ACCA - P5 Study text - Emile Woolf INT - 2010

Подождите немного. Документ загружается.

Chapter 12: Performance measurement systems

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 275

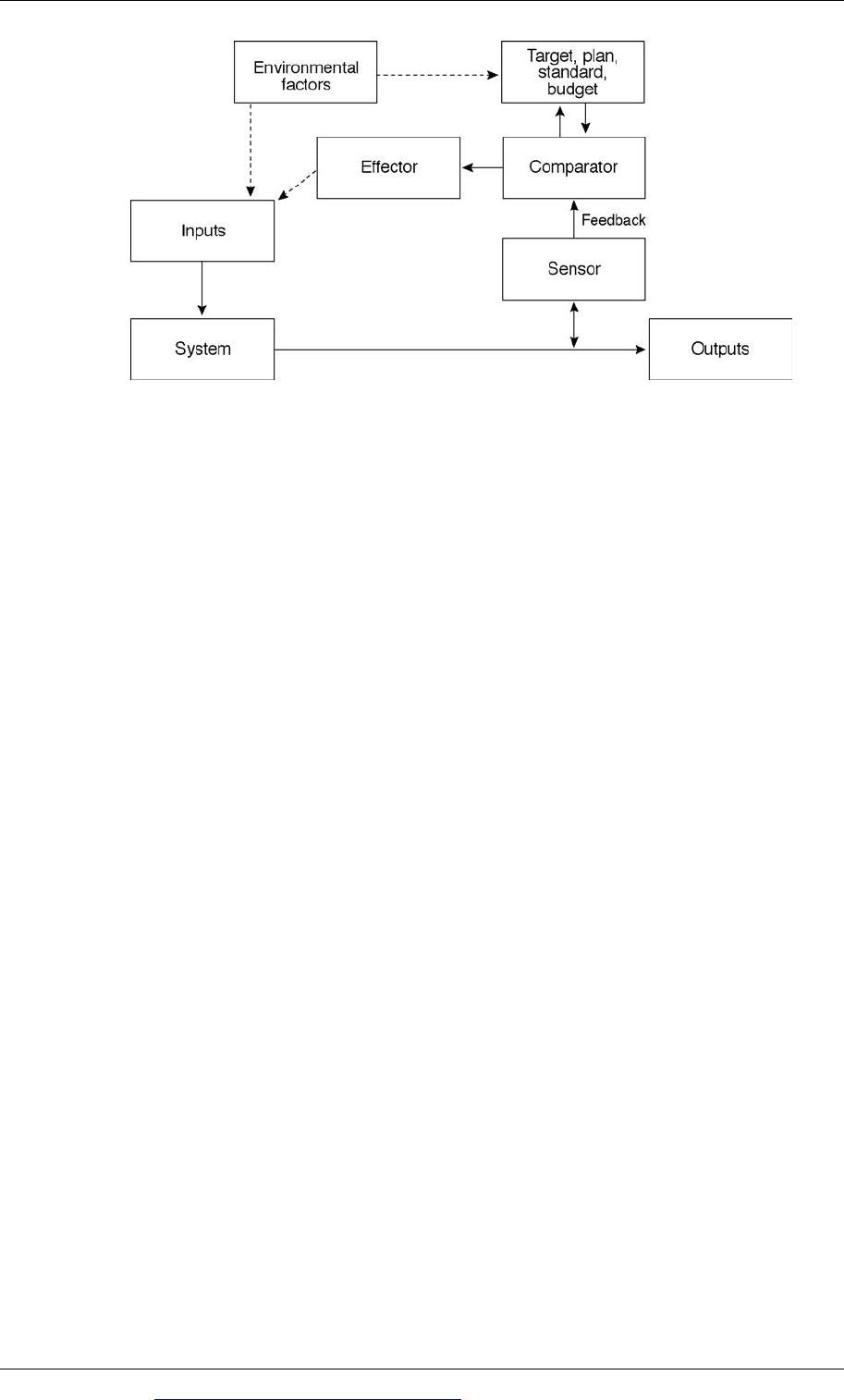

System

A system can be any operation or activity. It can be an entire business entity. A

system can be anything that is subject to planning and control. In this diagram, the

control information is measure output from the system itself. In this sense it is a

closed system

Inputs

Every system has inputs. In a business operation, inputs include resources –

materials, equipment, labour and cash. Inputs are used within a system to produce

outputs. Some inputs are controllable by management. Other inputs are not

controllable, and may be subject to influence from environmental factors.

For example, raw material prices are inputs to a production system. Materials prices

might be controllable to some extent, by efficient purchasing. However, materials

prices are often outside the control of management, and are affected by

environmental factors such as inflation rates and materials supply shortages.

Outputs

Every system produces outputs. Some outputs are planned. For example, outputs

from a business operation include the volume of production and sales. Some

outputs can be quantified; others are more difficult to quantify. For example, the

outputs from a business operation include the morale and satisfaction of the

workforce, and customer satisfaction.

Sensor

Outputs from a system are measured. However, not all outputs are measured.

Outputs are measured only if:

they are measurable and

if the control system has a procedure for measuring them.

Paper P5: Advanced performance management

276 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

For example, in the case of a business operation, measured outputs will include

sales, costs and profit. Other measured outputs might include the efficiency of

resource utilisation and capacity utilisation. Outputs that might or might not be

measured include customer satisfaction, the quality of output and employee

satisfaction. Management can decide what measurable outputs should be measured

and fed back as information for the purpose of performance assessment.

Feedback

Feedback is measured information that is reported back to management for control

purposes.

Comparator

A comparator compares measured outputs (feedback) with a target, plan or

standard. Performance has to be measured against expected performance or target

performance, to assess whether it is satisfactory. Where actual performance differs

from the plan, it may be necessary to amend the plan or change the target.

However, the comparison of actual performance with plan might suggest that action

can be taken to improve future performance.

Effector

Control action is taken through an effector mechanism. An effector makes

adjustments to the inputs to the system, so that future outputs will be changed.

An effector might take the form of management instructions to employees. For

example, the quality of output is low and the rate of rejected units in a production

process might be too high. On receiving feedback about the low quality of work,

management might try to take measures to improve the situation – by employing

more people in the work and instructing them to take more time and more care over

their work.

It is important to recognise, however, that the effectors in a control system can only

apply to controllable inputs to the system. Uncontrollable inputs, and inputs that

are subject to environmental influence, cannot be controlled.

3.3 Feed-forward and double loop feedback

Strategic planning and control information is often:

feed-forward control information, or

double-loop feedback information.

Feed-forward

Feed-forward control information is forward-looking control information. It

compares:

the target performance and

the latest forecast of what actual performance will be.

Chapter 12: Performance measurement systems

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 277

For example, the directors of a retail store company might obtain control

information in September comparing the targeted sales for the company for the year

to 31st December, and the latest forecast of what sales for the year will be. If the

forecast is below the target, the directors will study the difference (the ‘gap’)

between target and current forecast, and consider measures to close the gap.

A feed-forward system of control information is an alternative to a feedback system.

In management accounting, feedback systems are often associated with budgetary

control. Feed-forward systems are associated with decentralised decision-making,

and techniques such as continuous budgeting.

Double-loop feedback

Feedback is control information reported to the manager responsible, comparing

actual performance in a period with the target or budget for that period. In other

words, feedback compares actual results with a plan for the benefit of the manager

directly responsible for control. Double-loop feedback is control information

comparing actual results with the plan that is reported to a higher level of

management. Senior managers can use double-loop feedback to:

assess the performance of the managers responsible and

where appropriate, consider making changes to the budget or plan.

3.4 Using control system theory

Control system theory can be useful in providing a framework for the analysis of

control systems and performance measurement systems. Each aspect of a control

system can be reviewed, to decide whether it is appropriate or sufficient. For

example, it provides a framework for asking questions such as:

Are the targets or plans for the system suitable? Should there be different targets

or more targets for achievement?

Does the information system currently measure enough, or should it be

measuring other outputs from the system. Are the sensors used to measure the

outputs adequate? Is the feedback provided in an appropriate form?

Is the feedback being sent to the most appropriate individuals?

Are the effectors appropriate? Is enough control action being taken? To what

extent is management able to control the inputs to the system?

3.5 Information from internal sources

A control system such as a management accounting system must obtain data from

within the organisation (from internal sources) for the purposes of planning and

control. The system should be designed so that it captures and measures all the data

required for providing management with the information they need.

It is useful to remember the essential qualities of good information.

It should be relevant to the needs of management. Information must help

management to make decisions. Information that is not relevant to any decision-

making (such as planning and control decisions) is of no value. An important

Paper P5: Advanced performance management

278 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

factor in the design of information systems should be the purpose of the

information. What decisions should be made, and what information will be

needed to make those decisions.

It should be reliable. This means that the data should be sufficiently accurate for

its purpose. It should also be complete.

It should be available in a timely manner. In other words, it should be available

for when it is needed by management.

The cost of providing the information should not exceed the benefits that it

provides. The key factor that limits the potential size of many information

systems is that the cost of obtaining additional information is not justified by the

additional benefits that the information will provide.

In designing a performance measurement system, and deciding what information is

required from internal sources, these desirable qualities of good information should

influence the design of the system.

Traditionally, management accounting systems have obtained internal data from

the cost accounting system and costing records. In many organisations, IT systems

now integrate costing data with other operational data. This means that data is

available to the management accounting system from non-accounting sources.

Example

An information system might be required to provide information about the

profitability of different types of customer.

The starting point for the design of this information system is the purpose of the

information. Why is information about customer profitability needed? The answer

might be that the company wants to know which of its customers contribute the

most profits, and whether some customers are unprofitable. If some customers are

unprofitable, the company will presumably consider ways of improving

profitability (for example, by increasing prices charged to those customers) or will

decide to stop selling to those customers.

The next consideration is: What data is needed to measure customer profitability?

The answer might be that customers should first be divided into different

categories, and each category of customer should have certain unique

characteristics. Having established categories of customer, information is needed

about costs that are directly attributable to each category of customers. This might

be information relating to gross profits from sales, minus the directly attributable

selling and distribution costs (and any directly attributable administration costs and

financing costs).

Having established what information is required, the next step is to decide how the

information should be ‘captured’ and measured. In this example, a system is needed

for measuring each category of customer, sales revenues, costs of sales and other

directly attributable costs.

Chapter 12: Performance measurement systems

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 279

The information should be available for when management intend to review

customer profitability. This might be every three months, six months or even

annually.

3.6 Information from external sources

Managers need information about customers, competitors and other elements in

their business environment. The management information system must be able to

provide this in the form that managers need, and at the time that they need it.

External information is needed for strategic planning and control. However, it is

also often needed for tactical and operational management decisions.

Examples of the external information needed by companies are set out in the table

below.

Information area Examples of information needed

Customers

What are the needs and expectations of customers in the

market?

Are these needs and expectations changing?

What is the potential for our products or services to meet

these needs, or to meet them better?

Competitors

Who are they?

What are they doing?

Can we copy some of their ideas?

How large are they, and what is their market share?

How profitable are they?

What is their pricing policy?

Legal environment

What are the regulations and laws that must be complied

with?

Suppliers

What suppliers are there for key products or services?

What is the quality of their products or services?

What is the potential of new suppliers?

What is the financial viability of each supplier?

Political/

environmental

issues

Are there any relevant political developments or

developments relating to environmental regulation or

environmental conditions?

Economic/

financial

environment

What is happening to interest rates?

What is happening to exchange rates?

What is happening in other financial markets?

What is the predicted state of the economy

Paper P5: Advanced performance management

280 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Sources of external information

Sources of external information, some accessible through the Internet, include:

market research

supplier price lists and brochures

trade journals

newspapers and other media

government reports and statistics

reports published by other organisations, such as trade bodies.

3.7 Organising a system for providing external information

If managers are to be provided with external information by a management

information system (MIS), the system must be designed so that it is capable of

providing it:

There has to be a system of data capture. How should information be obtained

from the environment and filed within the MIS? How should the data be held

within the MIS?

How should the information be provided to managers? Should it be e-mailed to

them? Or should managers be expected to search for the information in the MIS

when they need it?

Should the external information be processed into a usable form for managers

when it is captured, or should it be supplied to managers as ‘raw unprocessed

data’?

The external information should be divided into strategic information and

operational information. Which managers should be provided with the strategic

information, and which ones need the operational information?

3.8 Limitations of external information

It is important to recognise the limitations of external information.

It might not be accurate, and it might be difficult to assess how accurate it is.

It might be incomplete.

It might provide either too much or not enough detail.

It might be difficult to obtain information in the form that is ideally required.

It might not always be available when required.

It might be difficult to find.

Chapter 12: Performance measurement systems

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 281

Recording and processing methods. Management reports

Recording data

Processing methods

Management reports

4 Recording and processing methods. Management

reports

4.1 Recording data

There are many different ways of ‘capturing’ data, and recording it in an

information system. Methods of recording data will depend on circumstances, and

also on the nature of the data required. For example:

Records of labour time spent on particular tasks or jobs might be recorded on

time sheets or job sheets.

Records of materials used might be recorded in materials requisition notes.

Data about customer satisfaction might be captured as records of customer

complaints. Alternatively, data might be obtained from market research surveys.

The system of recording data should be made as convenient as possible for the

individuals responsible for input of the data to the information system. Where

possible, the information system should be designed to minimise the risk of errors.

Data should also be recorded in a form that will allow it to be processed. As a

simple example, suppose that records of labour costs should provide for an analysis

of these costs into production costs, administration costs and sales and distribution

costs. The data about labour costs will have to be recorded in a way that will enable

the costs to be divided into their different categories.

4.2 Processing methods

Performance measurement systems should be designed so that data can be

processed in a way that meets the requirements of management. There are various

ways of processing data, and IT systems enable managers to obtain large amounts

of information for different purposes.

Data might be needed for planning or forecasting. Many managers use

spreadsheet models and other forecasting models.

Accountancy software packages, including management accounting packages or

modules, can be used to process accounting data.

Data might be used to prepare regular, formal management reports.

Alternatively, managers might want to obtain ‘ad hoc’ reports on demand.

E-mail allows managers to communicate information quickly between each other.

Paper P5: Advanced performance management

282 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

4.3 Management reports

Entities are able to produce large amounts of information, in formal reports or on

demand. This raises problems of control and security.

There should be controls to ensure that reports are distributed only to individuals

who are authorised to receive it. Much information is confidential, and access to it

should be restricted.

There should be distribution lists for routine reports, and a copy of the report

should be available only to the individuals in the list.

Access to online data files can be restricted by a system of identity codes and

passwords.

IT systems should have safeguards against unauthorised access by external

users. For example, intranet systems should include firewalls (hardware and

software). There should be physical controls over unauthorised access to

computers and computer terminals (such as making sure that office doors are

locked when the manager is away from his desk).

There should be established procedures for preventing unauthorised access to

confidential data. Managers should be required to keep all confidential

information in a secure place. There should be restrictions over the type of

information that can be sent by e-mail.

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 283

Paper P5

Advanced performance management

CHAPTER

13

Measuring performance

Contents

1 Performance hierarchy

2 Financial performance in the private sector

3 Non-financial performance indicators (NFPIs)

4 Performance measurement in not-for-profit

organisations

5 Behavioural aspects of performance reporting:

reward systems

6 Customer profitability

Paper P5: Advanced performance management

284 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Performance hierarchy

Agency theory

The nature of the performance hierarchy

Mission statement

Corporate vision

High-level corporate objectives and strategic objectives

Critical success factors (CSFs) and key performance indicators (KPIs)

The planning gap

The characteristics of operational performance

Accountability

Hard accountability and soft accountability

1 Performance hierarchy

1.1 Agency theory

Agency theory is associated with the work of Jensen and Meckling in the 1970s. The

theory considers the separation of ownership in business from its management. The

shareholders are the owners of a company and in a large company the shareholders

are not executive managers. Management is performed by professionals, who are

supposed to act as representatives of the shareholders.

It is therefore possible to describe the shareholders of a company as principals, who

use agents (management) to act on their behalf and in their interests. A similar

situation applies to not for-profit entities. For example, the management of a

government-owned hospital can be described as agents who work on behalf of the

hospital’s owners (the government or the general public) or the representatives of

the owners (say, the hospital’s board of governors).

For the purpose of the P5 examination, agency theory may be summarised briefly as

follows.

There is a conflict of interests between the principals of an entity and their

agents. The principals have their own objectives which they want the entity to

achieve. In a company, the shareholders may want to maximise their return on

investment, and invest in a company whose ‘mission’ they support.

Management on the other hand have personal interests to which they give

priority, such as remuneration and other rewards. The conflict of interests is

always at the heart of the principal-agent relationship.

Conflicts of interest are evident in a number of different ways.

- As a general rule, professional managers work less hard than they would do if

they were owners of the company. The result could be lower sales growth and

lower profits.