ACCA P2 (INT) Corporate Reporting - Study text - 2010 (Emile Woolf)

Подождите немного. Документ загружается.

Practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 563

Required

(a) Discuss why there is a need to disclose diluted earnings per share.

(b) Calculate the diluted EPS according to IAS 33 Earnings per Share from the

following information for X, a company whose shares are traded on a stock

market.

Accountingdatayearended31MayYear6:

Netprofitaftertaxandnon‐controllinginterest $18,000,000

Ordinarysharesof$1(fullypaid) 40,000,000

Averagefairvalueforyearofordinaryshares

$1.50

(1) Share options have been granted to directors giving them the right to

subscribe for ordinary shares between Year 7 and Year 9 at $1.20 per

share. There were 2,000,000 options outstanding at 31 May Year 6.

(2) The company has $20 million of 6% convertible bonds in issue: The

terms of conversion of the bonds per $250 nominal value of bond at the

date of issue (1 May Year 0) were:

31 May 2 Year 6 24 shares

31 May Year 7 23 shares

31 May Year 8 22 shares.

None of the bonds have as yet been converted.

(3) There are 1,600,000 convertible preference shares in issue. The

cumulative dividend is ten cents per share and each preference share

can convert into two ordinary shares. The preference shares can be

converted in Year 8.

(4) Assume a tax rate of 33%.

(c) Discuss the nature of the diluted EPS calculation in (b) where the order of the

dilutive effects is ignored.

(d) Discuss the view that the basic EPS should be based upon not only existing

issued shares but also on other shares which are in substance ‘share

equivalents’ and have a dilutive effect on the basic EPS.

25 Universal Solutions

(a) Explain the following as used in IAS 19 Employee Benefits:

(i) The term ‘defined benefit pension plan’

(ii) The basis to be adopted in measuring scheme assets

(iii) The basis to be adopted in measuring scheme liabilities

(iv) Actuarial gains and losses.

(b) Universal Solutions operates a defined benefit pension scheme on behalf of its

employees. The company conducts an annual review of funding in

conjunction with their actuaries who have supplied the following information:

Paper P2: Corporate reporting (International)

564 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

At 31 Dec

Year 3

At 31 Dec

Year 4

$

$

Present value of pension fund obligations 1,000

1,200

Market value of pension fund assets 1,000

1,150

Information relevant to the actuarial valuation:

Expected return on plan assets 8%

Discount rate used to determine pension fund liabilities 12%

Current service cost $100

Contributions to the pension fund $140

Benefits paid out amounted to $95

Required

(i) Calculate the charge to profit or loss for the year to 31 December Year 4.

(ii) Compute the amount of the pension surplus or deficit in the statement of

financial position as at 31 December Year 4

(iii) Compute any actuarial gain or loss as at 31

December Year 4 and explain the

available accounting treatments of such a gain or loss.

(iv) Describe proposals by the IASB to change the permitted methods of accounting

for actuarial gains or losses.

26 IFRS 2

(a) IFRS 2 requires an entity to recognise share-based payment transactions in its

financial statements. These include transactions with the employees or other

parties where they are to be settled in cash, other assets or equity instruments

of the entity.

The IFRS identifies three types of share-based payment transaction and sets

out the measurement principles and specific requirements for each.

Required

(i) Suggest why accounting standard setters felt that there was a need for a

standard in this area.

(ii) Identify and briefly explain the three types of share based payments

recognised by IFRS 2.

(b) A client of your firm, a listed company with a 31 December year end, contacts

you for advice on a proposed share option scheme for its employees.

On 1 January Year 5, the client granted 100 options to each of its 500

employees. The grant is conditional upon the employee working for the client

over the next three years. At the grant date, it is estimated that the fair value

of each option is $15.

Practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 565

Calculate the expense in profit or loss for each year of the vesting period .

(i) Assuming that the client’s expectations throughout the vesting period are that

all options will vest.

(ii) And, alternatively, assuming that the client’s best estimates of the proportion

of options that will vest are as follows:

Estimate at 31 December Year 5 85%

Estimate at 31 December Year 6 88%

And that 44,300 options actually vest at 31 December Year 7.

27 The Lucky Dairy

The Lucky Dairy, a company whose shares are traded in the stock market, produces

milk for supply to various customers. It produces 25% of the country’s milk

consumption. The company owns 150 farms and has stock of 70,000 cows and 35,000

heifers (young female cows) which are being raised to produce milk in the future.

The farms produce 2.5 million kilograms of milk per annum and normally hold an

inventory of 50,000 kilograms of milk.

Extracts from the draft accounts to May 20X2 shows that the herd consists of:

70,000 three year old cows (purchased on or before 1June 20X1)

25,000 heifers, average age one a half years old (purchase 1 December 20X1)

10,000 heifers, average age two years old (purchased 1 June 20X1)

There were no animals born or sold in the year.

The per unit values minus estimate point of sale costs were as follows:

1June20X1 31May20X2

2yearoldanimal

$50 $55

1yearoldanimal $40* $42

3yearoldanimal

$60

1½yearoldanimal

$46

* $40 was also the value at 1 December 20X1

The company has had a difficult year in financial and operating terms. The cows

had contracted a disease at the beginning of the year which had been passed on in

the food chain to a small number of consumers. The publicity surrounding the event

had caused a drop in the consumption of milk and as a result the dairy was holding

500,000 kilograms of milk in storage.

The government had stated on 1

April 20X2 that it was prepared to compensate

farmers for the drop in the price and consumption of milk. An official government

letter was received 6 June 20X2, stating that $1.5 million will be paid to Lucky on 1

August 20X2. Additionally, on 1

May 20X2 Lucky received a letter from its lawyers

saying that legal proceedings had started against the company by the persons

affected by the disease. The company lawyers have advised them that they feel that

Paper P2: Corporate reporting (International)

566 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

it is probable that they will be found liable and that the costs involved may reach

$2million. The lawyers, however, feel that the company may receive additional

compensation from the government if certain quality control procedures have been

carried out by the company. However, the lawyers will only state that the

compensation is possible.

The company’s activities are controlled in three locations: Dale, Shire and Ham. The

only region affected by the disease was Dale and the government has decided that it

is to restrict the milk production of the region significantly. Lucky estimates that the

discounted future cash income from the present herds of cattle in the region

amounts to $1.2 million, taking into account the government restriction order.

Lucky was not sure that the fair value of the cows in the region could be measured

reliably at the date of purchase because of the problems with the diseased cattle. The

cows in this region amounted to 20,000 in number and the heifers 10,000 in number.

All of the animals were purchased on 1

June 20X1.

Lucky has an offer of $1 million for all of the animals in the Dale region (net of

selling costs) and $2 million for the sale of the farms in the region. However, there

was a minority of directors who opposed the planned sale and Board approval was

not achieved until 30 June 20X2.

The directors of Lucky have approached your firm for professional advice on the

above matters.

Required

Advise the directors on how the biological assets and produce of Lucky should be

accounted for under IAS 41 Agriculture, and discuss the implications for the

published financial statements of the above events.

Your answer should include a table which shows the changes in value of the cattle

inventory for the year, split between physical and price changes and showing

separately the valuation of the Dale region. Ignore the effects of taxation.

28 Cohort

Cohort is a private limited company and has two 100% owned subsidiaries, Legion

and Air, both themselves private limited companies. Cohort acquired Air on 1

January 20X2 for $5 million when the fair value of the net assets was $4 million, and

the tax base of the net assets was $3.5 million. The acquisition of Air and Legion was

part of a business strategy whereby Cohort would build up the value of the group

over a three-year period and then list its share capital on the Stock Exchange.

(a) The following details relate to the acquisition of Air, which manufactures

electronic goods:

(i) Part of the purchase price has been allocated to intangible assets because

it relates to the acquisition of a database of key customers of Air. The

recognition and measurement criteria for an intangible asset under IFRS

3 Business Combinations and IAS 38 Intangible Assets do not appear to

have been met but the directors feel that the intangible asset of $500,000

will be allowed for tax purposes and have computed the tax provision

Practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 567

accordingly. However, the tax authorities could possibly challenge this

opinion.

(ii) Air has sold goods worth $3 million to Cohort since acquisition and

made a profit of $1 million on the transaction. The inventory of these

goods recorded in Cohort’s statement of financial position at the year

ending 31May 20X2 was $1.8 million.

(iii) The retained earnings of Air at acquisition were $2 million. The directors

of Cohort have decided that, during the three years leading up to the

date that they intend to list the shares of the company, they will realise

earnings through future dividend payments from the subsidiary

amounting to $500,000 per year. Tax is payable on any remittance of

dividends and no dividends have been declared for the current year.

(b) Legion was acquired on 1 June 20X1 and is a company which undertakes

various projects ranging from debt factoring to investing in property and

commodities. The following details relate to Legion for the year ending 31

May 20X2:

(i) Legion has a portfolio of readily marketable government securities

which are held as current assets. These investments are stated at market

value in the statement of financial position with any gain or loss taken to

profit or loss. These gains and losses are taxed when the investments are

sold. Currently the accumulated unrealised gains are $4 million.

(ii) Legion has calculated that it requires a general allowance of $2 million

against its total loan portfolio. Tax relief is available when the specific

loan is written off. Management feel that this part of the business will

expand and thus the amount of the general provision will increase.

(iii) When Cohort acquired Legion it had unused tax losses brought forward.

At 1 June 20X1, it appeared that Legion would have sufficient taxable

profit to realise the deferred tax asset created by these losses but

subsequent events have proven that the future taxable profit will not be

sufficient to realise all of the unused tax loss.

Impairment of goodwill is not allowed as a deduction in determining taxable profit.

Required

Write a note suitable for presentation to the partner of an accounting firm setting

out the deferred tax implications of the above information for the Cohort Group of

companies.

29 Reporting performance

“It is essential to ensure that financial and other relevant information is

communicated in a manner which can be understood by the recipients of corporate

reports. In addition, it is of the utmost importance that corporate reporting does not

become over-burdened with unnecessary detail and that the costs of collecting and

publishing the information are kept within reasonable bounds.”

Paper P2: Corporate reporting (International)

568 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Required

Explain the reasoning behind this statement and its implications for present day

financial reports of listed companies.

30 Rowsley

Rowsley is a diverse group with many subsidiaries. The group is proud of its

reputation as a ‘caring’ organisation and has adopted various ethical policies

towards its employees and the wider community in which it operates. As part of its

Annual Report, the group publishes details of its environmental policies, which

include setting performance targets for activities such as recycling, controlling

emissions of noxious substances and limiting use of non-renewable resources.

The finance director is reviewing the accounting treatment of various items prior to

finalising the accounts for the year ended 31

March 20X4. All items are material in

the context of the accounts as a whole. The accounts are due to be approved by the

directors on 30

June 20X4.

Closure of factory

On 15 February 20X4, the board of Rowsley decided to close down a large factory in

Derbytown. The board is trying to draw up a plan to manage the effects of the

reorganisation, and it is envisaged that production will be transferred to other

factories. The factory will be closed on 31 August 20X4, but at 31 March 20X4 this

decision had not yet been announced to the employees or to any other interested

parties. Costs of the reorganisation have been estimated at $45 million

Relocation of subsidiary

During December 20X3, one of the subsidiary companies moved from Buckington to

Sundertown in order to take advantage of government development grants. Its

main premises in Buckington are held under an operating lease, which runs until 31

March 20X9. Annual rentals under the lease are $10 million. The company is unable

to cancel the lease, but it has let some of the premises to a charitable organisation at

a nominal rent. The company is attempting to rent the remainder of the premises at

a commercial rent, but the directors have been advised that the chances of achieving

this are less than 50%.

Legal claim

During the year to 31 March 20X4, a customer started legal proceedings against the

group, claiming that one of the food products that it manufactures had caused

several members of his family to become seriously ill. The group’s lawyers have

advised that this action will probably not succeed.

Environmental impact of overseas subsidiary

The group has an overseas subsidiary that is involved in mining precious metals.

These activities cause significant damage to the environment, including

deforestation. The company expects to abandon the mine in eight years time. The

Practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 569

mine is situated in a country where there is no environmental legislation obliging

companies to rectify environmental damage and it is very unlikely that any such

legislation will be enacted within the next eight years. It has been estimated that the

cost of cleaning the site and re-planting the trees will be $25 million if the re-

planting was successful at the first attempt, but it will probably be necessary to

make a further attempt, which will increase the cost by a further $5 million.

Required

Explain how each of the items above should be treated in the consolidated financial

statements for the year ended 31

March 20X4

31 Engina

Engina, a foreign company has approached a partner in your firm to assist in

obtaining local stock exchange listing (or stock market registration) for the

company. Engina is registered in a country where transactions between related

parties are considered to be normal but where such transactions are not disclosed.

The directors of Engina are reluctant to disclose the nature of their related party

transactions as they feel that although they are a normal feature of business in their

part of the world, it could cause significant problems politically and culturally to

disclose such transactions.

The partner in your firm has requested a list of all transactions with parties

connected with the company and the directors of Engina have produced the

following summary:

(a) Every month, Engina sells $50,000 of goods per month to Mr Satay, the

financial director. The financial director has set up a small retailing business

for his son and the goods are purchased at cost price for him. The annual

turnover of Engina is $300 million. Additionally, Mr Satay has purchased his

company car from the company for $45,000 (market value $80,000). The

director, Mr Satay, earns a salary of $500,000 a year, and has a personal

fortune of many millions of pounds.

(b) A hotel property had been sold to a brother of Mr Soy, the Managing Director

of Engina, for $4 million (net of selling cost of $0.2 million). The market value

of the property was $4.3 million but prices have been falling rapidly. The

carrying value of the hotel was $5 million and its value in use was $3.6

million. There was an over-supply of hotel accommodation due to

government subsidies in an attempt to encourage hotel development and the

tourist industry.

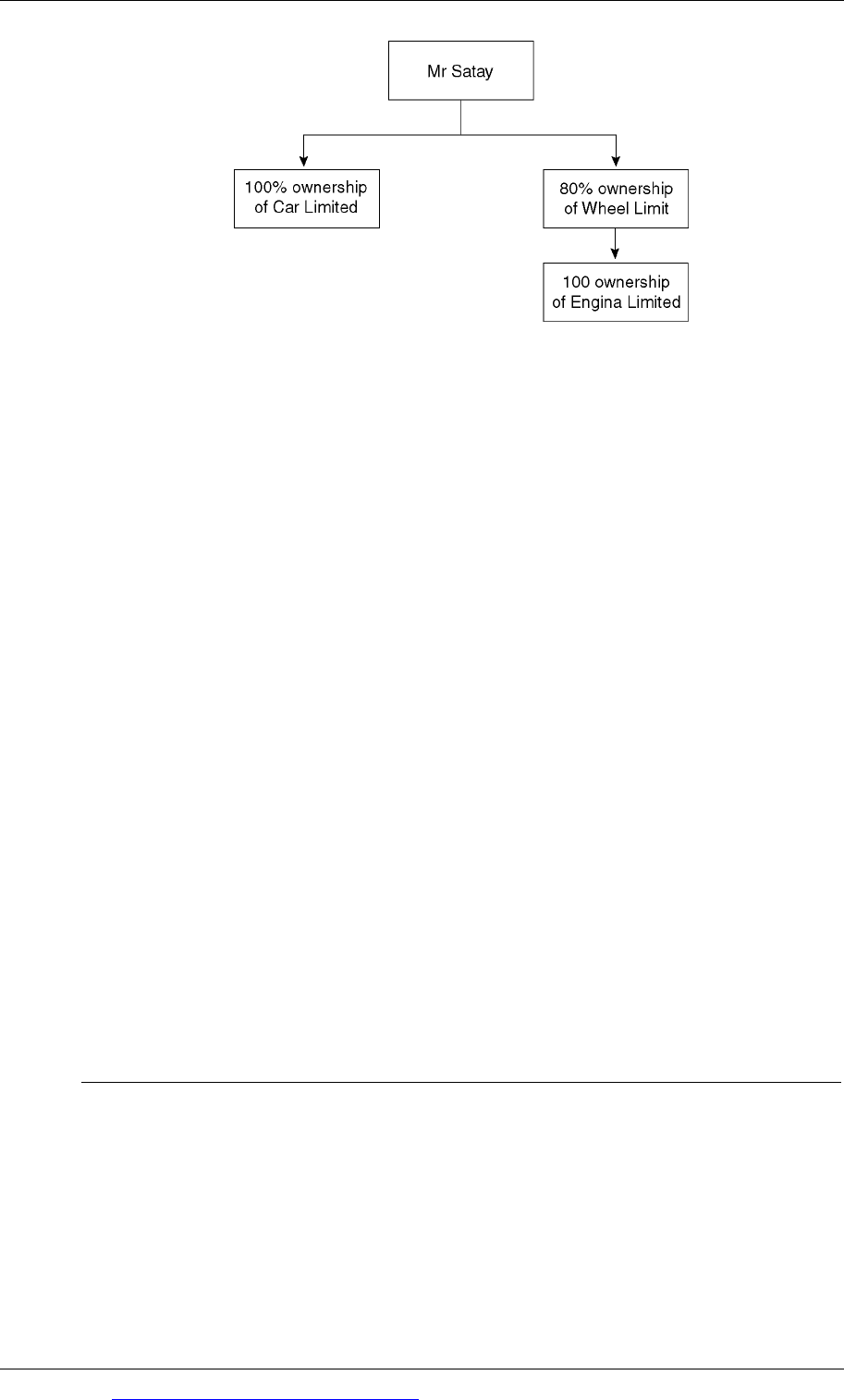

(c) Mr Satay owns several companies and the structure of the group is outlined

below. Engina earns 60% of its profits from transactions with Car and 40% of

its profits from transactions with Wheel. All of the above companies are

incorporated in the same country.

Paper P2: Corporate reporting (International)

570 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Required

Write a report to the directors of Engina setting out the reasons why it is important

to disclose related party transactions and the nature of any disclosure required for

the above transactions under IAS 24 Related Party Disclosures.

32 Property Venture

The directors of Property Venture, a limited liability company, are reviewing their

investment in Exceptional Properties. In 20X3 they had invested $2,476,000 in

Exceptional Properties’ share capital and made a further investment of $6,508,000 in

20X4. They have recently been requested by the directors of Exceptional Properties

to subscribe a further $5,000,000 in 20X5 as new ordinary share capital.

The following documents relating to Exceptional Properties (in draft form) are set

out below:

Statement of group cash flows for the year ended 31 December 20X4 together

with comparative figures for 20X3.

Group income statement for the year ended 31

December 20X4 together with

comparative figures for 20X3.

An analysis of movements on equity reserves attributable to the equity owners

of Exceptional Properties

Notes to the financial statements relating to turnover and profit.

ExceptionalProperties

Groupstatementofcashflowsforyearended31December

20X4 20X3

$000 $000

Cashoutflowfromoperatingactivities

Cashgeneratedfromoperations

(13,805) (7,195)

Interestpaid

(7,090) (3,300)

Incometaxpaid

(336) (494)

–––––––––––––––– ––––

–––––––––––––––– ––––

(21,231) (10,989)

Practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 571

Cashflowsfrominvestingactivities

Dividendsreceivedfromassociate

‐ 10

Interestreceived

300 390

Purchaseofnon‐currentassets

(1,607) (5,650)

Proceedsfromsaleofnon‐currentassets

16,820

Acquisitionofsubsidiary(netofcashacquired)

(7,444) (3,667)

–––––––––––––––– ––––

–––––––––––––––– ––––

8,069 (8,917)

Cashflowsfromfinancingactivities

Equitydividendspaid

(1,318) (628)

Issueofordinarysharecapital

6,508 2,476

Issueofloan

2,456 5,696

Repaymentofloans

(1,064) (5,242)

–––––––––––––––– ––––

–––––––––––––––– ––––

6,582 2,302

–––––––––––––––– ––––

–––––––––––––––– ––––

Decreaseincashandcashequivalents

(6,580) (17,604)

ExceptionalProperties

Groupincomestatementfortheyearended31December

20X4 20X3

$000 $000

Profitbeforetaxation(includingresultsofactivites

Retainedandthosebeingsold)

2,311 3,733

Taxation

(1,558) (784)

–––––––––––––––––––– ––––––––––––––––––––

Profitaftertaxation

753 2,949

–––––––––––––––––––– ––––––––––––––––––––

Profitattributabletonon‐controllinginterests

‐ 482

ProfitattributabletotheequityownersofExceptional

PropertiesGroup

753 2,467

–––––––––––––––––––– ––––––––––––––––––––

753 2,949

–––––––––––––––––––– ––––––––––––––––––––

Reservesanalysis:

20X4 20X3

Retainedprofit:

$000 $000

Profitaftertax

753 2,467

Dividends

(1,698) (768)

–––––––––––––––––––– ––––––––––––––––––––

(945) 1,699

Paper P2: Corporate reporting (International)

572 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Otherreservemovementsduringtheperiod:

Revaluationreserve

5,612 171

Other

370 (47)

–––––––––––––––––––– ––––––––––––––––––––

Increaseinreserves

5,037 1,823

–––––––––––––––––––– ––––––––––––––––––––

Notes forming part of the financial statements

(1) Turnover

20X8 20X7

Analysedbyoperatingsegment

$000 $000

Activitiesbeingretained:

Constructionandhousebuilding

86,603 61,710

Overseaspropertydevelopment

6,349 2,383

Engineering

8,647‐

TownHouseServices

10,763‐

–––––––––––– ––––––––––––

112,362 64,093

Activitiesbeingsold:

Propertydevelopmentandrentals

8,614 4,506

–––––––––––– ––––––––––––

120,976 68,599

–––––––––––– ––––––––––––

(2) Profit before taxation is stated after charging or crediting:

(a) Nettradingexpenses:

Changeinworkinprogressandownworkcapitalised

(4,575) (22,226)

Rawmaterialsandconsumables

42,819 28,990

Otherexternalcharges

55,779 44,095

Staffcosts

17,317 8,827

Depreciationandotheramounts

Written offtangibleassets

1,013 539

Otheroperatingcharges

4,006 4,554

–––––––––––– ––––––––––––

116,359 64,779

–––––––––––– ––––––––––––

(b) Shareofprofits/(losses)ofassociates (412) 47

(c) Incomeandprofits/(losses)fromnon‐currentasset

investmentsotherthanassociates

(173) 64

(d)Interestreceivableandsimilarinco me

335 383

(e) Interestpayableandsimilarcharges: