Brealey, Myers. Principles of Corporate Finance. 7th edition

Подождите немного. Документ загружается.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

18. How Much Should A

Firm Borrow

© The McGraw−Hill

Companies, 2003

How Do Interest Tax Shields Contribute to the Value

of Stockholders’ Equity?

MM’s proposition I amounts to saying that the value of a pie does not depend on

how it is sliced. The pie is the firm’s assets, and the slices are the debt and equity

claims. If we hold the pie constant, then a dollar more of debt means a dollar less

of equity value.

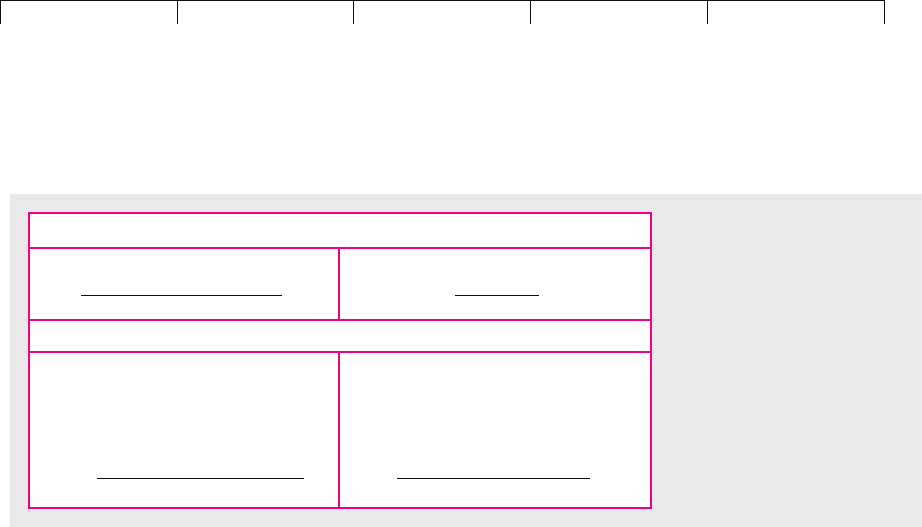

But there is really a third slice, the government’s. Look at Table 18.2. It shows

an expanded balance sheet with pretax asset value on the left and the value of the

government’s tax claim recognized as a liability on the right. MM would still say

that the value of the pie—in this case pretax asset value—is not changed by slic-

ing. But anything the firm can do to reduce the size of the government’s slice ob-

viously makes stockholders better off. One thing it can do is borrow money,

which reduces its tax bill and, as we saw in Table 18.1, increases the cash flows to

debt and equity investors. The after-tax value of the firm (the sum of its debt and

equity values as shown in a normal market value balance sheet) goes up by

PV(tax shield).

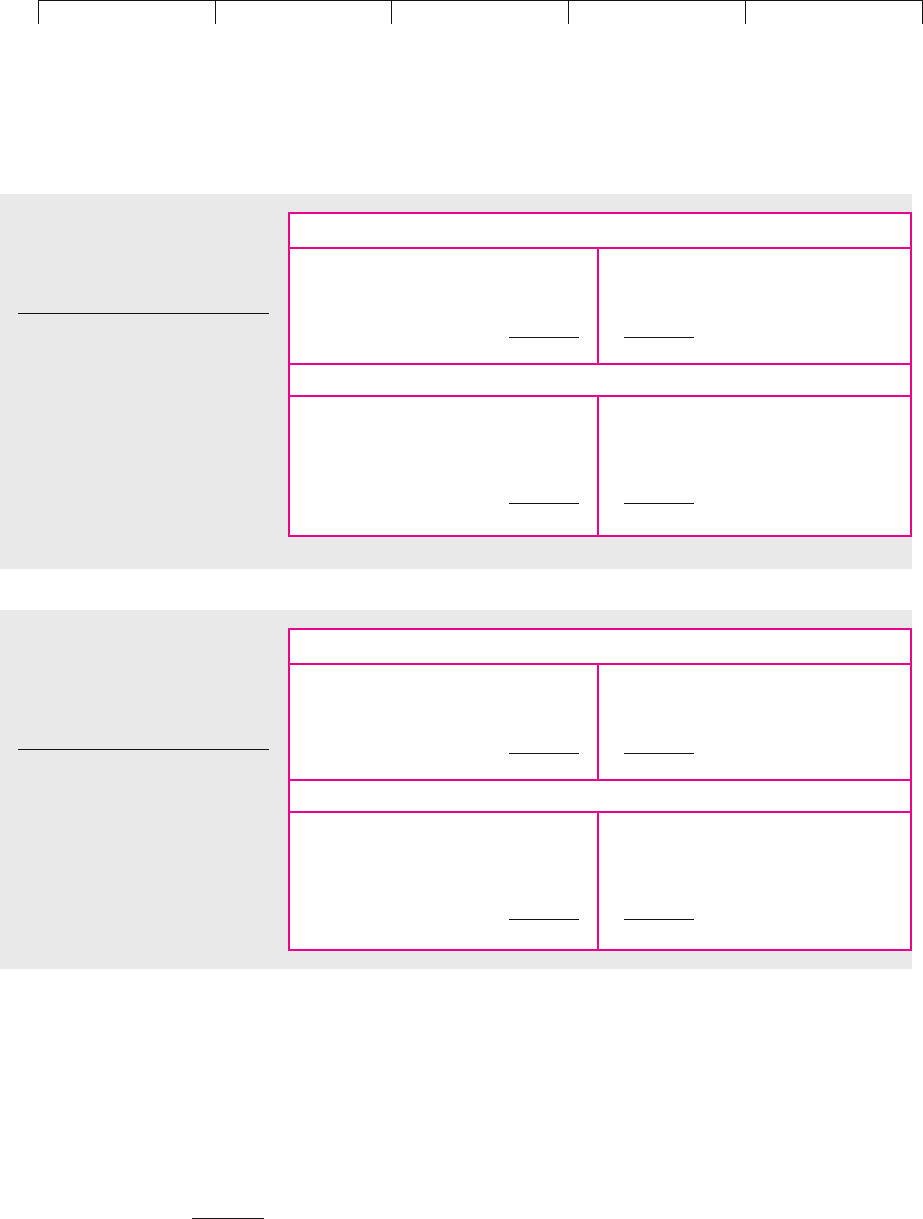

Recasting Pfizer’s Capital Structure

Pfizer, Inc., is a large successful firm that uses essentially no long-term debt. Table

18.3(a) shows simplified book and market value balance sheets for Pfizer as of

year-end 2000.

Suppose that you were Pfizer’s financial manager in 2001 with complete re-

sponsibility for its capital structure. You decide to borrow $1 billion on a perma-

nent basis and use the proceeds to repurchase shares.

Table 18.3(b) shows the new balance sheets. The book version simply has $1,000

million more long-term debt and $1,000 million less equity. But we know that

Pfizer’s assets must be worth more, for its tax bill has been reduced by 35 percent

of the interest on the new debt. In other words, Pfizer has an increase in PV(tax

shield), which is worth . If the MM the-

ory holds except for taxes, firm value must increase by $350 million to $296,247 mil-

lion. Pfizer’s equity ends up worth $289,794 million.

T

c

D ⫽ .35 ⫻ $1,000 million ⫽ $350 million

CHAPTER 18 How Much Should a Firm Borrow? 491

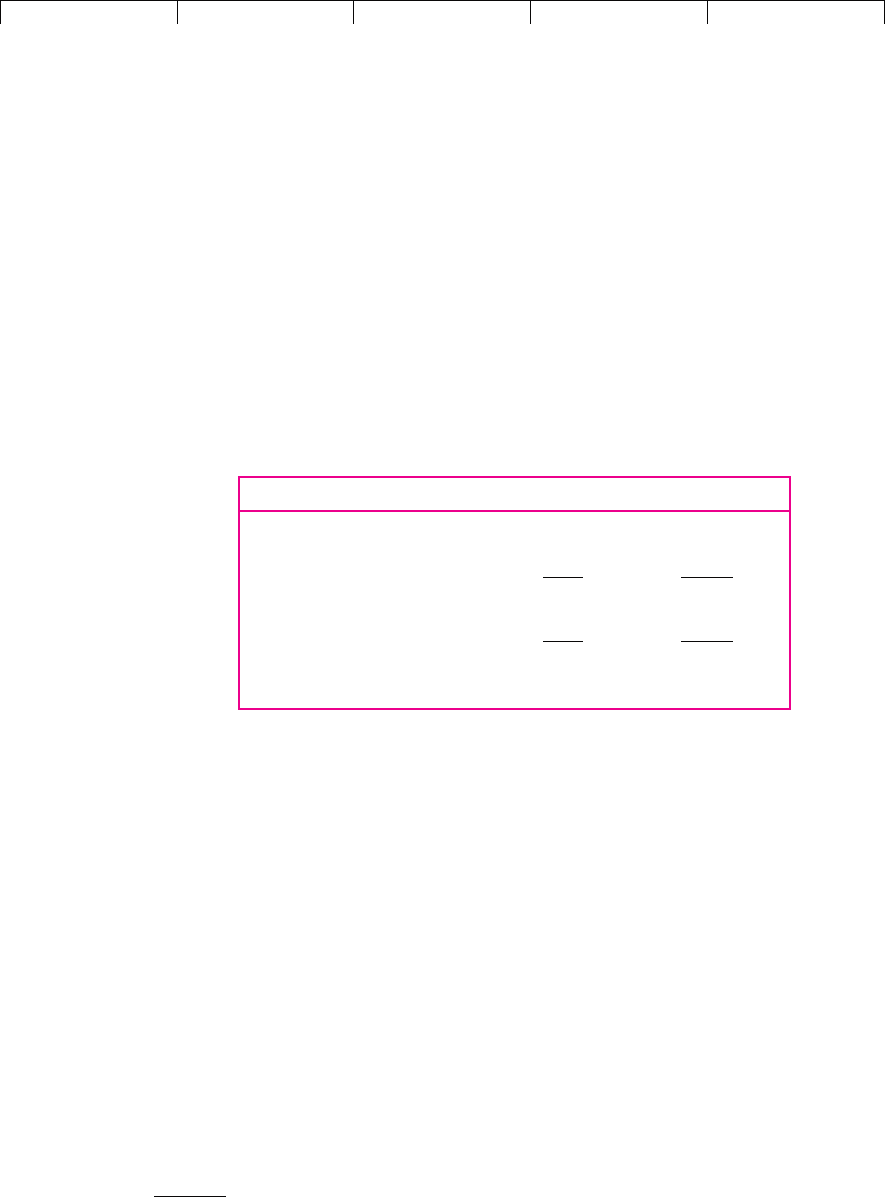

Normal Balance Sheet (Market Values)

Asset value (present value Debt

of after-tax cash flows) Equity

Total assets Total value

Expanded Balance Sheet (Market Values)

Pretax asset value (present Debt

value of pretax cash

flows) Government’s claim

(present value of future

taxes)

Equity

Total pretax assets Total pretax value

TABLE 18.2

Normal and expanded market

value balance sheets. In a

normal balance sheet, assets

are valued after tax. In the

expanded balance sheet, assets

are valued pretax, and the value

of the government’s tax claim is

recognized on the right-hand

side. Interest tax shields are

valuable because they reduce

the government’s claim.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

18. How Much Should A

Firm Borrow

© The McGraw−Hill

Companies, 2003

Now you have repurchased $1,000 million worth of shares, but Pfizer’s equity

value has dropped by only $650 million. Therefore Pfizer’s stockholders must be

$350 million ahead. Not a bad day’s work.

3

MM and Taxes

We have just developed a version of MM’s proposition I as corrected by them to re-

flect corporate income taxes.

4

The new proposition is

492 PART V

Dividend Policy and Capital Structure

Book Values

Net working capital $ 5,206 $ 1,123 Long-term debt

Long-term assets 16,323 4,330 Other long-term

liabilities

16,076 Equity

Total assets $ 21,529 $ 21,529 Total value

Market Values

Net working capital $ 5,206 $ 1,123 Long-term debt

4,330 Other long-term

liabilities

Market value of long-

term assets 290,691 290,444 Equity

Total assets $295,897 $295,897 Total value

TABLE 18.3(a)

Simplified balance sheets for

Pfizer, Inc., December 31, 2000

(figures in millions).

Notes:

1. Market value is equal to book value

for net working capital, long-term

debt, and other long-term liabilities.

Equity is entered at actual market

value: number of shares times closing

price on December 29, 2000. The

difference between the market and

book values of long-term assets is

equal to the difference between the

market and book values of equity.

2. The market value of the long-term

assets includes the tax shield on the

existing debt. This tax shield is

worth ..35 ⫻ 1,123 ⫽ $393

million

Book Values

Net working capital $ 5,206 $ 2,123 Long-term debt

Long-term assets 16,323 4,330 Other long-term

liabilities

15,076 Equity

Total assets $ 21,529 $ 21,529 Total value

Market Values

Net working capital $ 5,206 $ 2,123 Long-term debt

4,330 Other long-term

liabilities

Market value of

long-term assets 291,041 289,794 Equity

Total assets $296,247 $296,247 Total value

TABLE 18.3(b)

Balance sheets for Pfizer, Inc., with

additional $1 billion of long-term

debt substituted for stockholders’

equity (figures in millions).

Notes:

1. The figures in Table 18.3(b) for net

working capital, long-term assets,

and other long-term liabilities are

identical to those in Table 18.3(a).

2. Present value of tax shields assumed

equal to corporate tax rate (35

percent) times additional long-term

debt.

3

Notice that as long as the bonds are sold at a fair price, all the benefits from the tax shield go to the

shareholders.

4

Interest tax shields are recognized in MM’s original article, F. Modigliani and M. H. Miller, “The Cost

of Capital, Corporation Finance and the Theory of Investment,” American Economic Review 48 (June

1958), pp. 261–296. The valuation procedure used in Table 18.3(b) is presented in their 1963 article “Cor-

porate Income Taxes and the Cost of Capital: A Correction,” American Economic Review 53 (June 1963),

pp. 433–443.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

18. How Much Should A

Firm Borrow

© The McGraw−Hill

Companies, 2003

In the special case of permanent debt,

Our imaginary financial surgery on Pfizer provides the perfect illustration of the

problems inherent in this “corrected” theory. That $350 million came too easily;

it seems to violate the law that there is no such thing as a money machine. And

if Pfizer’s stockholders would be richer with $2,123 million of corporate debt,

why not $3,123 or $17,199 million?

5

Our formula implies that firm value and

stockholders’ wealth continue to go up as D increases. The optimal debt policy

appears to be embarrassingly extreme. All firms should be 100 percent debt-

financed.

MM were not that fanatical about it. No one would expect the formula to apply

at extreme debt ratios. There are several reasons why our calculations overstate the

value of interest tax shields. First, it’s wrong to think of debt as fixed and perpet-

ual; a firm’s ability to carry debt changes over time as profits and firm value fluc-

tuate.

6

Second, many firms face marginal tax rates less than 35 percent. Third, you

can’t use interest tax shields unless there will be future profits to shield—and no

firm can be absolutely sure of that.

But none of these qualifications explains why firms like Pfizer not only exist but

also thrive with no debt at all. It is hard to believe that the management of Pfizer is

simply missing the boat.

Therefore we have argued ourselves into a corner. There are just two ways out:

1. Perhaps a fuller examination of the U.S. system of corporate and personal

taxation will uncover a tax disadvantage of corporate borrowing, offsetting

the present value of the corporate tax shield.

2. Perhaps firms that borrow incur other costs—bankruptcy costs, for

example—offsetting the present value of the tax shield.

We will now explore these two escape routes.

Value of firm ⫽ value if all-equity-financed ⫹ T

c

D

Value of firm ⫽ value if all-equity-financed ⫹ PV1tax shield2

CHAPTER 18 How Much Should a Firm Borrow? 493

5

The last figure would correspond to a 100 percent book debt ratio. But Pfizer’s market value would be

$301,524 million according to our formula for firm value. Pfizer’s common shares would have an ag-

gregate value of $279,995 million.

6

The valuation of interest tax shields is discussed again in Section 19.4. Our calculation here adheres to

Chapter 19’s “Financing Rule 1,” which assumes that debt is fixed regardless of future performance of

the project or the firm.

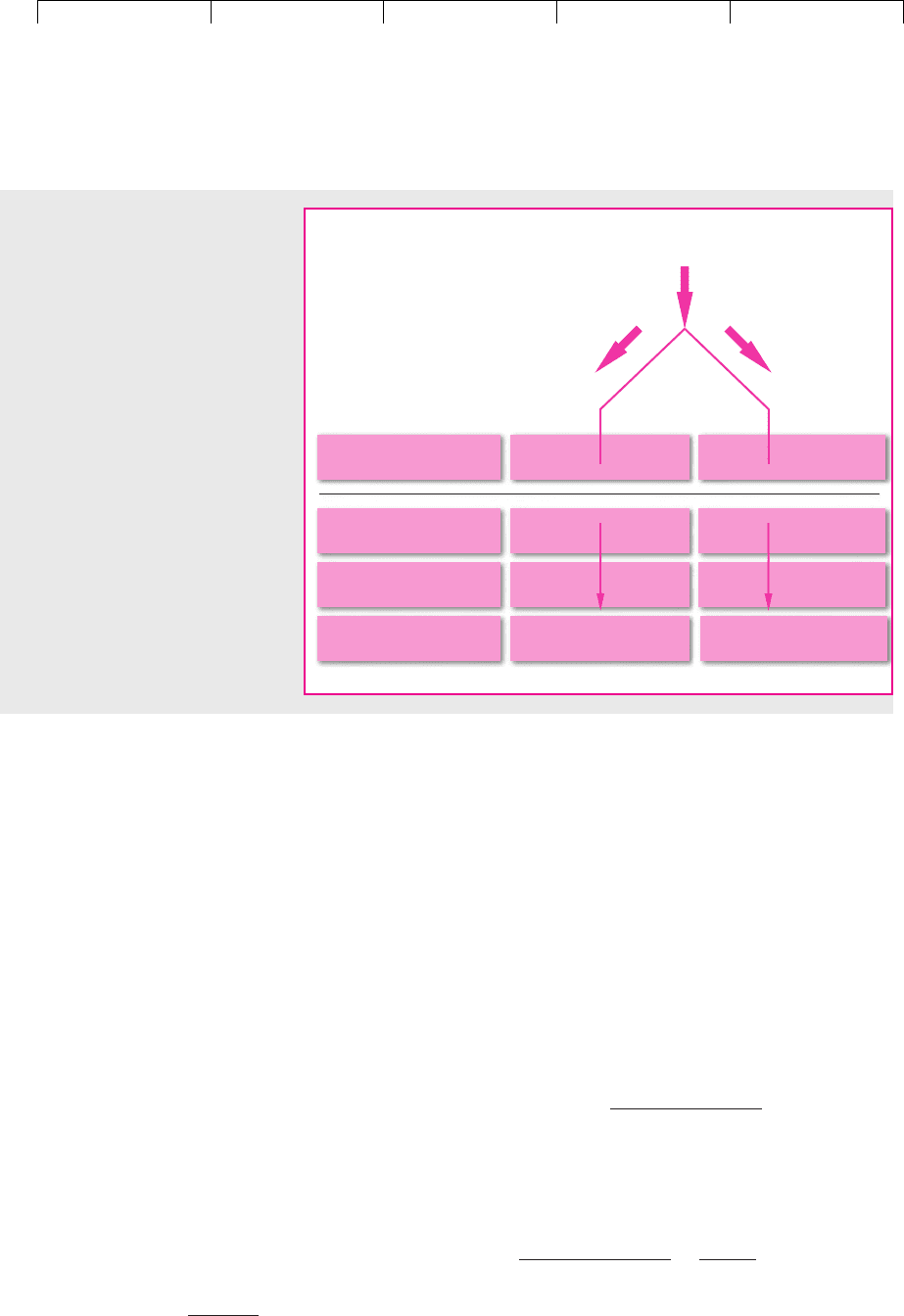

18.2 CORPORATE AND PERSONAL TAXES

When personal taxes are introduced, the firm’s objective is no longer to minimize

the corporate tax bill; the firm should try to minimize the present value of all taxes

paid on corporate income. “All taxes” include personal taxes paid by bondholders

and stockholders.

Figure 18.1 illustrates how corporate and personal taxes are affected by lever-

age. Depending on the firm’s capital structure, a dollar of operating income will

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

18. How Much Should A

Firm Borrow

© The McGraw−Hill

Companies, 2003

accrue to investors either as debt interest or equity income (dividends or capital

gains). That is, the dollar can go down either branch of Figure 18.1.

Notice that Figure 18.1 distinguishes between , the personal tax rate on inter-

est, and , the effective personal rate on equity income. The two rates are equal if

equity income comes entirely as dividends. But can be less than if equity in-

come comes as capital gains. In 2001 the top rate on ordinary income, including in-

terest and dividends, was 39.1 percent. The rate on realized capital gains was 20 per-

cent.

7

However, capital gains taxes can be deferred until shares are sold, so the top

effective capital gains rate can be less than 20 percent.

The firm’s objective should be to arrange its capital structure so as to maximize

after-tax income. You can see from Figure 18.1 that corporate borrowing is better if

( ) is more than ; otherwise it is worse. The relative tax

advantage of debt over equity is

This suggests two special cases. First, suppose all equity income comes as divi-

dends. Then debt and equity income are taxed at the same effective personal rate.

But with , the relative advantage depends only on the corporate rate:

Relative advantage ⫽

1 ⫺ T

p

11 ⫺ T

pE

211 ⫺ T

c

2

⫽

1

1 ⫺ T

c

T

pE

⫽ T

p

Relative tax advantage of debt ⫽

1 ⫺ T

p

11 ⫺ T

pE

211 ⫺ T

c

2

11 ⫺ T

pE

2⫻ 11 ⫺ T

c

21 ⫺ T

p

T

p

T

pE

T

pE

T

p

494 PART V Dividend Policy and Capital Structure

Corporate tax

Operating income

$1.00

Paid out as

interest

Or paid out as

equity income

None

T

c

Income after

corporate tax

$1.00 $1.00

–

T

c

Personal tax

To bondholder To stockholder

T

p

T

pE

(1.00

–

T

c

)

1.00

–

T

c

–

T

p

E

(1.00

–

T

c

)

=(1.00

–

T

p

E

)(1.00

–

T

c

)

(1.00

–

T

p

)

Income after all taxes

FIGURE 18.1

The firm’s capital structure deter-

mines whether operating income is

paid out as interest or equity income.

Interest is taxed only at the personal

level. Equity income is taxed at both

the corporate and the personal

levels. However, , the personal tax

rate on equity income, can be less

than , the personal tax rate on

interest income.

T

p

T

pE

7

See Section 16.6 for details. Note that we are simplifying by ignoring those corporate investors, such

as banks, which pay top rates on capital gains of 35 percent.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

18. How Much Should A

Firm Borrow

© The McGraw−Hill

Companies, 2003

In this case, we can forget about personal taxes. The tax advantage of corporate

borrowing is exactly as MM calculated it.

8

They do not have to assume away per-

sonal taxes. Their theory of debt and taxes requires only that debt and equity be

taxed at the same rate.

The second special case occurs when corporate and personal taxes cancel to

make debt policy irrelevant. This requires

This case can happen only if , the corporate rate, is less than the personal rate

and if , the effective rate on equity income, is small. Merton Miller explored this

situation at a time when tax rates in the United States were very different from to-

day, but we won’t go into the details of his analysis here.

9

In any event we seem to have a simple, practical decision rule. Arrange the firm’s

capital structure to shunt operating income down that branch of Figure 18.1 where the

tax is least. Unfortunately that is not as simple as it sounds. What’s , for example?

The shareholder roster of any large corporation is likely to include tax-exempt in-

vestors (such as pension funds or university endowments) as well as millionaires. All

possible tax brackets will be mixed together. And it’s the same with , the personal

tax rate on interest. The large corporation’s “typical” bondholder might be a tax-

exempt pension fund, but many taxpaying investors also hold corporate debt.

Some investors may be much happier to buy your debt than others. For exam-

ple, you should have no problems inducing pension funds to lend; they don’t have

to worry about personal tax. But taxpaying investors may be more reluctant to hold

debt and will be prepared to do so only if they are compensated by a high rate of

interest. Investors paying tax on interest at the top rate of 39.1 percent may be par-

ticularly unwilling to hold debt. They will prefer to hold common stock or munic-

ipal bonds whose interest is exempt from tax.

To determine the net tax advantage of debt, companies would need to know the

tax rates faced by the marginal investor—that is, an investor who is equally happy

to hold debt or equity. This makes it hard to put a precise figure on the tax benefit,

but we can nevertheless provide a back-of-the-envelope calculation. One way to

estimate the tax rate of the marginal debt investor is to see how much yield in-

vestors are prepared to give up when they invest in tax-exempt municipal bonds.

As we write this in August 2001, short-term municipals yield 2.49 percent, while

similar Treasury bonds yield 3.71 percent. An investor with a personal tax rate of

33 percent would receive exactly the same after-tax interest from the two securities

and would be equally happy to hold them.

10

T

p

T

pE

T

pE

T

p

T

c

1 ⫺ T

p

⫽ 11 ⫺ T

pE

211 ⫺ T

c

2

CHAPTER 18 How Much Should a Firm Borrow? 495

8

Of course, personal taxes reduce the dollar amount of corporate interest tax shields, but the appropri-

ate discount rate for cash flows after personal tax is also lower. If investors are willing to lend at a

prospective return before personal taxes of , then they must also be willing to accept a return after per-

sonal taxes of , where is the marginal rate of personal tax. Thus we can compute the value

after personal taxes of the tax shield on permanent debt:

This brings us back to our previous formula for firm value:

9

See M. H. Miller, “Debt and Taxes,” Journal of Finance 32 (May 1977), pp. 261–276.

10

That is, .11 ⫺ .332⫻ 3.71 ⫽ 2.49 percent

Value of firm ⫽ value if all-equity-financed ⫹ T

c

D

PV1tax shield2⫽

T

c

⫻ 1r

D

D2⫻ 11 ⫺ T

p

2

r

D

⫻ 11 ⫺ T

p

2

⫽ T

c

D

T

p

r

D

11 ⫺ T

p

2

r

D

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

18. How Much Should A

Firm Borrow

© The McGraw−Hill

Companies, 2003

To work out how much tax such an investor would pay on equity income, we

need to know the proportion of income that is in the form of capital gains and the

tax that is paid on these gains. Companies currently (2001) pay out on average 28

percent of their earnings. So for each $1.00 of equity income, $.28 consists of divi-

dends and the balance of $.72 comprises capital gains. We assume that by not real-

izing these capital gains immediately, investors can cut the effective tax to one-half

the statutory rate on realized gains, that is, .

11

Therefore, if our

marginal investor invests in common stock, the tax on each $1.00 of equity income

is .

Now we can calculate the effect of shunting a dollar of income down each of the

two branches in Figure 18.1:

T

pE

⫽ 1.28 ⫻ .332⫹ 1.72 ⫻ .102⫽ .16

20/2 ⫽ 10 percent

496 PART V Dividend Policy and Capital Structure

11

For an analysis of the effective rate of capital gains tax, see R. C. Green and B. Hollifield, “The Per-

sonal Tax Advantages of Equity,” working paper, Graduate School of Industrial Administration,

Carnegie Mellon University, January 2001.

12

For a discussion of these and other tax shields on company borrowing, see H. DeAngelo and R. Ma-

sulis, “Optimal Capital Structure under Corporate and Personal Taxation,” Journal of Financial Econom-

ics 8 (March 1980), pp. 5–29.

13

For some evidence on the average marginal tax rate of U.S. firms, see J. R. Graham, “Debt and the Mar-

ginal Tax Rate,” Journal of Financial Economics 41 (May 1996), pp. 41–73, and “Proxies for the Corporate

Marginal Tax Rate,” Journal of Financial Economics 42 (October 1996), pp. 187–221.

Interest Equity Income

Income before tax $1.00 $1.00

Less corporate tax

at 0 .35

Income after corporate tax 1.00 .65

Personal tax at

and .33 .107

Income after all taxes $ .67 $ .543

Advantage to debt ⫽ $.127

T

pE

⫽ .16

T

p

⫽ .33

T

c

⫽ .35

The advantage to debt financing appears to be about $.13 on the dollar.

We should emphasize that our back-of-the-envelope calculation is just that. Econ-

omists have come up with differing figures for the tax rate of the marginal

debtholder and the effective rate of capital gains tax. These estimates may give

higher or lower figures for the tax advantage of debt. Also our calculation of the ben-

efits of debt financing assumed that the firm could be confident that it would have

sufficient income to shield. In practice few firms can be sure they will show a taxable

profit in the future. If a firm shows a loss and cannot carry the loss back against past

taxes, its interest tax shield must be carried forward with the hope of using it later.

The firm loses the time value of money while it waits. If its difficulties are deep

enough, the wait may be permanent and the interest tax shield may be lost forever.

Notice also that borrowing is not the only way to shield income against tax.

Firms have accelerated write-offs for plant and equipment. Investment in many in-

tangible assets can be expensed immediately. So can contributions to the firm’s

pension fund. The more that firms shield income in these ways, the lower is the ex-

pected shield from corporate borrowing.

12

Even if the firm is confident that it will

earn a taxable profit with the current level of debt, it is unlikely to be so positive if

the amount of debt is increased.

13

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

18. How Much Should A

Firm Borrow

© The McGraw−Hill

Companies, 2003

Thus corporate tax shields are worth more to some firms than to others. Firms

with plenty of noninterest tax shields and uncertain future profits should borrow

less than consistently profitable firms with lots of taxable profits to shield. Firms

with large accumulated tax-loss carry-forwards shouldn’t borrow at all. Why

should such a firm pay a high rate of interest to induce taxpaying investors to hold

its debt when it can’t use interest tax shields? All this suggests that there is a mod-

erate tax advantage to corporate borrowing, at least for companies that are rea-

sonably sure they can use the corporate tax shields. For companies that do not ex-

pect corporate tax shields there is probably a moderate tax disadvantage.

Do companies make full use of interest tax shields? John Graham argues that

they don’t. His estimates suggest that for the typical firm unused tax shields are

worth nearly 5 percent of company value.

14

Presumably, well-established compa-

nies like Pfizer, with effectively no long-term debt, are leaving even more money

on the table. It seems either that managers of these firms are missing out or that

there are some offsetting disadvantages to increased borrowing. We will now ex-

plore this second escape route.

CHAPTER 18

How Much Should a Firm Borrow? 497

14

Graham’s estimates for individual firms recognize both the uncertainty in future profits and the exis-

tence of noninterest tax shields. See J. R. Graham, “How Big Are the Tax Benefits of Debt?” Journal of Fi-

nance 55 (October 2000), pp. 1901–1941.

18.3 COSTS OF FINANCIAL DISTRESS

Financial distress occurs when promises to creditors are broken or honored with

difficulty. Sometimes financial distress leads to bankruptcy. Sometimes it only

means skating on thin ice.

As we will see, financial distress is costly. Investors know that levered firms may

fall into financial distress, and they worry about it. That worry is reflected in the

current market value of the levered firm’s securities. Thus, the value of the firm can

be broken down into three parts:

The costs of financial distress depend on the probability of distress and the mag-

nitude of costs encountered if distress occurs.

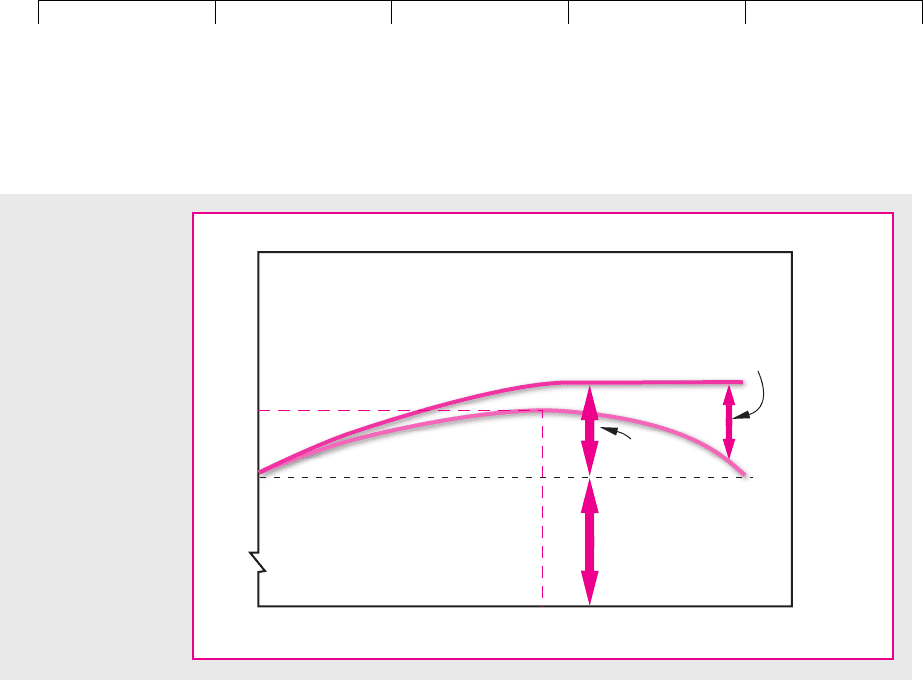

Figure 18.2 shows how the trade-off between the tax benefits and the costs of

distress determines optimal capital structure. PV(tax shield) initially increases as

the firm borrows more. At moderate debt levels the probability of financial distress

is trivial, and so PV(cost of financial distress) is small and tax advantages domi-

nate. But at some point the probability of financial distress increases rapidly with

additional borrowing; the costs of distress begin to take a substantial bite out of

firm value. Also, if the firm can’t be sure of profiting from the corporate tax shield,

the tax advantage of additional debt is likely to dwindle and eventually disappear.

The theoretical optimum is reached when the present value of tax savings due to

further borrowing is just offset by increases in the present value of costs of distress.

This is called the trade-off theory of capital structure.

Costs of financial distress cover several specific items. Now we identify these costs

and try to understand what causes them.

Value

of firm

⫽

value if

all-equity-financed

⫹ PV1tax shield2⫺

PV 1costs of

financial 1distress2

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

18. How Much Should A

Firm Borrow

© The McGraw−Hill

Companies, 2003

Bankruptcy Costs

You rarely hear anything nice said about corporate bankruptcy. But there is some

good in almost everything. Corporate bankruptcies occur when stockholders ex-

ercise their right to default. That right is valuable; when a firm gets into trouble, lim-

ited liability allows stockholders simply to walk away from it, leaving all its trou-

bles to its creditors. The former creditors become the new stockholders, and the old

stockholders are left with nothing.

In our legal system all stockholders in corporations automatically enjoy limited

liability. But suppose that this were not so. Suppose that there are two firms with

identical assets and operations. Each firm has debt outstanding, and each has

promised to repay $1,000 (principal and interest) next year. But only one of the

firms, Ace Limited, enjoys limited liability. The other firm, Ace Unlimited, does

not; its stockholders are personally liable for its debt.

Figure 18.3 compares next year’s possible payoffs to the creditors and stock-

holders of these two firms. The only differences occur when next year’s asset value

turns out to be less than $1,000. Suppose that next year the assets of each company

are worth only $500. In this case Ace Limited defaults. Its stockholders walk away;

their payoff is zero. Bondholders get the assets worth $500. But Ace Unlimited’s

stockholders can’t walk away. They have to cough up $500, the difference between

asset value and the bondholders’ claim. The debt is paid whatever happens.

Suppose that Ace Limited does go bankrupt. Of course, its stockholders are dis-

appointed that their firm is worth so little, but that is an operating problem having

nothing to do with financing. Given poor operating performance, the right to go

bankrupt—the right to default—is a valuable privilege. As Figure 18.3 shows, Ace

Limited’s stockholders are in better shape than Unlimited’s are.

The example illuminates a mistake people often make in thinking about the

costs of bankruptcy. Bankruptcies are thought of as corporate funerals. The mourn-

498 PART V

Dividend Policy and Capital Structure

Market value

PV(costs

of financial

distress)

PV(tax

shield)

Value if

all-equity-

financed

Debt ratio

Optimal

debt ratio

FIGURE 18.2

The value of the firm

is equal to its value if

all-equity-financed

plus PV(tax shield)

minus PV(costs of

financial distress).

According to the

trade-off theory of

capital structure, the

manager should

choose the debt ratio

that maximizes firm

value.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

18. How Much Should A

Firm Borrow

© The McGraw−Hill

Companies, 2003

ers (creditors and especially shareholders) look at their firm’s present sad state.

They think of how valuable their securities used to be and how little is left. More-

over, they think of the lost value as a cost of bankruptcy. That is the mistake. The

decline in the value of assets is what the mourning is really about. That has no nec-

essary connection with financing. The bankruptcy is merely a legal mechanism for

allowing creditors to take over when the decline in the value of assets triggers a de-

fault. Bankruptcy is not the cause of the decline in value. It is the result.

Be careful not to get cause and effect reversed. When a person dies, we do not

cite the implementation of his or her will as the cause of death.

We said that bankruptcy is a legal mechanism allowing creditors to take over

when a firm defaults. Bankruptcy costs are the costs of using this mechanism.

CHAPTER 18

How Much Should a Firm Borrow? 499

Payoff to

bondholders

ACE LIMITED

(limited liability)

1,000

500

500 1,000

Payoff

Asset

value

Payoff to

bondholders

ACE UNLIMITED

(unlimited liability)

1,000

500 1,000

Payoff

Asset

value

Payoff to

stockholders

1,000

–1,000

0

500 1,000

Payoff

Asset

value

Payoff to

stockholders

1,000

–1,000

–500

0

500 1,000

Payoff

Asset

value

FIGURE 18.3

Comparison of limited and unlimited liability for two otherwise identical firms. If the two firms’ asset values

are less than $1,000, Ace Limited stockholders default and its bondholders take over the assets. Ace

Unlimited stockholders keep the assets, but they must reach into their own pockets to pay off its bond-

holders. The total payoff to both stockholders and bondholders is the same for the two firms.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

V. Dividend Policy and

Capital Structure

18. How Much Should A

Firm Borrow

© The McGraw−Hill

Companies, 2003

There are no bankruptcy costs at all shown in Figure 18.3. Note that only Ace Lim-

ited can default and go bankrupt. But, regardless of what happens to asset value,

the combined payoff to the bondholders and stockholders of Ace Limited is always

the same as the combined payoff to the bondholders and stockholders of Ace Un-

limited. Thus the overall market values of the two firms now (this year) must be

identical. Of course, Ace Limited’s stock is worth more than Ace Unlimited’s stock

because of Ace Limited’s right to default. Ace Limited’s debt is worth correspond-

ingly less.

Our example was not intended to be strictly realistic. Anything involving courts

and lawyers cannot be free. Suppose that court and legal fees are $200 if Ace Lim-

ited defaults. The fees are paid out of the remaining value of Ace’s assets. Thus if

asset value turns out to be $500, creditors end up with only $300. Figure 18.4 shows

next year’s total payoff to bondholders and stockholders net of this bankruptcy

cost. Ace Limited, by issuing risky debt, has given lawyers and the court system a

claim on the firm if it defaults. The market value of the firm is reduced by the pres-

ent value of this claim.

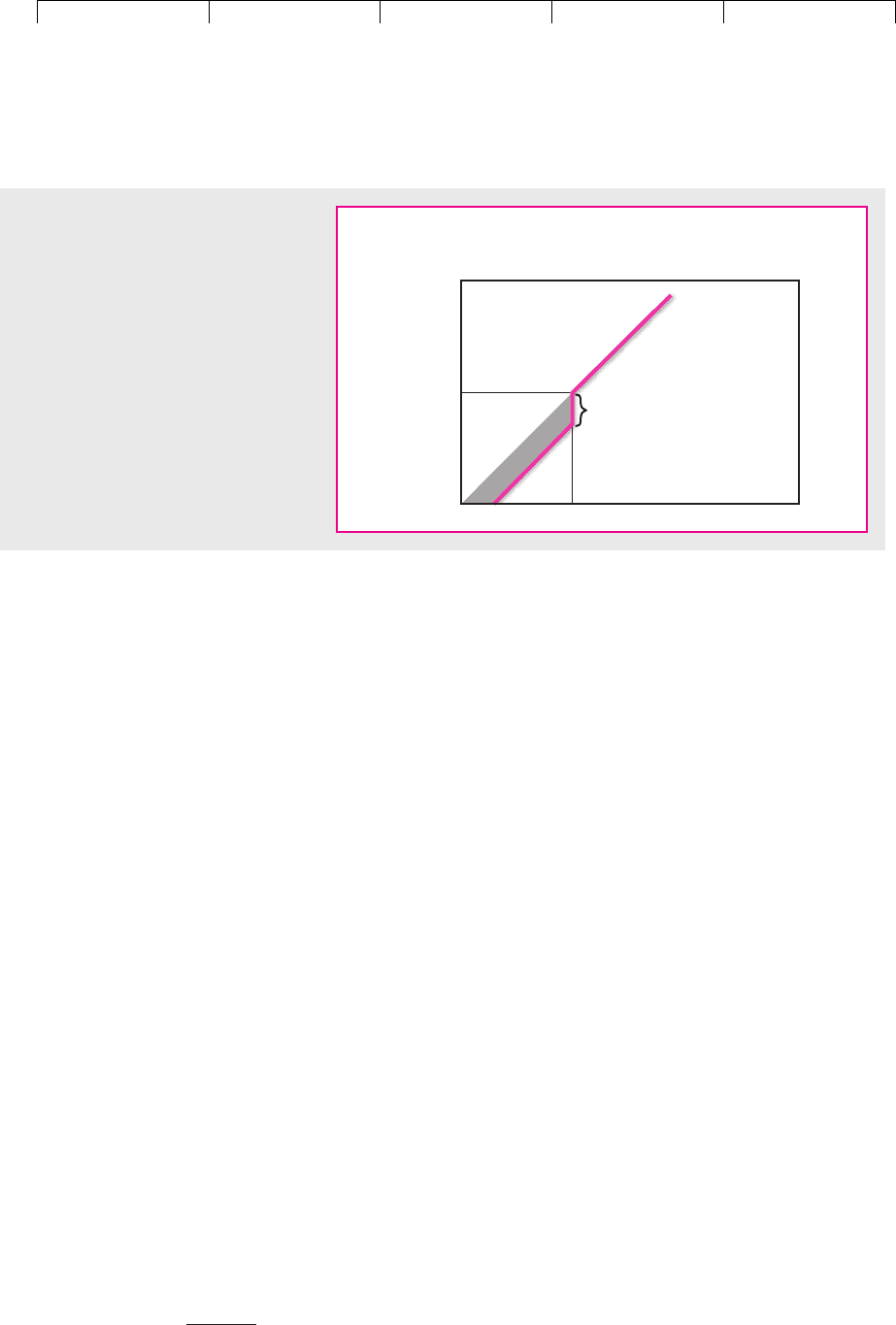

It is easy to see how increased leverage affects the present value of the costs of

financial distress. If Ace Limited borrows more, it increases the probability of de-

fault and the value of the lawyers’ claim. It increases PV (costs of financial distress)

and reduces Ace’s present market value.

The costs of bankruptcy come out of stockholders’ pockets. Creditors foresee the

costs and foresee that they will pay them if default occurs. For this they demand

compensation in advance in the form of higher payoffs when the firm does not de-

fault; that is, they demand a higher promised interest rate. This reduces the possi-

ble payoffs to stockholders and reduces the present market value of their shares.

Evidence on Bankruptcy Costs

Bankruptcy costs can add up fast. Manville, which declared bankruptcy in 1982 be-

cause of expected liability for asbestos-related health claims, spent $200 million on

fees before it emerged from bankruptcy in 1988.

15

While Eastern Airlines was in

500 PART V

Dividend Policy and Capital Structure

Combined payoff

to bondholders

and stockholders

1,000

200 1,000

Payoff

Asset

value

(Promised

payment to

bondholders)

200 Bankruptcy cost

FIGURE 18.4

Total payoff to Ace Limited security

holders. There is a $200 bankruptcy cost

in the event of default (shaded area).

15

S. P. Sherman, “Bankruptcy’s Spreading Blight,” Fortune, June 3, 1991, pp. 123–132.