

False

2 Fill in the gaps for each of the graph titles below.

(a)

$

(b)

$

(c)

$

(d)

$

3 Costs are assumed to be either fixed, variable or semi-variable within the normal or relevant range of output.

True

False

Graph of a ……………….. cost

Example:

Graph of a ……………….. cost

Example:

Graph of a ……………….. cost

Example:

Graph of a ……………….. cost

Example:

67433 www.ebooks2000.blogspot.com

Part A Cost determination and behaviour ⏐ 2: Cost behaviour

47

4 The costs of operating the canteen at 'Eat a lot Company' for the past three months are as follows.

Month Cost Employees

$

1 72,500 1,250

2 75,000 1,300

3 68,750 1,175

Variable cost (per employee per month) =

Fixed cost per month =

5 Pen Co produced the following units at the following costs during October, November and December.

Month Number Total Cost

of units $

October 4,700 252,800

November 5,500 264,000

December 9,500 320,000

The costs could be sub-divided into variable costs of $14 per unit and fixed costs of $........................................

per month.

6 The management accountant at G Co is analysing some costs which have been entered onto the computer as

'miscellaneous staff expenses'.

No of staff Cost per member

of staff

20 $5

100 $5

150 $5

250 $5

What type of cost is the miscellaneous staff expense?

A Fixed

B Variable

C Semi-variable

D Non-linear

68433 www.ebooks2000.blogspot.com

48

2: Cost behaviour ⏐ Part A Cost determination and behaviour

Answers to Quick Quiz

1 False. They will rise.

2 (a) Step cost. Example: rent, supervisors' salaries

(b) Variable cost. Example: raw materials, direct labour

(c) Semi-variable cost. Example: electricity and telephone

(d) Fixed. Example: rent, depreciation (straight-line)

3 True

4 Variable cost = $50 per employee per month

Fixed costs = $10,000 per month

Activity

Cost

$

High

1,300

75,000

Low

1,175

68,750

125

6,250

Variable cost per employee = $6,250/125 = $50

For 1,175 employees, total cost = $68,750

Total cost = variable cost + fixed cost

$68,750 = (1,175 × $50) + fixed cost

∴Fixed cost = $68,750 – $58,750

= $10,000

5 $187,000

Using the high-low method we have:

Units

Cost

$

Highest

9,500

320,000

Lowest

4,700

252,800

Difference

4,800

67,200

Variable costs = 67,200/4,800 = $14/unit

Fixed costs = Total cost – variable cost

At 9,500 units, fixed cost = $320,000 – (9,500 × $14) = $187,000

6 B Variable. Make sure you read the question carefully. Note that the $5 is per staff member so 100 staff would

mean $500 in expenditure.

Now try the questions below from the Question Bank

Question numbers Page

6–10 352

69433 www.ebooks2000.blogspot.com

49

Topic list Learning outcomes Syllabus references Ability required

1 Overhead allocation A(viii) A(4) Application

2 Overhead apportionment A(viii) A(4) Application

3 Overhead absorption A(ix) A(4) Application

4 Blanket absorption rates and departmental

absorption rates

A(ix) A(4) Application

5 Over and under absorption of overheads A(ix) A(4) Application

6 Activity based costing A(viii), (ix) A(4) Application

Overhead costs –

absorption costing

Introduction

Here we study one method of dealing with overheads, absorption costing, which is defined

in CIMA Official Terminology as a cost accounting method that 'assigns direct costs and all

or part of overhead to cost units using one or more overhead absorption rates'. (It is

sometimes referred to as full costing.)

Absorption costing is a method for sharing overheads between a number of different

products on a fair basis. The chapter begins by looking at the three stages of absorption

costing: allocation, apportionment and absorption. We then move on to the important issue

of over/under absorption. Over/under absorption is very likely to be included in your

assessment, so ensure you know how to deal with it.

In the next chapter we'll see an alternative approach to accounting for overheads – marginal

costing.

70433 www.ebooks2000.blogspot.com