CIMA - C1 Fundamentals of Management Accounting

Подождите немного. Документ загружается.

200

9: Budget preparation ⏐ Part C Financial planning and control

1 Why do organisations prepare budgets?

Budgeting is a multi-purpose activity.

1.1 Reasons for preparing budgets

Here are some of the reasons why budgets are used.

Function Detail

Compel planning

Budgeting forces management to look ahead, to set out detailed plans for

achieving the targets for each department, operation and (ideally) each manager

and to anticipate problems.

Communicate ideas and plans

A formal system is necessary to ensure that each person affected by the plans is

aware of what he or she is supposed to be doing. Communication might be one-

way, with managers giving orders to subordinates, or there might be a two-way

communication .

Coordinate activities

The activities of different departments need to be coordinated to ensure everyone in

an organisation is working towards the same goals. This means, for example, that the

purchasing department should base its budget on production requirements and that

the production budget should in turn be based on sales expectations.

Provide a framework for

responsibility accounting

Budgets require that managers are made responsible for the achievement of

budget targets for the operations under their personal control.

Establish a system of control

Control over actual performance is provided by the comparisons of actual results

against the budget plan. Departures from budget can then be investigated and the

reasons for the departures can be divided into controllable and uncontrollable

factors.

Provide a means of performance

evaluation

Budgets provide targets which can be compared with actual outcomes in order to

assess employee performance.

Motivate employees to improve

their performance

The interest and commitment of employees can be retained if there is a system

that lets them know how well or badly they are performing. The identification of

controllable reasons for departures from budget with managers responsible

provides an incentive for improving future performance.

Here's what the Official Terminology has to say:

Budget purposes: 'Budgets may help in authorising expenditure, communicating objectives and plans, controlling

operations, co-ordinating activities, evaluating performance, planning and rewarding performance. Often, reward

systems involve comparison of actual with budgeted performance.' CIMA Official Terminology

Key term

FA

S

T F

O

RWAR

D

221433 www.ebooks2000.blogspot.com

Part C Financial planning and control ⏐ 9: Budget preparation

201

1.2 Different things to different people

A budget, since it has different purposes, might mean different things to different people.

A budget might be a forecast, a means of allocating resources, a yardstick or a target.

What it might mean Detail

Forecast

It helps managers to plan for the future. Given uncertainty about the future, however, it is

quite likely that a budget will become outdated as events occur and so the budget will cease

to be a realistic forecast. New forecasts might be prepared that differ from the budget. (A

forecast is what is likely to happen; a budget is what an organisation wants to happen.

These are not necessarily the same thing.)

Means of allocating

resources

It can be used to decide how many resources are needed (cash, labour and so on) and how

many should be given to each area of the organisation's activities. As we saw when we

looked at limiting factor analysis, resource allocation is particularly important when some

resources are in short supply. Budgets often set ceilings or limits on how much

administrative departments and other service departments are allowed to spend in the

period. Public expenditure budgets, for example, set spending limits for each government

department.

Yardstick

By comparing it with actual performance, the budget provides a means of indicating where

and when control action may be necessary (and possibly where some managers or

employees are open to censure for achieving poor results).

Target

A budget might be a means of motivating the workforce to greater personal

accomplishment, another aspect of control.

A budget is a 'quantitative expression of a plan for a defined period of time. It may include planned sales volumes and

revenues; resource quantities, costs and expenses; assets, liabilities and cash flows.' CIMA Official Terminology

2 A framework for budgeting

2.1 Budget committee

The budget committee is the coordinating body in the preparation and administration of budgets.

The budget committee is usually headed up by the managing director (as chairman) and is assisted by a budget officer

who is usually an accountant. Every part of the organisation should be represented on the committee, so there should be

a representative from sales, production, marketing and so on. Functions of the budget committee include the following.

• Coordination and allocation of responsibility for the preparation of budgets

• Issuing of the budget manual

• Timetabling

• Provision of information to assist in the preparation of budgets

• Communication of final budgets to the appropriate managers

• Monitoring the budgeting process by comparing actual and budgeted results

FA

S

T F

O

RWAR

D

Key term

FAST FORWA

RD

222433 www.ebooks2000.blogspot.com

202

9: Budget preparation ⏐ Part C Financial planning and control

2.2 The budget period

A budget period is a 'period for which a budget is prepared, and used, which may then be sub-divided into control

periods'. CIMA Official Terminology

Except for capital expenditure budgets, the budget period is usually the accounting year (sub-divided into 12 or 13

control periods).

2.3 Responsibility for budgets

The manager responsible for preparing each budget should ideally be the manager responsible for carrying out the

budget.

For example, the preparation of particular budgets might be allocated as follows.

(a) The sales manager should draft the sales budget and the selling overhead cost centre budgets.

(b) The purchasing manager should draft the material purchases budget.

(c) The production manager should draft the direct production cost budgets.

Question

Budget committee

Which of the following is the budget committee not responsible for?

A Preparing functional budgets

B Timetabling the budgeting operation

C Allocating responsibility for the budget preparation

D Monitoring the budgeting process

Answer

The correct answer is A.

The manager responsible for implementing the budget that must prepare it, not the budget committee.

If you don't know the answer, remember not to fall for the common pitfall of thinking, 'Well, we haven't had a D for a

while, so I'll guess that'. It is good practice to guess if you don't know the answer (never leave out an assessment

question) but first eliminate some of the options if you can.

Since the committee is a co-ordinating body we can definitely say that they are responsible for B and D. Similarly, a co-

ordinating body is more likely to allocate responsibility than to actually undertake the budget preparation, so eliminate C

and select A as the correct answer.

FA

S

T F

O

RWAR

D

Key term

223433 www.ebooks2000.blogspot.com

Part C Financial planning and control ⏐ 9: Budget preparation

203

2.4 The budget manual

The budget manual is a collection of instructions governing the responsibilities of persons and the procedures, forms

and records relating to the preparation and use of budgetary data.

The budget manual is a 'detailed set of guidelines and information about the budget process typically including a

calendar of budgetary events, specimen budget forms, a statement of budgetary objectives and desired results, listing of

budgetary activities and budget assumptions, regarding, for example, inflation and interest rates'.

CIMA Official Terminology

A budget manual may contain the following.

(a) An explanation of the objectives of the budgetary process

(i) The purpose of budgetary planning and control

(ii) The objectives of the various stages of the budgetary process

(iii) The importance of budgets in the long-term planning of the business

(b) Organisational structures

(i) An organisation chart

(ii) A list of individuals holding budget responsibilities

(c) An outline of the principal budgets and the relationship between them

(d) Administrative details of budget preparation

(i) Membership and terms of reference of the budget committee

(ii) The sequence in which budgets are to be prepared

(iii) A timetable

(e) Procedural matters

(i) Specimen forms and instructions for their completion

(ii) Specimen reports

(iii) Account codes (or a chart of accounts)

(iv) The name of the budget officer to whom enquiries must be sent

3 Steps in the preparation of a budget

The first task in the budgetary process is to identify the principal budget factor. This is also known as the key budget

factor or limiting budget factor. The principal budget factor is the factor which limits the activities of an organisation.

The procedures for preparing a budget will differ from organisation to organisation but the steps described below will be

indicative of the steps followed by many organisations. The preparation of a budget may take weeks or months and the

budget committee may meet several times before the master budget (budgeted income statement, budgeted statement

of financial position and budgeted cash flow) is finally agreed. Functional budgets (sales budgets, production budgets,

direct labour budgets and so on), which are amalgamated into the master budget, may need to be amended many times

over as a consequence of discussions between departments, changes in market conditions and so on during the course

of budget preparation.

FAST FORWARD

Key term

FA

S

T F

O

RWAR

D

224433 www.ebooks2000.blogspot.com

204

9: Budget preparation ⏐ Part C Financial planning and control

3.1 Identifying the principal budget factor

The principal budget factor 'limits the activities of an undertaking. Identification of the principal budget factor is often

the starting point in the budget setting process. Often the principal budget factor will be sales demand but it could be

production capacity or material supply.' CIMA Official Terminology

The principal budget factor is usually sales demand. A company is usually restricted from making and selling more of

its products because there would be no sales demand for the increased output at a price which would be

acceptable/profitable to the company. The principal budget factor may also be machine capacity, distribution and selling

resources, the availability of key raw materials or the availability of cash. Once this factor is defined then the remainder

of the budgets can be prepared. For example, if sales are the principal budget factor then the production manager can

only prepare his budget after the sales budget is complete.

3.2 The order of budget preparation

Assuming that the principal budget factor has been identified as being sales, the stages involved in the preparation of a

budget can be summarised as follows.

(a) The sales budget is prepared in units of product and sales value. The finished goods inventory budget

can be prepared at the same time. This budget decides the planned increase or decrease in finished goods

inventory levels.

(b) With the information from the sales and inventory budgets, the production budget can be prepared. This

is, in effect, the sales budget in units plus (or minus) the increase (or decrease) in finished goods

inventory. The production budget will be stated in terms of units.

(c) This leads on logically to budgeting the resources for production. This involves preparing a materials

usage budget, machine usage budget and a labour budget.

(d) In addition to the materials usage budget, a materials inventory budget will be prepared, to decide the

planned increase or decrease in the level of inventory held. Once the raw materials usage requirements

and the raw materials inventory budget are known, the purchasing department can prepare a raw

materials purchases budget in quantities and value for each type of material purchased.

(e) During the preparation of the sales and production budgets, the managers of the cost centres of the

organisation will prepare their draft budgets for the department overhead costs. Such overheads will

include maintenance, stores, administration, selling and research and development.

(f) From the above information a budgeted income statement can be produced.

(g) In addition several other budgets must be prepared in order to arrive at the budgeted statement of

financial position. These are the capital expenditure budget (for non-current assets), the working capital

budget (for budgeted increases or decreases in the level of receivables and accounts payable as well as

inventories), and a cash budget.

Make sure that you understand the meaning of principal budget factor.

Key term

Assessment

focus point

225433 www.ebooks2000.blogspot.com

Part C Financial planning and control ⏐ 9: Budget preparation

205

4 Functional budgets

Functional/departmental budgets include budgets for sales, production, purchases and labour.

A departmental/functional budget is a 'budget of income and/or expenditure applicable to a particular function

frequently including sales budget, production cost budget (based on budgeted production, efficiency and utilisation),

purchasing budget, human resources budget, marketing budget and research and development budget'.

CIMA Official Terminology

Having seen the theory of budget preparation, let us look at functional (or departmental) budget preparation, which are

best explained by means of an example.

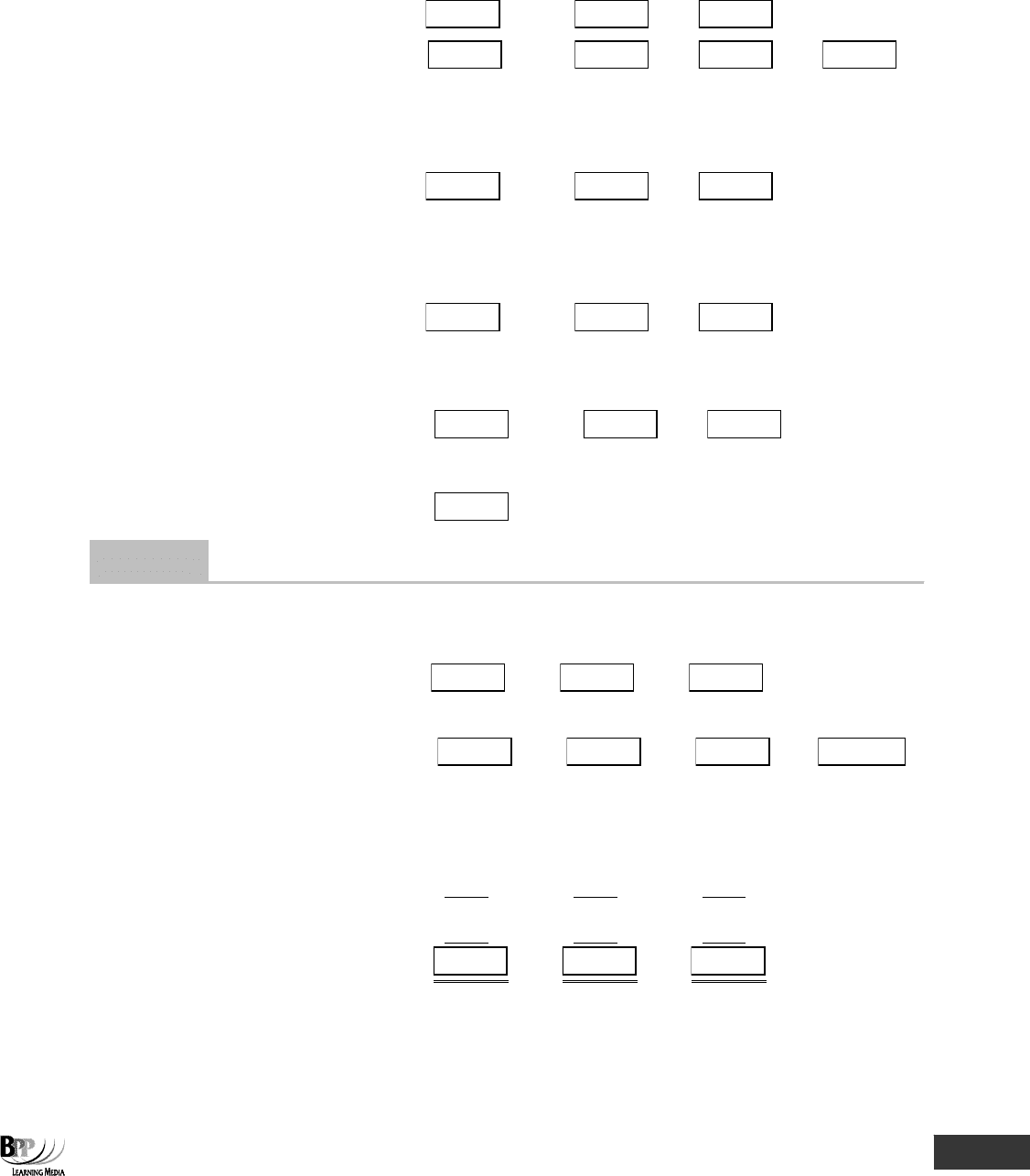

4.1 Example: preparing a materials purchases budget

ECO Co manufactures two products, S and T, which use the same raw materials, D and E. One unit of S uses 3 litres of D

and 4 kilograms of E. One unit of T uses 5 litres of D and 2 kilograms of E. A litre of D is expected to cost $3 and a

kilogram of E $7.

Budgeted sales for 20X2 are 8,000 units of S and 6,000 units of T; finished goods in inventory at 1 January 20X2 are

1,500 units of S and 300 units of T, and the company plans to hold inventories of 600 units of each product at 31

December 20X2.

Inventories of raw material are 6,000 litres of D and 2,800 kilograms of E at 1 January and the company plans to hold

5,000 litres and 3,500 kilograms respectively at 31 December 20X2.

The warehouse and stores managers have suggested that a provision should be made for damages and deterioration of

items held in store, as follows.

Product S: loss of 50 units Material D: loss of 500 litres

Product T: loss of 100 units Material E: loss of 200 kilograms

Required

Prepare a material purchases budget for the year 20X2.

Solution

To calculate material purchases requirements it is first necessary to calculate the material usage requirements. That in

turn depends on calculating the budgeted production volumes.

Product S

Product T

Units

Units

Production required

To meet sales demand

8,000

6,000

To provide for inventory loss

50

100

For closing inventory

600

600

8,650

6,700

Less inventory already in hand

1,500

300

Budgeted production volume

7,150

6,400

FA

S

T F

O

RWAR

D

Key term

226433 www.ebooks2000.blogspot.com

206

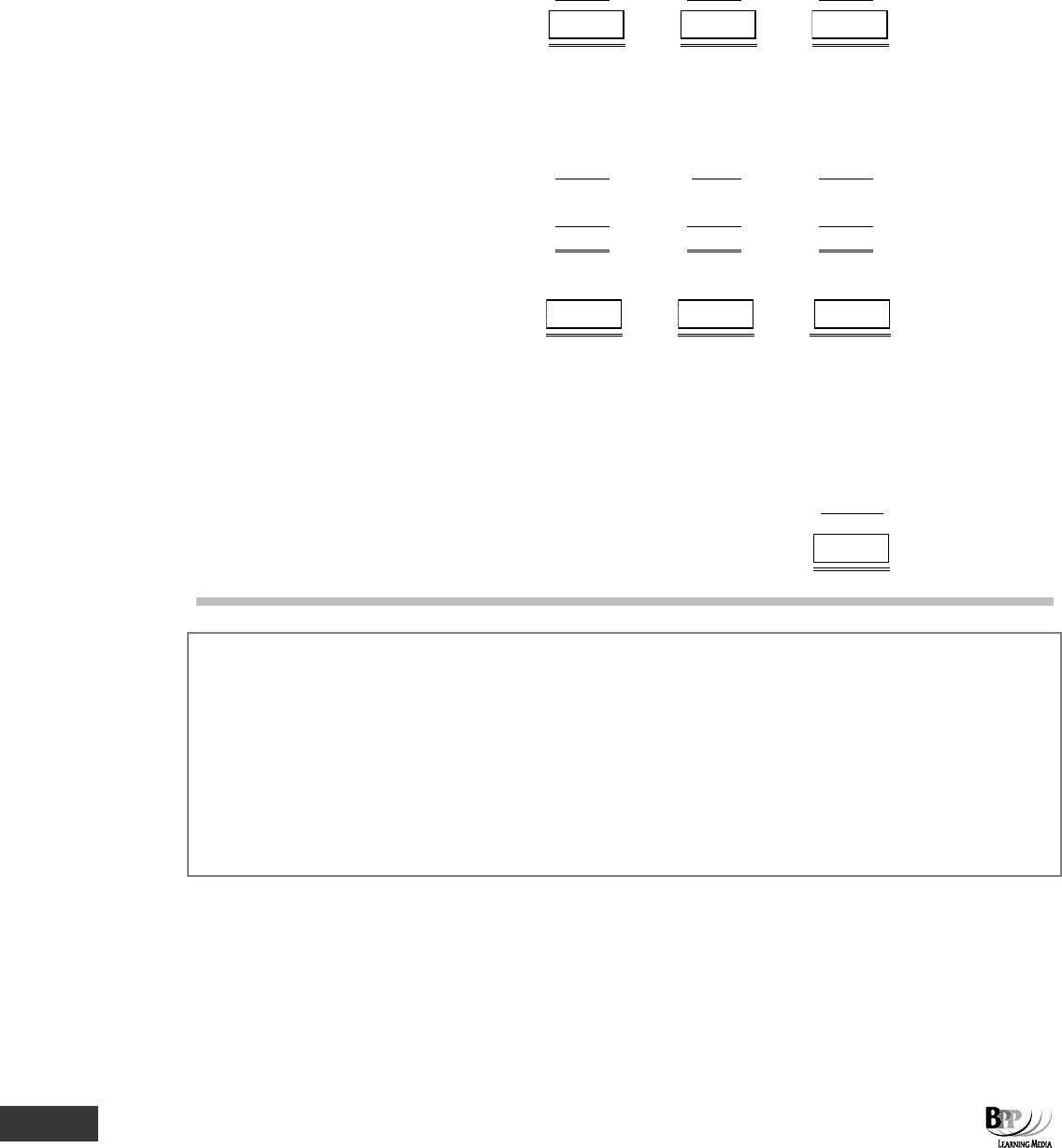

9: Budget preparation ⏐ Part C Financial planning and control

Material D

Material E

Litres

Kgs

Usage requirements

To produce 7,150 units of S

21,450

28,600

To produce 6,400 units of T

32,000

12,800

To provide for inventory loss

500

200

For closing inventory

5,000

3,500

58,950

45,100

Less inventory already in hand

6,000

2,800

Budgeted material purchases

52,950

42,300

Unit cost

$3

$7

Cost of material purchases

$158,850

$296,100

Total cost of material purchases

$454,950

The basics of the preparation of each functional budget are similar to those above. Work carefully through the following

question which covers the preparation of a number of different types of functional budget.

Question

Functional budgets

XYZ company produces three products X, Y and Z. For the coming accounting period budgets are to be prepared based

on the following information.

Budgeted sales

Product X 2,000 at $100 each

Product Y 4,000 at $130 each

Product Z 3,000 at $150 each

Budgeted usage of raw material

RM11 RM22 RM33

Product X 5 2 –

Product Y 3 2 2

Product Z 2 1 3

Cost per unit of material $5 $3 $4

Finished inventories budget

Product X Product Y Product Z

Opening 500 800 700

Closing 600 1,000 800

Raw materials inventory budget

RM11 RM22 RM33

Opening 21,000 10,000 16,000

Closing 18,000 9,000 12,000

Product X Product Y Product Z

Expected hours per unit 4 6 8

Expected hourly rate (labour) $9 $9 $9

Important!

227433 www.ebooks2000.blogspot.com

Part C Financial planning and control ⏐ 9: Budget preparation

207

Fill in the blanks.

(a) Sales budget

Product X Product Y Product Z Total

Sales quantity

Sales value $

$ $

$

(b) Production budget

Product X Product Y Product Z

Units Units Units

Budgeted production

(c) Material usage budget

RM11 RM22 RM33

Units Units Units

Budgeted material usage

(d) Material purchases budget

RM11 RM22 RM33

Budgeted material purchases $

$ $

(e) Labour budget

Budgeted total wages $

Answer

(a) Sales budget

Product X

Product Y

Product Z

Total

Sales quantity

2,000

4,000

3,000

Sales price

$100

$130

$150

Sales value

$

200,000

$

520,000

$

450,000

$

1,170,000

(b) Production budget

Product X

Product Y

Product Z

Units

Units

Units

Sales quantity

2,000

4,000

3,000

Closing inventories

600

1,000

800

2,600

5,000

3,800

Less opening inventories

500

800

700

Budgeted production

2,100

4,200

3,100

228433 www.ebooks2000.blogspot.com

208

9: Budget preparation ⏐ Part C Financial planning and control

(c) Material usage budget

Production

RM11

RM22

RM33

Units

Units

Units

Units

Product X

2,100

10,500

4,200

–

Product Y

4,200

12,600

8,400

8,400

Product Z

3,100

6,200

3,100

9,300

Budgeted material

usage

29,300

15,700

17,700

(d) Material purchases budget

RM11

RM22

RM33

Units

Units

Units

Budgeted material usage

29,300

15,700

17,700

Closing inventories

18,000

9,000

12,000

47,300

24,700

29,700

Less opening inventories

21,000

10,000

16,000

Budgeted material purchases

26,300

14,700

13,700

Standard cost per unit

$5

$3

$4

Budgeted material purchases

$

131,500

$

44,100

$

54,800

(e) Labour budget

Hours required Total

Rate per

Product

Production

per unit

hours

hour

Cost

Units

$

$

X

2,100

4

8,400

9

75,600

Y

4,200

6

25,200

9

226,800

Z

3,100

8

24,800

9

223,200

Budgeted total wages

525,600

You may get an assessment question which asks you to work out one budgeted figure from another. For example you

may be given the sales budget and asked to work out the production budget. Make sure that you learn this formula.

Units made = units sold + units in closing inventory – units in opening inventory.

The business must produce enough to cover its sales volume and to leave enough in closing inventory, but it gets a

'head start' from opening inventory. This is why opening inventory is deducted.

You can apply this principle to other areas of budgeting. For example

Materials purchases = materials usage + closing inventory material – opening inventory material.

Assessment

focus point

229433 www.ebooks2000.blogspot.com

Part C Financial planning and control ⏐ 9: Budget preparation

209

Question

The following information is available for B Co.

Budgeted annual sales 100,000 units

Opening inventory 25,000 units

Closing inventory 27,500 units

What is the number of units of production for the year?

A 72,500 C 100,000

B 97,500 D 102,000

Answer

D 102,500

Units made = units sold + closing inventory units – opening inventory units

= 100,000 + 27,500 – 25,000

= 102,500

5 Cash budgets

A cash budget is a statement in which estimated future cash receipts and payments are tabulated in such a way as to

show the forecast cash balance of a business at defined intervals.

A cash budget is a 'detailed budget of estimated cash inflows and outflows incorporating both revenue and capital

items'. CIMA Official Terminology

5.1 Preparing cash budgets

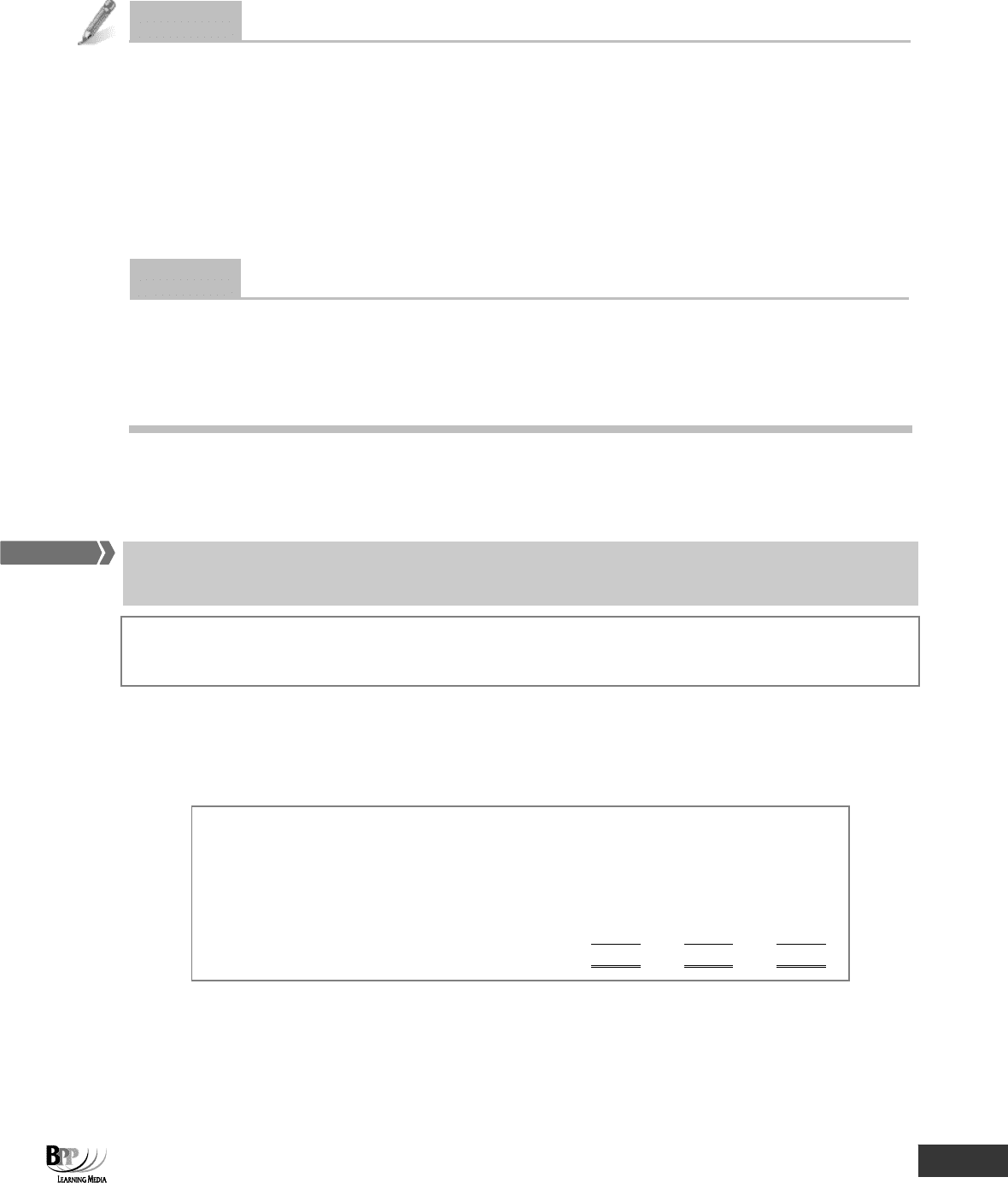

For example, in December 20X2 an accounts department might wish to estimate the cash position of the business during

the three following months, January to March 20X3. A cash budget might be drawn up in the following format.

Jan

Feb

Mar

$

$

$

Estimated cash receipts

From accounts payable

14,000

16,500

17,000

From cash sales

3,000

4,000

4,500

Proceeds on disposal of non-current assets

2,200

Total cash receipts

17,000

22,700

21,500

FA

S

T F

O

RWAR

D

Key term

230433 www.ebooks2000.blogspot.com