ACCA P2 (INT) Corporate Reporting - Study text - 2010 (Emile Woolf)

Подождите немного. Документ загружается.

Answers

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 583

P has an 80% interest in S1 and a 66% interest in S2. The non-controlling interest is

20% in S1 and 34% in S2. These percentages should be used in the consolidation

process, when the one-stage method is used..

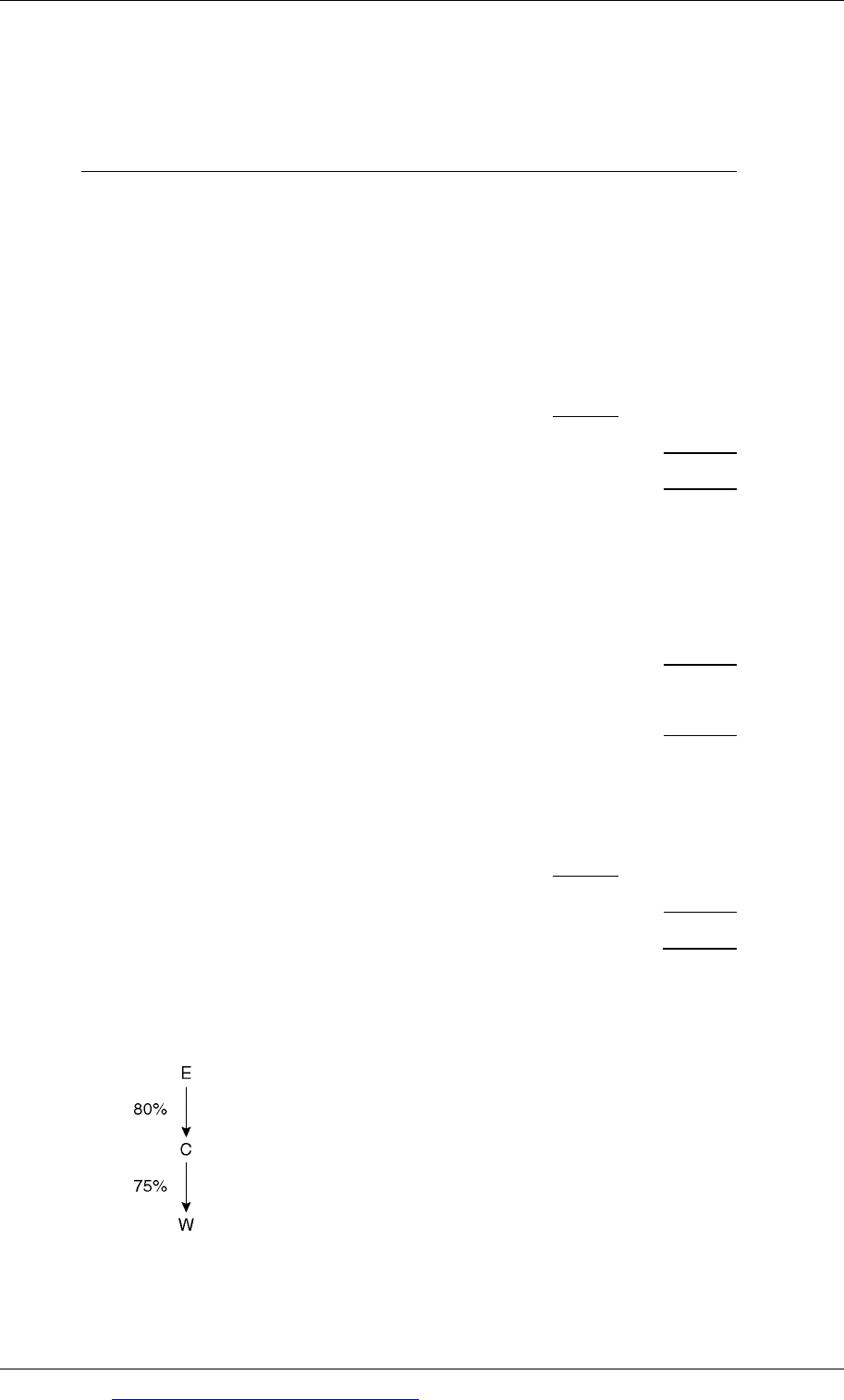

5 H, S and T

There is a vertical group structure. S joined the group on 1 January Year 2 and T

joined the group at a later date, 1 January Year 3.

Step 1

Calculate the percentage ownership of the subsidiaries held by H and the

percentage ownership of the non-controlling interests.

H acquired 80% of the shares of S (160,000/200,000)

S acquired 70% of the shares of T (35,000/50,000)

OwnershipofS

DirectholdingofH 80%

Non‐controllinginterestinS(balancingfigure) 20%

100%

OwnershipofT

Indirectholding(80%×70%) 56%

Non‐controllinginterestinT(balancingfigure)

44%

100%

Step 2

Calculate the net assets of S and T at (1) the end of the current reporting period and

(2) the date of acquisition by the group.

At31

December

Year6

Atacquisition

date

Post‐acquisition

accumulatedprofits

$000 $000 $000

EntitySnetassets 630 480 150

EntityTnetassets

250 150 100

PaperP2: Corporate reporting (International)

584 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Step 3

Calculate the non-controlling interest

$

Non‐controllinginterestinnetassetsofS

20%×630 126.0

Non‐controllinginterestinnetassetsofT 44%×250 110.0

236.0

Subtract

Costofindirectnon‐controllinginterestinT 20%×109 (21.8)

(20%×CostofinvestmentbySinT)

Non‐controllinginterestinHGroup

214.2

Step 4

Calculate the purchased goodwill.

To do this, we must first calculate the cost of the parent company’s investment in

Entity T.

$000

CostofinvestmentofSinT

109.0

Costofindirectnon‐controllinginterestinT(seeabove) (21.8)

Costofparent’sinvestmentinT

87.2

InvestmentinS

InvestmentinT

$000

$000

Costofinvestment 444 (seeabove) 87.2

Minusshareofnetassetsacquired:

80%×480 384

56%×150

84.0

Purchasedgoodwill

60

3.2

Total purchased goodwill for the group (in $000) before impairment = 60 + 3.2 =

63.2. There has been impairment of $26,000, so the purchased goodwill in the

consolidated statement of financial position is $63,200 - $26,000 = $37,200.

Answers

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 585

Step 5

Calculate the post-acquisition accumulated profits of the parent company.

$000

EntityHaccumulatedprofits(parentcompany)

500

Parent’sshareof:

EntitySaccumulatedprofits(80%×150)–seeStep2

120

EntityTaccumulatedprofits(56%×100)–seeStep2

56

676

Accumulatedimpairmentofgoodwill (26)

650

Consolidated statement of financial position at 31

DecemberYear6

$000

Goodwill(Step4)

37.2

Sundrynetassets(256+521+250) 1,027.0

1,064.2

Sharecapital 200.0

Reserves(Step5)

650.0

Parentcompany’sshareinequityofthegroup

850.0

Non‐controllinginterests(Step3) 214.2

1,064.2

6 Disposal

$

million

$

million

Considerationfromsaleofshares

960

FairvalueofretainedsharesinSpool

100

1,060

NetassetsofSpoolatcarryingvalue 800

Minus:non‐controllinginterestde‐recognised(10%×800) (80)

720

Gainonsaleofshares

340

PaperP2: Corporate reporting (International)

586 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

None of the assets of Spool have been re-valued, therefore there is no balance on a

revaluation reserve; therefore none of this gain should be transferred directly to

retained earnings and not reported in profit or loss.

There is no information to suggest that a reclassification adjustment is required to

reclassify income previously reported as other comprehensive income as profit or

loss.

The total gain of $340 million on disposal of the shares should therefore be

recognised in profit or loss for the period.

Hoo will recognise an investment in Spool in its statement of financial position in

accordance with the requirements of IAS 39. On initial recognition, this investment

should be valued at $100 million.

7 Step acquisiton and partial disposal

(a) The profits of AS since the investment was acquired (all retained) are $40

million (= $300m – $260m). During this period, HH held 25% of the equity of

AS and it is assumed that AS is an associate. Profits attributable to H for the

year are therefore $10 million (= 25% × $40 million).

$ million

Initial investment in associate at cost 80

Share of post-investment retained profits 10

90

Fair value of investment at 30 June 95

Gain recognised when step acquisition occurs 5

The total gain/profit recognised for the year from the investment in AS is

therefore $10 million + $5 million = $15 million.

Goodwill

$ million

Fair value of investment in 25% of AS 95

Cost of additional 40% of shares 160

255

H share of net assets of AS at 30 June (65% × 300)

195

Goodwill attributable to owner of H 60

Goodwill attributable to non-controlling interests 15

Total goodwill 75

$ million

Fair value of investment in 25% of AS (35% × 300)

105

Goodwill attributable to non-controlling interests 15

Total NCI 120

(b) The disposal of 10% of the shares in S leaves P with a controlling interest;

therefore the disposal of the shares should be accounted for as an equity

Answers

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 587

transaction between owners of the group. No gain or loss is recognised in the

consolidated financial statements of P.

It is assumed that the profits of S for the year were $200 million (all retained;

therefore $900 million - $700 million). At 30 June it is assumed that profits for

the year to date were $100 million (= $200 million × 6/12); therefore the net

assets of S at this date were $800 million.

P NCI

$m $m

Before the share sale

(80% × 800)

640 (20%) 160

After the share sale (70%)

560 (30%) 240

Change in interest in S - 80 + 80

The shares were sold for $94 million adding to the assets in P’s statement of

financial position. The transaction should therefore be accounted for in equity

as follows:

Debit: Cash $94 million

Credit: NCI $80 million

Credit: Reserves attributable to P (= gain = balance) $14 million

$ million $ million

Post-acquisition profit attributable to S (see above) 200

Less: Impairment of goodwill (8)

Recognised profit 192

Attributable to equity owners of P

1 January – 30 June (80% × 200 × 6/12)

80

1 July – 31 December (70% × 200 × 6/12)

70

Goodwill impairment (8)

Attributable to NCI 142

1 January – 30 June (20% × 200 × 6/12)

20

1 July – 31 December (30% × 200 × 6/12)

30

50

192

PaperP2: Corporate reporting (International)

588 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

8 The Edgeley Group

Consolidated statement of financial position at 31

December Year 4

ASSETS

$m

$m

Non‐currentassets

Intangible:Goodwill(652+148(W3)

800

Tangible(1,840+863+520)

3,223

Currentassets

Inventory(350‐20unrealisedprofit+212+108)

650

Receivables(213+127+82)

422

Bank(234+26+19)

279

1,351

TOTALASSETS

5,374

EQUITYANDLIABILITIES

Equity

Ordinarysharecapital

500

Accumulatedprofits(W5)

3,737

EquityattributabletoownersofEdgeley

4,237

Non‐controllinginterest(W6)

446

Totalequity

4,683

Currentliabilities

Tradepayables(262+151+92)

505

Taxationpayable(112+47+27)

186

691

TOTALEQUITYANDLIABILITIES

5,374

Workings

(1) Group structure

80 × 75 = 60% indirectly held by E in W.

NCI = 40%

Answers

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 589

Consolidation adjustments

(2) Intra-group trading

Cost

100%

Mark‐up

40%

Intra‐groupsalesprice

140%

Unrealised profit in inventory still held

25% × 280 ×

40

/

140

= 20

Consolidation adjustment:

DR Reserves account of Cheadle 20

CR Inventory 20

(3) Goodwill

Cheadle Wilmslow

$000

$000

Costofinvestment 1,452

500

Minusindirectholdingadjustment(20%x500)

(100)

Minusgroupshareofthefairvalueofnetassetsat

acquisitionasrepresentedbythepre‐acquisition

sharecapitalandreserves:

80%×1000(200+800) (800)

60%×420(100+320)

(252)

Goodwill

652

148

(4) Cheadle’s revised reserves

$000

Asgiveninthequestion

1,330

Minusunrealisedprofitincludedininventory(W2) (20)

Adjustedreserves

1,310

(5) Consolidated reserves

$000

Edgeley

3,215

Plusgroupshareofthepost‐acquisitionprofitsofthe

subsidiaries:

Cheadle:80%(1,310(W4)–800atacquisition)

408

Wilmslow:60%(510–320atacquisition)

114

3,737

PaperP2: Corporate reporting (International)

590 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Note: Wilmslow only became a subsidiary of the group when Cheadle was

acquired by Edgeley. Hence the acquisition date for Wilmslow is treated as the

1 January Year 4.

(6) Non-controlling interest

$000

Cheadle:20%(200+1,310(W4)

302

Wilmslow:40%(100+510) 244

Minusindirectholdingadjustment:(20%×500)

(100)

446

9 The A Group

A‘s original investment in C was 90% of C’s 400,000 shares (360,000 shares). During

the year A has disposed of 350,000 of these shares, which reduces the investment

from subsidiary status to that of a ‘simple’ investment.

AGroup

Consolidatedstatementoffinancialpositionasat31DecemberYear4

$000

Goodwill(W2,Bonly) 428

InvestmentinCatfairvalue

44

Othernetassets(W4)

6,661

7,133

Equity

Sharecapital 1,500

AccumulatedprofitsattributabletoownersofA(working1)

5,347

EquityattributabletoownersofA

6,847

Non‐controllinginterest:20%×(1,260+170) 286

Totalequity

7,133

Income statement working schedule for year ended 31 December Year 4

A

B

Group

$000

$000

$000

Operatingprofit 1,200

250

Minus:DividendfromB (16)

nil

1,184

250

1,434

GainondisposalofC(W2) 237

237

Profitbeforetax

1,421

250

1,771

Tax (360)

(60)

(420)

Profitaftertax

1,061

190

1,251

Answers

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 591

Attributableto:

EquityownersofA(1,061+80%×190)

1,213

Non‐controllinginterest:20%×190

38

1,251

Workings

(1) Movement on consolidated reserves attributable to owners of parent

A

B

C

Group

$000

$000

$000

$000

At31DecemberYear3(W5) 3,300

272

612

4,184

ProfitforyearattibutabletoA

1,213

DividendspaidbyA

(50)

At31DecemberYear4

5,347

(2) Disposal of shares in C, with loss of control

Gain to parent

$000 $000

NetassetsofCatdateofdisposal:de‐recognised

1,400

PurchasedgoodwillinCde‐recognised(seeworking3)

472

1,872

Minus:Non‐controllinginterestde‐recognised(10%×1,400) (140)

AssetsattributabletoAde‐recognised

1,732

Fairvalueofinvestmentretained 44

Saleproceeds 1,925

1,969

Totalgainondisposalofshares

237

Since there has been no revaluation of non-current assets and there is no

information about any reclassification adjustments that might be required, it is

assumed that this entire gain should be included in profit or loss for the year.

(3) Calculation of goodwill

B

C

$000

$000

CostofInvestment 1,164

1,120

Less:Groupshareofthefairvalueofthenetassetsat

acquisition

80%×(500+420) (736)

90%×(400+320)

(648)

428

472

PaperP2: Corporate reporting (International)

592 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

(4) Other net assets

$000

A’snetassetsas1JanuaryYear4

2,516

B’snetassetsat1JanuaryYear4 1,260

A’sretainedprofityearended31DecemberYear4

790

B’sretainedprofityearended31DecemberYear4

170

ProceedsofdisposalofC

1,925

6,661

(5) Calculation of post-acquisition retained profits b/fwd attributable to A

$000

A

Asgiveninthequestion 3,300

BandC Groupshareofpost‐acquisition

B80%×(760‐420) 272

C90%×(1,000‐320) 612

Total

4,184

10 Herbert

(a) Memorandum

To: The Managing Director

From: Accountant

Date:

Subject: Exclusion of subsidiaries from consolidation

Sarah

It has been suggested that Sarah should not be included in the consolidated

financial statements for the year ended 31 December Year 4 on the grounds

that the group’s interest in this company may be sold in the near future.

IAS 27 Consolidated financial statements and accounting for investments in

subsidiaries sets out the conditions under which subsidiaries may be excluded

from consolidation. It is quite correct that subsidiaries should not be

consolidated if they are acquired and held exclusively with a view to

subsequent re-sale. However, the group’s shareholding in Sarah does not

come within the definition of an interest held exclusively with a view to

subsequent resale from the time it was acquired.

It was clearly not originally acquired with a view to subsequent re-sale. Even

if a purchaser had been identified, the definition would still not be met.

Therefore Sarah must be included in the consolidated financial statements

until a disposal actually takes place.