ACCA P4 Advanced Financial Management - 2010 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

Chapter 5: Investing: portfolio theory and the CAPM

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 125

An efficient portfolio is a portfolio that offers:

a higher expected return than any other portfolio, for a given level of risk, or

a lower amount of risk than any other portfolio, for a given size of expected

return.

Rational, risk-averse investors will choose an efficient portfolio.

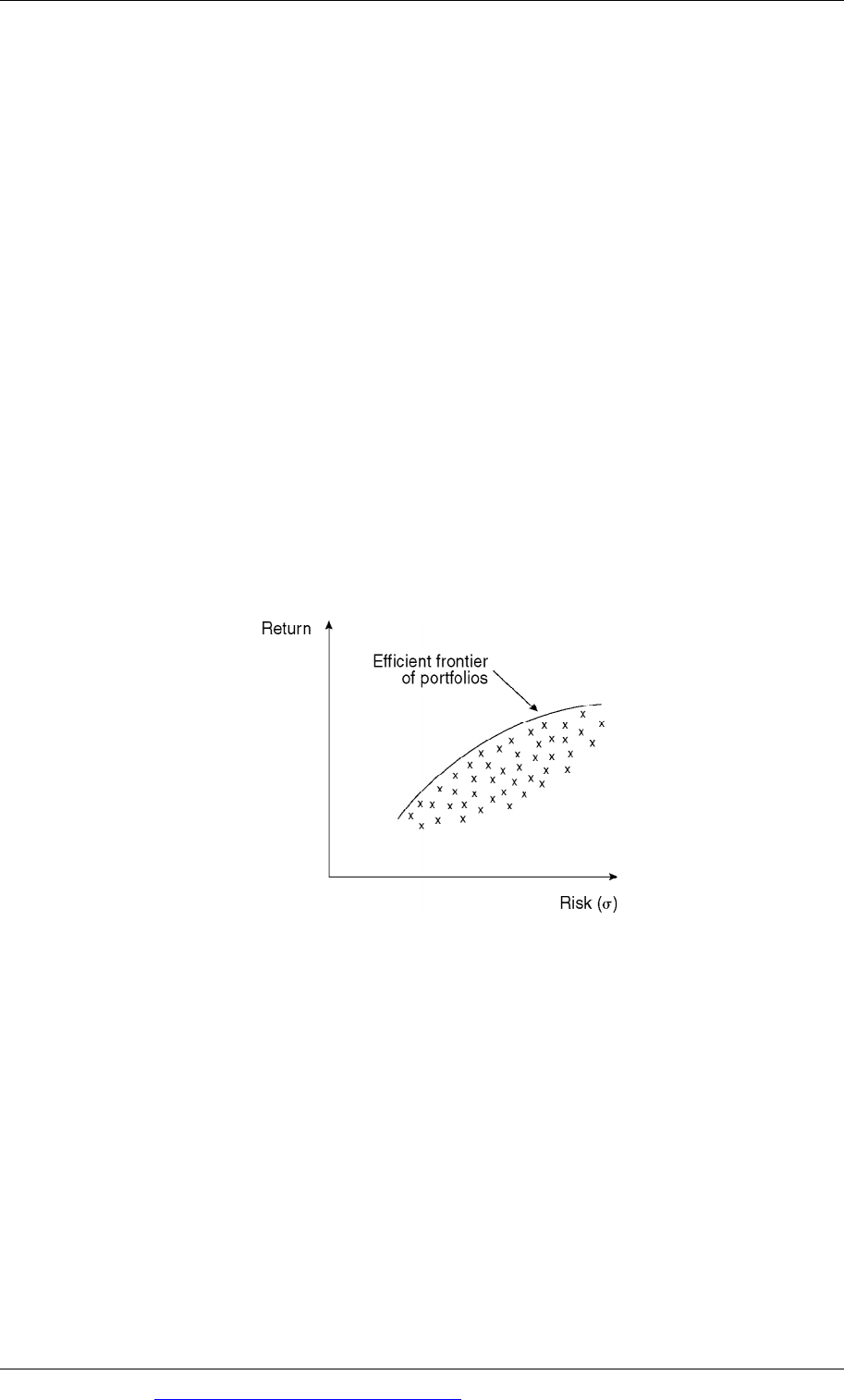

The efficient frontier of portfolios

In theory, it would be possible to prepare a graph showing every possible portfolio

that investors might choose, with the expected return from the portfolio plotted on

the y axis and the risk of the portfolio, measured as the standard deviation of its

expected returns, on the x axis.

This graph of portfolios would be shown as an egg-shaped grouping of portfolios,

with differing expected returns and differing risk.

The efficient portfolios all lie on the top edge. A line can be drawn through these

efficient portfolios, to obtain the efficient frontier of investment portfolios. A risk-

averse investor will always choose a portfolio on this efficient frontier.

Efficient frontier

X

X

X

X

X

X

X

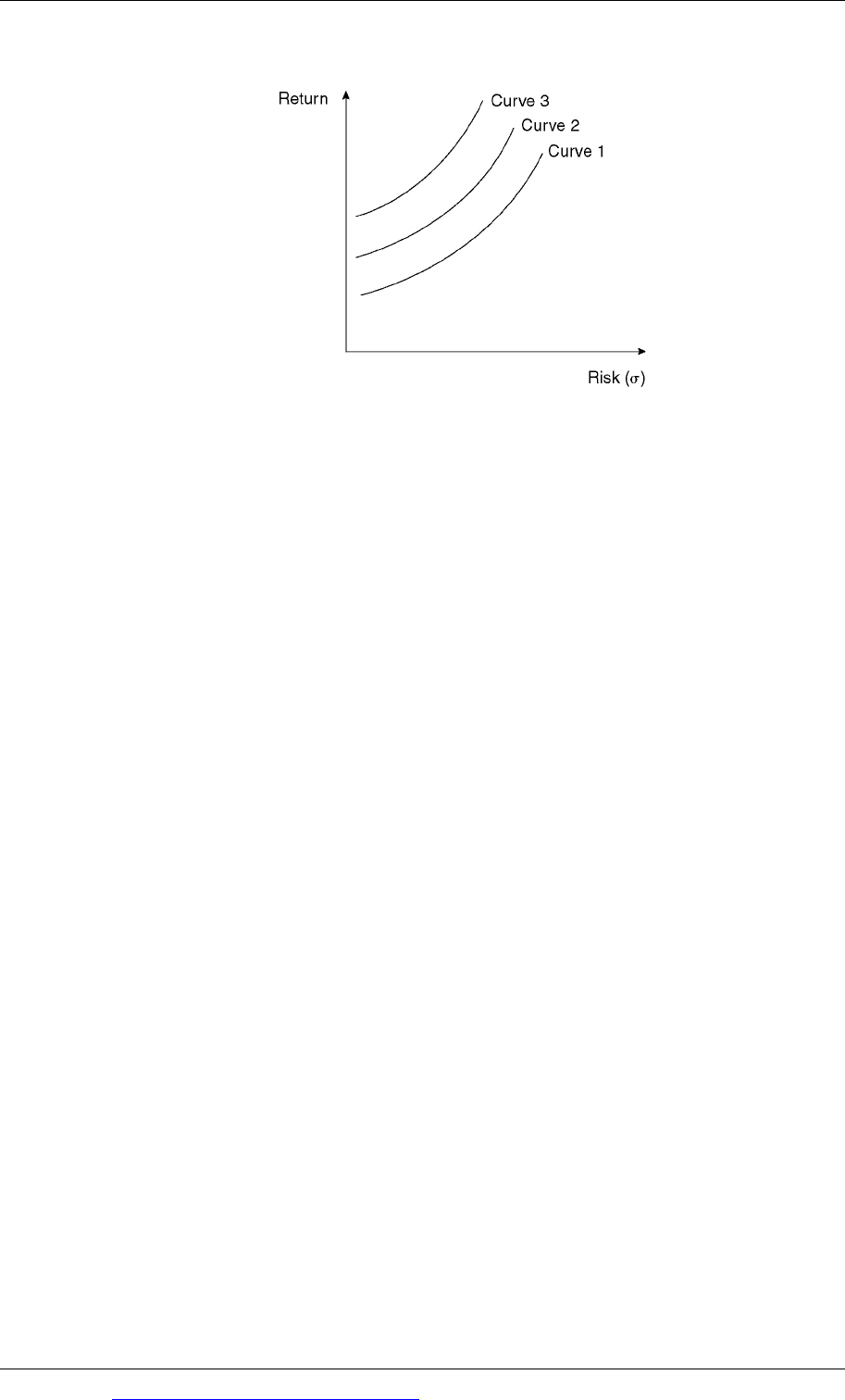

Investor preferences: indifference theory

The next question is whether investors might choose any investment portfolio on

this efficient frontier, or whether there is any particular portfolio that will be

preferred by all investors, above all the other portfolios.

In portfolio theory, this question is answered using the concept of indifference

curves and investor preferences.

Risk-averse investors are prepared to accept higher risk for a higher investment

return, but may also choose a lower expected return for lower risk. An investor’s

preferences for higher returns or less risk can be illustrated in a graph of

indifference curves.

Paper P4: Advanced Financial Management

126 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Investors’ indifference curves

In this graph, there are three indifference curves, Curve 1, Curve 2 and Curve 3.

Curve 1 shows the combinations of risk and return that are of equal merit or

attractiveness to the investor. The investor will be indifferent about choosing any

portfolio that lies on this curve.

Similarly, Curve 2 shows the combinations of risk and return that are of equal

merit or attractiveness to the investor. The investor will be indifferent about

choosing any portfolio that lies on this curve. However, the investor will prefer a

portfolio on Curve 2 rather than a portfolio on Curve 1, because portfolios on

Curve 2 will offer a higher return for less risk than portfolios on Curve 1 (or

lower risk for the same return).

Curve 3 also shows the combinations of risk and return that are of equal merit or

attractiveness to the investor, and the investor will be indifferent about choosing

any portfolio on this curve. However, the investor will prefer a portfolio on

Curve 3 rather than a portfolio on Curve 2, because portfolios on Curve 3 will

offer a higher return for less risk than portfolios on Curve 2 (or lower risk for the

same return).

The conclusion is that investors will select a portfolio for investment that lies on an

indifference curve as far to the left on the graph as possible.

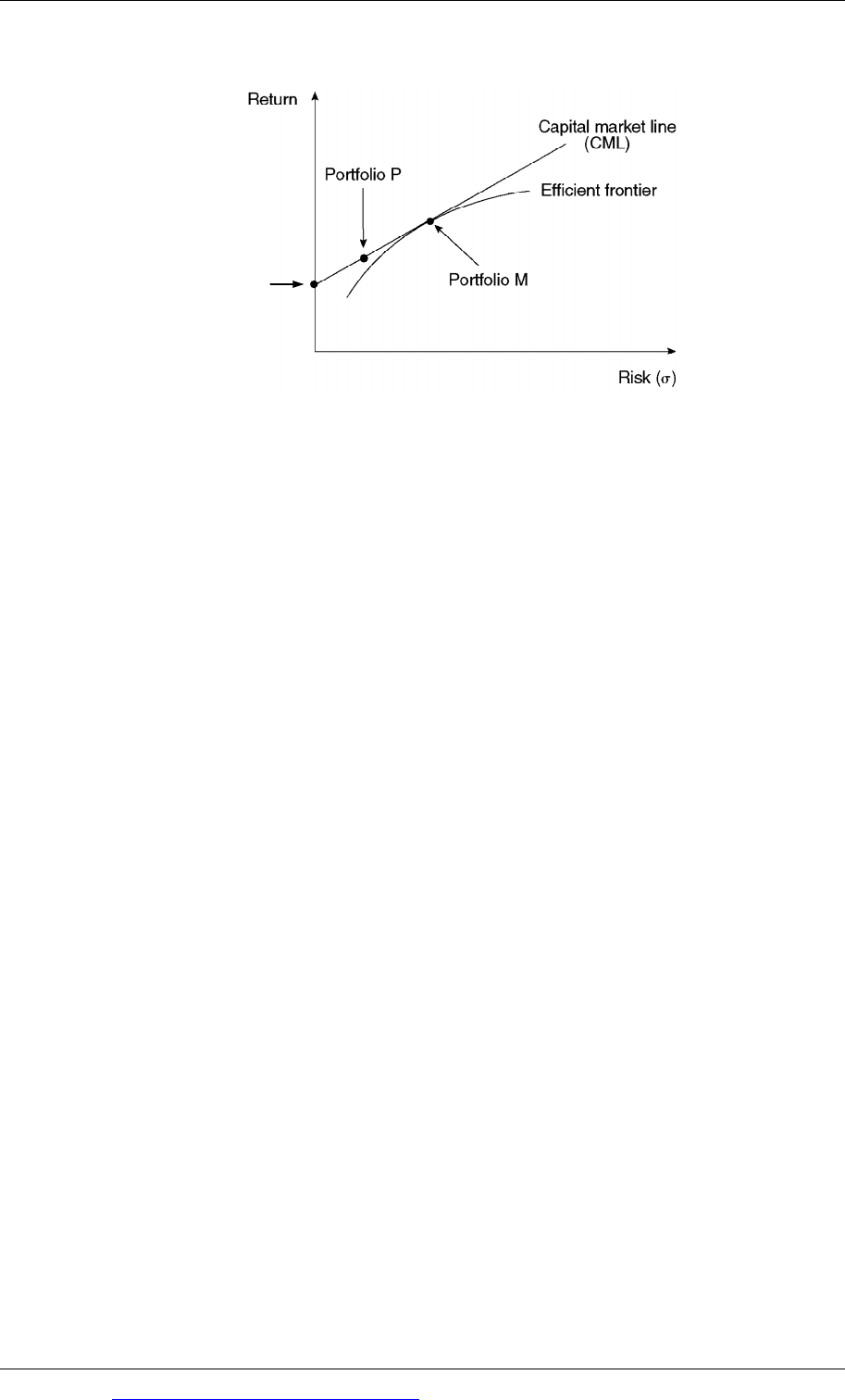

3.3 The market portfolio

We can combine the efficient frontier of portfolios with investors’ indifference

curves on the same graph. If we do, the graph will show that there is only one

portfolio on the efficient frontier that will maximise the satisfaction of investors.

This is at point M on the graph below.

This is the point where an indifference curve as far to the left as possible touches the

efficient frontier.

Chapter 5: Investing: portfolio theory and the CAPM

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 127

Portfolio M is called the market portfolio.

Market portfolio

The market portfolio is a portfolio of all investments traded on the stock market, in

quantities that reflect their relative overall market value, but excluding risk-free

investments.

The reason why the market portfolio contains all investments on the stock market is

that if it didn’t, there would be some investments that no rational, risk-averse

investors would ever buy. When investors are not buying particular investments,

the market price of the investments will change. Their price will fall, and their

expected return will increase. When this happens, they become more attractive to

investors, who will want to buy them.

In other words, market forces of supply and demand will ensure that investors are

willing to hold a portfolio of all investments in the market, weighted according to

the market valuation of the companies.

(

Note: In practice, investors do not hold shares in every company on the stock

market. However, major investors do hold a sufficiently large number of different

investments so that their portfolio closely resembles the market portfolio.)

3.4 Risk-free investments and choosing an investment portfolio

A stock market will have some risk-free investments. These are investments with no

investment risk. In practice, government bonds denominated in the domestic

currency are classified as risk-free investments.

If a portfolio of risk-free investments is shown on a graph with the efficient frontier

of portfolios and the market portfolio, it will be shown as a point on the y axis,

where risk is zero. This is shown as Portfolio G in the graph below.

Paper P4: Advanced Financial Management

128 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Risk-free investments and the capital market line

Portfolio G

The market portfolio does not include risk-free investments. Investors, however,

may choose a portfolio consisting partly of the market portfolio and partly of risk-

free investments.

A straight line can be drawn from the portfolio that is 100% risk-free (Portfolio G) to

touch the efficient frontier at a tangent. This will be at the market portfolio M. An

investor can select any portfolio on this line, such as Portfolio P, to provide a

mixture of risk-free investments and the market portfolio investments.

The line that joins Portfolio G and the market portfolio M is called the

capital

market line

. The capital market line (CML) shows all combinations of risk-free

investments and market portfolio investments that investors may select.

(

Note: The CML extends beyond Portfolio M. Portfolios on this part of the CML are

created when an investor uses all his own money and in addition borrows

additional funds (at the risk-free rate of interest) to invest in market portfolio

investments. This point is not important.)

3.5 The market premium

If an investor invests in a portfolio of risk-free assets, he will receive the risk-free

rate of return, which is the interest yield on those risk-free assets.

To compensate an investor for investing in the market portfolio, the expected return

must be higher than on risk-free investments. The

market premium is the difference

between the expected return on the market portfolio and a portfolio of risk-free

investments.

Market premium = R

m

– R

f

where:

R

m

is the market rate of return (the expected return on the market portfolio)

R

f

is the risk-free rate of return.

Chapter 5: Investing: portfolio theory and the CAPM

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 129

3.6 The beta factor of a portfolio

Any other portfolio on the capital market line must offer an expected return in

excess of the risk-free rate.

In the previous diagram, the expected return from Portfolio P can be stated as a

formula:

Expected return from Portfolio P:

R

p

= R

f

+ β(R

m

– R

f

)

where:

R

f

is the expected return from Portfolio P

β is a factor that represents the slope of the capital market line (and the element of

risk in the portfolio compared with the risk in the market portfolio). It is called the

beta factor.

Beta factors are explained in more detail later, in the section on the capital asset

pricing model. At this stage, it is sufficient to note the following points:

A beta factor can be calculated for every portfolio on the capital market line.

The market portfolio has a beta factor of 1.

R

m

= R

f

+ 1(R

m

– R

f

)

A portfolio of risk-free investments has a beta factor of 0.

R

f

= R

f

+ 0(R

m

– R

f

)

A portfolio on the capital market line consisting of 50% market portfolio

investments and 50% risk-free investments has a beta factor of 0.5 [= (50% × 1) +

(50% × 0)].

A beta factor can also be calculated for individual securities (shares or corporate

bonds) in the market portfolio. The beta factor of a portfolio of securities is simply

the weighted average of the beta factors of all the securities in the portfolio, with

weightings to allow for the different market value of each security in the portfolio.

Example

A pension fund is adding two new investments to the portfolio of investments in its

fund.

The existing pension fund consists of securities with a market value of $800 million.

These have a combined beta factor of 0.70.

It is now adding an investment of $100 million in domestic government bonds and

an investment if $50 million in equity shares that have a beta factor of 1.4.

Required

Calculate the beta factor of the enlarged portfolio after the addition of the two new

investments.

Paper P4: Advanced Financial Management

130 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Answer

The government bonds are risk-free and have a beta factor of 0.

Securities Value

Beta factor

Value

× Beta

$m

Existing fund 800

0.70

560

Government bonds 100

0.00

0

New equities 50

1.40

70

950

630

Beta of enlarged portfolio = 630/950 = 0.663.

3.7 Systematic and unsystematic risk

It was stated earlier that investors can reduce their investment risk by diversifying.

However, not all risk can be eliminated, and there will be some risk that cannot be

eliminated by diversification.

When the economy is weak and in recession, returns from the market as whole

are likely to fall. Diversification will not protect investors against falling returns

from the market as a whole

Similarly, when the economy is strong, returns from the market as a whole are

likely to rise. Investors in all or most shares in the market will benefit from the

general increase in returns.

Therefore there are two types of risk:

Unsystematic risk, which is risk that is unique to individual investments or

securities, that can be eliminated through diversification

Systematic risk, or market risk. This is risk that cannot be diversified away,

because it is risk that affects the market as a whole, and all investments in the

market in the same way.

Implications of systematic and unsystematic risk for portfolio investment

The distinction between systematic risk and unsystematic risk has important

implications for investment.

Investors expect a return on their investment that is higher than the risk-free rate

of return (unless they invest 100% in risk-free investments).

The higher expected return is to compensate investors for the higher investment

risk.

By diversifying, and investing in a wide range of different securities, investors

can eliminate unsystematic risk. This is because if some investments in the

portfolio perform much worse than expected, others will perform much better.

The good-performing and poor-performing investments ‘cancel each other out’.

Chapter 5: Investing: portfolio theory and the CAPM

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 131

In a well-diversified portfolio, the unsystematic risk is therefore zero. Investors

should therefore not require any additional return to compensate them for

unsystematic risk.

The only risk for which investors should want a higher return is systematic risk.

This is the risk that the market as a whole will perform worse or better than

expected.

In the earlier diagrams showing the efficient frontier of portfolios and the capital

market line, the risk measurement for portfolios on the efficient frontier and the

capital market line is systematic risk only.

Paper P4: Advanced Financial Management

132 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Capital asset pricing model (CAPM)

Systematic risk in securities

The beta factor of a security

Formula for the CAPM

The beta factor of a small portfolio

Alpha factor

Advantages and disadvantages of the CAPM

Using the CAPM for capital investment appraisal

International CAPM

4 Capital asset pricing model (CAPM)

Concepts that are used in portfolio theory can be applied to an analysis of risk in

individual securities, such as the shares of individual companies. The capital asset

pricing model (CAPM) establishes a relationship between investment risk and

expected return for individual securities.

4.1 Systematic risk in securities

Systematic risk is risk that cannot be eliminated by diversifying. Every individual

security, with the exception of risk-free securities, has some systematic risk.

Since investors can eliminate unsystematic risk through diversification in a

portfolio, their only concern should be with the systematic risk of the securities they

hold in their portfolio. The return that they expect to receive should be based on

their assessment of systematic risk, rather than total risk (systematic + unsystematic

risk) in the security.

The systematic risk of a security can be compared with the systematic risk in the

market portfolio as a whole.

A security might have a higher systematic risk than the market portfolio. This

means that when the average market return rises, due perhaps to growth in the

economy, the return from the security should rise by an even larger amount.

Similarly, if the average market return falls due to a deterioration in business

conditions, the return from the security will fall by an even larger amount.

A security might have a lower systematic risk than the market portfolio, so that

when the average market return rises, the return from the security will rise, but

by a smaller amount. Similarly, when the average market return falls, the return

from the security will also fall, but by a smaller amount.

A risk-free security has no systematic risk, because returns on these securities are

unaffected by changes in market conditions.

Chapter 5: Investing: portfolio theory and the CAPM

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 133

4.2 The beta factor (β) of a security

The systematic risk for an individual security is measured as a beta factor. This is a

measurement of the systematic risk of the security, in relation to the systematic risk

of the market portfolio as a whole.

The formula for calculating a security’s beta factor is as follows:

Beta factor of Security S (β

S

) =

S

y

stematic risk of Securit

y

S

Systematic risk of the market as a whole

(The ‘market as a whole’ is the market portfolio.)

There are two ways of re-stating this formula in statistical terms.

Formula 1:

β

S

=

Cov

S,M

σ

M

2

Formula 2:

β

S

=

ρ

S,M

x σ

S

σ

M

where:

Cov

S,M

= the covariance of returns from Security S with the returns from the market

as a whole

σ

M

is the standard deviation of returns for the market portfolio

σ

S

is the standard deviation of returns for Security S

ρ

S,M

is the correlation coefficient for returns from Security S with returns from the

market as a whole.

Example

The annual returns on shares in Company Z have a standard deviation of 3.58% and

the standard deviation of market returns is 2.72%. The correlation coefficient for

returns on shares in Company Z and returns for the market as a whole is + 0.85.

The beta factor for shares in Company Z is:

1.12=

2.72

3.580.85

=

Z

×

β

4.3 Formula for the CAPM

The beta factor for a risk-free security = 0.

The beta factor for the market portfolio = 1.0.

Paper P4: Advanced Financial Management

134 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

When the beta factor for an individual security is greater than 1, the increase or fall

in its expected return (ignoring unsystematic risk) will be greater than any given

increase or decrease in the market return.

When the beta factor for a security is less than 1, the security is relatively low-risk.

The expected increase or decrease in its expected return (ignoring unsystematic risk)

will be less than any given increase or decrease in the market return.

The formula for the capital asset pricing model is used to calculate the expected

return from a security (ignoring unsystematic risk).

R

S

= R

RF

+ β

S

(R

M

– R

RF

)

where:

R

S

is the expected return from a security S

R

RF

is the risk-free rate of return

R

M

is the expected market return

β

S

is the beta factor for security S.

(This formula is similar to the formula for the capital market line. It is important,

and you need to learn it.)

The expected return from an individual security will therefore vary up or down as

the return on the market as a whole goes up or down. The size of the increase or fall

in the expected return will depend on:

the size of the change in the returns from the market as a whole, and

the beta factor of the individual security.

Example

The risk-free rate of return is 4% and the return on the market portfolio is 8.5%.

What is the expected return from shares in companies X and Y if:

the beta factor for company X shares is 1.25

the beta factor for company Y shares is 0.90?

Answer

Expected return, security X = 4% + 1.25(8.5 – 4)% = 9.625%.

Expected return, security Y = 4% + 0.90(8.5 – 4)% = 8.05%.