CIMA - C1 Fundamentals of Management Accounting

Подождите немного. Документ загружается.

270

12: Process costing ⏐ Part D Costing and accounting systems

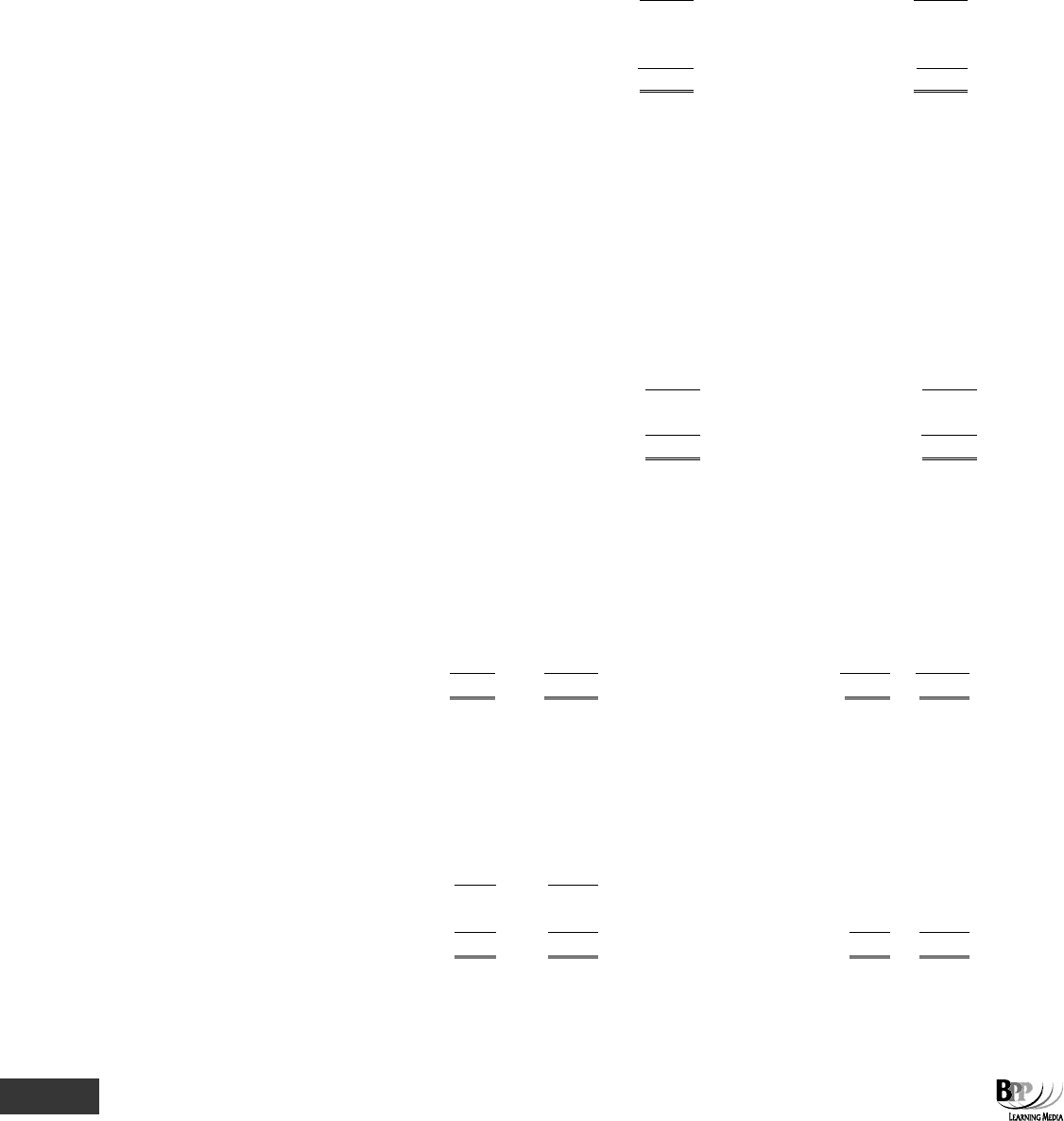

Step 3

Calculate total cost of output and losses

Period 3

$

Cost of output (850 × $32.30)

27,455

Normal loss

0

Abnormal loss (50 × $32.30)

1,615

29,070

Period 4

$

Cost of output (950 × $32.30)

30,685

Normal loss

0

Abnormal gain (50 × $32.30)

1,615

29,070

Step 4

Complete accounts

PROCESS ACCOUNT

Units

$

Units

$

Period 3

Cost of input

1,000

29,070

Normal loss

100

0

Finished goods a/c

850

27,455

(× $32.30)

Abnormal loss a/c

50

1,615

(× $32.30)

1,000

29,070

1,000

29,070

Period 4

Cost of input

1,000

29,070

Normal loss

100

0

Abnormal gain a/c

50

1,615

Finished goods a/c

950

30,685

(× $32.30)

(× $32.30)

1,050

30,685

1,050

30,685

ABNORMAL LOSS OR GAIN ACCOUNT

$

$

Period 3

Period 4

Abnormal loss in process a/c

1,615

Abnormal gain in process a/c

1,615

Abnormal loss in process a/c

1,615

Abnormal gain in process a/c

1,615

There is a zero balance on this account at the end of period 4.

Question

Cost of output

Charlton Co manufactures a product in a single process operation. Normal loss is 10% of input. Loss occurs at the end

of the process. Data for June are as follows.

Opening and closing inventories of work in progress Nil

Cost of input materials (3,300 units) $59,100

Direct labour and production overhead $30,000

Output to finished goods 2,750 units

The full cost of finished output in June was

A $74,250

B $81,000

C $82,500

D $89,100

291433 www.ebooks2000.blogspot.com

Part D Costing and accounting systems ⏐ 12: Process costing

271

Answer

The correct answer is C.

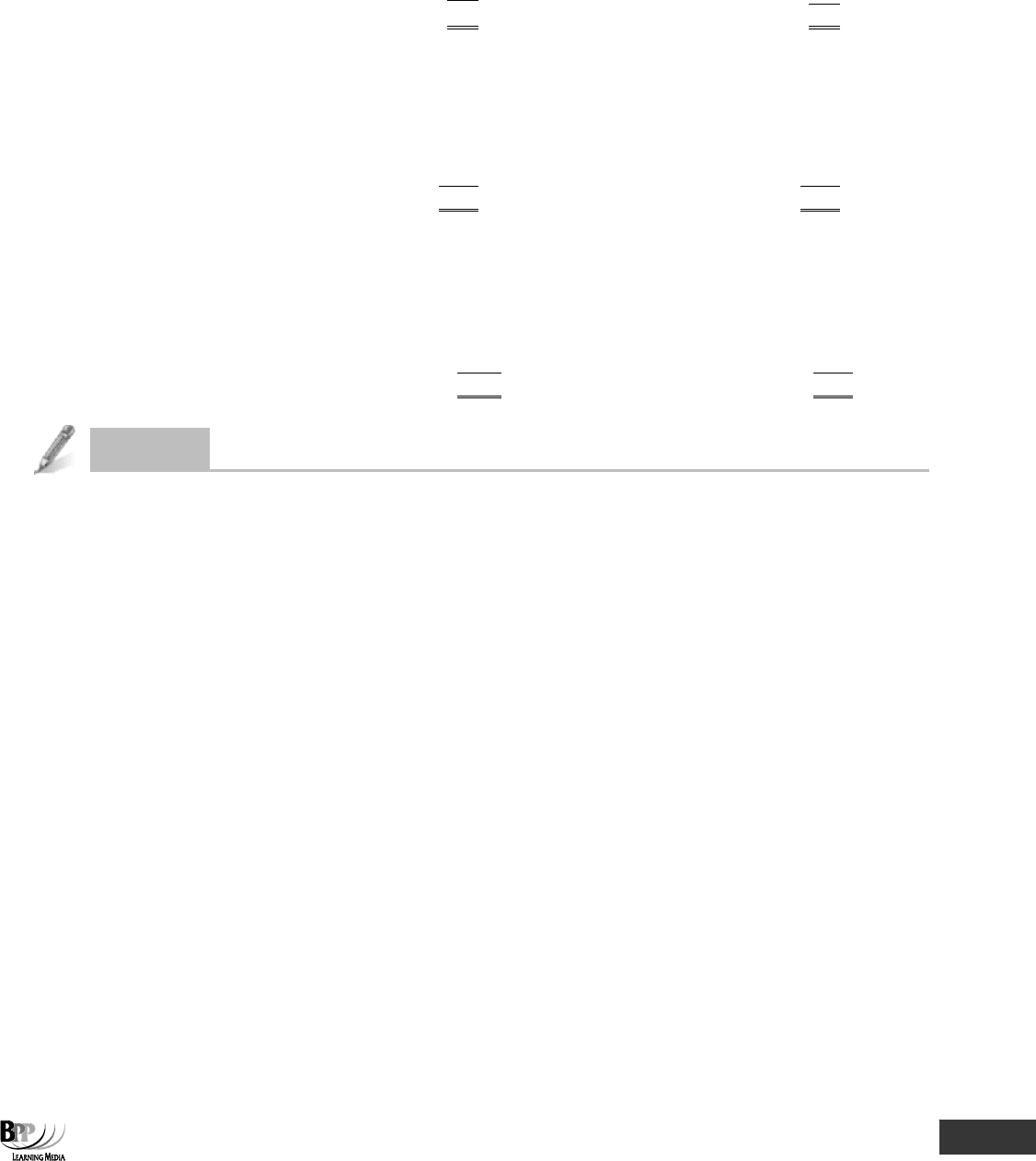

Step 1

Determine output and losses

Units

Actual output

2,750

Normal loss (10% × 3,300)

330

Abnormal loss

220

3,300

Step 2

Calculate cost per unit of output and losses

Cost of input

Expected units of output

=

−

$89,100

3,300 330

= $30 per unit

Step 3

Calculate total cost of output and losses

$

Cost of output (2,750 × $30)

82,500

Normal loss

0

Abnormal loss (220 × $30)

6,600

89,100

If you were reduced to making a calculated guess, you could have eliminated option D. This is simply the total input cost,

with no attempt to apportion some of the cost to the abnormal loss.

Option A is incorrect because it results from allocating a full unit cost to the normal loss: remember that normal loss

does not carry any of the process cost.

Option B is incorrect because it results from calculating a 10% normal loss based on output of 2,750 units (275 units

normal loss), rather than on input of 3,300 units.

Question

Abnormal gain

Zed Co makes a product Emm which goes through several processes. The following information is available for the

month of June.

Kg

Opening WIP 5,200

Closing WIP 3,500

Input 58,300

Normal loss 400

Transferred to finished goods 59,900

What was the abnormal gain in June?

A 260 kg

B 300 kg

C 400 kg

D 560 kg

292433 www.ebooks2000.blogspot.com

272

12: Process costing ⏐ Part D Costing and accounting systems

Answer

B

Process account

Dr

Cr

Opening WIP

5,200

Output

59,900

Input

58,300

Normal loss

400

Abnormal gain

Closing WIP

3,500

63,800

63,800

The abnormal gain is the balancing figure. 63,800 – 5,200 – 58,300 = 300

4 Accounting for scrap

Scrap is 'discarded material having some value'. CIMA Official Terminology

4.1 Basic rules for accounting for scrap

(a) Revenue from scrap is treated, not as an addition to sales revenue, but as a reduction in costs.

The valuation of normal loss is either at scrap value or nil. It is conventional for the scrap value of normal loss to be

deducted from the cost of materials before a cost per equivalent unit is calculated.

(b) The scrap value of normal loss is therefore used to reduce the material costs of the process.

DEBIT Scrap account

CREDIT Process account

with the scrap value of the normal loss.

Abnormal losses and gains never affect the cost of good units of production. The scrap value of abnormal losses is not

credited to the process account, and the abnormal loss and gain units carry the same full cost as a good unit of

production.

(c) The scrap value of abnormal loss is used to reduce the cost of abnormal loss.

DEBIT Scrap account

CREDIT Abnormal loss account

with the scrap value of abnormal loss, which therefore reduces the write-off of cost to the income

statement.

(d) The scrap value of abnormal gain arises because the actual units sold as scrap will be less than the scrap

value of normal loss. Because there are fewer units of scrap than expected, there will be less revenue from

scrap as a direct consequence of the abnormal gain. The abnormal gain account should therefore be

debited with the scrap value.

FA

S

T F

O

RWAR

D

FAST FORWARD

Key term

293433 www.ebooks2000.blogspot.com

Part D Costing and accounting systems ⏐ 12: Process costing

273

DEBIT Abnormal gain account

CREDIT Scrap account

with the scrap value of abnormal gain.

(e) The scrap account is completed by recording the actual cash received from the sale of scrap.

DEBIT Cash received

CREDIT Scrap account

with the cash received from the sale of the actual scrap.

The same basic principle therefore applies that only normal losses should affect the cost of the good output. The scrap

value of normal loss only is credited to the process account. The scrap values of abnormal losses and gains are

analysed separately in the abnormal loss or gain account.

4.2 Example: scrap and abnormal loss or gain

A factory has two production processes. Normal loss in each process is 10% and scrapped units sell for $0.50 each

from process 1 and $3 each from process 2. Relevant information for costing purposes relating to period 5 is as follows.

Direct materials added:

Process 1 Process 2

units 2,000 1,250

cost $8,100 $1,900

Direct labour $4,000 $10,000

Production overhead 150% of direct labour cost 120% of direct labour cost

Output to process 2/finished goods 1,750 units 2,800 units

Actual production overhead $17,800

Required

Prepare the accounts for process 1, process 2, scrap, abnormal loss or gain.

Solution

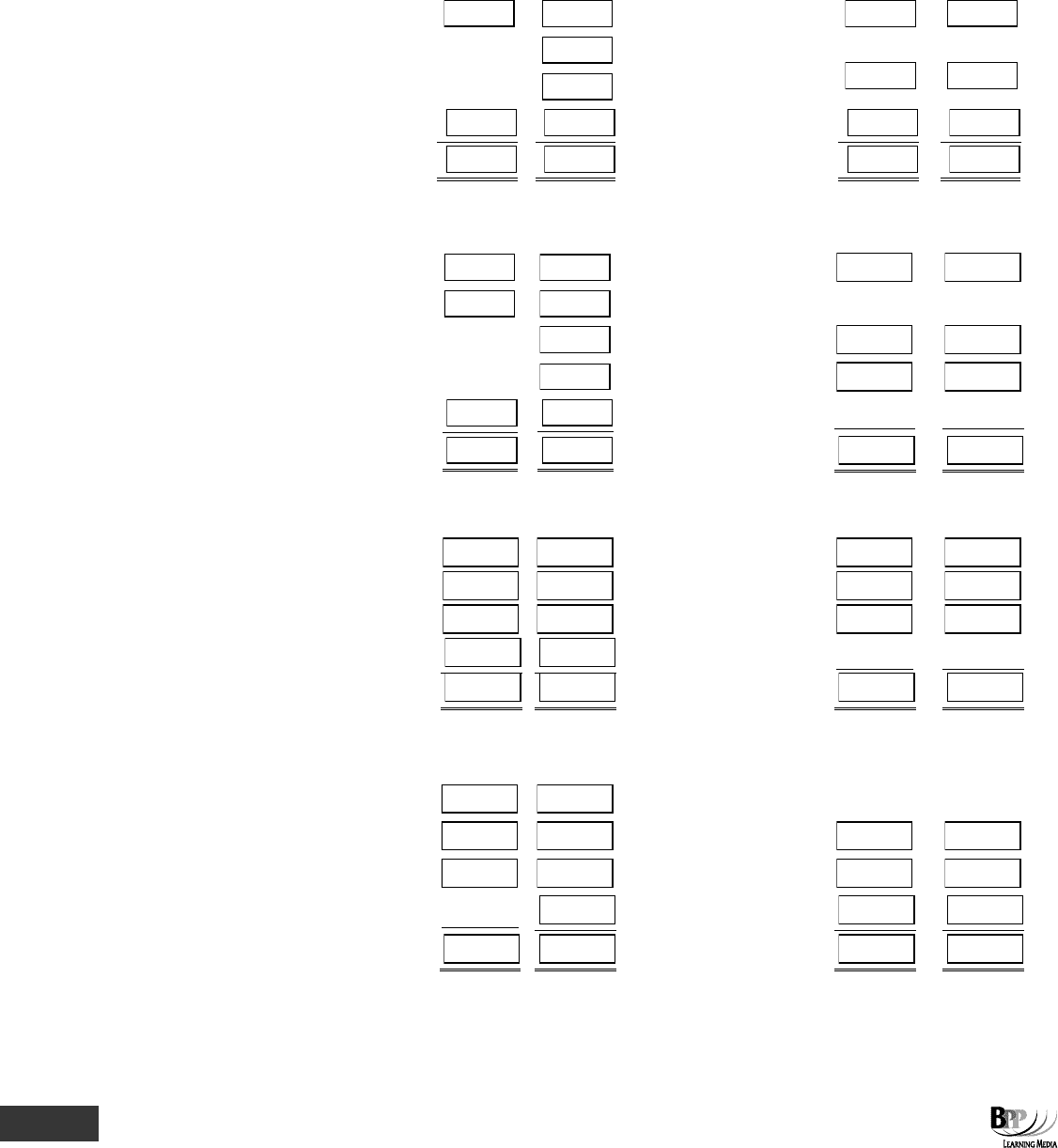

Step 1

Determine output and losses

Process 1

Process 2

Units

Units

Output

1,750

2,800

Normal loss (10% of input)

200

300

Abnormal loss

50

-

Abnormal gain

-

(100

)

2,000

3,000

*

* 1,750 units from Process 1 + 1,250 units input to process.

Important!

294433 www.ebooks2000.blogspot.com

274

12: Process costing ⏐ Part D Costing and accounting systems

Step 2

Calculate cost per unit of output and losses

Process 1

Process 2

$

$

Cost of input

– material

8,100

1,900

– from Process 1

–

(1,750 × $10)

17,500

– labour

4,000

10,000

– overhead

(150% × $4,000)

6,000

(120% × $10,000)

12,000

18,100

41,400

Less: scrap value of

normal loss

(200 × $0.50)

(100

)

(300 × $3)

(900)

18,000

40,500

Expected output

90% of 2,000 1,800

90% of 3,000 2,700

Cost per unit

$18,000 ÷ 1,800 $10

$40,500 ÷ 2,700

$15

Step 3

Calculate total cost of output and losses

Process 1

Process 2

$

$

Output (1,750 × $10)

17,500

(2,800 × $15)

42,000

Normal loss (200 × $0.50)*

100

(300 × $3)*

900

Abnormal loss (50 × $10)

500

–

18,100

42,900

Abnormal gain

–

(100 × $15)

(1,500

)

18,100

41,400

* Remember that normal loss is valued at scrap value only.

Step 4

Complete accounts

PROCESS 1 ACCOUNT

Units $ Units $

Direct material 2,000 8,100 Scrap a/c (normal loss) 200 100

Direct labour 4,000 Process 2 a/c 1,750 17,500

Production

Abnormal loss a/c

50

500

overhead a/c

6,000

2,000

18,100

2,000

18,100

PROCESS 2 ACCOUNT

Units

$

Units

$

Direct materials

From process 1

1,750

17,500

Scrap a/c (normal loss)

300

900

Added materials

1,250

1,900

Finished goods a/c

2,800

42,000

Direct labour

10,000

Production o'hd

12,000

3,000

41,400

Abnormal gain

100

1,500

3,100

42,900

3,100

42,900

295433 www.ebooks2000.blogspot.com

Part D Costing and accounting systems ⏐ 12: Process costing

275

ABNORMAL LOSS ACCOUNT

$ $

Process 1 (50 units) 500 Scrap a/c: sale of scrap of

extra loss (50 units) 25

Income statement

475

500

500

ABNORMAL GAIN ACCOUNT

$

$

Scrap a/c (loss of scrap revenue

Process 2 abnormal gain

1,500

due to abnormal gain,

(100 units)

100 units × $3)

300

Income statement

1,200

1,500

1,500

SCRAP ACCOUNT

$ $

Scrap value of normal loss Cash a/c - cash received

Process 1 (200 units) 100 Loss in process 1 (250 units) 125

Process 2 (300 units) 900 Loss in process 2 (200 units) 600

Abnormal loss a/c (process 1)

25

Abnormal gain a/c (process 2)

300

1,025

1,025

Question

Process accounts

Parks Co operates a processing operation involving two stages, the output of process 1 being passed to process 2. The

process costs for period 3 were as follows.

Process 1

Material 3,000 kg at $0.25 per kg

Labour $120

Process 2

Material 2,000 kg at $0.40 per kg

Labour $84

General overhead for period 3 amounted to $357 and is absorbed into process costs at a rate of 375% of direct labour

costs in process 1 and 496% of direct labour costs in process 2.

The normal output of process 1 is 80% of input and of process 2, 90% of input. Waste matter from process 1 is sold for

$0.20 per kg and that from process 2 for $0.30 per kg.

The output for period 3 was as follows.

Process 1 2,300 kgs

Process 2 4,000 kgs

There was no inventory of work in progress at either the beginning or the end of the period and it may be assumed that

all available waste matter had been sold at the prices indicated.

296433 www.ebooks2000.blogspot.com

276

12: Process costing ⏐ Part D Costing and accounting systems

Required

Show how the foregoing data would be recorded in process, scrap and abnormal loss/gain accounts by completing the

proformas below. (Hint. Not all boxes require entries.)

PROCESS 1 ACCOUNT

kg $ kg $

Material

Normal loss to scrap a/c

Labour

General overhead

Production transferred to

process 2

Abnormal gain account

Abnormal loss a/c

PROCESS 2 ACCOUNT

kg $ kg $

Transferred from process 1

Normal loss to scrap a/c

Material added

Production transferred to

Labour

finished inventory

General overhead

Abnormal loss

Abnormal gain

SCRAP ACCOUNT

kg $ kg $

Normal loss (process 1)

Abnormal gain (process 1)

Normal loss (process 2)

Abnormal gain (process 2)

Abnormal loss (process 1)

Cash

Abnormal loss (process 2)

ABNORMAL LOSS AND GAIN ACCOUNT

kg $ kg $

Process 1 (loss)

Scrap value of abnormal

Process 2 (loss)

loss

Scrap value of abnormal gain

Process 1 (gain)

Income statement

Process 2 (gain)

297433 www.ebooks2000.blogspot.com

Part D Costing and accounting systems ⏐ 12: Process costing

277

Answer

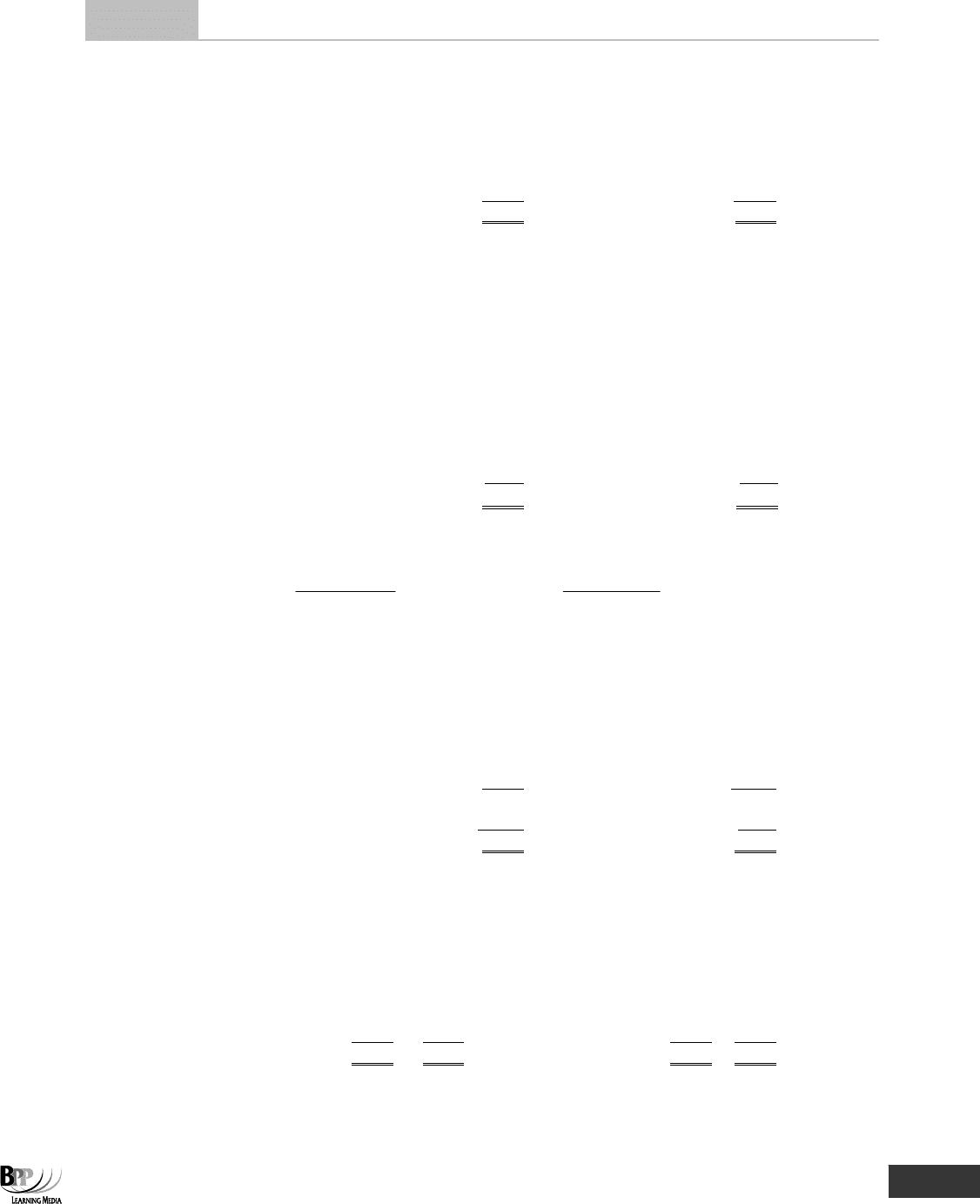

Step 1

Determine output and losses

Process 1

Process 2

kgs

kgs

Output

2,300

4,000

Normal loss (20% of 3,000 kgs)

600

(10% of 4,300)

430

Abnormal loss

100

–

Abnormal gain

–

(130

)

3,000

4,300

*

* From process 1 (2,300 kgs) + 2,000 kgs added

Step 2

Determine cost per unit of output and losses

Process 1

Process 2

$

$

Material (3,000 × $0.25)

750

(2,000 × $0.40)

800

From process 1

×

(2,300 × $0.50)

1,150

Labour

120

84

Overhead (375% × $120)

450

(496% × $84)

417

Less: scrap value of normal loss

(600 × $0.20)

(120

)

(430 × $0.3)

(129)

1,200

2,322

Expected output

3,000 × 80%

2,400

4,300 × 90%

3,870

Cost per unit

$

$1,320 $120

3,000 600

−

−

⎛⎞

⎜⎟

⎝⎠

$0.50

$2,451 $129

4,300 430

−

−

⎛⎞

⎜⎟

⎝⎠

$0.60

Step 3

Determine total cost of output and losses

Process 1

Process 2

$

$

Output (2,300 × $0.50)

1,150

(4,000 × $0.60)

2,400

Normal loss (scrap)

(600 × $0.20)

120

(430 × $0.30)

129

Abnormal loss (100 × $0.50)

50

–

1,320

2,529

Abnormal gain

–

(130 × $0.60)

(78

)

1,320

2,451

Step 4

Complete accounts

PROCESS 1 ACCOUNT

kg

$

kg

$

Material

3,000

750

Normal loss to scrap a/c

Labour

120

(20%)

600

120

General overhead

450

Production transferred to

process 2

2,300

1,150

Abnormal loss a/c

100

50

3,000

1,320

3,000

1,320

298433 www.ebooks2000.blogspot.com

278

12: Process costing ⏐ Part D Costing and accounting systems

PROCESS 2 ACCOUNT

kg

$

kg

$

Transferred from

process 1

2,300

1,150

Normal loss to scrap a/c

Material added

2,000

800

(10%)

430

129

Labour

84

Production transferred to

General overhead

417

finished inventory

4,000

2,400

4,300

2,451

Abnormal gain

130

78

4,430

2,529

4,430

2,529

SCRAP ACCOUNT

kg

$

kg

$

Normal loss (process 1)

600

120

Abnormal gain (process 2)

130

39

Normal loss (process 2)

430

129

Cash

1,000

230

Abnormal loss

(process 1)

100

20

1,130

269

1,130

269

ABNORMAL LOSS AND GAIN ACCOUNT

kg

$

kg

$

Process 1 (loss) 100 50 Scrap value of

Scrap value of abnormal abnormal loss 100 20

gain 130 39 Process 2 (gain) 130 78

Income statement

9

230

98

230

98

(Note. In this answer, a single account has been prepared for abnormal loss/gain. It is also possible to separate this

single account into two separate accounts, one for abnormal gain and one for abnormal loss.)

5 Valuing closing work in progress

When units are partly completed at the end of a period (ie when there is closing work in progress) it is necessary to

calculate the equivalent units of production in order to determine the cost of a completed unit.

In the examples we have looked at so far we have assumed that opening and closing inventories of work in process have

been nil. We must now look at more realistic examples and consider how to allocate the costs incurred in a period

between completed output (ie finished units) and partly completed closing inventory.

Some examples will help to illustrate the problem, and the techniques used to share out (apportion) costs between

finished output and closing work in progress.

5.1 Example: valuation of closing inventory

Trotter Co is a manufacturer of processed goods. In March 20X3, in one process, there was no opening inventory, but

5,000 units of input were introduced to the process during the month, at the following cost.

$

Direct materials

16,560

Direct labour

7,360

Production overhead

5,520

29,440

FA

S

T F

O

RWAR

D

299433 www.ebooks2000.blogspot.com

Part D Costing and accounting systems ⏐ 12: Process costing

279

Of the 5,000 units introduced, 4,000 were completely finished during the month and transferred to the next process.

Closing inventory of 1,000 units was only 60% complete with respect to materials and conversion costs.

Solution

(a) The problem in this example is to divide the costs of production ($29,440) between the finished output of 4,000

units and the closing inventory of 1,000 units. It is argued, with good reason, that a division of costs in

proportion to the number of units of each (4,000:1,000) would not be 'fair' because closing inventory has not

been completed, and has not yet 'received' its full amount of materials and conversion costs, but only 60% of the

full amount. The 1,000 units of closing inventory, being only 60% complete, are the equivalent of 600 fully

worked units.

(b) To apportion costs fairly and proportionately, units of production must be converted into the equivalent of

completed units, ie into equivalent units of production.

Equivalent units are 'notional whole units representing incomplete work. Used to apportion costs between work in

progress and completed output …' CIMA Official Terminology

Step 1

Determine output

For this step in our framework we need to prepare a statement of equivalent units.

STATEMENT OF EQUIVALENT UNITS

Total

Equivalent

units

Completion

units

Fully worked units

4,000

100%

4,000

Closing inventory

1,000

60%

600

5,000

4,600

Step 2

Calculate cost per unit of output, and WIP

For this step in our framework we need to prepare a statement of costs per equivalent unit because

equivalent units are the basis for apportioning costs.

STATEMENT OF COSTS PER EQUIVALENT UNIT

Total costs

Equivalent units

=

$29,440

4,600

Cost per equivalent unit $6.40

Step 3

Calculate total cost of output and WIP

For this step in our framework a statement of evaluation may now be prepared, to show how the costs

should be apportioned between finished output and closing inventory.

STATEMENT OF EVALUATION

Equivalent

Cost per equivalent

Item

units

unit

Valuation

$

Fully worked units

4,000

$6.40

25,600

Closing inventory

600

$6.40

3,840

4,600

29,440

Key term

300433 www.ebooks2000.blogspot.com