ACCA - P5 Study text - Emile Woolf INT - 2010

Подождите немного. Документ загружается.

Chapter 13: Measuring performance

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 295

Measuring financial security: liquidity and gearing

A long-term objective of a company should be survival, as well as growth. It is

therefore appropriate to measure financial risk. Measures of financial risk include:

liquidity risk, measured by ratios such as the current ratio or quick ratio, or by

cash flow analysis

gearing or debt/equity ratios, which measure the potential risk to a company

from its funding structure.

Liquidity can be important. Liquidity means having cash or access to cash to make

payments when these are due. For example, a company must have cash to pay

salaries and wages of its employees, and to pay suppliers and other creditors. In

some cases, profitable companies might become insolvent because they cannot pay

their debts.

A lack of liquidity also restricts flexibility of action. A company that is short of cash

is often unable to take advantage of new opportunities that might arise, because

they do not have the money to spend.

Gearing and debt levels can also be important. Highly-geared companies are

exposed to the risk of a big fall in earnings per share whenever there is a fall in their

operating profits. When they borrow at variable rates of interest, an increase in

interest rates will also reduce profitability.

Historical profits and expected future profits

The main objective of a commercial company might be to maximise the wealth of

shareholders. Wealth is increased by paying dividends and through increases in the

share price. A common assumption in financial management is that the share price

of a company depends on expectations of future profits and dividends.

During the late 1990s and early 2000s, the share prices of newly-formed ‘new

technology’ companies reached very high levels, even though these companies were

making heavy losses. The view of investors at the time was that high values for new

technology companies were justified by the expectation of enormous future profits.

The high share prices reached by these companies are now known as the ‘dot.com

bubble’, which collapsed in 2001. In 2000 and 2001 the share prices of these

companies collapsed, and many went out of business.

It was eventually recognised that most of the new technology companies would

never compete successfully against larger ‘traditional’ companies. Most never

became profitable before they went out of business or were taken over at low prices.

A lesson from the ‘dot.com bubble’ is that future share prices (and shareholder

wealth) will depend on future profits and dividends. However, it is important to

convince investors that the company will be profitable in the future. Historical

returns and profits, and trends in profitability, might provide some guide to what

profits might be in the future.

Paper P5: Advanced performance management

296 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

2.3 Other financial measures of performance

Financial measures are used to set targets for performance and monitor actual

performance throughout the management hierarchy. You should be familiar with

many of these financial measures, such as:

gross profit margin

net profit margin

cost/sales ratios

growth in sales

cost variances.

Another way of measuring the management of costs is to measure costs as a

percentage of total sales revenue, and monitoring changes in this percentage figure

over time. Cost ratios might include:

production costs as a percentage of sales

distribution and marketing costs as a percentage of sales

administrative costs as a percentage of sales

material costs as a percentage of total cost

labour costs as a percentage of total costs.

Costs can also be monitored in terms of:

cost per unit

cost per machine hour

cost per activity – for example the cost to process and despatch a customer’s

order, or the cost to rectify a defective unit

comparison with a target cost.

2.4 Short-run and long-run financial performance

DCF methods of measuring financial performance are forward-looking and long-

term in perspective. As stated already, DCF is not suitable for measuring historical

performance.

A problem with other financial measures of performance is that they are mainly

short-term in perspective, and focus in the current financial year. Trends can also be

monitored (growth in EPS, sales, profits and so on), but it can be difficult to project

historical trends into the future.

Rewards to individuals for performance are also often based on the achievement of

targets for the current financial year, adding to the short-term focus.

The need to find a balance between short-term and long-term financial success has

led to the development of differing views of performance measurement, such as the

balanced scorecard and performance pyramid. These are described in a later

chapter.

Chapter 13: Measuring performance

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 297

2.5 Setting financial targets: methods

There are several different ways of setting targets, such as financial targets, or

making financial forecasts:

engineering-based targets

historical-based targets

negotiated targets

Engineering-based targets

Engineering targets may be used when there is a stable and predictable relationship

between inputs to the forecasting model and outputs. An example of this type of

forecasting or targeting is standard costing. Standard costs assume a fixed

relationship between the resources that go into making an item of product and the

production of one finished unit. By setting a standard cost, it is possible to set a

target total cost for the production of any given quantity of the items.

Historical-based targets

When it is not possible to identify stable and predictable relationships between

inputs and outputs, it may be appropriate to establish targets on the basis of either:

historical performance, and what has been accomplished in the past, or

historical targets that have been used in the past, on the assumption that they are

still based on valid assumptions

For example, a financial target may be set to achieve a gross profit to sales ratio of

40%, because this target has been used consistently for the past few years.

However, the past is not always a suitable basis for setting targets for the future:

the circumstances that applied in the past may no longer apply for the future,

and different assumptions might be appropriate for setting targets for the future

the historical targets used in the past may allow for inefficiencies that ought to

be eliminated for the future.

Negotiated targets

Financial targets may also be agreed as the outcome of negotiations between

superiors and subordinates. Senior managers may try to impose financial targets on

their subordinates, and the subordinates may argue that the targets are unrealistic

and unfair. As a result of the discussions and negotiations that follow, ‘compromise’

targets may be agreed that are acceptable to both sides.

Advocates of negotiated financial targets argue that the negotiation process between

superiors and subordinates helps to bridge the information gap between:

senior managers, who can see the ‘big picture’ and what the entity should be

trying to achieve (which subordinate managers may not be aware of)

Paper P5: Advanced performance management

298 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

subordinate managers, who understand operational matters at a level of detail

that their seniors do not.

Negotiating financial targets enables senior and subordinate managers to exchange

information and views, each from their own perspective. As a result of the

negotiations, the financial targets that are agreed should be achievable, striking a

realistic balance between higher-level objectives and lower-level practical realities.

2.6 Making comparisons of financial performance

The performance of departments or divisions may be assessed through comparison.

In other words, has one division performed better than the other? However, when

making comparisons of performance between two divisions of the business, it is

important to be aware of the reasons why their performance might be different.

There could be very good reasons why one division has performed better than the

other in the short-term. When there are good reasons for differences in performance,

the comparison should take these reasons into consideration.

A simple example may help to illustrate this point.

Example

An international company has two operating divisions, one in Country X and the

other in Country Y. The operating division in Country X has been in existence for

many years. The operating division in country Y was established two years ago,

when the company invested in country Y for the first time.

The financial results for the two divisions for the year just ended are as follows:

Year 1 Year 2

Country X Country Y Total Country X Country Y Total

$

million

$

million

$

million

$

million

$

million

$

million

Sales 800 80

880

860

120 980

Direct costs

Labour 280 15

295

302

22 324

Materials 160 20

180

182

28 210

440 35

475

484

50 534

Other costs

Marketing 70 40

110

80

80 160

Depreciation 100 8

108

100

16 116

170 48

218

180

96 276

Total costs 610 83

693

664

146 810

Profit before

interest

190 (3)

187

196

(26) 170

Interest

20

40

165

130

Non-current

assets (net

book value)

90 25

115

100

55 155

Debt

300

650

Chapter 13: Measuring performance

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 299

These figures might suggest that operating performance was much better in

Country X than in Country Y. Country Y made a loss in Year 1 and an even bigger

loss in Year 2.

However, the operations in Country Y are fairly new, and the difference in the

results between the two countries is probably due to the costs of starting up in

Country Y. In particular, the marketing costs in Country Y are very high relative to

sales. High marketing spending may be necessary to establish a foothold in the

market and a suitable market share.

The ratio of total costs to sales can be compared. The ratio of material costs to sales

is slightly higher in Country Y than in Country X, possibly due to difficulty in

obtaining material supplies locally. However, the ratio of labour costs to sales is

much lower in Country Y, suggesting that at some time in the future, it may be

beneficial to switch production from country X to Country Y.

Sales are growing in Country X, but the profit/sales ratio has fallen slightly. Sales

grew by 50% in Country Y in Year 2, suggesting that the greatest potential for

growth in sales and profits might be in Country Y rather than Country X.

The data is by no means conclusive. The key point, however, is that comparisons

should be made with care.

Paper P5: Advanced performance management

300 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Non-financial performance indicators (NFPIs)

The nature of non-financial measures of performance

Strategic NFPIs

Operational NFPIs

Capacity utilisation and resource utilisation

Multiple measures of performance

Measurements of quality

Performance through quality

Qualitative performance

3 Non-financial performance indicators (NFPIs)

3.1 The nature of non-financial measures of performance

Performance measures might be non-financial. Non-financial performance

indicators (NFPIs) can be both quantitative and qualitative.

Non-financial measures of performance should focus on critical success factors of a

non-financial nature. These will vary from one type of business entity to another,

and they will also vary according to the ‘level’ of performance reporting – strategic

or operational.

Typically, non-performance measures of performance will relate to a critical success

factor in one of the following areas:

quality

speed (for example, speed of service or speed of delivery)

reliability

efficiency

achieving a specific non-financial target

meeting customer needs/customer satisfaction.

3.2 Strategic NFPIs

Non-financial performance measures are needed because success in achieving some

strategic objectives cannot be measured in money terms alone, and in terms of

financial performance measurements. Some strategic objectives are therefore set in

terms of a non-financial performance target, and actual results are compared with

this non-financial target.

Non-financial targets should be compatible with financial targets.

Chapter 13: Measuring performance

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 301

Examples of quantitative strategic non-financial performance measurements

include:

market share (as a target for competitive strategy and sales strategy)

number of new products developed (as a target for innovation strategy)

quality measures (where quality is a key strategic objective for meeting customer

needs and expectations).

3.3 Operational NFPIs

Many operational targets are set and operational performance measured by NFPIs.

For example, measures of success in meeting customer needs include:

customer service measures, such as average time to respond to customer calls,

and average time to meet customer orders

customer satisfaction reports

measures of repeat business obtained or customer loyalty.

Measures of performance in relation to the management of employees would

include:

staff turnover rates

absenteeism and sickness rates

productivity ratios or similar productivity measurements.

3.4 Capacity utilisation and resource utilisation

Measures of performance in relation to the utilisation of resources include capacity

utilisation ratios, such as:

hotel room occupancy rates (hotels)

machine utilisation rates

proportion of seats filled (airlines, cinemas).

Capacity utilisation is an important aspect of performance, because successful

performance often depends on the extent to which available key resources are used.

In a manufacturing business, a company may have invested heavily in special

production equipment. If the machines are used to 98% of their capacity, this would

indicate that operations are performing well. On the other hand, if the machines are

operating at only 40% capacity, this would indicate scope for improvement.

In your exam, you may be required to calculate capacity utilisation ratios as

measures of performance, and comment on them (change from the previous year, or

comparison with the budget or with another entity’s capacity utilisation). Other

examples of capacity utilisation measures are:

The capacity utilisation of classrooms in a school (actual number of students as a

percentage of capacity)

Paper P5: Advanced performance management

302 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The utilisation of bed space in a hospital (actual patient days compared with

maximum capacity)

The utilisation of seats in a bus service or train service, compared with capacity

The utilisation of space in transport vehicles, compared with capacity.

Actual capacity utilisation is usually reported as a percentage of total capacity.

Example

Cloudy Airlines has a fleet of three passenger planes that fly between Bendia

Airport and Dandia Airport. Each plane does two return journeys each day. They

operate for 360 days each year. The seating capacity on each plane is 150 seats, all

the same class.

During the year just ended, Cloudy Airlines sold 180,000 return flight tickets on the

route and 97,200 one-way tickets.

Capacity utilisation on the route was 75% last year.

What was capacity utilisation in the current year (just ended) and what does this

suggest about performance?

Answer

We need to calculate the capacity on the route.

100% capacity = 3 planes × 4 trips per day (two return trips) × 150 seats per plane ×

360 days per year = 648,000 passengers.

Actual capacity = (180,000 × 2) + 97,200 = 457,200.

Capacity utilisation = 457,200/648,000 = 0.7056 = 70.56%.

If capacity utilisation was 75% last year, capacity utilisation has fallen in the current

year, which should be a matter of concern to management.

3.5 Multiple measures of performance

Performance can be assessed using several different measures or indicators. For

example, performance can be measured by:

A combination of financial measures, quantified non-financial measures and

(possibly) non-quantified (qualitative) non-financial measures

A balanced scorecard approach, with four different perspectives on performance

targets

Measures related to short-term financial and operating targets and measures

related to longer-term strategic objectives.

Chapter 13: Measuring performance

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 303

3.6 Measurements of quality

Quality targets may be a major element in strategic planning. Quality is associated

with meeting customer needs and expectations.

Quality performance can be measured and evaluated in relation to the key

performance objectives of quality, speed, dependability (reliability), flexibility and

cost. For example:

Performance

objective

Performance measure

Quality

Percentage of items rejected or scrapped

Average number of defects per unit produced

Average time between machine breakdowns

Number of customer complaints

Number or cost of warranty claims

Speed

Average time between receiving an order and

completing the work

Throughput cycle time

Transport times

Dependability

Percentage of customer orders met from inventory

Percentage of orders or items delivered late

Average delays

Flexibility

Average set-up time

New product development time

Range of products

Cost

Variances

Cost per operating hour/per machine hour

Labour productivity

Throughput, contribution

Another approach to quality performance measurement is to use a combination of

operational measures, financial measures and customer measures. For example:

Operational measures

- percentage of items rejected

- time lost in production

Financial measures

- the cost per unit produced

- quality costs

Customer measures, such as:

- number of customer complaints

- number of claims under warranty

- change in total market share.

Paper P5: Advanced performance management

304 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

3.7 Performance through quality

Cost and quality are inter-connected issues. Business entities provide goods or

services to customers that combine a particular cost per unit (and sales price per

unit) with a perceived level of quality. In a competitive business environment,

companies should be trying either:

to provide customers with more quality for a given cost per unit or

to provide products of a given quality for a lower cost.

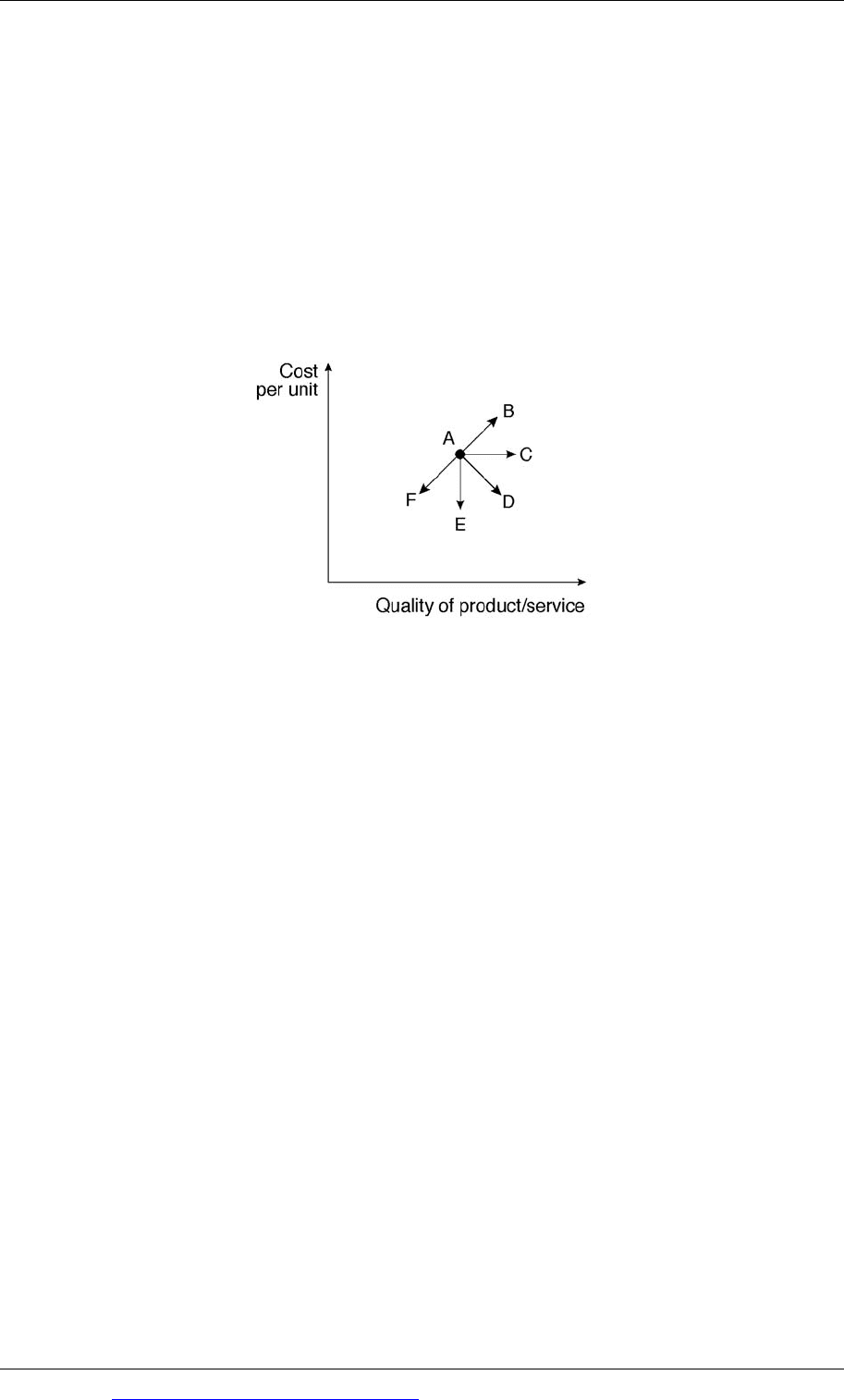

In the following diagram, the current position for a company in a competitive

market is shown as point A. The company has six strategic options, A to F.

Strategy A. This is a do-nothing strategy. In a competitive business

environment, it is the strategy most likely to result in eventual business failure.

Companies cannot ‘do nothing’. Like their competitors, they need to seek ways

of providing more value to customers, by reducing costs or improving quality.

Strategy B. This strategy is to improve the quality of the product or service, and

increasing the cost per unit to achieve the quality improvement.

Strategy C. This is a strategy of more quality for the same cost – improving the

quality of the product or service without any change in the cost per unit.

Strategy D. This is a strategy of improving quality and at the same time

reducing the cost per unit. This is the strategy most likely to succeed over the

long term, but improving quality and reducing costs may be difficult to achieve.

Strategy E. This is a strategy of maintaining the same quality, but at a lower cost

per unit.

Strategy F. This is a strategy of ‘going down-market’, and providing a cheaper

product or service, but at a lower standard of quality.

Strategy A is the least likely to succeed and Strategy D the most likely to succeed.

The likely success of the other strategies will depend on competitive conditions in

the market (what competitors are doing) and on customer preferences.