CIMA - C1 Fundamentals of Management Accounting

Подождите немного. Документ загружается.

230

10: Flexible budgeting ⏐ Part C Financial planning and control

(a) In this example, the variances are meaningless for purposes of control. Costs were higher than budget because

the volume of output was also higher; variable costs would be expected to increase above the budgeted costs in

the fixed budget. There is no information to show whether control action is needed for any aspect of costs or

revenue.

(b) For control purposes, it is necessary to know the answers to questions such as the following.

(i) Were actual costs higher than they should have been to produce and sell 3,000 CLs?

(ii) Was actual revenue satisfactory from the sale of 3,000 CLs?

2.1.1 The correct approach to control

The correct approach to control is as follows.

•

Identify fixed and variable costs.

•

Produce a flexible budget based on the actual activity level.

In the previous example of W Co, let us suppose that we have the following estimates of cost behaviour.

(a) Direct materials, direct labour and maintenance costs are variable.

(b) Rent and rates and depreciation are fixed costs.

(c) Other costs consist of fixed costs of $1,600 plus a variable cost of $1 per unit made and sold.

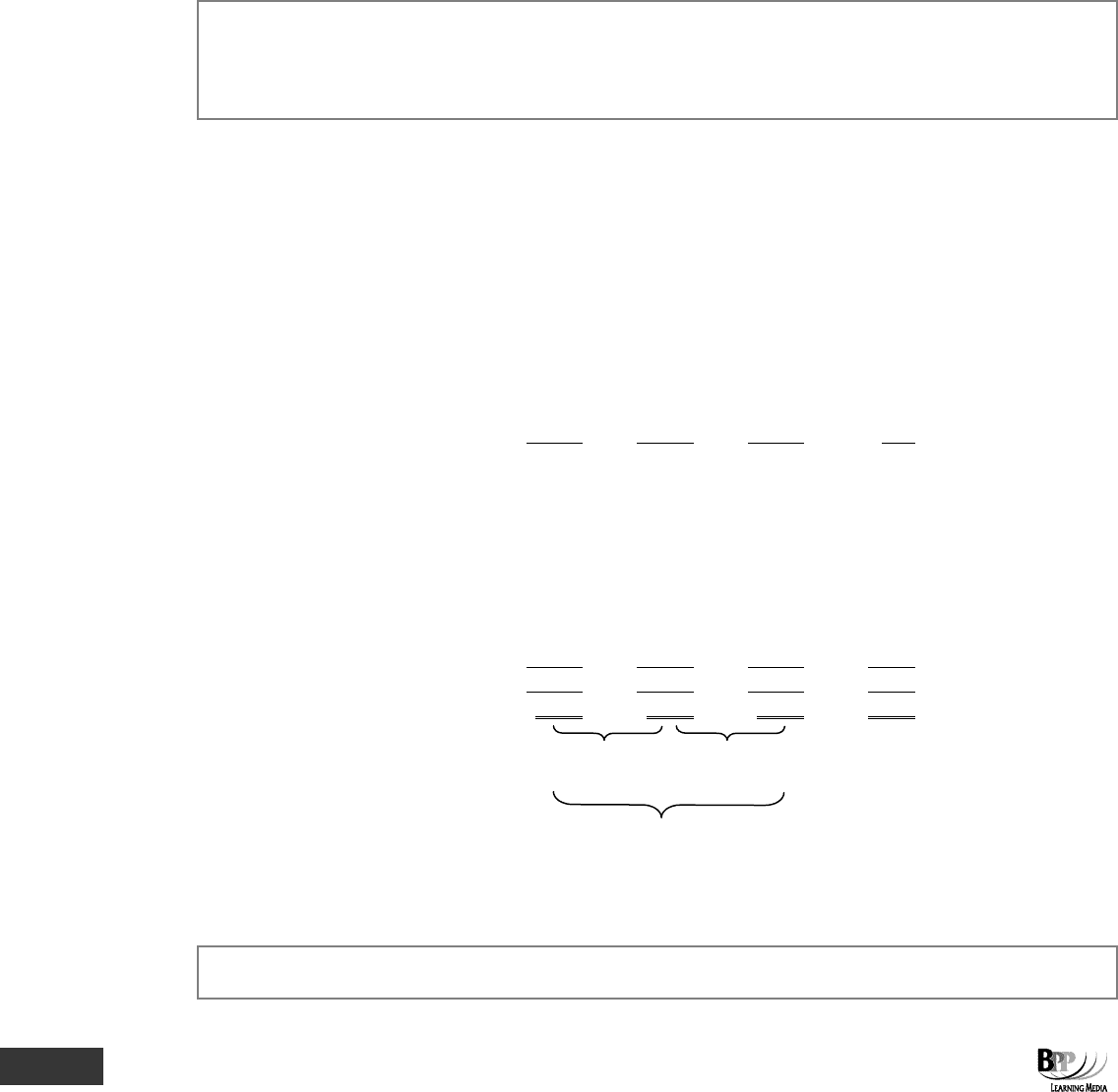

The control analysis should therefore be based on a flexible budget as follows.

Fixed Flexible Actual Budget

budget budget results variance

(a) (b) (c) (c)–(b)

Production and sales (units) 2,000 3,000 3,000

$ $ $ $

Sales revenue

20,000

30,000

30,000

0

Variable costs

Direct materials 6,000 9,000 8,500 500 (F)

Direct labour 4,000 6,000 4,500 1,500 (F)

Maintenance 1,000 1,500 1,400 100 (F)

Semi-variable costs

Other costs 3,600 4,600 5,000 400 (A)

Fixed costs

Depreciation 2,000 2,000 2,200 200 (A)

Rent and rates

1,500

1,500

1,600

100

(A)

Total costs

18,100

24,600

23,200

1,400

(F)

Profit

1,900

5,400

6,800

1,400

(F)

$3,500 (F)

Volume variance

$1,400 (F)

Expenditure variance

$4,900 (F)

Total variance

Notice that the total variance has not altered. It is still $4,900 (F) as in Section 2.1. The flexible budget comparison

merely analyses the total variance into two separate components.

Variances are calculated by comparing actual results and the flexible budget, not actual results and the original budget.

Important!

Important!

251433 www.ebooks2000.blogspot.com

Part C Financial planning and control ⏐ 10: Flexible budgeting

231

2.1.2 Interpretation of the control statement

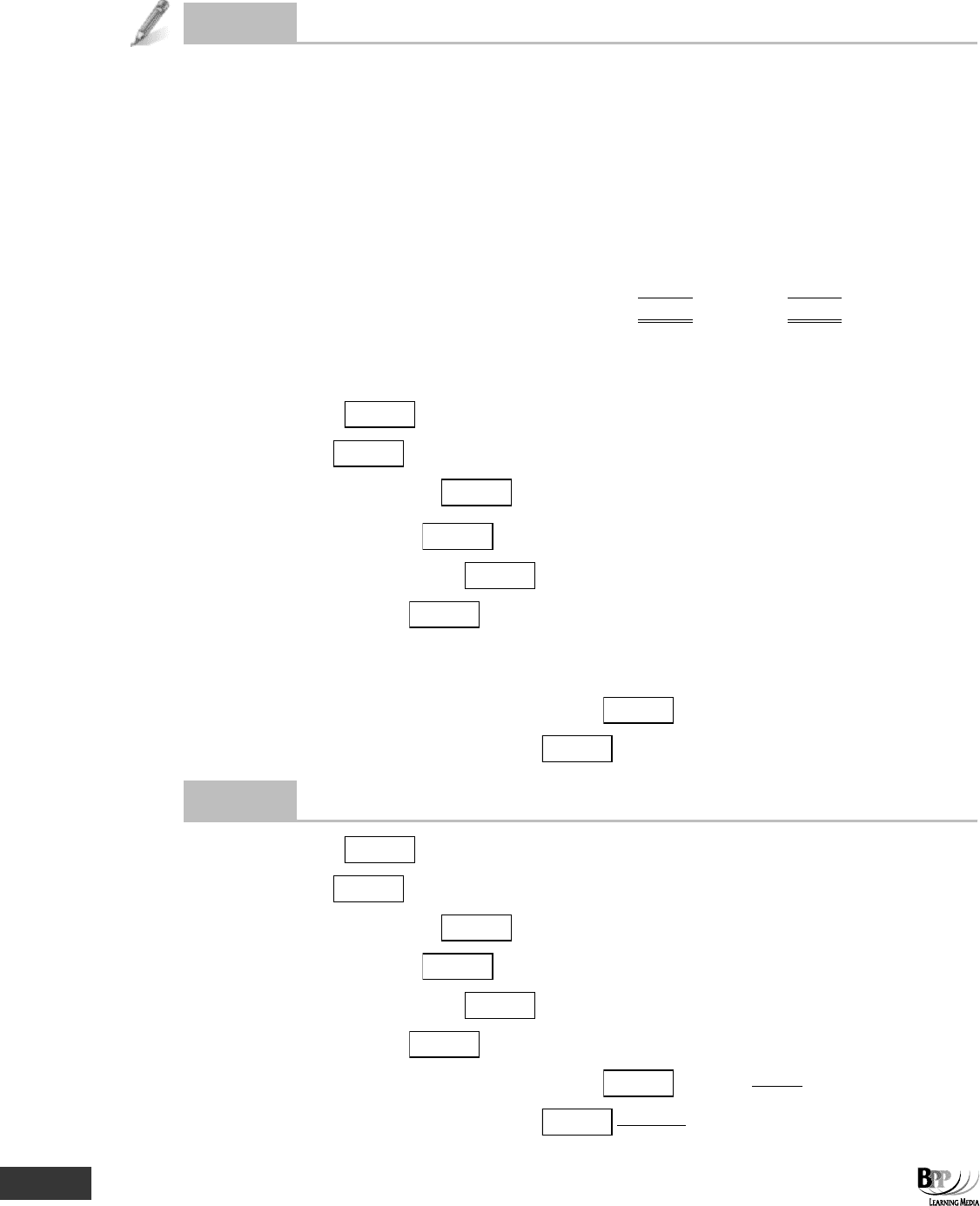

We can analyse the above as follows.

(a) In selling 3,000 units the expected profit should have been, not the fixed budget profit of $1,900, but the

flexible budget profit of $5,400. Instead, actual profit was $6,800 ie $1,400 more than we should have

expected. This is the $1,400 favourable expenditure variance. The reason for this $1,400 improvement is

that, given output and sales of 3,000 units, overall costs were lower than expected (and sales revenue was

exactly as expected). For example the direct material cost was $500 lower than expected.

(b) Another reason for the improvement in profit above the fixed budget profit is the sales volume. W Co sold

3,000 units of CL instead of 2,000, with the following result.

$

$

Budgeted sales revenue increased by

10,000

Budgeted variable costs increased by:

direct materials

3,000

direct labour

2,000

maintenance

500

variable element of other costs

1,000

Budgeted fixed costs are unchanged

6,500

Budgeted profit increased by

3,500

Budgeted profit was therefore increased by $3,500 because sales volume increased. This is the $3,500

favourable volume variance.

(c) A full variance analysis statement would be as follows.

$

$

Fixed budget profit

1,900

Variances

Sales volume

3,500 (F)

Direct materials cost

500 (F)

Direct labour cost

1,500 (F)

Maintenance cost

100 (F)

Other costs

400 (A)

Depreciation

200 (A)

Rent and rates

100

(A)

Total expenditure variance

1,400

(F)

Actual profit

6,800

If management believes that any of these variances are large enough to justify it, they will investigate the reasons for

them to see whether any corrective action is necessary.

Important!

252433 www.ebooks2000.blogspot.com

232

10: Flexible budgeting ⏐ Part C Financial planning and control

Question

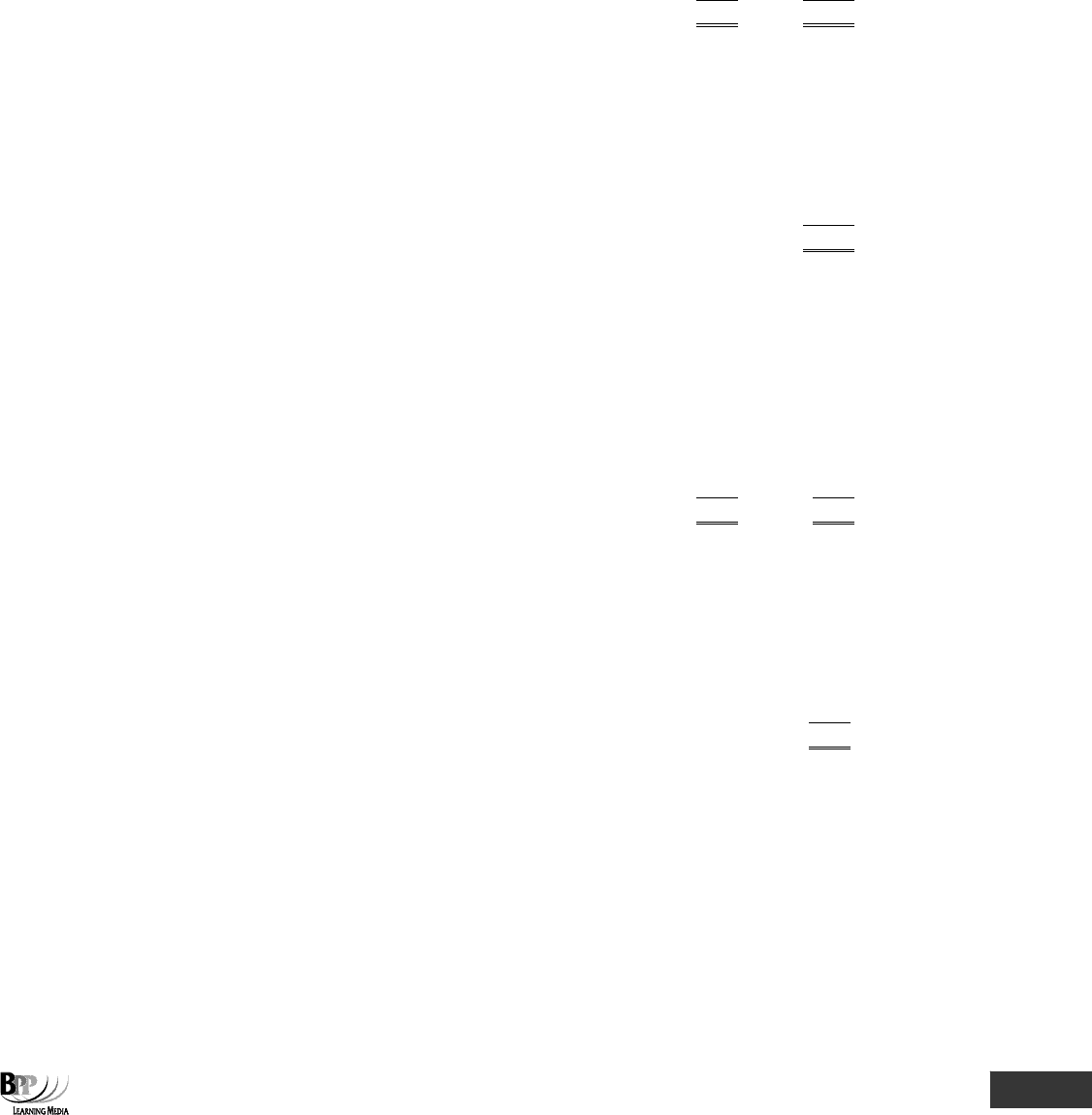

Budget cost allowances

WL Co manufactures and sells a single product, R. Since the R is highly perishable, no inventories are held at any time.

WL Co's management uses a flexible budgeting system to control costs. Extracts from the flexible budget are as follows.

Output and sales (units)

4,000

5,500

Budget cost allowances

$

$

Direct material

16,000

22,000

Direct labour

20,000

24,500

Variable production overhead

8,000

11,000

Fixed production overhead

11,000

11,000

Selling and distribution overhead

8,000

9,500

Administration overhead

7,000

7,000

Total expenditure

70,000

85,000

Production and sales of product R amounted to 5,100 units during period 5.

The total budget cost allowances in the flexible budget for period 5 will be:

(a) Direct material $

(b) Direct labour $

(c) Variable production overhead $

(d) Fixed production overhead $

(e) Selling and distribution overhead $

(f) Administration overhead $

(g) Production and sales of product R in period 6 amounted to 5,500 units. Budgeted output for the period was 4,000

units. Actual total expenditure was $82,400.

(i) The total expenditure variance for period 6 was $

favourable/adverse (delete as necessary)

(ii) The volume variance for period 6 was $

favourable/adverse (delete as necessary)

Answer

(a) Direct material $

20,400

(b) Direct labour $

23,300

(c) Variable production overhead $

10,200

(d) Fixed production overhead $

11,000

(e) Selling and distribution overhead $

9,100

(f) Administration overhead $

700

(g) (i) The total expenditure variance for period 6 was $

2,600

favourable/adverse

(ii) The volume variance for period 6 was $

15,000

favourable/adverse

253433 www.ebooks2000.blogspot.com

Part C Financial planning and control ⏐ 10: Flexible budgeting

233

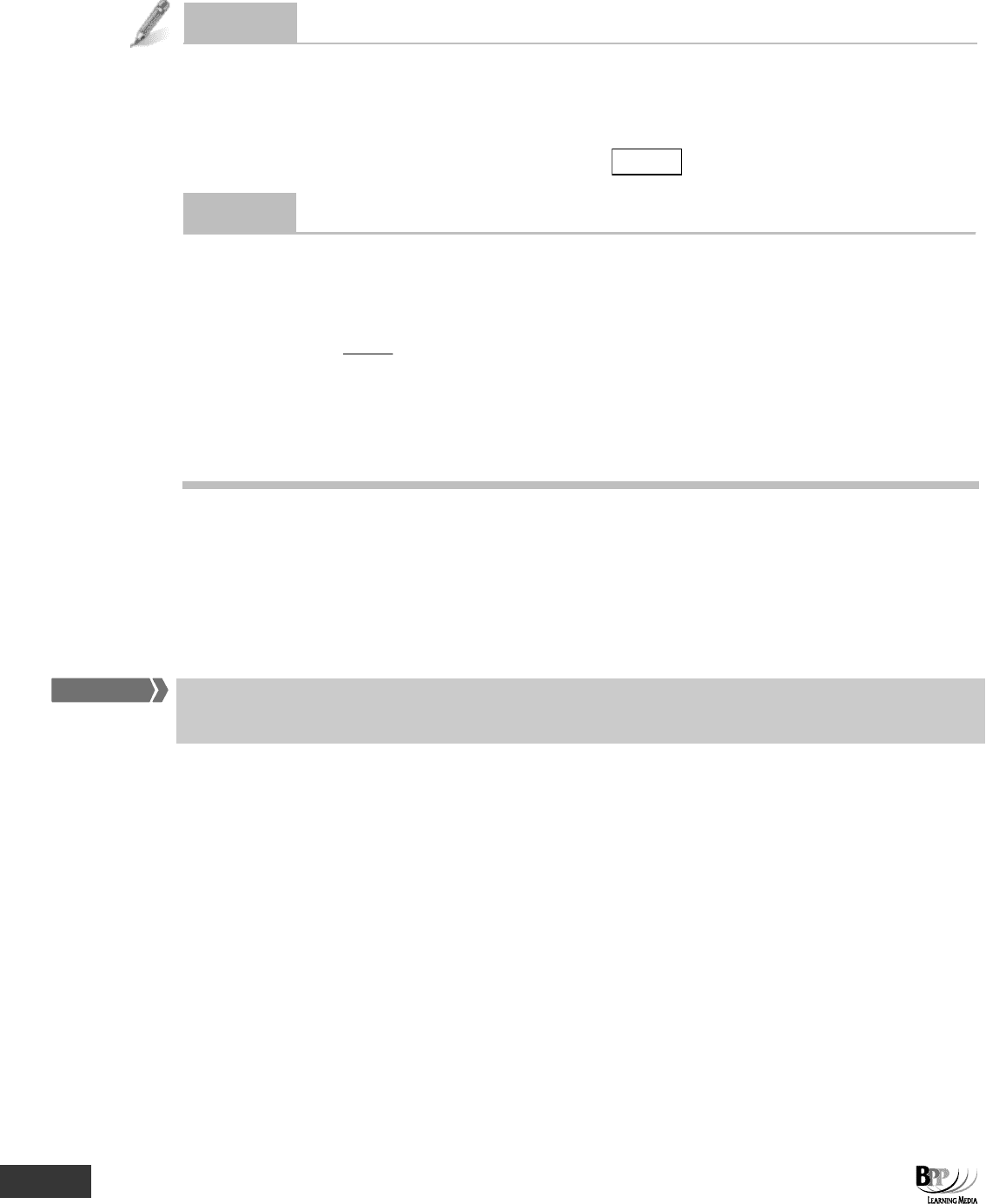

Workings

(a) Direct material is a variable cost of $16,000/4,000 = $4 per unit

Budget cost allowance for 5,100 units = 5,100 × $4 = $20,400

(b) Direct labour is a semi-variable cost which can be analysed using the high-low method.

Output

Units

$

High

5,500

24,500

Low

4,000

20,000

Change

1,500

4,500

Variable cost per unit = $4,500/1,500 = $3

Substituting in high output, fixed cost = $24,500 – (5,500 × $3)

= $8,000

Budget cost allowance for 5,100 units:

$

Variable cost = 5,100 × $3

15,300

Fixed cost

8,000

23,300

(c) Variable production overhead per unit = $8,000/4,000 = $2 per unit

Budget cost allowance for 5,100 units = 5,100 × $2 = $10,200

(d) Fixed production overhead cost allowance is fixed at $11,000.

(e) Selling and distribution is a semi-variable cost which can be analysed using the high-low method.

Output

Units

$

High

5,500

9,500

Low

4,000

8,000

Change

1,500

1,500

Variable cost per unit = $1,500/1,500 = $1

Substituting in high output, fixed cost = $9,500 – (5,500 × $1)

= $4,000

Budget cost allowance for 5,100 units:

$

Variable cost = 5,100 × $1

5,100

Fixed cost

4,000

9,100

(f) Administration overhead cost allowance is fixed at $7,000.

(g) The budgeted and actual output volumes correspond to the two activity levels provided in the question data. The

total budget cost allowance for each activity level can be used as the basis for the variance calculations.

(i) Expenditure variance = budget cost allowance for 5,500 units – actual expenditure for 5,500 units

= $85,000 – $82,400

= $2,600 favourable

(ii) Volume variance = budget cost allowance for original budget of 4,000 units – budget cost allowance for

actual volume of 5,500 units

= $70,000 – $85,000 = $15,000 adverse

254433 www.ebooks2000.blogspot.com

234

10: Flexible budgeting ⏐ Part C Financial planning and control

Question

Zebra Co

The following extract is taken from the production cost budget of Zebra Co:

Production units 4,000 6,000

Production cost $35,529 $41,280

The budget cost allowance for an activity level of 8,000 units is $

Answer

Change

Production units 4,000 6,000 2,000

Production cost $35,520 $41,280 $5,760

Variable cost per unit =

$5,760

2,000

= $2.88

Fixed costs = $35,520 – (4,000 × $2.88) = $24,000

Therefore, budget cost allowance for activity level of 8,000 units = $24,000 + (8,000 × $2.88)

= $47,040

You may come across the term 'flexed budget'. This is similar to a flexible budget. A flexible budget is designed at the

planning stage to vary with activity levels. A flexed budget is a revised budget that reflects the actual activity levels

achieved in the budget period.

3 Budgets and management reward

Budgets can be used in a system of reward strategies for managers. They act as targets or benchmarks for managerial

performance.

We mentioned at the start of Chapter 9 that one of the reasons for using budgets is to provide a means of evaluating the

performance of managers.

Research has shown that if an organisation’s reward system (promotions, salary increases, bonuses, ‘perks’) is

connected to a control system, management motivation will increase and management will perceive the control

system as important, which should improve its effectiveness.

For performance evaluation purposes, a system of control using budgets as targets or benchmarks for managerial

performance, against which actual performance is compared, can be adopted.

This provides a way of evaluating the performance of the manager and good results can be rewarded with a financial

bonus or promotion.

The process needs to be carried out so as to motivate managers, however, rather than create resentment and adverse

reactions. The process should not make managers feel under pressure to achieve but should encourage:

• Participation

• Initiative

• Responsibility

FA

S

T F

O

RWAR

D

255433 www.ebooks2000.blogspot.com

Part C Financial planning and control ⏐ 10: Flexible budgeting

235

It is therefore important that budget targets are:

• Under the control of managers (ie they can control the costs and revenues in question)

• Clearly defined

• Attainable (but not too easy to achieve as this will be demotivating)

• Understood and accepted as a target

• Focused on the short, medium and long term

Keeping managers informed of their performance also helps to encourage motivation. Feedback on performance

therefore needs to be:

• Frequent

• Up to date

• Accurate

• Relevant (ie relates to items over which the manager has control)

Chapter Roundup

• A fixed budget is a budget which is set for a single activity level.

• A flexible budget is a budget which recognises different cost behaviour patterns and is designed to change as volume of

activity changes.

• Control involves comparing a flexible budget (based on the actual activity level) with actual results. The differences

between the flexible budget figures and the actual results are budget variances.

• Budgets can be used in a system of reward strategies for managers. They act as targets or benchmarks for managerial

performance.

Quick Quiz

1 Fill in the blanks with the word 'fixed' or the word 'flexible'.

(a) At the planning stage, a ……………………. budget can show what the effects would be if the actual outcome

differs from the prediction.

(b) At the end of each period, actual results may be compared with the relevant activity level in the

……………………. budget as a control procedure.

(c) Master budgets are ……………………. budgets.

2 Flexible budgets are normally prepared on a marginal costing basis.

True

False

3 Fill in the gaps.

Budget cost allowance = ……………………. + (……………………. × …………………….)

4 What is the wrong approach to budgetary control?

5 What is the correct approach to budgetary control?

256433 www.ebooks2000.blogspot.com

236

10: Flexible budgeting ⏐ Part C Financial planning and control

Answers to Quick Quiz

1 (a) At the planning stage, a flexible budget can show what the effects would be if the actual outcome differs from the

prediction.

(b) At the end of each period, actual results may be compared with the relevant activity level in the flexible budget as

a control procedure.

(c) Master budgets are fixed budgets.

2 True

3 Budget cost allowance = budgeted fixed cost + (number of units × variable cost per unit)

4 To compare actual results against a fixed budget.

5 • To identify fixed and variable costs

• To produce a flexible budget using marginal costing techniques

Now try the questions below from the Question Bank

Question numbers Page

52–56 363

257433 www.ebooks2000.blogspot.com

237

Part D

Costing and accounting

systems

258433

www.ebooks2000.blogspot.com

238

259433 www.ebooks2000.blogspot.com

239

Topic list

Learning outcomes

Syllabus references

Ability required

1 Accounting for costs D(i) D(2) Comprehension

2 Integrated systems D(i), (ii) D(1), (2) Comprehension, Application

3 Standard cost bookkeeping D(ii) D(3) Application

Cost bookkeeping

Introduction

In Part A of this Study Text you saw how to determine the major elements of the cost of a

unit of product - material, labour, overhead - and how to build up these elements into a total

cost. In Chapters 12 and 13 you will see how costs are recorded depending on the costing

method adopted by an organisation. But what you need to know first is how to account for

costs within a cost accounting system. This chapter will teach you. It will teach you cost

bookkeeping.

The overall bookkeeping routine will vary from organisation to organisation but either an

integrated or an interlocking system will be used. For the purposes of this Paper C1 syllabus

you only need to know about integrated systems, however.

In the last part of this chapter we will look at how a standard costing system is used in

conjunction with an integrated system of cost bookkeeping.

260433

www.ebooks2000.blogspot.com