ACCA P4 Advanced Financial Management - 2010 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

Chapter 8: International investment and financing decisions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 215

This leaves 880,000 dinars after tax, but if it wants to remit as much as possible to

the parent company and pays withholding tax of 10%, the parent company will only

receive × 100/110 of the available profits after tax (gross distribution). The parent

will receive 800,000 dinars and withholding tax will be (10%) 80,000 dinars.

The parent will exchange the dinars into $800,000 and it has paid tax at the effective

rate of 20% on its foreign subsidiary’s profits. The tax rate in the parent company’s

country is 25% on world-wide profits, so tax on $1,000,000 will be $250,000.

However, since tax of 250,000 dinars ($250,000) has already been paid in the

subsidiary’s country, and a double taxation agreement exists, the parent company

must pay $50,000 in extra tax to its domestic tax authorities.

Note. If the rate of tax had been lower in the parent company’s country, say 18%

rather than 25%, the subsidiary would pay profits on tax of 120,000 dinars and

withholding tax of 80,000 dinars, but no further additional tax would be payable by

the company to its domestic tax authorities.

The net effect is for the total amount of tax payable to be equivalent to tax at the

higher rate of the two countries concerned.

1.6 Fiscal risk

Fiscal risk is the risk that after a capital investment project has been implemented,

the government might increase the rate of tax payable on the profits or cash flows

from the project. Higher tax payments could significantly affect the returns from a

project.

Fiscal risk varies between countries. Some countries have a reputation for fiscal

stability, so that any changes in tax are fairly insignificant. In other countries there is

a much higher risk of tax changes. Obviously, companies considering an investment

in a country, even their domestic country, should take fiscal risk into consideration

when deciding whether or not to invest in a project.

Example

The oil and natural gas industry is an example of an industry where fiscal risk has

had a significant impact on capital expenditure decisions.

Oil companies purchase concessions to explore for oil or gas, and extract any that

they find. If they fail to find any oil or gas, they will lose their investment. However,

they face a risk that if they are successful in finding and extracting oil, the

government will decide to tax their profits. One way of doing this is to charge a

windfall tax on the profits of firms in the industry that operate in the country.

In the past the UK government has charged a windfall tax on the profits of

companies in the North Sea oil business. The matter was debated in Parliament in

2002, where it was claimed that if the government raised the rate of tax on the

profits of offshore oil and gas extraction to 40% or 50%, further exploration by the

oil companies would cease to be viable.

Paper P4: Advanced Financial Management

216 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Reducing fiscal risk

Fiscal risk is unavoidable for companies that pay tax on their profits. However, the

risk might sometimes be reduced for large companies. A large company can try to

negotiate with the government of a country before deciding whether to invest in the

country. They might argue that they will not invest unless the government gives an

assurance of fiscal stability.

The risk of an unexpected additional tax (windfall tax) cannot be removed simply

by a government’s promise, because promises might be broken. Another approach

that might be used by some companies is to offer to pay a royalty tax on their

output. For example, an oil company might undertake to pay a royalty on every

barrel of oil that it extracts under a concession agreement. If the company pays tax

in this way, so that the royalty payments increase with the volume of business, the

government might be less inclined to charge additional tax on what it sees as

excessive profits.

Chapter 8: International investment and financing decisions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 217

Estimating exchange rates and the impact of exchange rate

movements on investment decisions

Estimating future ‘spot’ exchange rates

Purchasing power parity theory

International Fisher effect

Interest rate parity theory

2 Estimating exchange rates and the impact of

exchange rate movements on investment decisions

2.1 Estimating future ‘spot’ exchange rates

A company might wish to estimate future ‘spot’ exchange rates in order to carry out

a capital investment appraisal of a proposed foreign investment, where:

the cash flows will be in a foreign currency, but

at some stage in the life of the project the cash will be converted into cash flows

in the currency of the investing parent company.

An estimate of a future spot rate is a forecast of what the exchange rate might be at a

future date, sometimes several years ahead.

(Confusion can arise because an estimate of a future spot rate is not the same as a

forward exchange rate that can be obtained in the foreign exchange markets.

Forward exchange rates for forward exchange contracts are described in a later

chapter.)

There are two related methods of estimating future spot exchange rates:

purchasing power parity theory

interest rate parity theory.

Remember, however, that spot exchange rates move up and down continually, and

any forecast of what the spot rate will be can only be an approximate estimate of

what the average exchange rate for a future period will be.

2.2 Purchasing power parity theory

Purchasing power parity (PPP) theory states that the spot rates between two

currencies will change over time in relation to the rate of inflation in the countries

from which the currencies originate. When the rate of inflation is higher in Country

A than in Country B, the currency of Country A will fall in value against the

currency of Country B.

Paper P4: Advanced Financial Management

218 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Estimated spot rate in Year n = Current spot rate ×

1+ i

VBLE

(

)

n

1+ i

BASE

()

n

where:

i

VBLE

is the forecast annual rate of inflation for the variable currency

i

BASE

is the forecast annual rate of inflation for the base currency

n is the number of years in the future

The base currency is the currency for which there is 1 unit in the quoted exchange

rate, and the variable currency is the currency whose value is expressed as a number

of units in value per 1 unit of the base currency. For example in the exchange rate £1

= $1.90, the pound sterling is the base currency and the dollar is the variable

currency.

(This formula is included in the formula sheet for your examination, using different

symbols. You can use the formula provided, but you need to understand what the

various symbols in the formula mean.)

Note that this formula calculates the expected

exchange rate as at the end of the

year

. However in DCF analysis it is assumed that cash flows occur at the year end.

The formula therefore provides the exchange rate required for DCF analysis of

international investments.

Example

The current exchange rate for euro/British pound (£/€1) is 0.6750. A UK company

wishes to evaluate a proposed capital investment in Germany. The investment will

be for five years, and a large proportion of the project cash flows will be in euros.

The company needs to forecast what the euro/British pound spot rate will be each

year for the full project period. It has been estimated that inflation in the UK will be

3% each year UK for years 1 to 4 and 5% in year 5. It has also been estimated that

inflation in the euro zone will be 1.5% each year for three years, and 2% in each of

years 4 and 5.

The spot exchange rates at the end of each year can be estimated using PPP theory,

as follows. (The variable currency in this example is the British pound, since €1 =

£0.6750).

Year Forecast rate

0 Actual rate 0.6750

1 0.6750 × (1.03)/(1.015)

0.6850

2 0.6750 × (1.03)

2

/

(1.015)

2

0.6951

3 0.6750 × (1.03)

3

/

(1.015)

3

0.7054

4 0.6750 × (1.03)

4

/

[(1.015)

3

)(1.02)]

0.7123

5 0.6750 × [(1.03)

4

(1.05)]/[(1.015)

3

(1.02)

2

]

0.7332

Chapter 8: International investment and financing decisions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 219

2.3 International Fisher effect

The economist Irving Fisher argued that investors in all countries expect the same

real rate of return, after allowing for inflation, and the difference in interest rates

between two countries could be explained by differences in the rates of inflation in

those countries. From this argument and PPP theory, it is possible to derive interest

rate parity theory.

2.4 Interest rate parity theory

This states that it is possible to predict future spot exchange rates from differences

in interest rates between the currencies.

Estimated spot rate in Year n = Current spot rate ×

1+ r

VBLE

(

)

n

1+ r

BASE

()

n

where:

r

VBLE

is the forecast annual rate of interest for the variable currency

r

BASE

is the forecast annual rate of interest for the base currency.

This formula is similar to the PPP theory formula, except that the forecast annual

interest rate is used instead of the annual forecast rate of inflation. The formula is

also given in the formula sheet for the examination.

(This formula is also used to obtain a forward exchange rate for forward exchange

contracts. This is explained in a later chapter on currency risk and currency risk

management.)

Example

The current exchange rate for British pound against the euro (€/£1) is 1.4815. The

forecast annual interest rate for the British pound is 5% in years 1 and 2 and 6% in

years 3 and 4.

The forecast annual interest rate for the euro is 2.5% in year 1 and 3% in each of

years 2 – 4.

Required

Use this data to estimate a spot rate (€/£1) at the end of each year for years 1 – 4.

Answer

The current exchange rate for British pound against the euro (€/£1) is 1.4815. The

forecast annual interest rate for the British pound is 5% in years 1 and 2 and 6% in

years 3 and 4.

The forecast annual interest rate for the euro is 2.5% in year 1 and 3% in each of

years 2 – 4.

Paper P4: Advanced Financial Management

220 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Year Forecast rate

0 Actual rate 1.4815

1 1.4815 × (1.025)/(1.05)

1.4741

2 1.4815 × [(1.025)(1.03)]/(1.05)

2

1.4462

3 1.4815 × [(1.025)(1.03)

2

]/[(1.05)

2

(1.06)]

1.4053

4 1.4815 × [(1.025)(1.03)

3

]/[(1.05)

2

)(1.06)

2

]

1.3655

Example

Expected changes in an exchange rate can have a significant effect on the financial

viability of an international investment project, as this example demonstrates.

A company is considering a four-year investment in another country, where it will

establish a subsidiary. The subsidiary will remit all its profits each year to the parent

company, and no additional tax will be paid by the parent company in its own

country on the profits and dividends of its foreign subsidiary.

The investment will cost $230,000 in Year 0, and expected after-tax profits of the

subsidiary (all distributable) are as follows:

Year 000 pesetas

1 200

2 400

3 500

4 300

The current exchange rate is $1 = 4 pesetas. The cost of capital for evaluating all

aspects of the project is 15%.

The expected rate of inflation in the parent company’s country and Peseta-land is as

follows:

Year Forecast annual inflation

Dollar-land Peseta-land

1 2% 5%

2 3% 6%

3 3% 8%

4 2% 5%

Required

(a) Calculate the expected NPV of the project if changes in the exchange rate are

ignored.

(b)

Calculate the NPV of the project allowing for expected changes in the exchange

rate.

Chapter 8: International investment and financing decisions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 221

Answer

(a)

Ignoring changes in the exchange rate

Year Pesetas cash

flow

Exchange

rate

$ cash flow Discount

rate 15%

PV

000 pesetas $000 $000

0 (225)

1.000 (230.0)

1 200 4.0 50

0.870 43.5

2 400 4.0 100

0.756 75.6

3 500 4.0 125

0.658 82.3

4 300 4.0 75

0.572 42.9

NPV

+ 14.3

(b) Allowing for changes in the exchange rate

Year Estimated

exchange

rate

1 4.0 × (1.05)/(1.02) 4.12

2 4.0 × (1.05)(1.06)/(1.02)(1.03)

4.24

3 4.0 × (1.05)(1.06)(1.08)/(1.02)(1.03)

2

4.44

4 4.0 × (1.05)

2

(1.06)(1.08)/(1.02)

2

(1.03)

2

4.57

Year Pesetas cash

flow

Exchange

rate

$ cash flow Discount

rate 15%

PV

000 pesetas $000 $000

0 (225)

1.000 (230.0)

1 200 4.12 48.5

0.870 42.2

2 400 4.24 94.3

0.756 71.3

3 500 4.44 112.6

0.658 74.1

4 300 4.57 65.6

0.572 37.5

NPV

(4.9)

In this example, the project will not achieve a return of 15% and its NPV is negative,

because of the expected movement in the exchange rate during the project period.

Paper P4: Advanced Financial Management

222 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

DCF appraisal: investment in a developing country

Features of a foreign country investment appraisal

Method of making the DCF appraisal

3 DCF appraisal: investment in a developing country

An examination question might ask you to evaluate a proposed capital investment

in a foreign country, possibly a developing country where the risks of investment

are comparatively high due to a weak local currency and the risk of exchange

controls.

3.1 Features of a foreign country investment appraisal

The features of investing in a foreign country include the following:

The investment could be a very high-risk investment, and you might be required

to establish a

special cost of capital for evaluating the project, possibly using

the CAPM and a beta factor for the project.

Most of the cash flows for the foreign investment will be in the currency of the

foreign country, although some cash flows might be in the currency of the parent

company.

If the foreign country is a developing country, there will probably be

expectations of high rates of inflation in future years. If so, estimated cash flows

should be calculated allowing for the expected inflation rates. (These cash flows

including an allowance for inflation should be discounted at the money cost of

capital.)

If the foreign country is a developing country, there might be restrictions on the

amount of payments that can be made from the foreign country, due to

exchange control restrictions. This means that the cash profits from the project

might not be payable immediately in full as dividends to the investing company.

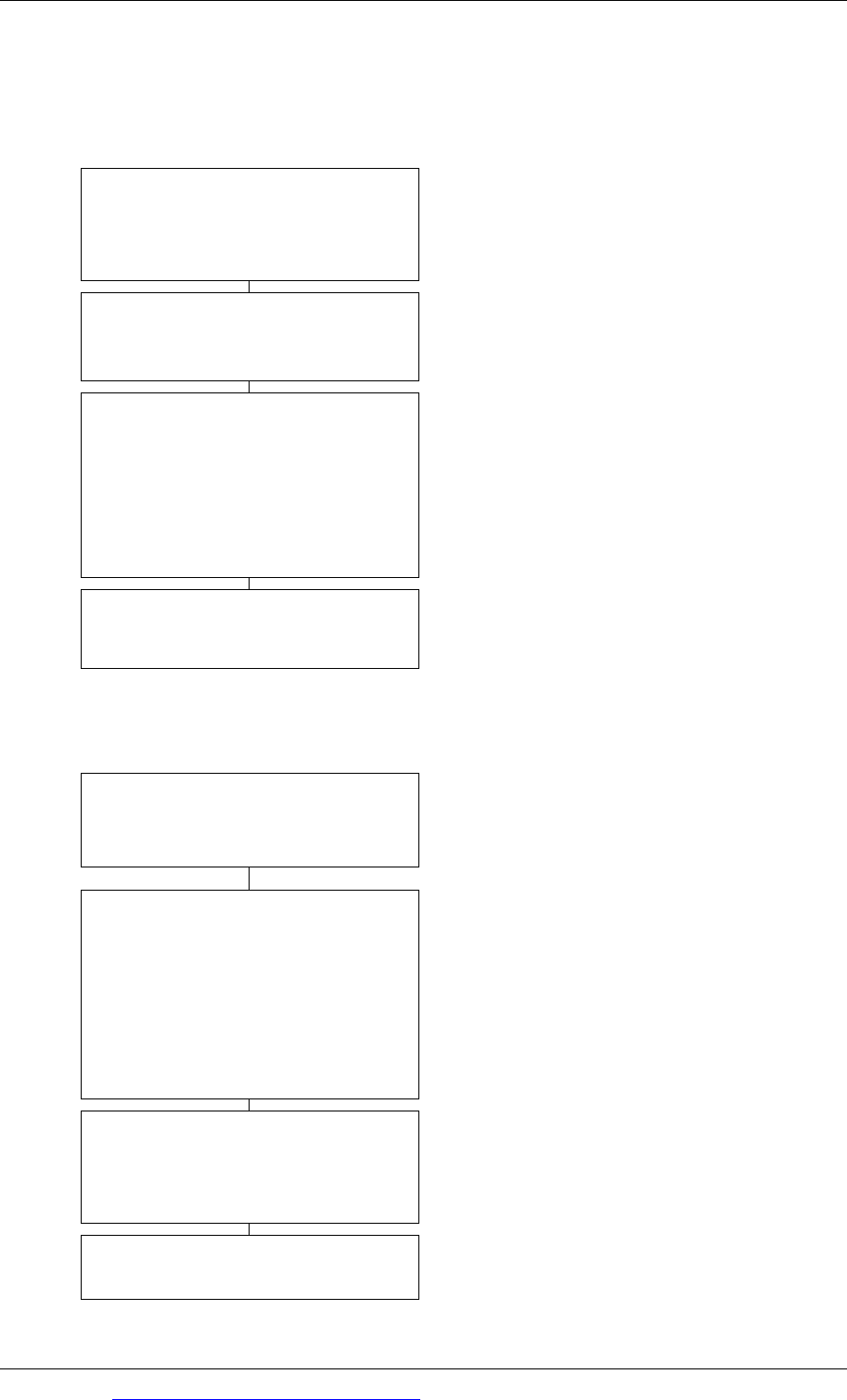

3.2 Method of making the DCF appraisal

Two stages in the appraisal

When a company is considering an investment in another country, a DCF analysis

should be carried out in two stages, and two net present values should be

calculated.

Stage 1. Ignore the fact that the proposed investment is an investment in another

country, and consider the investment as a capital project for the subsidiary company

in the foreign country. Calculate an NPV for the project on the basis of cash flows

for the subsidiary in the foreign country. This should be an NPV based on foreign

currency cash flows.

Chapter 8: International investment and financing decisions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 223

If the NPV is positive and the risk seems acceptable, you should then go on to Stage

2 of the DCF analysis.

Stage 2. Consider the project from the viewpoint of the parent company, and

estimate the cash payments and receipts for the parent company in its own

currency. These might include costs incurred in the parent company’s own country

to set up the project. They will also include the dividend or interest payments

received from the foreign subsidiary, in the currency of the parent company. These

cash flows should be discounted at an appropriate cost of capital, which might be

different from the cost of capital used in Stage 1.

The Stage 2 analysis uses different cash flows from the Stage 1 analysis.

Stage 1 evaluates the cash flows and cash profits in the foreign country. Stage 2

evaluates the actual returns received by the parent company.

Stage 1 is an evaluation of the foreign currency cash flows. The Stage 2

evaluation is an evaluation of the cash flows for the parent company in its own

currency.

This approach to evaluating the NPV of a foreign investment therefore involves two

separate NPV calculations:

Calculating the NPV of the cash flows in the foreign country, at an appropriate

cost of capital.

If the NPV calculated in this way is positive, calculating a different NPV for the

estimated cash flows for the project in the company’s domestic currency,

probably using the WACC as the discount rate. The cash flows in the company’s

domestic currency will be different from the cash flows in the currency of the

foreign country for several reasons:

− There may be some costs incurred in the company’s domestic currency and

outside the country where the investment is made. For example, the

company’s head office may incur costs in its own currency to establish the

project in the foreign country.

− There may be restrictions on dividend payments and other cash transfers out

of the country where the investment is made.

− The amount paid as dividends from the foreign country will also vary over

time with changes in the foreign exchange rate between the currency of the

investment country and the currency of the investing company.

Paper P4: Advanced Financial Management

224 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The project is financially viable only if both NPVs are positive.

Stage 1

The Stage 1 NPV calculation may be summarised as follows:

Comments

Establish the cash flows of the project for

the foreign subsidiary, in the currency of

the foreign subsidiary.

Where appropriate, allow for estimated

rates of inflation. Where you are given

the tax regulations, calculate the after-tax

cash flows.

Establish a discount rate for the foreign

project.

If you are given a beta factor for the

project, you can use this to establish the

cost of capital.

Discount these project cash flows at the

cost of capital you have established

The project

might be viable if it has a

positive NPV. A positive NPV would

show that the capital investment would

be viable if the company were based in

that country. However, you should

assess the project risk as well as the

return.

If the NPV is positive and risk is

acceptable, go on to Stage 2.

Stage 2

The Stage 2 NPV calculation may be summarised as follows:

Comments

Estimate the actual dividends that will be

paid from the foreign country out of the

project cash flows, allowing for foreign

exchange controls in that country.

The aim is to establish

when the

company will receive the cash in its own

currency and in what quantities.

Convert the foreign currency dividends into

the domestic currency of the company.

Where you are given inflation rates or

interest rates for the company’s own

country and the foreign country, you

should estimate what the future

exchange rates are likely to be, and

convert the dividends in each year at the

appropriate estimated exchange rate for

that year.

Establish all the cash flows of the project

for the parent company, in the currency of

the parent company.

Include any other cash flows for the

project that the company will expect to

incur in its own currency, as part of the

project.

Discount all the estimated cash flows in

the company’s own currency.

Use the company’s WACC as the

discount rate.