CIMA - C1 Fundamentals of Management Accounting

Подождите немного. Документ загружается.

280

12: Process costing ⏐ Part D Costing and accounting systems

Step 4

Complete accounts

The process account would be shown as follows.

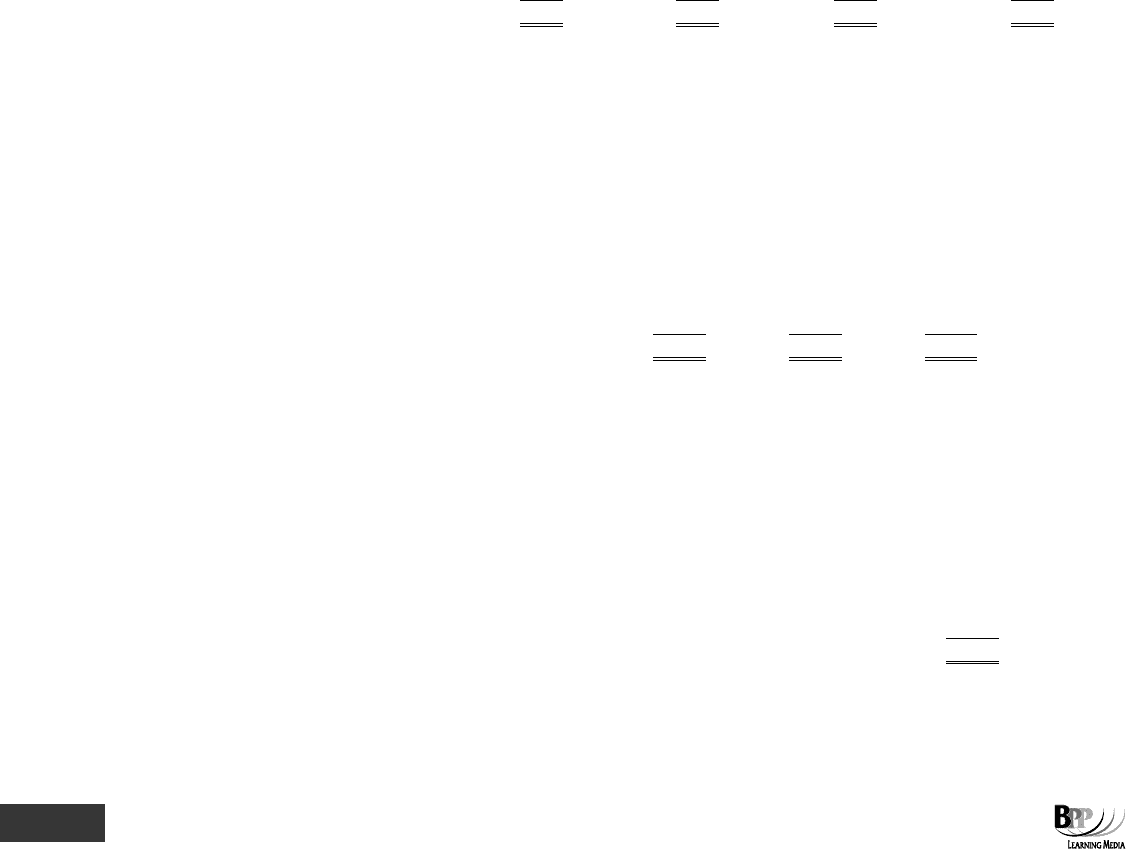

PROCESS ACCOUNT

Units

$

Units

$

Direct materials

5,000

16,560

Output to next process

4,000

25,600

Direct labour

7,360

Closing inventory c/f

1,000

3,840

Production o'hd

5,520

5,000

29,440

5,000

29,440

5.2 A few hints on preparing accounts

When preparing a process account, it might help to make the entries as follows.

(a) Enter the units first. The units columns are simply memorandum columns, but they help you to make sure

that there are no units unaccounted for (for example as loss).

(b) Enter the costs of materials, labour and overheads next. These should be given to you.

(c) Enter your valuation of finished output and closing inventory next. The value of the credit entries should,

of course, equal the value of the debit entries.

5.3 Different rates of input

In many industries, materials, labour and overhead may be added at different rates during the course of production.

(a) Output from a previous process (for example the output from process 1 to process 2) may be introduced

into the subsequent process all at once, so that closing inventory is 100% complete in respect of these

materials.

(b) Further materials may be added gradually during the process, so that closing inventory is only partially

complete in respect of these added materials.

(c) Labour and overhead may be 'added' at yet another different rate. When production overhead is absorbed

on a labour hour basis, however, we should expect the degree of completion on overhead to be the same

as the degree of completion on labour.

When this situation occurs, equivalent units, and a cost per equivalent unit, should be calculated separately for each

type of material, and also for conversion costs.

5.4 Example: equivalent units and different degrees of completion

Suppose that Shaker Co is a manufacturer of processed goods, and that results in process 2 for April 20X3 were as

follows.

Opening inventory nil

Material input from process 1 4,000 units

Costs of input:

$

Material from process 1 6,000

Added materials in process 2 1,080

Conversion costs 1,720

Output is transferred into the next process, process 3.

301433 www.ebooks2000.blogspot.com

Part D Costing and accounting systems ⏐ 12: Process costing

281

Closing work in process amounted to 800 units, complete as to:

%

Process 1 material 100

Added materials 50

Conversion costs 30

Required

Prepare the account for process 2 for April 20X3.

Solution

Step 1

Determine output and losses

STATEMENT OF EQUIVALENT UNITS (OF PRODUCTION IN THE PERIOD)

Equivalent units of production

Process 1

Added

Labour and

Input

Output

Total

material

materials

overhead

Units

Units

Units

%

Units

%

Units

%

4,000

Completed

3,200

3,200

100

3,200

100

3,200

100

production

Closing inventory

800

800

100

400

50

240

30

4,000

4,000

4,000

3,600

3,440

Step 2

Calculate cost per unit of output, losses and WIP

STATEMENT OF COST (PER EQUIVALENT UNIT)

Equivalent production

Cost per

Input

Cost

in units

unit

$

$

Process 1 material

6,000

4,000

1.50

Added materials

1,080

3,600

0.30

Labour and overhead

1,720

3,440

0.50

8,800

2.30

Step 3

Calculate total cost of output, losses and WIP

STATEMENT OF EVALUATION (OF FINISHED WORK AND CLOSING INVENTORIES)

Number of

Cost per

equivalent

equivalent

Production

Cost element

units

unit

Total

Cost

$

$

$

Completed

production

3,200

2.30

7,360

Closing inventory:

process 1 material

800

1.50

1,200

added material

400

0.30

120

labour and

240

0.50

120

overhead

1,440

8,800

302433 www.ebooks2000.blogspot.com

282

12: Process costing ⏐ Part D Costing and accounting systems

Step 4

Complete accounts

PROCESS ACCOUNT

Units

$

Units

$

Process 1 material

4,000

6,000

Process 3 a/c

3,200

7,360

Added material

1,080

(finished output)

Conversion costs

1,720

Closing inventory c/f

800

1,440

4,000

8,800

4,000

8,800

5.5 Closing work in progress and losses

The previous sections have dealt separately with the following.

(a) The treatment of loss and scrap.

(b) The use of equivalent units as a basis for apportioning costs between units of output and units of closing

inventory.

We must now look at a situation where both problems occur together. We shall begin with an example where loss has no

scrap value.

The rules are as follows.

(a) Costs should be divided between finished output, closing inventory and abnormal loss/gain using

equivalent units as a basis of apportionment.

(b) Units of abnormal loss/gain are often taken to be one full equivalent unit each, and are valued on this

basis, ie they carry their full 'share' of the process costs.

(c) Abnormal loss units are an addition to the total equivalent units produced but abnormal gain units are

subtracted in arriving at the total number of equivalent units produced.

(d) Units of normal loss are valued at zero equivalent units, ie they do not carry any of the process costs.

5.6 Example: changes in inventory level and losses

The following data have been collected for a process.

Opening inventory none Output to finished goods 2,000 units

Input units 2,800 units Closing inventory 450 units, 70% complete

Cost of input $16,695 Total loss 350 units

Normal loss 10%; nil scrap value

Required

Prepare the process account for the period.

303433 www.ebooks2000.blogspot.com

Part D Costing and accounting systems ⏐ 12: Process costing

283

Solution

Step 1

Determine output and losses

STATEMENT OF EQUIVALENT UNITS

Equivalent units

of work

done this

Total units

period

Completely worked units

2,000

(× 100%)

2,000

Closing inventory

450

(× 70%)

315

Normal loss

280

0

Abnormal loss

70

(× 100%)

70

2,800

2,385

Step 2

Calculate cost per unit of output, losses and WIP

STATEMENT OF COST PER EQUIVALENT UNIT

Costs incurred

Equivalent units of work done

=

$16,695

2,385

Cost per equivalent unit = $7

Step 3

Calculate total cost of output, losses and WIP

STATEMENT OF EVALUATION

Equivalent

units $

Completely worked units 2,000 14,000

Closing inventory 315 2,205

Abnormal loss

70

490

2,385

16,695

Step 4

Complete accounts

PROCESS ACCOUNT

Units

$

Units

$

Opening inventory

–

–

Normal loss

280

0

Input costs

2,800

16,695

Finished goods a/c

2,000

14,000

Abnormal loss a/c

70

490

Closing inventory c/d

450

2,205

2,800

16,695

2,800

16,695

5.7 Closing work in progress, loss and scrap

When loss has a scrap value, the accounting procedures are the same as those previously described. However, if the

equivalent units are a different percentage (of the total units) for materials, labour and overhead, it is a convention that

the scrap value of normal loss is deducted from the cost of materials before a cost per equivalent unit is calculated.

304433 www.ebooks2000.blogspot.com

284

12: Process costing ⏐ Part D Costing and accounting systems

Question

Closing work in progress

Complete the process account below from the following information.(Hint. Not all boxes require entries.)

Opening inventory Nil

Input units 10,000

Input costs

Material $5,150

Labour $2,700

Normal loss 5% of input

Scrap value of units of loss $1 per unit

Output to finished goods 8,000 units

Closing inventory 1,000 units

Completion of closing inventory 80% for material

50% for labour

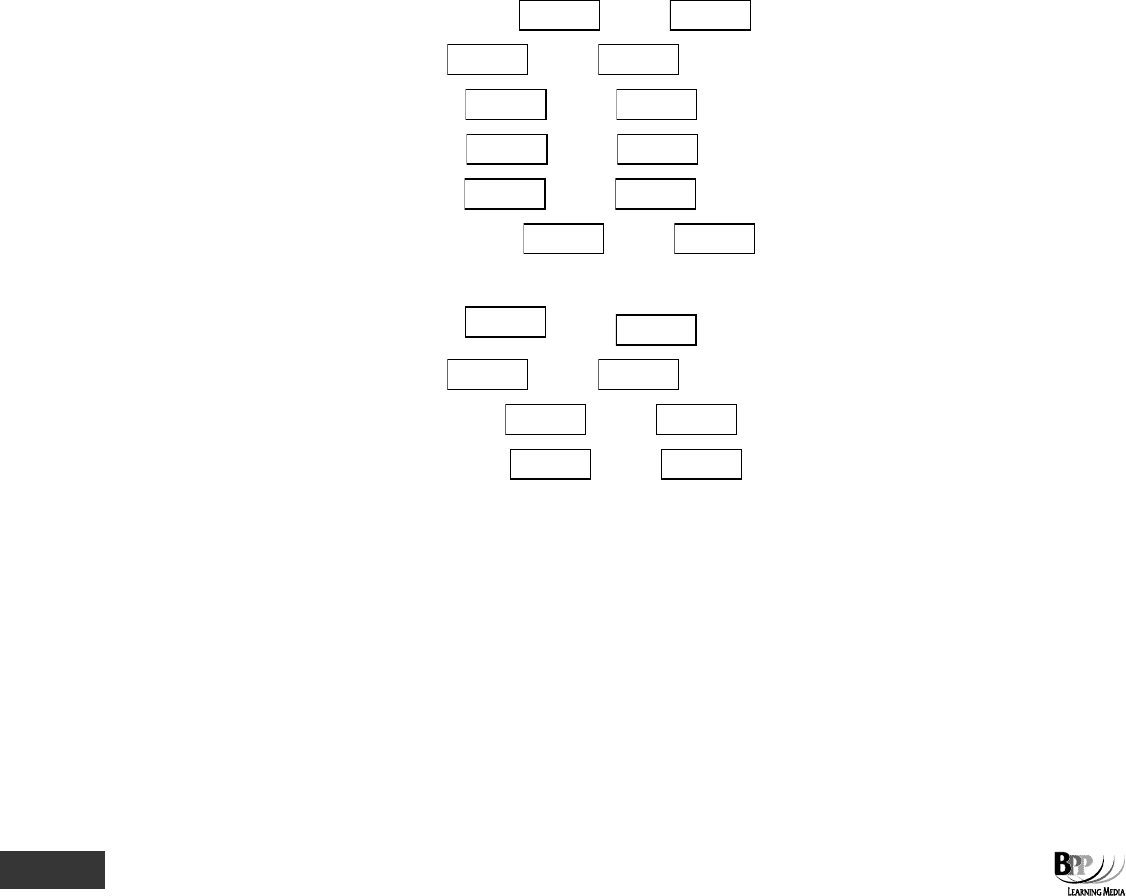

PROCESS ACCOUNT

Units $ Units $

Material

Completed production

Labour

Closing inventory

Abnormal gain

Normal loss

Abnormal loss

Answer

Step 1

Determine output and losses

STATEMENT OF EQUIVALENT UNITS

Equivalent units

Total

Material

Labour

Units

%

Units

%

Units

Completed production

8,000

100

8,000

100

8,000

Closing inventory

1,000

80

800

50

500

Normal loss

500

Abnormal loss

500

100

500

100

500

10,000

9,300

9,000

Step 2

Calculate cost per unit of output, losses and WIP

STATEMENT OF COST PER EQUIVALENT UNIT

Cost per

Equivalent

equivalent

Cost

units

unit

$

$

Material ($(5,150 – 500))

4,650

9,300

0.50

Labour

2,700

9,000

0.30

7,350

0.80

305433 www.ebooks2000.blogspot.com

Part D Costing and accounting systems ⏐ 12: Process costing

285

Step 3

Calculate total cost of output, losses and WIP

STATEMENT OF EVALUATION

Cost per

Equivalent equivalent

units

unit

Total

$

$

$

Completed production

8,000

0.80

6,400

Closing inventory: material

800

0.50

400

labour

500

0.30

150

550

Abnormal loss

500

0.80

400

7,350

Step 4

Complete accounts

PROCESS ACCOUNT

Units

$

Units

$

Material

10,000

5,150

Completed production

8,000

6,400

Labour

2,700

Closing inventory

1,000

550

Abnormal gain

0

0

Normal loss

500

500

Abnormal loss

500

400

10,000

7,850

10,000

7,850

6 Valuing opening work in progress

The weighted average cost method of valuing opening WIP makes no distinction between units of opening WIP and

new units introduced to the process during the current period.

6.1 Weighted average cost method

The weighted average cost method of inventory valuation is a inventory valuation method that calculates a weighted

average cost of units produced from both opening inventory and units introduced in the current period. (We studied this

method earlier in the Study Text in Chapter 5.)

With the weighted average cost method no distinction is made between units of opening WIP and new units introduced

to the process during the current period. The cost of opening WIP is added to costs incurred during the period, and

completed units of opening WIP are each given a value of one full equivalent unit of production.

6.2 Example: weighted average cost method

Magpie Co produces an item which is manufactured in two consecutive processes. Information relating to Process 2

during September 20X3 is as follows.

Opening inventory 800 units

Degree of completion:

%

$

process 1 materials

100

4,700

added materials

40

600

conversion costs

30

1,000

6,300

Important!

FA

S

T F

O

RWAR

D

306433 www.ebooks2000.blogspot.com

286

12: Process costing ⏐ Part D Costing and accounting systems

During September 20X3, 3,000 units were transferred from process 1 at a valuation of $18,100. Added materials cost

$9,600 and conversion costs were $11,800.

Closing inventory at 30 September 20X3 amounted to 1,000 units which were 100% complete with respect to process 1

materials and 60% complete with respect to added materials. Conversion cost work was 40% complete.

Magpie Co uses a weighted average cost system for the valuation of output and closing inventory.

Required

Prepare the Process 2 account for September 20X3.

Solution

Step 1

Determine output and losses

Opening inventory units count as a full equivalent unit of production when the weighted average cost

system is applied. Closing inventory units are assessed in the usual way.

STATEMENT OF EQUIVALENT UNITS

Equivalent units

Total

Process 1

Added

Conversion

units

material

material

costs

Output to finished goods*

2,800

(100%)

2,800

2,800

2,800

Closing inventory

1,000

(100%)

1,000

(60%)

600

(40%)

400

3,800

3,800

3,400

3,200

* 3,000 units from Process 1 minus closing inventory of 1,000 units plus opening inventory of 800 units.

Step 2

Calculate cost per unit of output and WIP

The cost of opening inventory is added to costs incurred in September 20X3, and a cost per equivalent

unit is then calculated.

STATEMENT OF COSTS PER EQUIVALENT UNIT

Process 1 Added Conversion

material materials costs

$ $ $

Opening inventory 4,700 600 1,000

Added in September 20X3

18,100

9,600

11,800

Total cost

22,800

10,200

12,800

Equivalent units 3,800 units 3,400 units 3,200 units

Cost per equivalent unit $6 $3 $4

Step 3

Calculate total cost of output and WIP

STATEMENT OF EVALUATION

Process 1

Added

Conversion

Total

material

materials

costs

cost

$

$

$

$

Output to finished goods

(2,800 units)

16,800

8,400

11,200

36,400

Closing inventory

6,000

1,800

1,600

9,400

45,800

307433 www.ebooks2000.blogspot.com

Part D Costing and accounting systems ⏐ 12: Process costing

287

Step 4

Complete accounts

PROCESS 2 ACCOUNT

Units

$

Units

$

Opening inventory b/f

800

6,300

Finished goods a/c

2,800

36,400

Process 1 a/c

3,000

18,100

Added materials

9,600

Conversion costs

11,800

Closing inventory c/f

1,000

9,400

3,800

45,800

3,800

45,800

You must be prepared to deal with assessment questions which have opening WIP, closing WIP and losses all occurring

together in the same process.

6.3 A final question

The following question involves the following process costing situations.

•

Normal loss (with and without sale of scrap)

•

Abnormal loss

•

Abnormal gain

•

Opening work in progress

•

Closing work in progress

Take time to work through this question carefully and to check your workings against the answer given below. This is an

excellent question which should help you to consolidate all of the process costing knowledge that you have acquired

while studying this chapter.

Question

Watkins Co

W Co has a financial year which ends on 30 April. It operates in a processing industry in which a single product is

produced by passing inputs through two sequential processes. A normal loss of 10% of input is expected in each

process.

The following account balances have been extracted from its ledger at 31 March 20X0.

Debit Credit

$ $

Process 1 (Materials $4,400; Conversion costs $3,744) 8,144

Process 2 (Process 1 $4,431; Conversion costs $5,250) 9,681

Abnormal loss 1,400

Abnormal gain 300

Overhead control account 250

Sales 585,000

Cost of sales 442,500

Finished goods inventory 65,000

W Co uses the weighted average method of accounting for work in process.

During April 20X0 the following transactions occurred.

Process 1 Materials input (kg, $) 4,000 kg 22,000

Labour cost $12,000

Transfer to process 2 2,400 kg

Assessment

focus point

308433 www.ebooks2000.blogspot.com

288

12: Process costing ⏐ Part D Costing and accounting systems

Process 2 Transfer from process 1 2,400 kg

Labour cost $15,000

Transfer to finished goods 2,500 kg

Overhead costs incurred amounted to $54,000

Sales to customer were $52,000

Overhead costs are absorbed into process costs on the basis of 150% of labour cost.

The losses which arise in process 1 have no scrap value: those arising in process 2 can be sold for $2 per kg.

Details of opening and closing work in process for the month of April 20X0 are as follows.

Opening Closing

Process 1 3,000 kg 3,400 kg

Process 2 2,250 kg 2,600 kg

In both processes closing work in process is fully complete as to material cost and 40% complete as to conversion cost.

Inventories of finished goods at 30 April 20X0 were valued at cost of $60,000.

Required

(a) In an account for process 1, the monetary and quantity values for:

(i) transfers to process 2 are

kgs at $

(ii) normal loss are

kgs at $

(iii) abnormal loss are

kgs at $

(iv) abnormal gain are

kgs at $

(v) WIP materials are

kgs at $

(vi) WIP conversion costs are

kgs at $

(b) In an account for process 2, the monetary and quantity values for:

(i) finished goods are

kgs at $

(ii) normal loss are

kgs at $

(iii) WIP from process 1 are

kgs at $

(iv) WIP from process 2 are

kgs at $

309433 www.ebooks2000.blogspot.com

Part D Costing and accounting systems ⏐ 12: Process costing

289

Answer

(a) Process 1

STATEMENT OF EQUIVALENT UNITS

Equivalent units

Conversion

Total units

Material costs

costs

Transfers to process 2

2,400

2,400

2,400

Closing WIP

3,400

(100%) 3,400

(40%) 1,360

Normal loss (10% × 4,000)

400

0

0

Abnormal loss

800

800

800

7,000

6,600

4,560

STATEMENT OF COSTS PER EQUIVALENT UNIT

Costs incurred

Equivalent units

= Cost per equivalent unit

∴Materials cost per equivalent unit =

+$4,400 $22,000

6,600

=

$26,400

6,600

= $4

∴ Conversion costs per equivalent unit =

++$3,744 $12,000 $18,000

4,560

=

$33,744

4,560

= $7.40

STATEMENT OF EVALUATION

Materials

Conversion cost

s

Total

$

$

$

Transfers to process 2

9,600

17,760

27,360

Abnormal loss

3,200

5,920

9,120

Closing WIP

13,600

10,064

23,664

26,400

33,744

60,144

PROCESS 1 ACCOUNT

Kg

$

Kg

$

WIP materials

3,000

4,400

Process 2

2,400

27,360

WIP conversion costs

–

3,744

Normal loss

400

–

Materials

4,000

22,000

Abnormal loss

800

9,120

Labour

–

12,000

WIP materials

3,400

13,600

Overhead

–

18,000

WIP conversion costs

–

10,064

7,000

60,144

7,000

60,144

The monetary and quantity values for:

(i) transfer to process 2 are

2,400

kgs at $

27,360

(ii) normal loss are

400

kgs at $

0

(iii) abnormal loss are

800

kgs at $

9,120

310433 www.ebooks2000.blogspot.com