ACCA P2 (INT) Corporate Reporting - Study text - 2010 (Emile Woolf)

Подождите немного. Документ загружается.

Practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 533

Reporting performance, post balance sheet events,

provisions, contingencies, related party

disclosures

29 Reportingperformance 567

30 Rowsley 568

31 Engina 569

32 PropertyVenture 570

Performance measurement

33 TimberProducts 573

Paper P2: Corporate reporting (International)

534 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

1 Environmental reporting

(a) “Just as the corporate report now includes a statement on corporate

governance, perhaps in the future a statement of environmental cost or

expenditure could be disclosed, in order to avoid suggestions that a company

may not be showing the full cost to society of its operations, and that the lack

of accounting rules for environmental items penalises the environmentally

responsible business.” Alan Pizzey February 1998

Required

You are required to provide suggestions of information that might be

disclosed in an environmental report.

(b) At a manufacturing site, $8million must now be spent to reduce pollution,

because new local laws have been introduced. The cost of legal damages

against the company for pollution that it has caused in the past total $5million.

Required

Discuss the required accounting treatment of these costs.

2 P and Q

Company P, a parent company, owns one third of the ordinary shares of Company

Q, a jointly-controlled entity. Company P uses the proportionate consolidation

method in respect of its interest in Company Q.

During the current reporting period, Company P made a loan to Company Q of

$600,000.

Which of the following treatments should be adopted in the consolidated statement

of financial position of the Company P Group in respect of the loan receivable from

Company Q?

(a) The loan is eliminated on consolidation and will not appear in the

consolidated statement of financial position.

(b) One third of the amount of the loan is eliminated on consolidation and the

remainder ($400,000) appears in the consolidated statement of financial

position as a loan receivable from the venture.

(c) The full amount ($600,000) appears in the consolidated statement of financial

position as a loan receivable from the venture.

(d) The full amount of the loan is reported in the consolidated statement of

financial position as an addition to the cost of the investment in the venture.

Practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 535

3 P, S and A

The statements of financial position of three entities P, S and A are shown below, as

at 31 December Year 5. However, the statement of financial position of P records its

investment in Entity A incorrectly. The investment in A is shown at cost, instead of in

accordance with the equity method of accounting and the requirements of IAS 28.

P S A

$ $ $

Non‐currentassets

Property,plantandequipment 450,000 240,000 460,000

InvestmentinSatcost

320,000 ‐ ‐

InvestmentinAatcost

140,000 ‐ ‐

–––––––––––––––––– –––––––––––––––––– –––––––––––––––––

–

910,000 240,000 460,000

Currentassets

Inventory 70,000 90,000 70,000

CurrentaccountwithP

‐ 60,000 ‐

CurrentaccountwithA

20,000 ‐ ‐

Othercurrentassets

110,000 130,000 40,000

–––––––––––––––––––––– –––––––––––––––––– –––––––––––––––––

–

Totalassets 1,110,000 520,000 570,000

––––––––––––––––––––––– –––––––––––––––––– –––––––––––––––––

–

Equityandreserves

Equitysharesof$1 100,000 200,000 100,000

Sharepremium

160,000 80,000 120,000

Accumulatedprofits

650,000 140,000 250,000

–––––––––––––––––– –––––––––––––––––– –––––––––––––––––

–

910,000 420,000 470,000

Long‐termliabilities

40,000 20,000 30,000

Currentliabilities

CurrentaccountwithP ‐ ‐ 20,000

CurrentaccountwithS

60,000 ‐ ‐

Othercurrentliabilities

100,000 80,000 50,000

––––––––––––––––––––––– –––––––––––––––––– –––––––––––––––––

–

1,110,000 520,000 570,000

––––––––––––––––––––––– –––––––––––––––––– –––––––––––––––––

–

Additional information

P bought 150,000 shares in S several years ago when the fair value of the net

assets of S was $340,000.

P bought 30,000 shares in A several years ago when the fair value of A’s net

assets was $370,000.

There has been no change in the issued share capital or share premium of either

S or A since P acquired its shares in them.

Paper P2: Corporate reporting (International)

536 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

There has been impairment of $20,000 in the goodwill relating to the investment

in S, but no impairment in the value of the investment in A.

At 31 December Year 5, A holds inventory purchased during the year from P

which is valued at $16,000 and P holds inventory purchased from S which is

valued at $40,000. Sales from P to A and from S to P are priced at a mark-up of

one-third on cost.

None of the entities has paid a dividend during the year.

P uses the partial goodwill method to account for goodwill and no goodwill is

attributed to the non-controlling interests in S.

Required

Prepare the consolidated statement of financial position of the P group as at 31

December Year 5.

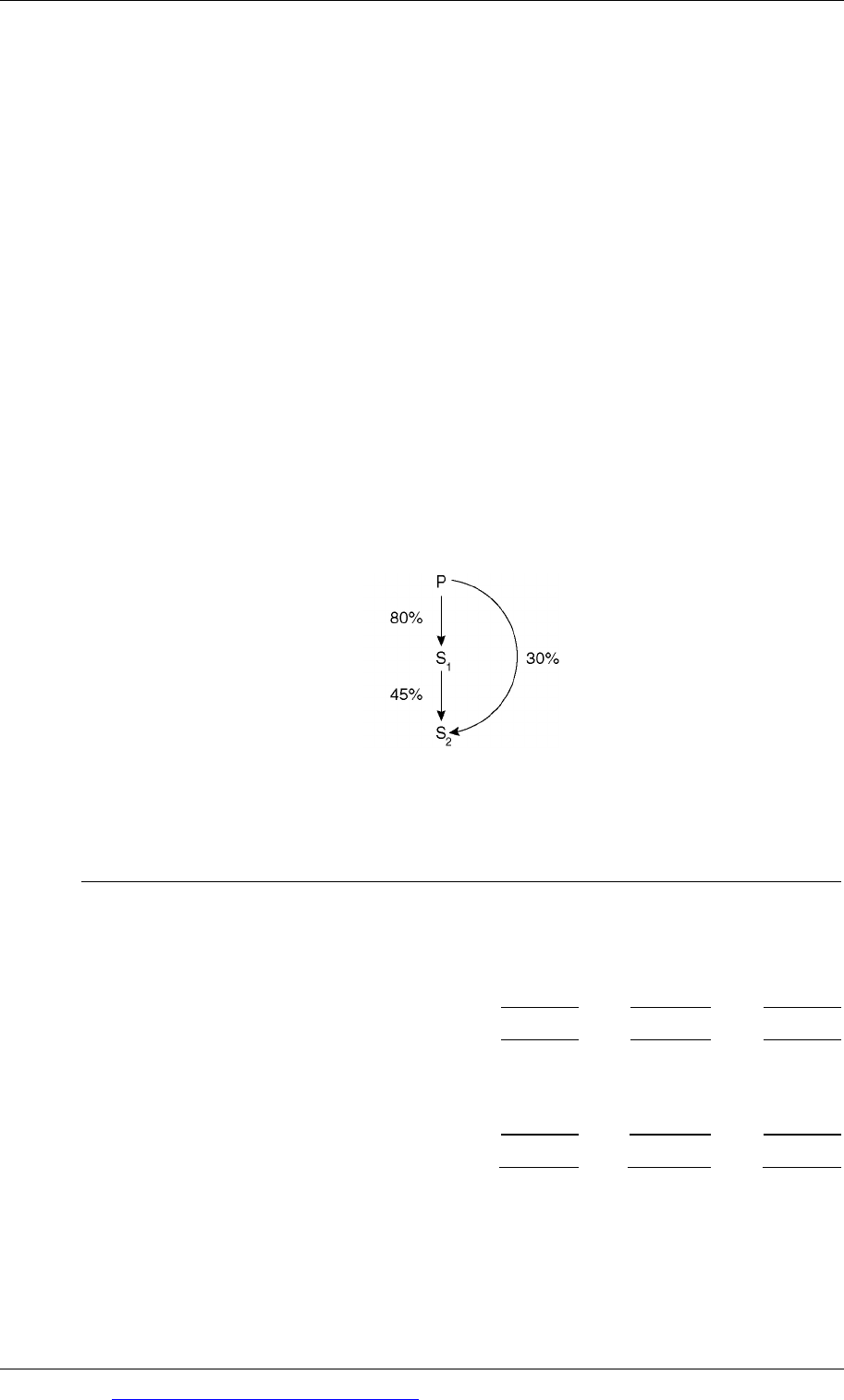

4 Group and NCI

Calculate the group interest and the non-controlling interest in the two subsidiaries,

S1 and S2, in the group shown below, for use in the one-stage method of

consolidation for complex groups.

5 H, S and T

The summary statements of financial position of Entity H, Entity S and Entity T as at

31 December Year 6 are as follows:

EntityH

EntityS

EntityT

$000

$000

$000

InvestmentinSatcost 444

‐

‐

InvestmentinTatcost

‐

109

‐

Sundrynetassets

256

521

250

700

630

250

Sharecapital:ordinarysharesof$1each 200

200

50

Accumulatedprofits

500

430

200

700

630

250

Entity H acquired 160,000 shares of Entity S on 1 January Year 2, when the net assets

of S were $480,000. Entity S acquired 35,000 shares in Entity T on 1 January Year 3,

when the net assets of T were $150,000.

The accumulated impairment of the goodwill arising on the acquisition of the shares

in S is $26,000.

Practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 537

Required

Prepare the consolidated statement of financial position for the H group as at 31

December Year 6. The H Group uses the partial goodwill method to account for

acquisitions and no goodwill is attributed to the non-controlling interests in S or T.

6 Disposal

At 31 December Year 1, Hoo owned 90% of the shares in Spool. At this date the

carrying amount of the net assets of Spool in the consolidated financial statements

of the Hoo Group was $800 million. None of the assets of Spool are re-valued.

On 1 January Year 2, Hoo sold 80% of the equity of Spool for $960 million in cash.

The remaining shares in Spool held by Hoo are estimated to have a fair value of

$100 million.

Required

Explain how the disposal of the shares in Spool should be accounted for in the

consolidated financial statements of the Hoo Group.

7 Step acquisition and partial disposal

(a) On 1 January Year 1, H purchased 25% of the equity of AS for $80 million. H

then acquired an additional 40% of the equity of AS for $160 million on 30

June Year 1. At this date it was estimated that the fair value of the original 25%

shareholding in S was $95 million.

During the year S did not issue any new shares or make any distribution to its

shareholders.

The carrying value of the net assets of AS were as follows:

$ million

At 1 January Year 1 260

At 30 June Year 1 300

H decides to use the fair value method to measure the non-controlling

interests, and estimates that the value of goodwill in AS attributable to the

non-controlling interest at 30 June Year 1 is $15 million.

The financial year of H ends on 30 June.

Required

For the consolidated financial statements of H for the year to 30 June Year 1,

state:

(i) the total gain or profit attributable to the investment in AS for the year

(ii) total amount of goodwill arising with the acquisition

Paper P2: Corporate reporting (International)

538 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

(iii) the value of the non-controlling interest in AS.

(b) On 1 January Year 2, P acquired 80% of the equity of S for $620 million in cash.

On 30 June Year 2 it sold 10% of the equity in S for $94 million. S did not issue

any shares or make any distribution to its shareholders in the year to 31

December Year 2. P uses the partial goodwill method to account for the

acquisition of S and no goodwill is attributed to the non-controlling interest.

The net assets of S were as follows, at carrying value:

$ million

At 1 January Year 2 700

At 31 December Year 2 900

At 31 December Year 2, P carries out an impairment review and decides that

the goodwill in its investment in S has been impaired by $8 million.

Required

(i) Explain how the disposal of the shares in S should be accounted for.

(ii) From the information given above, show much profit or loss would be

recognised in the consolidated statement of comprehensive income for

the year to 31 December Year 2, and how much of this is attributable to

the equity owners of P.

8 The Edgeley Group

You are provided with the following information relating to the Edgeley Group of

companies.

(1) On 1 January Year 4, Edgeley acquired 80% of the ordinary share capital and

voting rights of Cheadle.

(2) Cheadle had acquired 75% of the ordinary share capital and voting rights of

Wilmslow on 1 January Year 2.

(3) The summarised statements of financial position of these three companies at

31 December Year 4 were as follows:

Edgeley

Cheadle Wilmslow

$m

$m

$m

Property,plantandequipment 1,840

863

520

InvestmentinSubsidiary(atcost)

1,452

500

‐

Inventory

350

212

108

Receivables

213

127

82

Bank

234

26

19

4,089

1,728

729

Practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 539

Tradepayables 262

151

92

Taxationpayable

112

47

27

Ordinarysharecapital

500

200

100

Accumulatedprofits

3,215

1,330

510

4,089

1,728

729

(4) At acquisition the following information was known:

Company

Date Ordinarysharecapital Retainedprofit

$m $m

Cheadle 1JanuaryYear2 200 560

Cheadle

1JanuaryYear4 200 800

Wilmslow

1JanuaryYear2 100 240

Wilmslow

1JanuaryYear4 100 320

(5) During Year 4 the following intra-group trading took place:

Selling

company

Buying

company

Salesattransfer

price

Profiton

sales

Cheadle

Edgeley $280m 40%oncost

25% of these transfers are held as inventory at 31 December Year 4

Required

Prepare the consolidated statement of financial position of the Edgeley Group at 31

December Year 4. Edgeley uses the partial goodwill method to account for all

acquisitions and no goodwill is attributable to non-controlling interests.

9 The A Group

The summarised statements of financial position of A and its two subsidiaries B and

C at 31 December Year 3 are shown below:

Summarised statements of financial position at 31 December Year 3

A

B

C

$000

$000

$000

Investmentinsubsidiaries:

B

1,164

C

1,120

Othernetassets

2,516

1,260

1,400

4,800

1,260

1,400

Paper P2: Corporate reporting (International)

540 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Ordinarysharecapital

($1shares)

1,500

500

400

Accumulatedprofits

3,300

760

1,000

4,800

1,260

1,400

The summarised income statements for A and B for the year ended 31 December

Year 4 are as follows:

A B

$000 $000

Profitbeforetax 1,200 250

Taxation

(360) (60)

––––––––––––– –––––––––––––

Profitaftertax

840 190

Dividendspaid

(50) (20)

––––––––––––– –––––––––––––

Retainedprofitforyear

790 170

Retainedprofitatstartofyear

3,300 760

––––––––––––– –––––––––––––

Retainedprofitsatendofyear

4,090 930

––––––––––––– –––––––––––––

Additional information:

(i) A acquired 80% of the ordinary share capital of B on 1 January Year 0 when

the reserves of B were $420,000.

(ii) A acquired 90% of the ordinary share capital of C on 1January Year 1 when

the reserves of C were $320,000.

(iii) On 1 January Year 4, A disposed of 350,000 shares in C for $1,925,000. This

transaction has not yet been accounted for by A. The remaining investment in

shares of C at this date had a fair value of $44,000.

(iv) There were no changes in the issued share capital of the subsidiaries since

acquisition by A.

(v) None of the companies re-value any of their non-current assets.

(vi) The A Group uses the partial goodwill method of accounting for

acquisitions and no goodwill is attributed to non-controlling interests. There

has been no impairment of goodwill.

Required

Prepare A’s consolidated income statement and show the movement on

consolidated equity reserves for the year to 31 December 2 Year 4 and a

consolidated statement of financial position as at that date.

Practice questions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 541

10 Herbert

You are given the following information:

(a) The details of the investments held by Herbert in Sarah and Amanda are as

follows:

Date

Pricepaid

byHerbert

Ordinary

sharecapital

acquired

Retainedprofits

atdateof

acquisition

$000

Sarah 1JanuaryYear0 34,000 80% $10million

Amanda

1JanuaryYear2 10,000 33

1

/3% $5million

(1) Each ordinary share has identical voting rights.

(2) Share capital and retained profits represented the full amount of the

shareholders’ interest at these dates.

(b) The summarised income statements of Herbert, Sarah and Amanda for the

year to 31 December Year 4 were as follows:

Herbert Sarah Amanda

$ʹ000 $ʹ000 $ʹ000

Salesrevenue 290,000 110,000 60,000

Costofsales

(162,000) (51,000) (23,500)

––––––––––––––––– ––––––––––––––––– –––––––––––––––––

Grossprofit 128,000 59,000 36,500

Distributioncosts

(48,800) (12,400) (9,000)

Administrativeexpenses

(16,200) (8,600) (8,000)

Investmentincome

9,000

––––––––––––––––– ––––––––––––––––– –––––––––––––––––

Profitbeforetax 72,000 38,000 19,500

Incometax

(25,000) (12,000) (9,000)

––––––––––––––––– ––––––––––––––––– –––––––––––––––––

Profitaftertax 47,000 26,000 10,500

––––––––––––––––– ––––––––––––––––– –––––––––––––––––

(c) During the year Sarah and Amanda paid dividends to their shareholders of

$10m and $3m respectively.

(d) It is group policy use the partial goodwill method to account for non-

controlling interests, and value non-controlling interests at a proportionate

share of the net assets of the subsidiary. It is also group policy to perform an

impairment review on goodwill at the end of each reporting period.

Paper P2: Corporate reporting (International)

542 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

(e) Details of inter-company trading profits in inventory were as follows:

Transactiondetails

Inventorystillheldas

at

Profitontheinventory

balance$

SarahtoHerbert

1JanuaryYear4 10million

SarahtoHerbert 31DecemberYear4 20million

AmandatoSarah

31DecemberYear4 30million

It is the group’s accounting policy to eliminate the intra-group inventory

profits made by the subsidiary against the profits attributable to both the

owners of the parent company and the non-controlling interests.

(f) Retained profits of Herbert, Sarah and Amanda at 1 January Year 4 were

respectively $106 million, $24 million and $9 million.

(g) The directors of Herbert are currently planning to restructure their

investments. No firm decisions have yet been taken. The two main

possibilities currently under discussion are:

(i) Sale of all or part of the shares in Sarah, which is expected to make

losses in future periods; and

(ii) Acquisition of a 75% interest in Jeremy, which will give Herbert control.

Jeremy operates in the country of Ovonia. Until recently, Ovonian law

required company boards to have a majority of government appointed

nationals and prevented monies from being remitted outside the

country. Some recent administrations have also imposed stringent

controls on cross-border trade. The current administration has repealed

these laws. The political situation in Overonia is extremely unstable,

with frequent changes of government.

The managing director of Herbert is concerned about the impact of these

restructuring proposals on the consolidated financial statements of the group. In

particular, he believes that Sarah should not be included in the consolidated

financial statements for the year ended 31 December Year 4, on the grounds that the

subsidiary is likely to be sold in the near future. He also believes that Jeremy need

not be consolidated as a consequence of the difficulty of obtaining the necessary

information within a reasonable time.

Required

(a) Write a memorandum to the managing director of Herbert, which:

(i) responds to his suggestion that Sarah should not be consolidated;

(ii) explains the conditions under which subsidiary undertakings are

excluded from consolidation and the required accounting treatment for

excluded subsidiary undertakings. You should reach a conclusion on the

appropriate accounting treatment of the proposed investment in Jeremy.

(b) Prepare the consolidated income statement for the Herbert Group for the year

ended 31 December Year 4.