CIMA - C1 Fundamentals of Management Accounting

Подождите немного. Документ загружается.

290

12: Process costing ⏐ Part D Costing and accounting systems

(iv) abnormal gain are

0

kgs at $

0

(v) WIP materials are

3,400

kgs at $

13,600

(vi) WIP conversion costs are

0

kgs at $

10,064

(b) Process 2

STATEMENT OF EQUIVALENT UNITS

Total units

Process 1

Conversion costs

Finished goods

2,500

2,500

2,500

Normal loss

240

0

0

Abnormal gain

(690)

(690)

(690)

Closing WIP

*

2,600

*

2,600

1,040

**

4,650

4,410

2,850

* Total input units = opening WIP + input = 2,250 + 2,400 = 4,650

Total output units = finished goods + closing WIP + normal loss – abnormal gain

= 2,500 + 2,600 + 240 – 690

= 4,650

** 2,600 × 40% = 1,040

STATEMENT OF COSTS PER EQUIVALENT UNIT

Process 1 =

+−$4,431 $27,360 480

4,410

= $7.10

Conversion costs =

++$5,250 $15,000 $22,500

2,850

= $15.00

STATEMENT OF EVALUATION

Process 1

Conversion costs

Totals

$ $ $

Finished goods 17,750 37,500 55,250

Abnormal gain (4,899) (10,350) (15,249)

Closing WIP 18,460 15,600 34,060

PROCESS 2 ACCOUNT

Kg

$

Kg

$

WIP Process 1

2,250

4,431

Finished goods

2,500

55,250

WIP conversion costs

–

5,250

Normal loss

240

480

Process 1

2,400

27,360

WIP Process 1

2,600

18,460

Labour

–

15,000

WIP conversion costs

–

15,600

Overhead

–

22,500

Abnormal gain

690

15,249

5,340

89,790

5,340

89,790

The monetary and quantity values for:

(i) finished goods are

2,500

kgs at $

55,250

(ii) normal loss are

240

kgs at $

480

(iii) WIP from process 1 are

2,600

kgs at $

18,460

(iv) WIP from process 2 are

0

kgs at $

15,600

311433 www.ebooks2000.blogspot.com

Part D Costing and accounting systems ⏐ 12: Process costing

291

Many students find process costing difficult. The best ways to improve your understanding are to memorise the step

approach and to practise as many questions as possible.

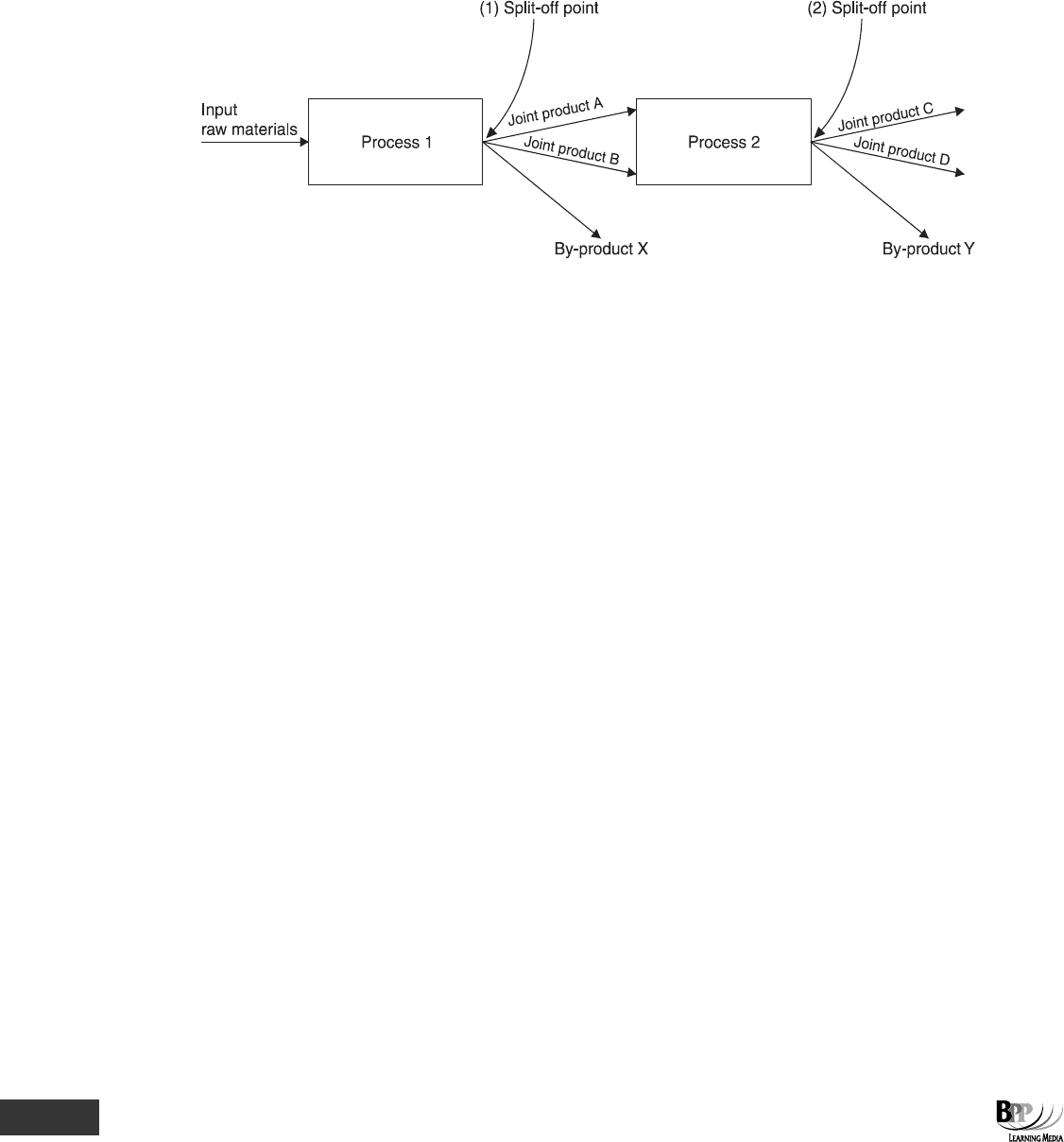

7 Joint products and by-products

7.1 Joint products

Joint products are two or more products separated in a process each of which has a significant value compared to the other.

Joint products are 'two or more products produced by the same process and separated in processing, each having a

sufficiently high saleable value to merit recognition as a main product'. CIMA Official terminology

Joint products:

•

Are produced in the same process

•

Are indistinguishable from each other until the separation point

•

Have a substantial sales value (after further processing, if necessary)

•

May require further processing after the separation point

For example in the oil refining industry the following joint products all arise from the same process.

•

Diesel fuel • Paraffin

•

Petrol

•

Lubricants

7.2 By-products

A by-product is an incidental product from a process which has an insignificant value compared to the main

product(s).

A by-product is 'output of some value produced incidentally while manufacturing the main product’.

CIMA Official terminology

A by-product is a product which is similarly produced at the same time and from the same common process as the

'main product' or joint products. The distinguishing feature of a by-product is its relatively low sales value in

comparison to the main product. In the timber industry, for example, by-products include sawdust, small offcuts and

bark.

7.3 Distinguishing joint products from by-products

The answer lies in management attitudes to their products, which in turn is reflected in the cost accounting system.

(a) A joint product is regarded as an important saleable item, and so it should be separately costed. The

profitability of each joint product should be assessed in the cost accounts.

(b) A by-product is not important as a saleable item, and whatever revenue it earns is a 'bonus' for the

organisation. It is not worth costing by-products separately, because of their relative insignificance. It is

therefore equally irrelevant to consider a by-product's profitability. The only question is how to account for

the 'bonus' net revenue that a by-product earns.

Assessment

focus point

FA

S

T F

O

RWAR

D

FA

S

T F

O

RWAR

D

Key term

Key term

312433 www.ebooks2000.blogspot.com

292

12: Process costing ⏐ Part D Costing and accounting systems

7.4 Accounting for joint and by-products

The point at which joint and by-products become separately identifiable is known as the split-off point or separation

point. Costs incurred up to this point are called common costs or joint costs.

Common or joint costs need to be allocated (apportioned) in some manner to each of the joint products. In the following

sketched example, there are two different split-off points.

7.5 Apportioning common costs

Reasons for apportioning common costs to individual joint products are as follows.

(a) To put a value to closing inventories of each joint product.

(b) To record the costs and therefore the profit from each joint product. This is of limited value however,

because the costs and therefore profit from one joint product are influenced by the share of costs

assigned to the other joint products. Management decisions would be based on the apparent relative

profitability of the products which has arisen due to the arbitrary apportionment of the joint costs.

(c) Perhaps to assist in pricing decisions.

Here are some examples of the common costs problem.

(a) How to spread the common costs of oil refining between the joint products made (petrol, naphtha,

kerosene and so on).

(b) How to spread the common costs of running the telephone network between telephone calls in peak rate times

and cheap rate times, or between local calls and long-distance calls.

Note that joint costs are not allocated to by-products.

7.5.1 Methods of apportioning common costs

The main methods that might be used to establish a basis for apportioning or allocating common costs to each product

are as follows.

•

Physical measurement (eg weight of output)

•

Relative sales value apportionment method 1; sales value at split-off point

•

Relative sales value apportionment method 2; sales value of end product less further processing costs

after split-off point, ie the net realisable value of each product at the split-off point.

313433 www.ebooks2000.blogspot.com

Part D Costing and accounting systems ⏐ 12: Process costing

293

7.6 Accounting for by-products

Despite the fact that the by-product has a small value relative to that of the main product, it does have some

commercial value and its accounting treatment usually consists of one of the following.

(a) Income (minus any post-separation further processing or selling costs) from the sale of the by-product

may be added to sales of the main product, thereby increasing sales revenue for the period.

(b) The sales of the by-product may be treated as a separate, incidental source of income against which are

set only post-separation costs (if any) of the by-product. The revenue would be recorded in the income

statement as 'other income'.

(c) The sales income of the by-product may be deducted from the cost of production or cost of sales of the

main product.

(d) The net realisable value of the by-product may be deducted from the cost of production of the main

product. The net realisable value is the final saleable value of the by-product minus any post-separation

costs.

The choice of method will be influenced by the circumstances of production and ease of calculation, as much as by

conceptual correctness. The most common method is method (d). Notice that this method is the same as the accounting

treatment of a normal loss which is sold for scrap.

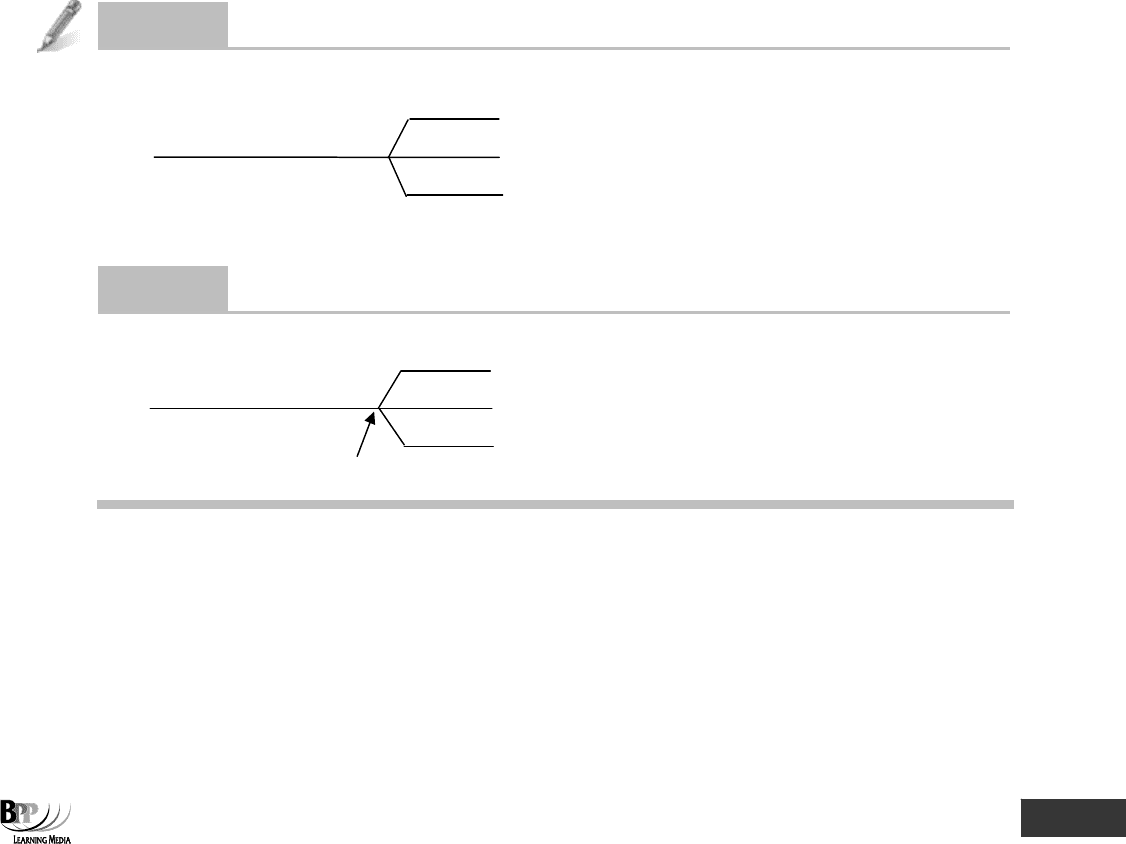

Question

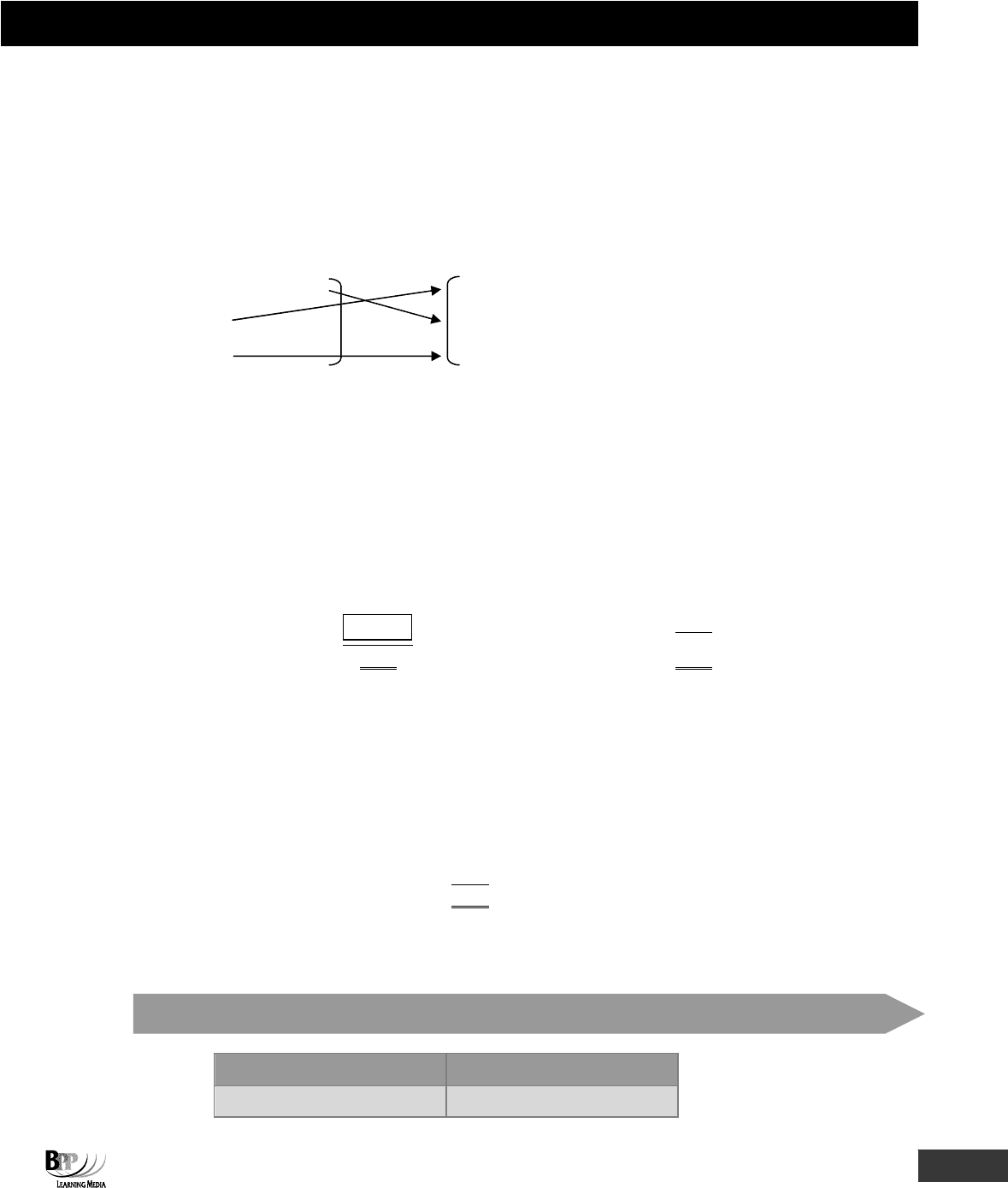

Split-off point

Butter

Milk Cream

Yoghurt

Mark the split-off point on the diagram above.

Answer

Butter

Milk Cream

Yoghurt

Split off point

314433 www.ebooks2000.blogspot.com

294

12: Process costing ⏐ Part D Costing and accounting systems

Chapter Roundup

•

Process costing is a costing method used where it is not possible to identify separate units of production, or jobs,

usually because of the continuous nature of the production processes involved.

•

A process account has two sides, and on each side there are two columns – one for quantities (of raw materials, work

in progress and finished goods) and one for costs.

•

Use our suggested four-step approach when dealing with process costing questions.

Step 1

Determine output and losses

Step 2

Calculate cost per unit of output, losses and WIP

Step 3

Calculate total cost of output, losses and WIP

Step 4

Complete accounts

•

Losses may occur in process. If a certain level of loss is expected, this is known as normal loss. If losses are greater

than expected, the extra loss is abnormal loss. If losses are less than expected, the difference is known as abnormal

gain.

•

The valuation of normal loss is either at scrap value or nil. It is conventional for the scrap value of normal loss to be

deducted from the cost of materials before a cost per equivalent unit is calculated.

•

Abnormal losses and gains never affect the cost of good units of production. The scrap value of abnormal losses is not

credited to the process account, and the abnormal loss and gain units carry the same full cost as a good unit of

production.

•

When units are partly completed at the end of a period (ie when there is closing work in progress) it is necessary to

calculate the equivalent units of production in order to determine the cost of a completed unit.

•

The weighted average cost method of valuing opening WIP makes no distinction between units of opening WIP and new

units introduced to the process during the current period.

•

Joint products are two or more products separated in a process, each of which has a significant value to the other.

•

A by-product is an incidental product from a process which has an insignificant value compared to the main

products(s).

315433 www.ebooks2000.blogspot.com

Part D Costing and accounting systems ⏐ 12: Process costing

295

Quick Quiz

1 Choose the correct words from those highlighted.

Process costing is often identified with construction of large buildings/paint manufacture/services provided in a

supermarket.

2 Process costing is centred around four key steps. What are they?

Step 1

………………………………………………………………………………………..

Step 2

………………………………………………………………………………………..

Step 3

………………………………………………………………………………………..

Step 4

………………………………………………………………………………………..

3 Abnormal gains result when actual loss is less than normal or expected loss.

True

False

4 Match the types of loss with the correct method of valuation.

Normal loss (no scrap value) Same value as good output (positive cost)

Abnormal loss No value

Abnormal gain Same value as good output (negative cost)

5 How is revenue from scrap treated?

A As an addition to sales revenue

B As a reduction in costs of processing

C As a bonus to employees

D Any of the above

6 When there is closing WIP at the end of a process, the first step in the four-step approach to process costing questions

is to draw up a statement of evaluation.

True

False

7 Choose the correct words from those highlighted.

The weighted average cost method of inventory valuation makes no distinction/makes a distinction between units of

opening WIP and new units introduced to the process during the current period.

?

316433 www.ebooks2000.blogspot.com

296

12: Process costing ⏐ Part D Costing and accounting systems

8 Yum Co makes a fizzy drink which passes through several processes. The normal loss is 5% of the input from the

previous period and can be sold at $0.50 per litre. The equivalent cost per litre has been calculated as $9.50 per

complete litre.

The following information is available for June.

From

Opening previous To next Closing

Inventory period period inventory

Litres 200 1,000 1,150 160

Are the following statements true or false?

True False

Yum Co would make an abnormal loss

The level of abnormal loss/gain is 40 litres

9 A factory operates a processing operation which has a normal loss of 10%. Scrapped units sell for $2 per kg. The

following information is available for June.

Materials used 2,000 kg @ $4 per kg

Output 1,700 kg

What is the scrap value for the abnormal loss?

A Nil

B $200

What would the double entry be for the scrap value of the abnormal loss?

C Dr Scrap value

Cr Abnormal loss account

D Dr Scrap value

Cr Process account

317433 www.ebooks2000.blogspot.com

Part D Costing and accounting systems ⏐ 12: Process costing

297

Answers to Quick Quiz

1 Process costing is often identified with paint manufacture.

2

Step 1

Determine output and losses

Step 2

Calculate cost per unit of output, losses and WIP

Step 3

Calculate total cost of output, losses and WIP

Step 4

Complete accounts

3 True

4 Normal loss (no scrap value) Same value as good output (positive cost)

Abnormal loss No value

Abnormal gain Same value as good output (negative cost)

5 B

6 False. The first step is to calculate the equivalent units of production by drawing up a statement of equivalent units.

7 The weighted average cost method of inventory valuation makes no distinction between units of opening WIP and new

units introduced to the process during the current period.

8 False, False

Process account

Dr

Cr

Opening WIP

200

Output

1,150

Input

1,000

Normal loss

50

Abnormal gain

Closing WIP

1,360

1,360

The balancing figure is a debit therefore an abnormal gain. 1,360 – 200 – 1,000 = 160.

9 B & C

Determine output and losses:

Process

Kg

Output

1,700

Normal loss (10% of input)

200

Abnormal loss (balancing figure)

100

2,000

Scrap value of abnormal loss = 100 kg x $2

= $200

Now try the questions below from the Question Bank

Question numbers Page

65–78 366

318433 www.ebooks2000.blogspot.com

298

12: Process costing ⏐ Part D Costing and accounting systems

319433 www.ebooks2000.blogspot.com

299

Topic list Learning outcomes Syllabus references Ability required

1 Job costing D(iii) D(4) Analysis

2 Job costing example D(iv) D(4) Application

3 Job costing for internal services D(iii) D(4) Analysis

4 Batch costing D(iii), (iv) D(4) Analysis, Application

5 Contracts and contract costing D(iii) D(4) Analysis

6 Contract costs D(iv) D(4) Application

7 Progress payments and retentions D(iv) D(4) Application

8 Profits on contracts D(iv) D(4) Application

9 Losses on incomplete contracts D(iv) D(4) Application

10 Disclosure of long-term contracts in

financial accounts

D(iv) D(4) Application

Job, batch and

contract costing

Introduction

A costing method is designed to suit the way goods are processed or manufactured or the

way services are provided. Each organisation's costing method will therefore have unique

features but costing methods of firms in the same line of business will more than likely have

common aspects. We've already looked at process costing, which is used when production is

a continuous flow of identical units.

In this chapter we will be looking at specific order costing methods, specific order costing

being the 'basic cost accounting method applicable if work consists of separately identifiable

batches, contracts or jobs' (CIMA Official Terminology).

This chapter begins by covering job costing and then moves on to batch costing, the

procedure for which is similar to job costing.

The third costing method considered in this chapter is contract costing. Contract costing is

similar to job costing but the job is of such importance that a formal contract is made

between the supplier and the customer. We will see how to record contract costs, how to

account for any profits and losses arising on contracts at the end of an accounting period

and we will look briefly at how contract balances are disclosed in financial accounts.

320433 www.ebooks2000.blogspot.com