CIMA - C1 Fundamentals of Management Accounting

Подождите немного. Документ загружается.

xx

Introduction

International terminology

Your Fundamentals of Management Accounting assessment will use international accounting terms and this text is written

in international accounting terms.

It is a good idea to start now getting used to these terms. Below is a list of UK terms with their international equivalents.

UK term International term

Profit and loss account Income statement (statement of comprehensive income)

Profit and loss reserve (in balance sheet) Accumulated profits

Balance sheet Statement of financial position

Turnover Revenue

Debtor account Account receivable

Debtors (eg debtors have increased) Receivables

Debtor Customer

Creditor account Account payable

Creditors (eg creditors have increased) Payables

Creditor Supplier

Debtors control account Receivables control account

Creditors control account Payables control account

Stock Inventory

Fixed asset

Non-current asset (generally). Tangible fixed assets are also referred to

as ‘property, plant and equipment’.

Long term liability Non-current liability

Provision (eg for depreciation) Allowance (you will sometimes see ‘provision’ used too).

Nominal ledger General ledger

VAT Sales tax

Debentures Loan notes

Preference shares/dividends Preferred shares/dividends

Cash flow statement Statement of cash flows

21433 www.ebooks2000.blogspot.com

1

Part A

Cost determination and

behaviour

22433

www.ebooks2000.blogspot.com

2

23433 www.ebooks2000.blogspot.com

3

Introduction to management

accounting and costing

Introduction

Welcome to BPP's Study Text for CIMA's Certificate Paper C1 Fundamentals of

Management Accounting. This chapter will introduce the subject of cost accounting and

explain what cost accounting is and what a cost accountant does.

We will then turn our attention to costs and consider what cost actually is! We'll then look at

some of the ways in which costs can be classified to assist the work of the cost accountant.

Terms and concepts you encounter in these sections of the chapter are vitally important and

will appear throughout this text and indeed all stages of your studies.

The chapter will end with a section on cost codes. Once costs are classified (see Sections 4

to 7), they are coded so that they are identifiable. They can then be manipulated and used by

cost accountants.

Topic list Learning outcomes Syllabus references Ability required

1 What is cost accounting? A(i) A(1) Comprehension

2 Some cost accounting concepts A(ii) A(1) Comprehension

3 The concept of cost A(iv), (v) A(2) Comprehension

4 Cost classification A(i), D(vi) A(1), D(6) Comprehension

5 Cost classification for inventory valuation and

profit measurement

A(iii) A(1) Comprehension

6 Cost classification for decision making A(i) A(1) Comprehension

7 Cost classification for control A(i) A(1) Comprehension

8 Cost codes D(vi), (vii) D(5) Comprehension,

Analysis

24433 www.ebooks2000.blogspot.com

4

1: Introduction to management accounting and costing ⏐ Part A Cost determination and behaviour

1 What is cost accounting?

Cost accounting is a management information system which analyses past, present and future data to provide the basis

for managerial action.

1.1 The cost accountant

Who can provide the answers to the following questions?

• What was the cost of goods produced or services provided last period?

• What was the cost of operating a department last month?

• What revenues were earned last week?

Yes, you've guessed it, the cost accountant.

Knowing about costs incurred or revenues earned enables management to do the following.

(a) Assess the profitability of a product, a service, a department, or the whole organisation.

(b) Perhaps, set selling prices with some regard for the costs of sale.

(c) Put a value on inventory (raw materials, work in progress, finished goods) that are still held in store at the

end of a period, for preparing a statement of financial position showing of the company's assets and

liabilities.

That was quite easy. But who could answer the following questions?

(a) What are the future costs of goods and services likely to be?

(b) How do actual costs compare with planned costs?

(c) What information does management need in order to make sensible decisions about profits and costs?

Well, you may be surprised, but again it is the cost accountant.

1.2 Cost accounting and management accounting

Management accounting, and nowadays cost accounting, provide management information for planning, control and

decision-making purposes.

Originally cost accounting did deal with ways of accumulating historical costs and of charging these costs to units of

output, or to departments, in order to establish inventory valuations, profits and statement of financial position items. It

has since been extended into planning, control and decision making, so that the cost accountant is now able to answer

the second set of questions. In today's modern industrial environment, the role of cost accounting in the provision of

management information is therefore almost indistinguishable from that of management accounting, which is basically

concerned with the provision of information to assist management with planning, control and decision making.

Cost accounting is the 'gathering of cost information and its attachment to cost objects, the establishment of budgets,

standard costs and actual costs of operations, processes, activities or products; and the analysis of variances,

profitability or the social use of funds'. CIMA Official Terminology

So, as you can see, the cost accountant has his or her hands full! Don't worry about the terms mentioned in CIMA's

definition – all will become clearer as you work through this Study Text.

FA

S

T F

O

RWAR

D

FAST FORWARD

Key term

25433 www.ebooks2000.blogspot.com

Part A Cost determination and behaviour ⏐ 1: Introduction to management accounting and costing

5

1.3 Cost accounting systems

The managers of a business have the responsibility of planning and controlling the resources used. To carry out this task

effectively they must be provided with sufficiently accurate and detailed information, and the cost accounting system

should provide this. Indeed a costing system is the basis of an organisation's internal financial information system for

managers.

Cost accounting systems are not restricted to manufacturing operations.

(a) Cost accounting information is also used in service industries, government departments and welfare

organisations.

(b) Within a manufacturing organisation, the cost accounting system should be applied not only to

manufacturing operations but also to administration, selling and distribution, research and development

and so on.

Cost accounting is concerned with providing information to assist the following.

• Establishing inventory valuations, profits and statement of financial position items

• Planning (for example the provision of forecast costs at different activity levels)

• Control (such as the provision of actual and standard costs for comparison purposes)

• Decision making (for example, the provision of information about actual unit costs for the period just

ended for pricing decisions).

1.4 Financial accounting versus cost accounting

In general terms, financial accounting is for external reporting whereas cost accounting is for internal reporting.

The financial accounting and cost accounting systems in a business both record the same basic data for income and

expenditure, but each set of records may analyse the data in a different way. This is because each system has a different

purpose.

(a) Financial accounts are prepared for individuals external to an organisation eg shareholders, customers,

suppliers, HM Revenue and Customs and employees.

(b) Management accounts are prepared for internal managers of an organisation.

The data used to prepare financial accounts and management accounts are the same. The differences between the

financial accounts and the management accounts arise because the data is analysed differently.

Financial accounts Management accounts

Financial accounts detail the performance of an

organisation over a defined period and the state of affairs

at the end of that period.

Management accounts are used to aid management

record, plan and control the organisation's activities and to

help the decision-making process.

In the UK, limited companies must, by law, prepare

financial accounts.

There is no legal requirement to prepare management

accounts.

FAST FORWARD

26433 www.ebooks2000.blogspot.com

6

1: Introduction to management accounting and costing ⏐ Part A Cost determination and behaviour

Financial accounts Management accounts

The format of published financial accounts is determined

by law (mainly the Companies Acts), by Statements of

Standard Accounting Practice and by Financial Reporting

Standards. In principle the accounts of different

organisations can therefore be easily compared.

The format of management accounts is entirely at

management discretion: no strict rules govern the way

they are prepared or presented. Each organisation can

devise its own management accounting system and format

of reports.

Financial accounts concentrate on the business as a whole,

aggregating revenues and costs from different operations,

and are an end in themselves.

Management accounts can focus on specific areas of an

organisation's activities. Information may be produced to aid

a decision rather than to be an end product of a decision.

Most financial accounting information is of a monetary

nature.

Management accounts incorporate non-monetary

measures. Management may need to know, for example,

tonnes of aluminium produced, monthly machine hours, or

miles travelled by sales representatives.

Financial accounts present an essentially historical picture

of past operations.

Management accounts are both a historical record and a

future planning tool.

2 Some cost accounting concepts

2.1 Functions and departments

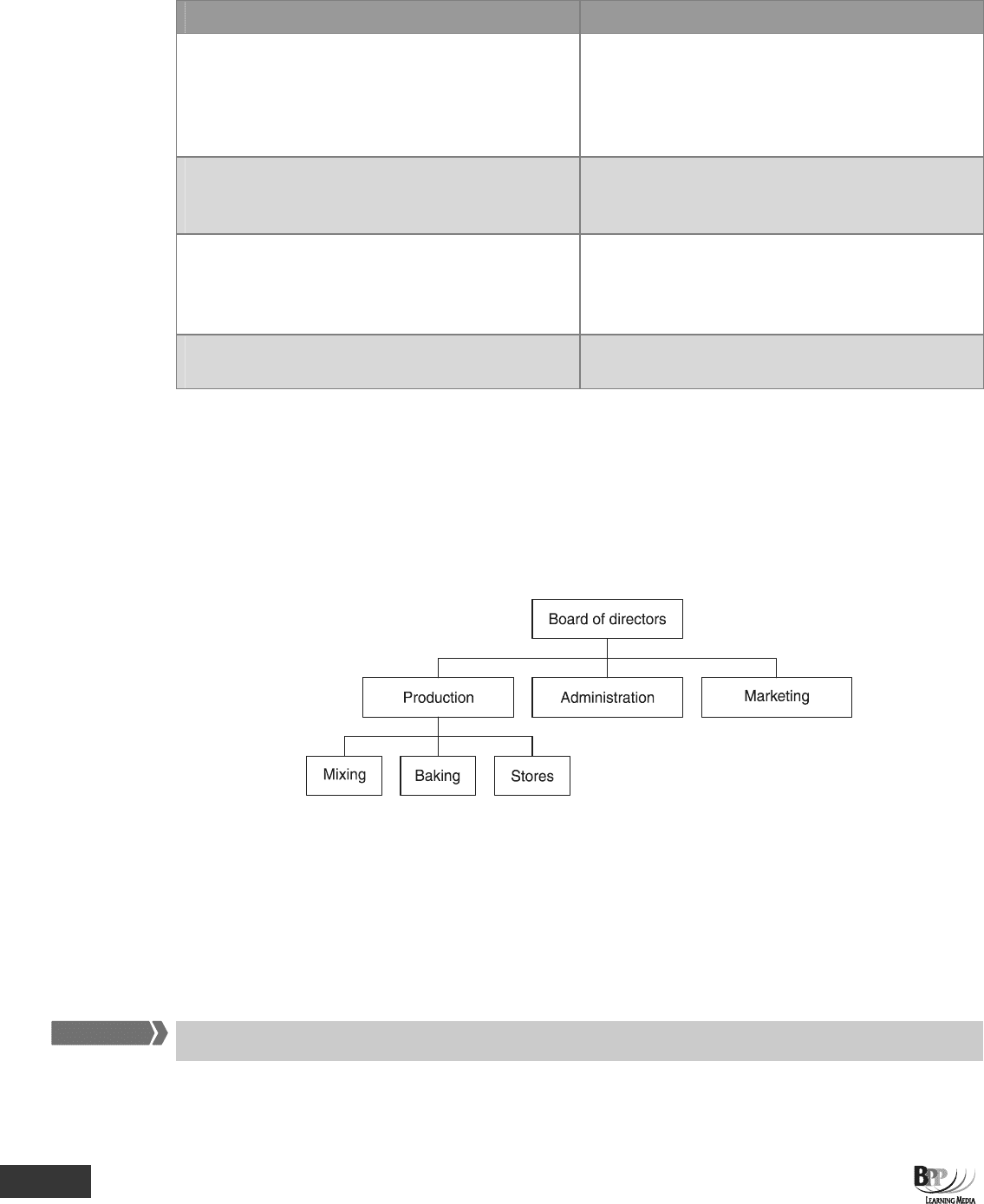

An organisation, whether it is a manufacturing company, a provider of services (such as a bank or a hotel) or a public

sector organisation (such as a hospital), may be divided into a number of different functions within which there are a

number of departments. A manufacturing organisation might be structured as follows.

Suppose the organisation above produces chocolate cakes for a number of supermarket chains. The production function

is involved with the making of the cakes, the administration department with the preparation of accounts and the

employment of staff and the marketing department with the selling and distribution of the cakes.

Within the production function there are three departments, two of which are production departments (the mixing

department and the baking department) which are actively involved in the production of the cakes and one of which is a

service department (stores department) which provides a service or back-up to the production departments.

2.2 Cost objects

If the users of accounting information want to know the cost of something, that something is called a cost object.

Examples of cost objects include:

• A product

FAST FORWARD

27433 www.ebooks2000.blogspot.com

Part A Cost determination and behaviour ⏐ 1: Introduction to management accounting and costing

7

• A service to a hotel guest

• A sales territory

A cost object is 'for example a product, service, centre, activity, customer or distribution channel in relation to which

costs are ascertained'. CIMA Official Terminology

In our example, cost objects include:

• Chocolate cakes

• The provision of supply to one of the supermarkets

• The administration department

2.3 Cost centres

Cost centres are collecting places for costs before they are further analysed.

In general, for cost accounting purposes, departments are termed cost centres and the product produced by an

organisation is termed the cost unit. In our example, the cost centres of the production function could be the mixing

department, the baking department and the stores department and the organisation's cost unit could be one chocolate

cake.

When costs are incurred, they are generally allocated to a cost centre. Cost centres may include the following.

• A department (as in our example above)

• A machine or group of machines

• A project (eg the installation of a new computer system)

• A new product (to enable the costs of development and production to be identified)

• A person (eg a marketing director. Costs might include salary, company car and other expenses incurred

by the director)

A typical objective testing (OT) question on the contents of this chapter might be to ask you to select appropriate cost

centres from a number of suggestions for a particular organisation.

2.4 Cost units

Cost units are the basic control units for costing purposes.

A cost unit is a 'unit of product or service in relation to which costs are ascertained'. CIMA Official Terminology

Once costs have been traced to cost centres, they can be further analysed in order to establish a cost per cost unit.

Alternatively, some items of costs may be charged directly to a cost unit, for example direct materials and direct labour

costs, which you will meet later in this text.

Different organisations use different cost units. Here are some suggestions.

Organisation Possible cost unit

Steelworks

Tonne of steel produced

Tonne of coke used

Hospital

Patient/day

Key term

F

A

S

T F

O

RWAR

D

Assessment

focus point

FAST FORWARD

Key term

28433 www.ebooks2000.blogspot.com

8

1: Introduction to management accounting and costing ⏐ Part A Cost determination and behaviour

Operation

Out-patient visit

Freight organisation Tonne/kilometre

Passenger transport organisation

Passenger/kilometre

Accounting firm

Audit performed

Chargeable hour

Restaurant

Meal served

Note that cost units can be tangible or non-tangible. Tangible cost units can be seen and touched, for example, a meal

served. A chargeable hour is intangible.

2.5 Composite cost units

Notice that some of the cost units in this table are made up of two parts. For example the patient/day cost unit for the

hospital. These two-part cost units are known as composite cost units and they are used most often in service

organisations.

Composite cost units help to improve cost control. For example the measure of 'cost per patient' might not be

particularly useful for control purposes. The cost per patient will vary depending on the length of the patient's stay,

therefore monitoring costs using this basis would be difficult.

The cost per patient/day is not affected by the length of the individual patient's stay. Therefore it would be more useful

for monitoring and controlling costs. Similarly, in a freight organisation the cost per tonne/kilometre (the cost of

carrying one tonne for one kilometre) would be more meaningful for control than the cost per tonne carried, which

would vary with the distance travelled.

Question

Cost centres and cost units

Identify the following as suitable cost centres or cost units for a hospital.

• Ward

• Operating theatre

• Bed/night

• Patient/day

• Outpatient visit

• Operating theatre hour

Answer

Cost unit

Cost Centre

Bed/night

Patient/day

Operating theatre hour

Outpatient visit

Ward

Operating theatre

29433

www.ebooks2000.blogspot.com

Part A Cost determination and behaviour ⏐ 1: Introduction to management accounting and costing

9

3 The concept of cost

3.1 Cost measurement

In practice most cost accounting transactions are recorded at historic cost, but costs can be measured in terms of

economic cost.

Cost accounting transactions, indeed all accounting transactions, can be measured (or valued) on numerous bases. For

example:

(a) Cost accounts kept on a historical cost basis use original/past values.

(b) Cost accounts kept on a current cost basis use up-to-date market values.

Transactions can also be recorded at economic cost.

3.1.1 Economic cost

Economic cost, also referred to as opportunity cost, is the value of the best alternative course of action that was not

chosen. In other words, it is what could have been accomplished with the resources used in the course of action not

chosen. It represents opportunities forgone.

If a person has a job offer that pays $25 for an hour's work, and instead chooses to take a nap for an hour, the historical

cost of the nap is zero; the person did not hand over any money in order to nap. The economic cost of the nap is the $25

that could have been earned working.

In practice most cost accounting systems use historical cost as a measurement basis.

3.2 Economic value

Economic value is the amount someone is willing to pay.

The economic value of a particular item, for example a kilogram of rice, is measured by the maximum amount of other

things that a person is willing to give up to have that kilogram of rice. If we simplify our example 'economy' so that the

person only has two goods to choose from, rice and pasta, the value of a kilogram of rice would be measured by the

amount of pasta that the person is willing to give up to have one more kilogram of rice.

Economic value is therefore measured by the most someone is willing to give up in other products and services in

order to obtain a product or service. Dollars (or some other currency) are a universally accepted measure of economic

value in many markets, because the number of dollars that a person is willing to pay for something tells how much of all

other goods and services they are willing to give up to get that item. This is often referred to as ‘willingness to pay’.

3.3 Qualifying the concept of cost

As a noun, cost is ‘The amount of cash or cash equivalent paid ….’

As a verb, cost is ‘To ascertain the cost of a specified thing or activity.

The word cost can rarely stand alone and should be qualified as to its nature and limitations.’

CIMA Official Terminology

Costs need to be qualified or classified in some way so that they can be arranged into logical groups in order to

facilitate an efficient system for collecting and analysing costs.

FA

S

T F

O

RWAR

D

Key term

FAST FORWARD

30433 www.ebooks2000.blogspot.com