Brealey, Myers. Principles of Corporate Finance. 7th edition

Подождите немного. Документ загружается.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

17. Does Debt policy

Matter?

© The McGraw−Hill

Companies, 2003

Therefore, a share in the levered company must also sell for $10. If Macbeth goes

ahead and borrows, it will not allow investors to do anything that they could not

do already, and so it will not increase value.”

The argument that you are using is exactly the same as the one MM used to

prove proposition I.

CHAPTER 17

Does Debt Policy Matter? 471

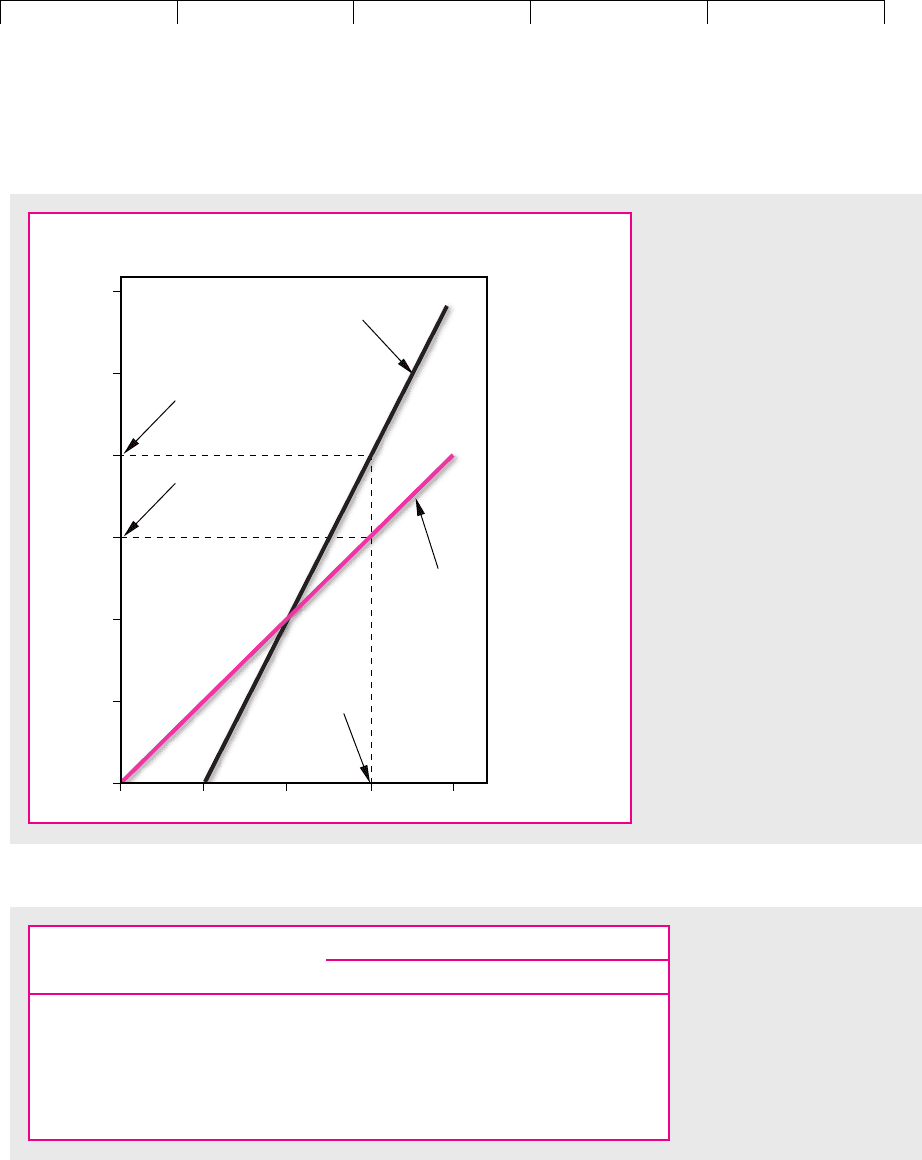

3.00

2.50

2.00

1.50

1.00

0.50

0.00

500

1000 1500 2000

Earnings per share

(EPS), dollars

Equal proportions

debt and equity

Expected EPS with

debt and equity

Expected

operating

income

Operating

income, dollars

Expected EPS

with all equity

All equity

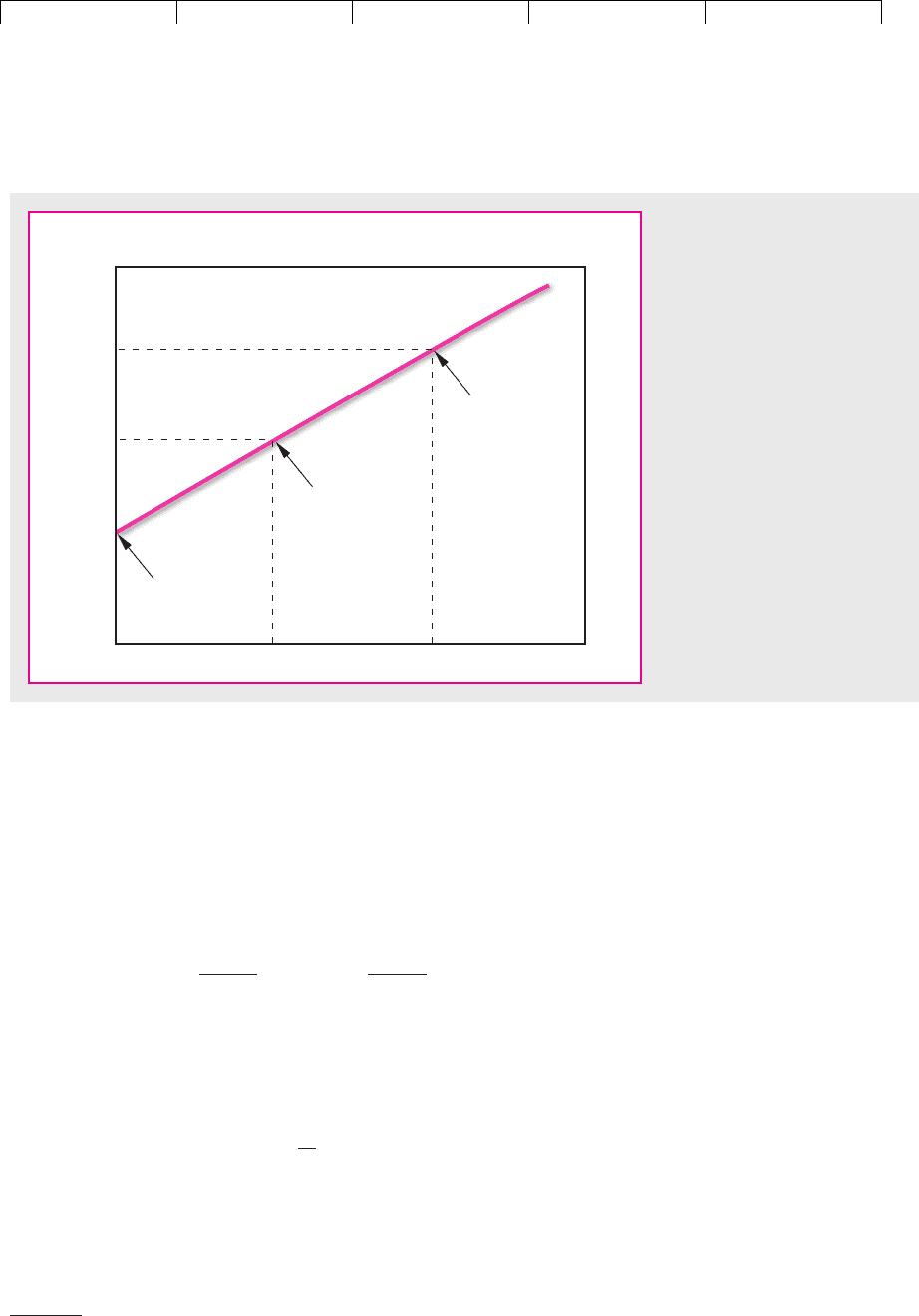

FIGURE 17.1

Borrowing increases Macbeth’s

EPS (earnings per share) when

operating income is greater than

$1,000 and reduces EPS when

operating income is less than

$1,000. Expected EPS rises from

$1.50 to $2.

Operating Income ($)

500 1,000 1,500 2,000

Earnings on two shares ($) 1 2 3 4

Less interest at 10% ($) 1 1 1 1

Net earnings on investment ($) 0 1 2 3

Return on $10 investment (%) 0 10 20 30

Expected

outcome

TABLE 17.3

Individual investors can

replicate Macbeth’s leverage.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

17. Does Debt policy

Matter?

© The McGraw−Hill

Companies, 2003

Implications of Proposition I

Consider now the implications of proposition I for the expected returns on Mac-

beth stock:

472 PART V

Dividend Policy and Capital Structure

17.2 HOW LEVERAGE AFFECTS RETURNS

Current Structure: Proposed Structure:

All Equity Equal Debt and Equity

Expected earnings per share ($) 1.50 2.00

Price per share ($) 10 10

Expected return on share (%) 15 20

Leverage increases the expected stream of earnings per share but not the share

price. The reason is that the change in the expected earnings stream is exactly off-

set by a change in the rate at which the earnings are capitalized. The expected re-

turn on the share (which for a perpetuity is equal to the earnings–price ratio) in-

creases from 15 to 20 percent. We now show how this comes about.

The expected return on Macbeth’s assets is equal to the expected operating in-

come divided by the total market value of the firm’s securities:

We have seen that in perfect capital markets the company’s borrowing decision

does not affect either the firm’s operating income or the total market value of its se-

curities. Therefore the borrowing decision also does not affect the expected return

on the firm’s assets .

Suppose that an investor holds all of a company’s debt and all of its equity. This

investor would be entitled to all the firm’s operating income; therefore, the ex-

pected return on the portfolio would be equal to .

The expected return on a portfolio is equal to a weighted average of the expected

returns on the individual holdings. Therefore the expected return on a portfolio

consisting of all the firm’s securities is

6

We can rearrange this equation to obtain an expression for , the expected return

on the equity of a levered firm:

r

E

r

A

a

D

D E

r

D

b a

E

D E

r

E

b

a

proportion

in equity

expected return

on equity

b

Expected return

on assets

a

proportion

in debt

expected return

on debt

b

r

A

r

A

Expected return on assets r

A

expected operating income

market value of all securities

r

A

6

This equation should look familiar. We introduced it in Chapter 9 when we showed that the company

cost of capital is a weighted average of the expected returns on the debt and equity. (Company cost of cap-

ital is simply another term for the expected return on assets, .) We also stated in Chapter 9 that chang-

ing the capital structure does not change the company cost of capital. In other words, we implicitly as-

sumed MM’s proposition I.

r

A

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

17. Does Debt policy

Matter?

© The McGraw−Hill

Companies, 2003

r

E

r

A

D

E

1r

A

r

D

2

a

expected return

on assets

expected return

on debt

b

Expected return

on equity

expected return

on assets

debt–equity

ratio

CHAPTER 17 Does Debt Policy Matter? 473

Proposition II

This is MM’s proposition II: The expected rate of return on the common stock of a

levered firm increases in proportion to the debt–equity ratio (D/E), expressed in

market values; the rate of increase depends on the spread between , the expected

rate of return on a portfolio of all the firm’s securities, and , the expected return

on the debt. Note that if the firm has no debt.

We can check out this formula for Macbeth Spot Removers. Before the decision

to borrow

If the firm goes ahead with its plan to borrow, the expected return on assets is

still 15 percent. The expected return on equity is

The general implications of MM’s proposition II are shown in Figure 17.2. The

figure assumes that the firm’s bonds are essentially risk-free at low debt levels.

Thus is independent of D/E, and increases linearly as D/E increases. As the

firm borrows more, the risk of default increases and the firm is required to pay

higher rates of interest. Proposition II predicts that when this occurs the rate of in-

crease in slows down. This is also shown in Figure 17.2. The more debt the firm

has, the less sensitive is to further borrowing.

Why does the slope of the line in Figure 17.2 taper off as D/E increases? Es-

sentially because holders of risky debt bear some of the firm’s business risk. As the

firm borrows more, more of that risk is transferred from stockholders to bond-

holders.

The Risk–Return Trade-off

Proposition I says that financial leverage has no effect on shareholders’ wealth.

Proposition II says that the rate of return they can expect to receive on their shares

increases as the firm’s debt–equity ratio increases. How can shareholders be indif-

ferent to increased leverage when it increases expected return? The answer is that

any increase in expected return is exactly offset by an increase in risk and therefore

in shareholders’ required rate of return.

r

E

r

E

r

E

r

E

r

D

.20, or 20%

.15

5,000

5,000

1.15 .102

r

E

r

A

D

E

1r

A

r

D

2

r

A

1,500

10,000

.15, or 15%

r

E

r

A

expected operating income

market value of all securities

r

E

r

A

r

D

r

A

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

17. Does Debt policy

Matter?

© The McGraw−Hill

Companies, 2003

Look at what happens to the risk of Macbeth shares if it moves to equal debt–

equity proportions. Table 17.4 shows how a shortfall in operating income affects

the payoff to the shareholders.

The debt–equity proportion does not affect the dollar risk borne by equity-

holders. Suppose operating income drops from $1,500 to $500. Under all-equity

financing, equity earnings drop by $1 per share. There are 1,000 outstanding

shares, and so total equity earnings fall by . With 50 percent

debt, the same drop in operating income reduces earnings per share by $2. But

there are only 500 shares outstanding, and so total equity income drops by

, just as in the all-equity case.

However, the debt–equity choice does amplify the spread of percentage re-

turns. If the firm is all-equity-financed, a decline of $1,000 in the operating in-

come reduces the return on the shares by 10 percent. If the firm issues risk-free

debt with a fixed interest payment of $500 a year, then a decline of $1,000 in the

operating income reduces the return on the shares by 20 percent. In other words,

$2 500 $1,000

$1 1,000 $1,000

474 PART V

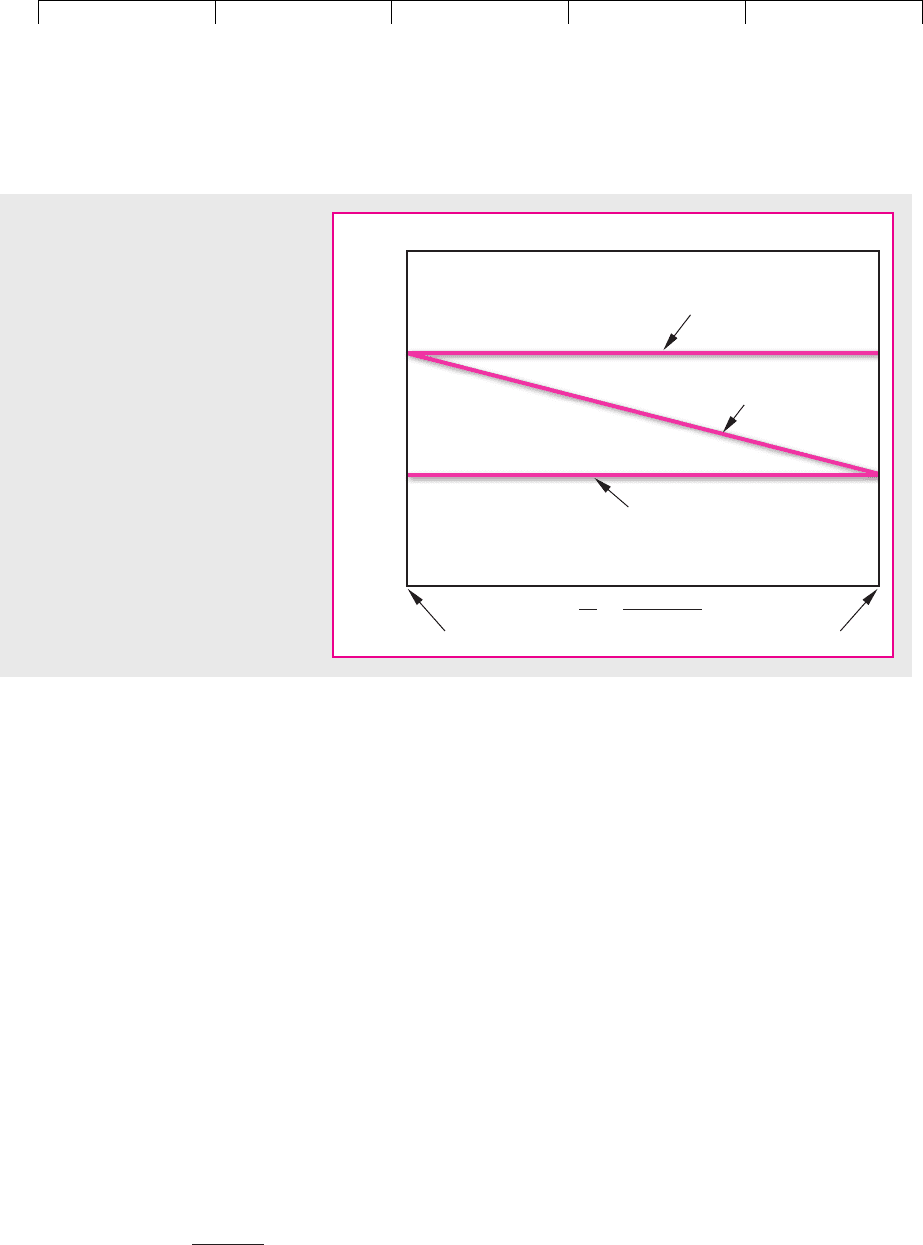

Dividend Policy and Capital Structure

Risk-free debt Risky debt

debt

equity

D

E

Rates of return

r

E

= Expected return on equity

r

A

= Expected return on assets

r

D

= Expected return on debt

=

FIGURE 17.2

MM’s proposition II. The expected return on

equity increases linearly with the debt–equity

ratio so long as debt is risk-free. But if leverage

increases the risk of the debt, debtholders

demand a higher return on the debt. This causes

the rate of increase in to slow down.r

E

r

E

Operating Income

$500 $1,500

All equity: Earnings per share ($) .50 1.50

Return on shares (%) 5 15

50 percent debt: Earnings per share ($) 0 2

Return on shares (%) 0 20

TABLE 17.4

Leverage increases the risk of

Macbeth shares.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

17. Does Debt policy

Matter?

© The McGraw−Hill

Companies, 2003

the effect of leverage is to double the amplitude of the swings in Macbeth’s

shares. Whatever the beta of the firm’s shares before the refinancing, it would be

twice as high afterward.

Just as the expected return on the firm’s assets is a weighted average of the ex-

pected return on the individual securities, so likewise is the beta of the firm’s as-

sets a weighted average of the betas of the individual securities:

7

We can rearrange this equation also to give an expression for , the beta of the eq-

uity of a levered firm:

Now you can see why investors require higher returns on levered equity. The re-

quired return simply rises to match the increased risk.

In Figure 17.3, we have plotted the expected returns and the risk of Macbeth’s

securities, assuming that the interest on the debt is risk-free.

8

E

A

D

E

1

A

D

2

Beta of equity

beta of

assets

debt–equity

ratio

a

beta of

assets

beta of

debt

b

E

A

a

D

D E

D

b a

E

D E

E

b

Beta of

assets

a

proportion

of debt

beta of

debt

b a

proportion

of equity

beta of

equity

b

CHAPTER 17

Does Debt Policy Matter? 475

7

This equation should also look old-hat. We used it in Section 9.3 when we stated that changes in the

capital structure change the beta of stock but not the asset beta.

8

In this case and .

E

A

1D/E2

A

D

0

Risk

Debt

Equity

All firm's assets

Expected rates

of return

β

E

β

A

β

D

r

A

=

.15

r

E

=

.20

r

D

=

.10

FIGURE 17.3

If Macbeth is unlevered, the

expected return on its equity

equals the expected return on its

assets. Leverage increases both

the expected return on equity ( )

and the risk of equity ( ).

E

r

E

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

17. Does Debt policy

Matter?

© The McGraw−Hill

Companies, 2003

What did financial experts think about debt policy before MM? It is not easy to say

because with hindsight we see that they did not think too clearly.

9

However, a “tra-

ditional” position has emerged in response to MM. In order to understand it, we

have to discuss the weighted-average cost of capital.

The expected return on a portfolio of all the company’s securities is often re-

ferred to as the weighted-average cost of capital:

10

The weighted-average cost of capital is used in capital budgeting decisions to

find the net present value of projects that would not change the business risk of

the firm.

For example, suppose that a firm has $2 million of outstanding debt and 100,000

shares selling at $30 per share. Its current borrowing rate is 8 percent, and the fi-

nancial manager thinks that the stock is priced to offer a 15 percent return. There-

fore and . (The hard part is estimating

,

of course.) This is all we

need to calculate the weighted-average cost of capital:

Note that we are still assuming that proposition I holds. If it doesn’t, we can’t use

this simple weighted average as the discount rate even for projects that do not

change the firm’s business “risk class.” As we will see in Chapter 19, the weighted-

average cost of capital is only a starting point for setting discount rates.

Two Warnings

Sometimes the objective in financing decisions is stated not as “maximize overall

market value” but as “minimize the weighted-average cost of capital.” If MM’s

proposition I holds, then these are equivalent objectives. If MM’s proposition I

does not hold, then the capital structure that maximizes the value of the firm also

minimizes the weighted-average cost of capital, provided that operating income is

independent of capital structure. Remember that the weighted-average cost of cap-

ital is the expected rate of return on the market value of all of the firm’s securities.

.122,

or 12.2%

a

2

5

.08 b a

3

5

.15 b

Weighted-average cost of capital a

D

V

r

D

b a

E

V

r

E

b

V D E 2 3 $5 million

E 100,000 shares $30 per share $3 million

D $2 million

r

E

r

E

.15r

D

.08

Weighted-average cost of capital r

A

a

D

V

r

D

b a

E

V

r

E

b

476 PART V Dividend Policy and Capital Structure

17.3 THE TRADITIONAL POSITION

9

Financial economists in 20 years may remark on Brealey and Myers’s blind spots and clumsy reason-

ing. On the other hand, they may not remember us at all.

10

Remember that in this chapter we ignore taxes. In Chapter 19, we shall see that the weighted-average

cost of capital formula needs to be amended when debt interest can be deducted from taxable profits.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

17. Does Debt policy

Matter?

© The McGraw−Hill

Companies, 2003

Anything that increases the value of the firm reduces the weighted-average cost of

capital if operating income is constant. But if operating income is varying too, all

bets are off.

In Chapter 18 we will show that financial leverage can affect operating income

in several ways. Therefore maximizing the value of the firm is not always equiva-

lent to minimizing the weighted-average cost of capital.

Warning 1 Shareholders want management to increase the firm’s value. They are

more interested in being rich than in owning a firm with a low weighted-average

cost of capital.

Warning 2 Trying to minimize the weighted-average cost of capital seems to en-

courage logical short circuits like the following. Suppose that someone says,

“Shareholders demand—and deserve—higher expected rates of return than bond-

holders do. Therefore debt is the cheaper capital source. We can reduce the

weighted-average cost of capital by borrowing more.” But this doesn’t follow if the

extra borrowing leads stockholders to demand a still higher expected rate of re-

turn. According to MM’s proposition II the cost of equity capital increases by just

enough to keep the weighted-average cost of capital constant.

This is not the only logical short circuit you are likely to encounter. We have

cited two more in practice question 5 at the end of this chapter.

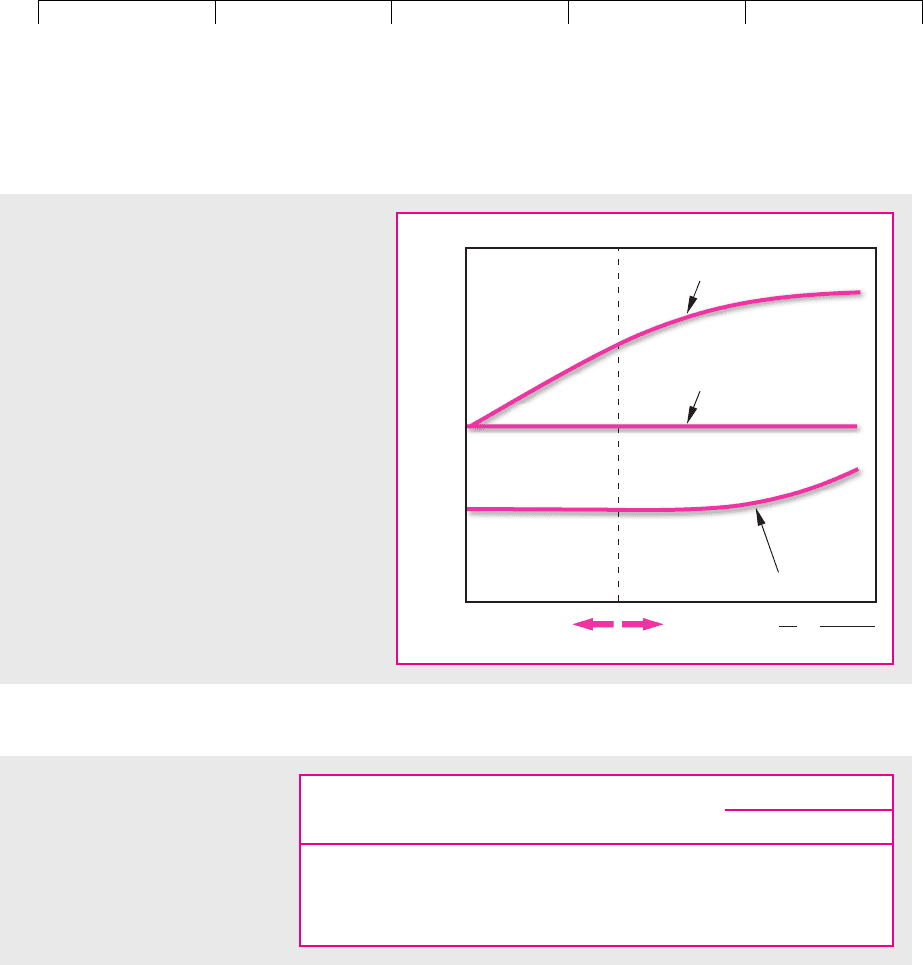

Rates of Return on Levered Equity—The Traditional Position

You may ask why we have even mentioned the aim of minimizing the weighted-

average cost of capital if it is often wrong or confusing. We had to because the tra-

ditionalists accept this objective and argue their case in terms of it.

The logical short circuit we just described rested on the assumption that , the

expected rate of return demanded by stockholders, does not rise as the firm bor-

rows more. Suppose, just for the sake of argument, that this is true. Then , the

weighted-average cost of capital, must decline as the debt–equity ratio rises.

Take Figure 17.4, for example, which is drawn on the assumption that share-

holders demand 12 percent no matter how much debt the firm has and that bond-

holders always want 8 percent. The weighted-average cost of capital starts at 12

percent and ends up at 8. Suppose that this firm’s operating income is a level, per-

petual stream of $100,000 a year. Then firm value starts at

and ends up at

The gain of $416,667 falls into the stockholders’ pockets.

11

Of course this is absurd: A firm that reaches 100 percent debt has to be bankrupt.

If there is any chance that the firm could remain solvent, then the equity retains

V

100,000

.08

$1,250,000

V

100,000

.12

$833,333

r

A

r

E

r

E

CHAPTER 17 Does Debt Policy Matter? 477

11

Note that Figure 17.4 relates and to D/V, the ratio of debt to firm value, rather than to the debt–

equity ratio D/E. In this figure we wanted to show what happens when the firm is 100 percent debt-

financed. At that point and D/E is infinite.E 0

r

D

r

E

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

17. Does Debt policy

Matter?

© The McGraw−Hill

Companies, 2003

some value, and the firm cannot be 100 percent debt-financed. (Remember that we

are working with the market values of debt and equity.)

But if the firm is bankrupt and its original shares are worthless pieces of paper,

then its lenders are its new shareholders. The firm is back to all-equity financing! We

assumed that the original stockholders demanded 12 percent—why should the

new ones demand any less? They have to bear all of the firm’s business risk.

12

The situation described in Figure 17.4 is just impossible.

13

However, it is possi-

ble to stake out a position somewhere between Figures 17.3 and 17.4. That is exactly

what the traditionalists have done. Their hypothesis is shown in Figure 17.5. They

hold that a moderate degree of financial leverage may increase the expected equity

return , although not to the degree predicted by MM’s proposition II. But irre-

sponsible firms that borrow excessively find shooting up faster than MM predict.

Consequently, the weighted-average cost of capital declines at first, then rises.

Its minimum point is the point of optimal capital structure. Remember that mini-

mizing is equivalent to maximizing overall firm value if, as the traditionalists as-

sume, operating income is unaffected by borrowing.

Two arguments might be advanced in support of the traditional position. First, it

could be that investors don’t notice or appreciate the financial risk created by “mod-

erate” borrowing, although they wake up when debt is “excessive.” If so, investors in

moderately leveraged firms may accept a lower rate of return than they really should.

r

A

r

A

r

E

r

E

478 PART V Dividend Policy and Capital Structure

Zero debt 100 percent debt

.08

.12

r

E

= Expected return on equity

r

D

= Expected return on debt

r

A

= Weighted-average

cost of capital

debt

Rates of return

firm value

D

V

=

FIGURE 17.4

If the expected rate of return demanded

by stockholders is unaffected by

financial leverage, then the weighted-

average cost of capital declines as the

firm borrows more. At 100 percent debt

equals the borrowing rate . Of

course this is an absurd and totally unre-

alistic case.

r

D

r

A

r

A

r

E

12

We ignore the costs, delays, and other complications of bankruptcy. They are discussed in Chapter 18.

13

This case is often termed the net-income (NI) approach because investors are assumed to capitalize in-

come after interest at the same rate regardless of financial leverage. In contrast, MM’s approach is a net-

operating-income (NOI) approach because the value of the firm is fundamentally determined by oper-

ating income, the total dollar return to both bondholders and stockholders. This distinction was

emphasized by D. Durand in his important, pre-MM paper, “Cost of Debt and Equity Funds for Busi-

ness: Trends and Problems of Measurement,” in Conference on Research in Business Finance, National Bu-

reau of Economic Research, New York, 1952.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

17. Does Debt policy

Matter?

© The McGraw−Hill

Companies, 2003

That seems naive.

14

The second argument is better. It accepts MM’s reasoning as

applied to perfect capital markets but holds that actual markets are imperfect. Im-

perfections may allow firms that borrow to provide a valuable service for in-

vestors. If so, levered shares might trade at premium prices compared to their the-

oretical values in perfect markets.

Suppose that corporations can borrow more cheaply than individuals. Then it

would pay investors who want to borrow to do so indirectly by holding the stock

of levered firms. They would be willing to live with expected rates of return that

do not fully compensate them for the business and financial risk they bear.

Is corporate borrowing really cheaper? It’s hard to say. Interest rates on home

mortgages are not too different from rates on high-grade corporate bonds.

15

Rates on

margin debt (borrowing from a stockbroker with the investor’s shares tendered as

security) are not too different from the rates firms pay banks for short-term loans.

There are some individuals who face relatively high interest rates, largely because

of the costs lenders incur in making and servicing small loans. There are economies

of scale in borrowing. A group of small investors could do better by borrowing via a

corporation, in effect pooling their loans and saving transaction costs.

16

CHAPTER 17 Does Debt Policy Matter? 479

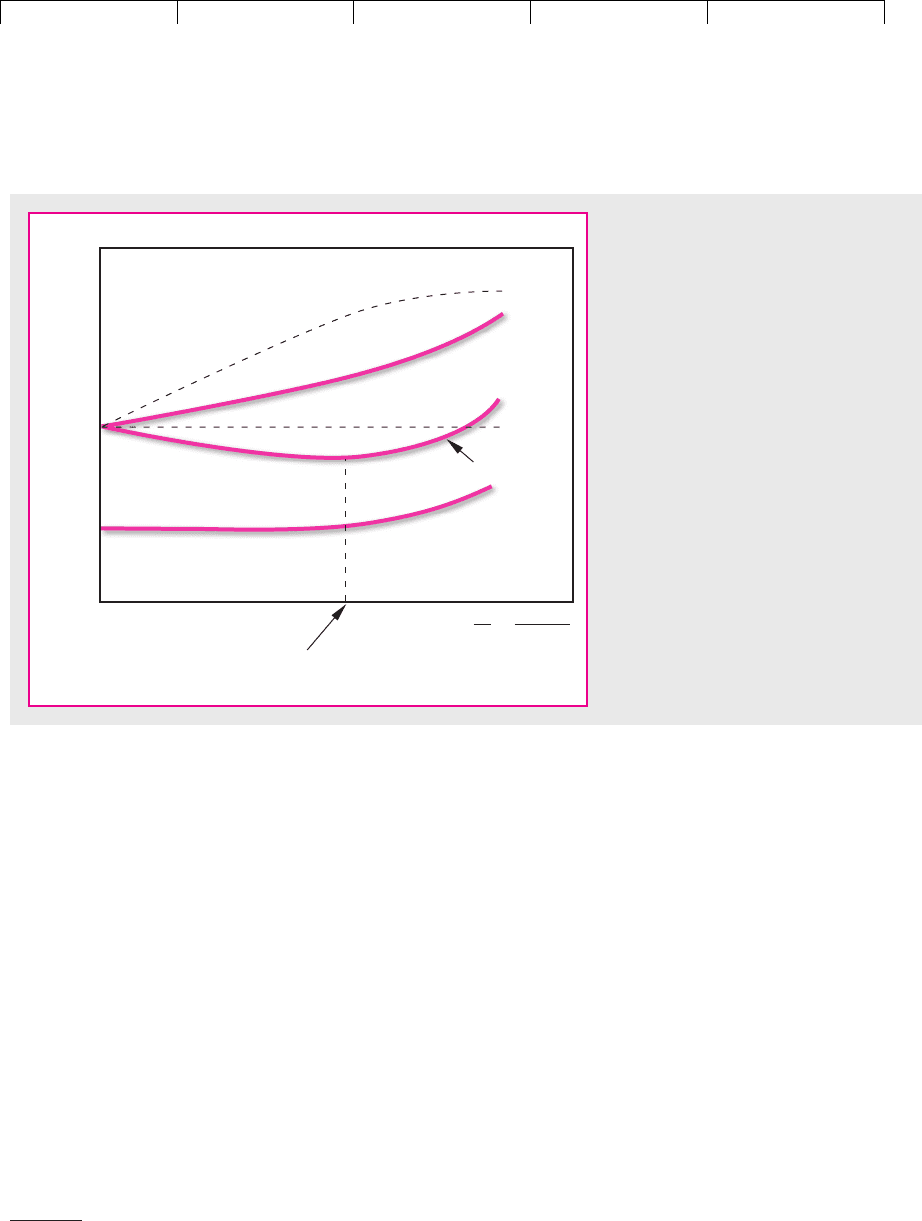

Rates of return

debt

equity

D

E

=

r

E

(MM)

r

E

(traditional)

r

A

(traditional)

r

A

(MM)

r

D

Traditionalists believe there is an optimal

debt–equity ratio that minimizes

r

A

.

FIGURE 17.5

The dashed lines show MM’s view of the

effect of leverage on the expected

return on equity and the weighted-

average cost of capital . (See Figure

17.2.) The solid lines show the traditional

view. Traditionalists say that borrowing

at first increases more slowly than MM

predict but that shoots up with

excessive borrowing. If so, the

weighted-average cost of capital can be

minimized if you use just the right

amount of debt.

r

E

r

E

r

A

r

E

14

This first argument may reflect a confusion between financial risk and the risk of default. Default is

not a serious threat when borrowing is moderate; stockholders worry about it only when the firm goes

“too far.” But stockholders bear financial risk—in the form of increased volatility of rate of return and

higher beta—even when the chance of default is nil. We demonstrated this in Figure 17.3.

15

One of the authors once obtained a home mortgage at a rate

1

⁄2 percentage point less than the contem-

poraneous yield on long-term AAA bonds.

16

Even here there are alternatives to borrowing on personal account. Investors can draw down their sav-

ings accounts or sell a portion of their investment in bonds. The impact of reductions in lending on the

investor’s balance sheet and risk position is exactly the same as increases in borrowing.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

17. Does Debt policy

Matter?

© The McGraw−Hill

Companies, 2003

But suppose that this class of investors is large, both in number and in the aggregate

wealth it brings to capital markets. Shouldn’t the investors’ needs be fully satisfied by

the thousands of levered firms already existing? Is there really an unsatisfied clientele

of small investors standing ready to pay a premium for one more firm that borrows?

Maybe the market for corporate leverage is like the market for automobiles.

Americans need millions of automobiles and are willing to pay thousands of dol-

lars apiece for them. But that doesn’t mean that you could strike it rich by going

into the automobile business. You’re at least 50 years too late.

Where to Look for Violations of MM’s Propositions

MM’s propositions depend on perfect capital markets. We believe capital markets

are generally well-functioning, but they are not 100 percent perfect 100 percent of

the time. Therefore, MM must be wrong some times in some places. The financial

manager’s problem is to figure out when and where.

That is not easy. Just finding market imperfections is insufficient.

Consider the traditionalists’ claim that imperfections make borrowing costly

and inconvenient for many individuals. That creates a clientele for whom corpo-

rate borrowing is better than personal borrowing. That clientele would, in princi-

ple, be willing to pay a premium for the shares of a levered firm.

But maybe it doesn’t have to pay a premium. Perhaps smart financial managers

long ago recognized this clientele and shifted the capital structures of their firms

to meet its needs. The shifts would not have been difficult or costly to make. But if

the clientele is now satisfied, it is no longer willing to pay a premium for levered

shares. Only the financial managers who first recognized the clientele extracted

any advantage from it.

Today’s Unsatisfied Clienteles Are Probably Interested in Exotic Securities

So far we have made little progress in identifying cases where firm value might

plausibly depend on financing. But our examples illustrate what smart financial

managers look for. They look for an unsatisfied clientele, investors who want a par-

ticular kind of financial instrument but because of market imperfections can’t get

it or can’t get it cheaply.

MM’s proposition I is violated when the firm, by imaginative design of its capital

structure, can offer some financial service that meets the needs of such a clientele. Ei-

ther the service must be new and unique or the firm must find a way to provide some

old service more cheaply than other firms or financial intermediaries can.

Now, is there an unsatisfied clientele for garden-variety debt or levered equity?

We doubt it. But perhaps you can invent an exotic security and uncover a latent de-

mand for it.

In the next several chapters we will encounter a number of new securities that

have been invented by companies and advisers. These securities take the com-

pany’s basic cash flows and repackage them in ways that are thought to be more

attractive to investors. However, while inventing these new securities is easy, it is

more difficult to find investors who will rush to buy them.

17

Imperfections and Opportunities

The most serious capital market imperfections are often those created by govern-

ment. An imperfection which supports a violation of MM’s proposition I also cre-

480 PART V

Dividend Policy and Capital Structure

17

We return to the topic of security innovation in Section 25.8.