ACCA P4 Advanced Financial Management - 2010 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

Chapter 6: Cost of capital

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 155

Calculating the WACC

Method of calculating the WACC

WACC and market value

4 Calculating the WACC

4.1 Method of calculating the WACC

The WACC is a weighted average of the (after-tax) cost of all the sources of capital

for the company. It is calculated as follows:

Source of finance Market value

×

Cost Market value × Cost

r MV × r

Equity MV

E

×

K

E

MV

E

× K

E

Preference shares MV ×

K

P

MV

P

× K

P

Debt MV

D

×

K

D

MV

D

× K

D

Total

Σ

MV

ΣMV x r

WACC =

Σ

MV x r

Σ

MV

The WACC for a company is found using the method shown above. K

D

is the after-

tax cost of debt capital. If there is more than one source of debt, each with a different

cost, you can either:

have a separate line in the table for each item of debt, or

calculate a weighted average cost of all debt capital first (after-tax), then have

just one line in the table with the total market value of all debt capital and the

weighted average after-tax cost of the debt.

Example

A company has 8 million shares each with a value of $7.90, whose cost is 8.4%. It has

6% bonds with a market value of $50 million and an after-tax cost of 3.6%. It has a

bank loan of $10 million whose after-tax cost is 4.1%. It also has 2 million 8%

preference shares of $1 whose market price is $1.33 per share and whose cost is 6%.

Calculate the WACC.

Paper P4: Advanced financial management

156 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Answer

Source of finance Market value Cost Market value × Cost

$ million r % MV × r

Equity 63.20

8.4

530.88

Preference shares 2.66

6.0

15.96

Bonds 50.00

3.6

180.00

Bank loan 10.00

4.1

41.00

125.86

767.84

WACC =

6.10%

125.86

767.84

=

Example

You should be prepared in your examination to calculate the cost of equity in a

company, given the WACC, the cost of debt and the market value of equity and

debt. Here is an example.

A company has a weighted average cost of capital of 8.2%. It has 100 million shares

currently valued at $6 each, and it has a bank loan of $200 million on which the rate

of interest is 6.5%. The rate of taxation is 30%.

Required

Calculate the current cost of equity in the company.

Answer

The cost of equity can be calculated as the solution to a mathematical problem.

Let the cost of equity be r.

The after-tax cost of debt is 6.5% × (1 – 0.30) = 4.55%.

The WACC , which is 8.2%, is calculated as follows:

Source of finance Market

value

Cost

Market value

× Cost

$ million

%

MV × r

Equity 600.0

r

600r

Debt 200.0

4.55

910.0

800.0

600r + 910

WACC = 8.2% =

%

800

910 600r

+

8.2 (800) = 600r + 910

600r = 5,650

r = 9.417%

The cost of equity is 9.417%, say 9.4%.

Chapter 6: Cost of capital

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 157

4.2 WACC and market value

For a company with constant annual ‘cash profits’, there is an important connection

between WACC and market value. (Note: ‘Cash profits’ are cash flows generated

from operations, before deducting interest costs.)

If we assume that annual cash profits are a constant amount in perpetuity, the total

value of a company, equity plus debt capital, is calculated as follows:

Total market value of the company =

Annual cash profits

WACC

From this formula, the following conclusions can be made:

The lower the WACC, the higher the total value of the company will be (equity +

debt capital), for any given amount of annual profits.

Similarly, the higher the WACC, the lower the total value of the company.

For example, if annual cash profits are $12 million, the total market value of the

company would be:

$100 million if the WACC is 12% ($12 million/0.12)

$120 million if the WACC is 10% ($12 million/0.10)

$200 million if the WACC is 6% ($12 million/0.06).

The

aim should therefore be to achieve a level of financial gearing that minimises

the WACC

, in order to maximise the value of the company.

Important questions in financial management are:

How does the WACC change with changes in gearing?

For each company, is there an ‘ideal’ level of gearing that minimises the WACC?

Paper P4: Advanced financial management

158 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Cost of capital and gearing

The traditional view of gearing and WACC

The Modigliani-Miller propositions: ignoring corporate taxation

The Modigliani-Miller propositions: allowing for corporate taxation

5 Cost of capital and gearing

For a given level of annual cash profits before interest and tax, the value of a

company (equity + debt) is maximised at the level of gearing where WACC is

lowest. This should also be the level of gearing that optimises the wealth of equity

shareholders.

The question is therefore:

How does a change in gearing affect the WACC, and is there a level of gearing

where the WACC is minimised?

The most important analysis of gearing and the cost of capital, for the purpose of

your examination, is the analysis provided by Modigliani and Miller that allows for

tax relief on debt interest.

However, the traditional view of WACC and gearing, and Modigliani and Miller’s

propositions ignoring tax relief on debt are also described briefly.

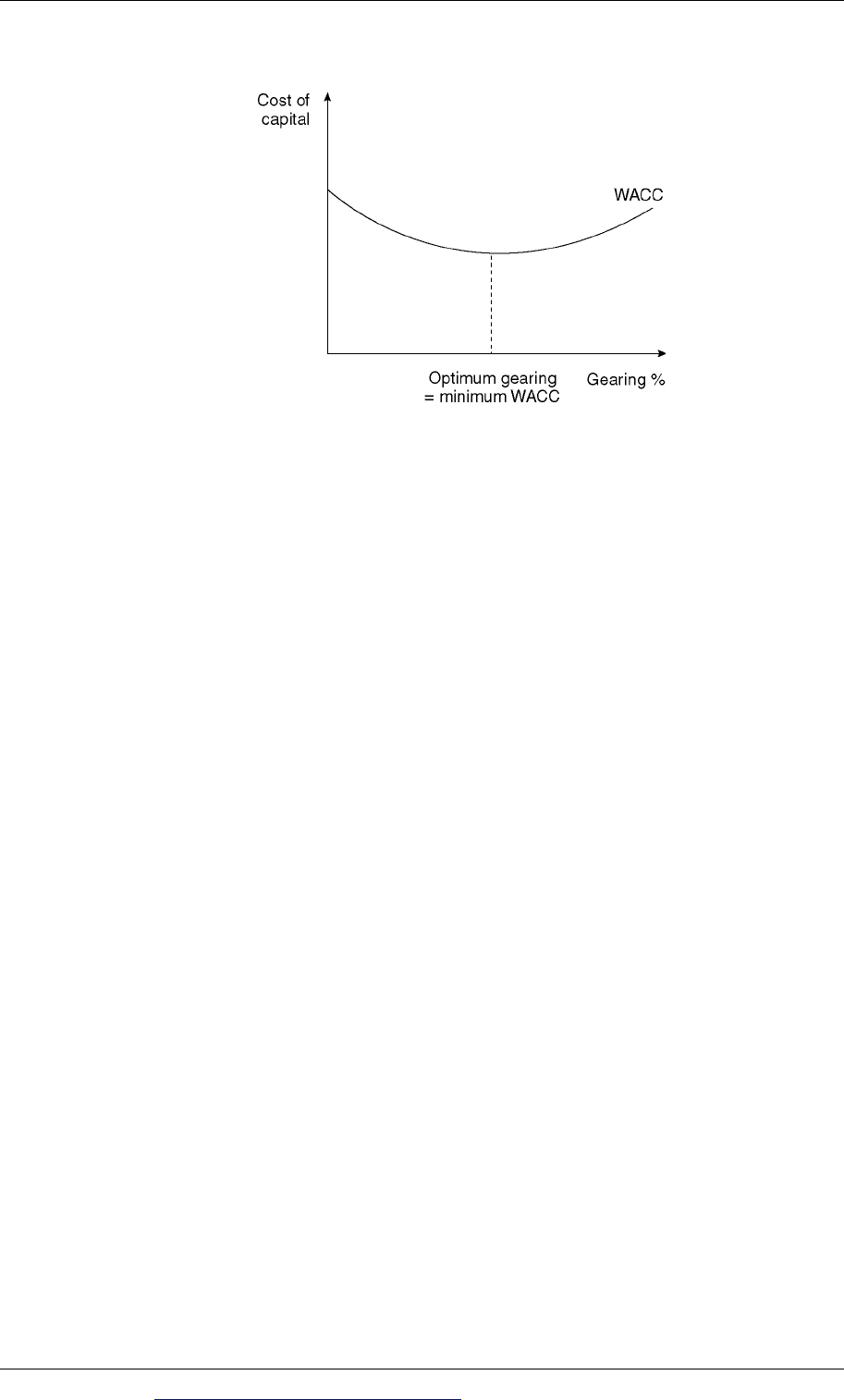

5.1 The traditional view of gearing and WACC

The traditional view of gearing is that there is an optimum level of gearing for a

company. This is the level of gearing at which the WACC is minimised.

As gearing increases, the cost of equity rises. However, as gearing increases,

there is a greater proportion of debt capital in the capital structure, and the cost

of debt is cheaper than the cost of equity. Up to a certain level of gearing, the

effect of having more debt capital has a bigger effect on the WACC than the

rising cost of equity, so that the WACC falls as gearing increases.

However, when gearing rises still further, the increase in the cost of equity has a

greater effect than the larger proportion of cheap debt capital, and the WACC

starts to rise.

The traditional view of gearing is therefore that an optimum level of gearing exists,

where WACC is minimised and the value of the company is maximised.

Chapter 6: Cost of capital

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 159

Traditional view of gearing and the WACC

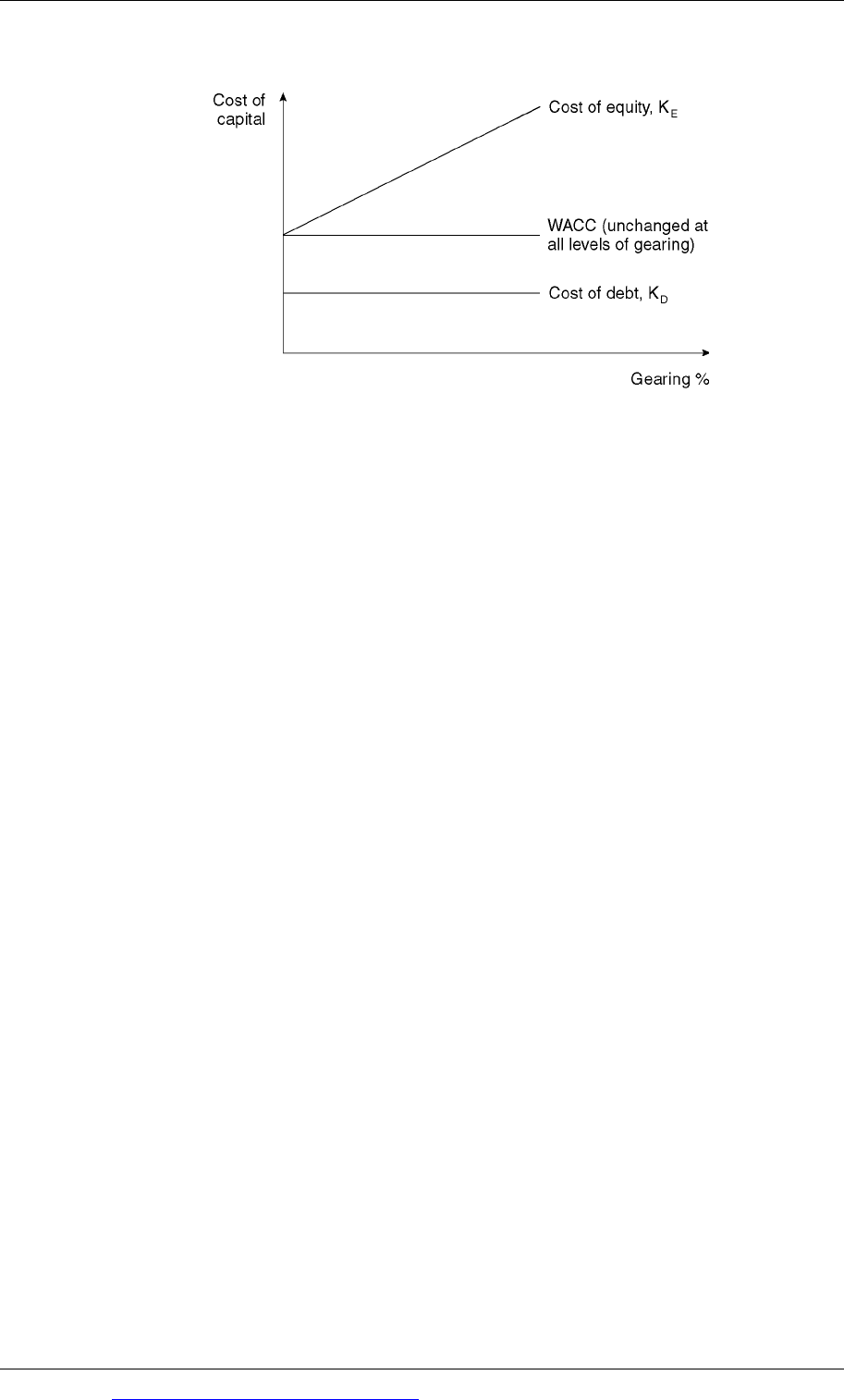

5.2 The Modigliani-Miller propositions: ignoring corporate taxation

The traditional view of gearing and WACC was challenged by Modigliani and

Miller in the 1950s. Initially, their arguments were based on the assumption that

corporate taxation, and the tax relief on interest, could be ignored.

You do not need to know Modigliani and Miller’s arguments, only the conclusions

they reached. They argued that if corporate taxation is ignored, an increase in

gearing will have the following effect:

As the level of gearing increases, there is a greater proportion of cheaper debt

capital in the capital structure of the firm.

However, the cost of equity rises as gearing increases.

As gearing increases, the net effect of the greater proportion of cheaper debt and

the higher cost of equity is that the WACC remains unchanged.

The WACC is the same at all levels of financial gearing.

The total value of the company is therefore the same at all levels of financial

gearing

Modigliani and Miller therefore reached the conclusion that the level of gearing is

irrelevant for the value of a company. There is no optimum level of gearing that a

company should be trying to achieve.

Paper P4: Advanced financial management

160 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Modigliani-Miller view of gearing and the WACC: no taxation

Modigliani and Miller’s propositions: ignoring taxation

Modigliani and Miller’s arguments, ignoring taxation, can be summarised as two

propositions.

Proposition 1. The WACC is constant at all levels of gearing. For companies

with identical annual profits and identical business risk characteristics, their

total market value (equity plus debt) will be the same regardless of differences in

gearing between the companies.

Proposition 2. The cost of equity rises as the gearing increases. The cost of equity

will rise to a level such that, given no change in the cost of debt, the WACC

remains unchanged.

Modigliani-Miller formulae: ignoring taxation

There are three formulae for the Modigliani and Miller theory, ignoring corporate

taxation. These are shown below. The letter ‘

U

’ refers to an ungeared company (all-

equity company) and the letter ‘

G

’ refers to a geared company.

(1)

WACC

The WACC in a geared company and the WACC in an identical but ungeared

(all-equity) company are the same:

WACC

G

= WACC

U

This formula expresses a part of proposition 1.

(2)

Total value of the company (equity plus debt capital)

The total value of an ungeared company is equal to the total value of an

identical geared company (combined value of equity + debt capital):

V

G

= V

U

This formula expresses another part of proposition 1.

Chapter 6: Cost of capital

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 161

(3) Cost of equity

The cost of equity in a geared company is higher than the cost of equity in an

ungeared company, by an amount equal to:

the difference between the cost of equity in the ungeared company and the

cost of debt (K

EU

– K

D

)

multiplied by the ratio of the market value of debt to the market value of

equity in the geared company (D/E).

K

EG

= K

EU

+

D

E

K

EU

−K

D

()

This formula expresses proposition 2.

Example

An all-equity company has a market value of $150 million and a cost of equity of

10%. It borrows $50 million of debt finance, costing 6%, and uses this to buy back

and cancel $50 million of equity. Tax relief on debt interest is ignored.

Required

According to Modigliani and Miller, if taxation is ignored, what would be the effect

of the higher gearing on (a) the WACC (b) the total market value of the company

and (c) the cost of equity in the company?

Answer

According to Modigliani and Miller:

(a)

WACC. The WACC in the company is unchanged, at 10%.

(b)

Total value. The total market value of the company with gearing is identical

to the market value of the company when it was all equity, at $150 million.

This now consists of $50 million in debt and $100 million equity ($150 million

– $50 million of debt)

(c)

Cost of equity. The cost of equity in the geared company is

()

12.0%%610

100

50

10% =

⎥

⎦

⎤

⎢

⎣

⎡

−×+

Example

A company has $500 million of equity capital and $100 million of debt capital, all at

current market value. The cost of equity is 14% and the cost of the debt capital is 8%.

The company is planning to raise $100 million by issuing new shares. It will use the

money to redeem all the debt capital.

Paper P4: Advanced financial management

162 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Required

According to Modigliani and Miller, if the company issues new equity and redeems

all its debt capital, what will be the cost of equity of the company after the debt has

been redeemed? Assume that there is no corporate taxation.

Answer

In the previous example, the Modigliani-Miller formulae were used to calculate a

cost of equity in a geared company, given the cost of equity in the company when it

is ungeared (all-equity). This example works the other way, from the cost of equity

in a geared company to a cost of equity in an ungeared company. The same

formulae can be used.

Using the known values for the geared company, we can calculate the cost of equity

in the ungeared company after the debt has been redeemed.

K

EG

= K

EU

+ D/E [K

EU

-

K

D

]

14.0 = K

EU

+ 100/500 [K

EU

– 8.0]

1.2 K

EU

= 14.0 + 1.6

K

EU

= 13.0% (15.6/1.2).

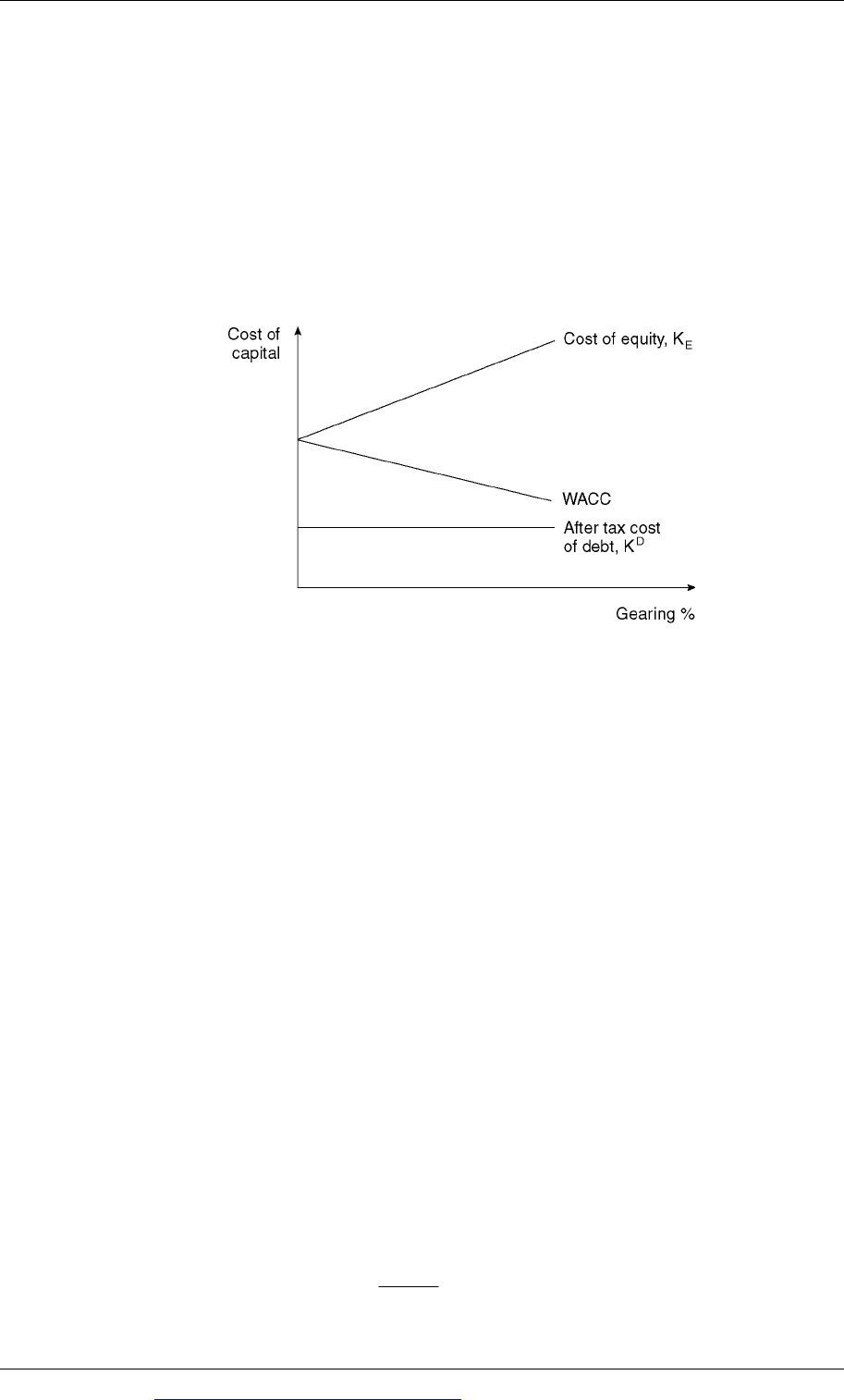

5.3 The Modigliani-Miller view: allowing for corporate taxation

Modigliani and Miller revised their arguments to allow for the fact that there is tax

relief on interest. You do not need to know the arguments they used to reach their

conclusions, but you must know what their conclusions were. You should also

know and be able to apply the formulae described below.

(The formula for the cost of equity is given in the formula sheet in your

examination, so you do not need to learn it.)

Modigliani and Miller argued that allowing for corporate taxation and tax relief on

interest, an increase in gearing will have the following effect:

As the level of gearing increases, there is a greater proportion of cheaper debt

capital in the capital structure of the firm. However, the cost of equity rises as

gearing increases.

As gearing increases, the net effect of the greater proportion of cheaper debt and

the higher cost of equity is that the WACC becomes lower. Increases in gearing

result in a reduction in the WACC.

The WACC is therefore at its lowest at the highest practicable level of gearing.

(There are practical limitations on gearing that stop it from reaching very high

levels. For example, lenders will not provide more debt capital except at a much

higher cost, due to the high credit risk).

Chapter 6: Cost of capital

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 163

The total value of the company is therefore higher for a geared company than for

an identical all-equity company. The value of a company will rise, for a given

level of annual cash profits before interest, as its gearing increases.

Modigliani and Miller therefore reached the conclusion that because of tax relief on

interest, there is an optimum level of gearing that a company should be trying to

achieve. A company should be trying to make its gearing as high as possible, to the

maximum practicable level, in order to maximise its value.

Modigliani-Miller view of gearing and the WACC: with taxation

Modigliani and Miller’s propositions: allowing for taxation

Modigliani and Miller’s arguments, allowing taxation, can be summarised as two

propositions.

Proposition 1. The WACC falls continually as the level of gearing increases. In

theory, the lowest cost of capital is where gearing is 100% and the company is

financed entirely by debt. (Modigliani and Miller recognised, however, that

‘financial distress’ factors have an effect at high levels of gearing, increasing the

cost of debt and the WACC.) For companies with identical annual profits and

identical business risk characteristics, their total market value (equity plus debt)

will be higher for a company with higher gearing.

Proposition 2. The cost of equity rises as the gearing increases. There is a

positive correlation between the cost of equity and gearing (as measured by the

debt/equity ratio).

Modigliani-Miller formulae: allowing for taxation

There are three formulae for the Modigliani and Miller theory, allowing for

corporate taxation. These are shown below. The letter ‘

U

’ refers to an ungeared

company (all-equity company) and the letter ‘

G

’ refers to a geared company.

(1)

WACC

The WACC in a geared company is lower than the WACC in an all-equity

company, by a factor of

1−

Dt

D +E

()

.

Paper P4: Advanced financial management

164 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

WACC

G

= WACC

U

1−

Dt

D +E

()

⎡

⎣

⎢

⎢

⎤

⎦

⎥

⎥

This formula expresses a part of proposition 1.

(2)

Value of a company

The total value of a geared company (equity + debt) is equal to the total value

of an identical ungeared company plus the value of the ‘tax shield’. This is the

market value of the debt in the geared company multiplied by the rate of

taxation (Dt).

V

G

= V

U

+Dt

where:

V

G

= value of geared company

V

U

= value of an identical but ungeared (all-equity) company

D = market value of the debt in the geared company

t = the rate of taxation on company profits.

This formula expresses another part of proposition 1.

(3)

Cost of equity

The cost of equity in a geared company is higher than the cost of equity in an

ungeared company, by a factor equal to:

the difference between the cost of equity in the ungeared company and the

cost of debt, (K

EU

– K

D

)

multiplied by the ratio

1−t

()

×

D

E

.

()

E

D

KK)1(KK

DEUEUEG

−−+= t

This formula expresses proposition 2. It is given to you in your examination,

in a formula sheet. Although you do not need to learn the formula, you should

become familiar with it, and know how to use it.

Example

An all-equity company has a market value of $60 million and a cost of equity of 8%.

It borrows $20 million of debt finance, costing 5%, and uses this to buy back and

cancel $20 million of equity. The rate of taxation on company profits is 25%.

According to Modigliani and Miller:

(a)

Market value

The market value of the company after the increase in its gearing will be:

V

G

= V

U

+Dt